Background

China Sunsine (Sunsine) is the largest producer of rubber accelerators in the world and the largest producer of insoluble sulphur in China. It has a client base of more than 1,000, including two-third of the top 75 global tyre manufacturers. By 2018, Sunsine annual capacity is expected to reach 172k tonnes (+6%).

China has dominated the rubber chemical market. As of 2015, total production of rubber chemicals in China reached 1.1mn tonne, accounting for 76% of the global output. Production from 47 companies took up more than 80% of the domestic volume.

Investment Thesis

Healthy demand from tyre industry. 90% of the consumption of rubber chemicals is associated with the automobile industry, predominantly in the production of car tyres. The consumption ratio of rubber chemicals to rubber is 6:100. Global tyre production is expected to grow from 2.2bn in 2017 to 2.7bn in 2020 with CAGR of 3.4% during the period. Meanwhile, total global production of rubber chemical is expected to reach 1.8mn tonnes by 2020, delivering a CAGR of 3.5% from 2015 to 2020.

Supply short and upswing prices of raw materials drove market prices to surge: In 2016, supply-side reform initiatives in China began phasing out environmentally obsolete capacity. Consequently, shortage began to appear as quality producers were not able to make up the demand gap. The average export price of aniline, the main material of rubber chemicals, was on course for recovery with 33% growth in recent two years and the average domestic price soared by 131% during the period.

Existing leading companies will consolidate further the market: Three main factors will result in a more consolidated market in the foreseeable future:

Investment Actions

Based on a required rate of return of 7.9%, sustainable growth rate of 1%, and FX (SGD/RMB) of 4.85, we derive a TP of S$1.60 (FY18e PE: 10x) by free cash flow to equity (FCFE) valuation method and initial a BUY call with an upside of 44.4%.

Company Background

Investment Thesis

Overview of rubber chemical sector

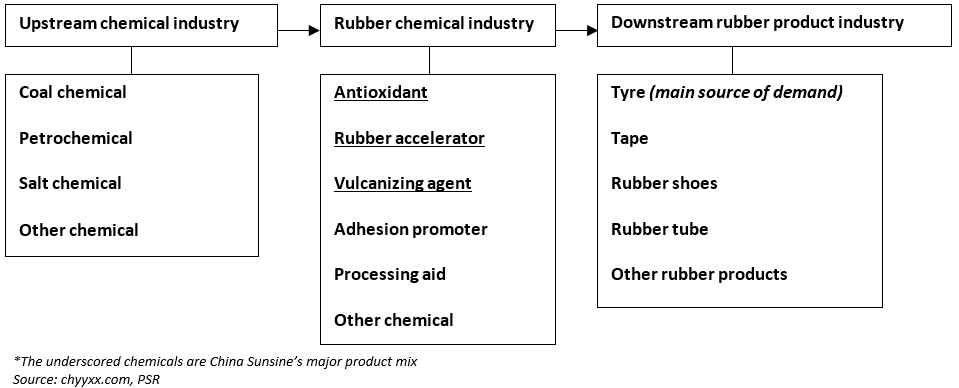

Rubber chemicals, also called rubber additives, are ingredients used to blend into either natural or synthetic rubber to produce rubber products that can possess various properties such as antioxidation, antidegradation and extension of lifespan. It is an indispensable intermediate that improves technique and quality in the process of production of rubber products, shown in Figure 1.

Figure 1: Rubber chemical industry chain

The raw materials of rubber chemicals comprise of aniline, carbon disulphide, hydrogen peroxide and morpholine. Aniline is the key chemical that is used for the production of antioxidant and rubber accelerator. Theoretically, aniline consumption ranges from 50% to 70% of per unit production of antioxidant and accelerator. Therefore, the price of it substantially affects the overall cost of production.

90% of the consumption of rubber chemicals is associated with the automobile industry, and 70% of the output is used for the production of car tyres, which consumes 70% of global rubber output averagely. The consumption ratio of rubber chemicals to rubber is 6:100. Therefore, the supply of car tyre markedly drives the demand for rubber chemicals.

China has become the biggest rubber chemical market and expected to consolidate

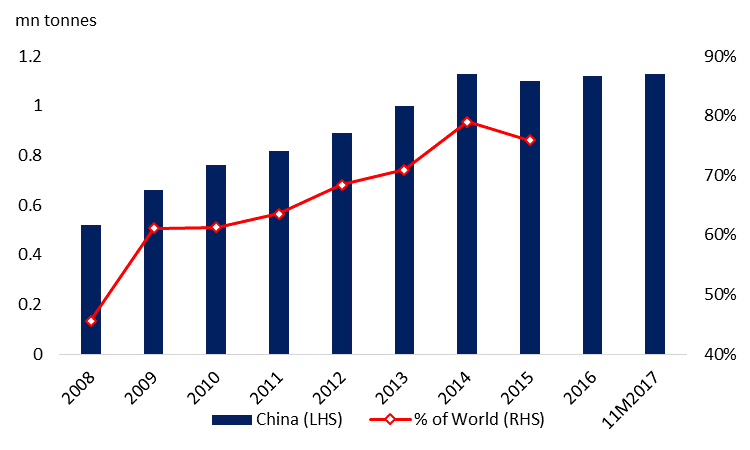

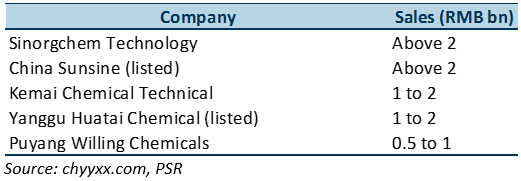

Over the past 10 years, China has been taking the lead in this niche market. See Figure 2, total production of rubber chemicals in China arrived at 520k tonnes, taking up 45.6% of the global volume in 2008. Since 2013, domestic production surpassed 1mn tonnes along with more than 70% of global market share. In the recent four years, the total output maintained at above 1.1mn tonnes, and the market share stabilised at c.75%. It is worth noting that more than 80% of the output come from 47 members of China Rubber Industry Association Rubber Chemical Committee. According to China Rubber Industry Association, as of 2016, gross industry output value of rubber chemical sector grew by 5.1% YoY to RMB19.2bn, and total sales grew by 7.4% YoY to RMB18.8bn in 2016. During the period, sales generated by top 5 companies, shown in Figure 3, accounted for more than 40% of the whole industry sales. Sales from top 20 companies out of over 100 peers took up more than 80% of market share. In a nutshell, the sector is trending to be consolidated, favouring the existing market leaders to maintain or even expand their market shares.

Figure 2: Production volume of rubber chemical in China dominates the world

Source: China rubber industry yearbook 2015-2016, cria.org.cn, PSR

Figure 3: Top 5 rubber chemical companies in 2016 (sorted by sales)

Sustainable growth of auto and tyre demand underpins the sector prosperity

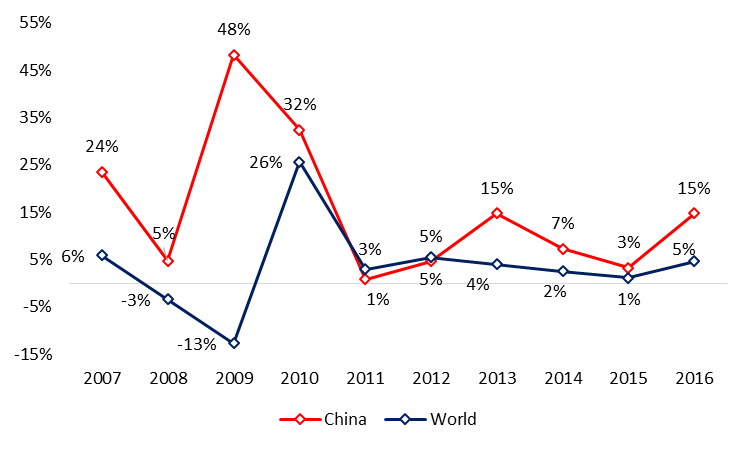

According to Organisation Internationale des Constructeurs d’Automobiles (OICA), also called International Organization of Motor Vehicle Manufacturers, China has become the fastest growing countries in the development of auto industry, see Figure 4. As of 2016, total car production in China reached 28mn units, representing a 15% YoY growth that outperformed the global 5% YoY growth. Meanwhile, the number of vehicle in use (VIU) in China has been maintaining at an over 10% annual growth for the last decade, which delivered a CAGR of 18%, shown in Figure 5. Apart from tyres being equipped with the newly built cars and vehicles, other car accessories such as tubes, dampers, and brake pads are also sources of consumption of rubber and rubber chemicals. The expanding volume of VIU that increasingly require recurring replacement tyres and components also drives it. In 2005, China surpassed US and became the top tyre producer globally along with the domestic tyre production arriving at 250mn units. During the last decade, China has also been the largest tyre consumer and exporter in the world. Shown in Figure 6, tyre production generated a CARG of 8%. It is expected that the volume will reach a new high of 635mn with 4.1% YoY growth in 2017.

Figure 4: Growth of China auto production outpaced the world

Source: OICA, PSR

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Guangzhi graduated from Singapore Management University with a Master degree in Applied Finance and from South China University of Technology with a Bachelor degree in Electronic Commerce.

The current sector coverages include Energy, Utilities, and Mining sectors. He has 3 years experience in equity research in both Hong Kong and Singapore market. He is the mandarin spokesperson for Phillip Securities Research in relation to China-related projects and all mandarin seminars and client events.