The Positives

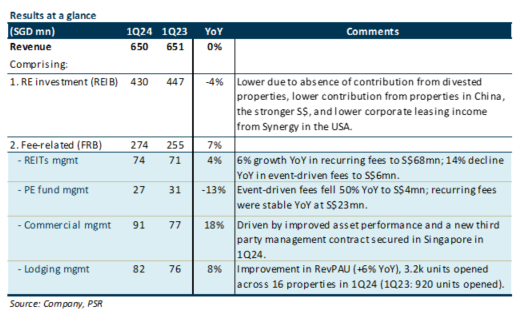

+ 1Q24 FRB revenue continues its growth trajectory, rising 7% YoY. This was due to improvements in commercial management fees (+18%), lodging management fees (+8%), and recurring fund management fees (+5%). Event-driven fees under the fund management platform remain a drag (-33% YoY), but we expect these to pick up this year as global transaction volumes gradually recover. Additionally, private funds recorded S$1bn in total investments in 1Q24, taking deployed funds under management to S$91bn from S$90bn in FY23. There is still S$9bn of dry powder pending deployment. CLI remains committed to double FUM to S$200bn in five years.

+ Faster pace of capital recycling. In 1Q24, CLI made S$600mn worth of divestments, up from S$35mn in 1Q23. More than 75% were divested into CLI’s fund vehicles. Divestment proceeds will be used to lower gearing and to pare down higher-cost debt. CLI is on track to hit its S$3bn annual divestment target, with the majority coming from China and the USA.

The Negative

– REIB revenue remains weak, falling 4% YoY. This was due to asset divestments, weaker operating performance in China, and lower revenue from the lodging platform Synergy in the USA.

Darren has over three years of experience on the buy-side as a fund manager. During his time as fund manager, he has managed multiple funds and mandates including dividend income, growth, customised, Singapore focused and regionally focused funds. He graduated from the University of London with a First-Class Honours degree in Banking and Finance.