Cache Logistics Trust: Bear with the initial pain of portfolio rebalancing strategy April 26, 2018 949

PSR Recommendation: ACCUMULATEStatus: Maintained

Target Price: SGD0.91

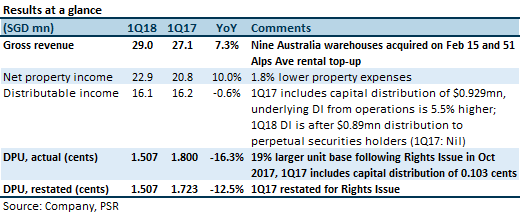

Gross revenue and DPU were within our expectation

Gross revenue and DPU met 24% and 24% respectively, of consensus FY18 estimates

Key events after the reporting period are the conversion of CWT Commodity Hub (April 12) and the pending divestment of Hi-Speed Logistics Centre

Maintain Accumulate; unchanged target price of $0.91

The Positives

Portfolio WALE lengthened QoQ from 3.4 years to 3.5 years. This is the effect of the nine Australia properties that were acquired in February 2018. The nine Australia properties had a combined WALE of 5.0 years, as at Dec 31, 2017.

Renewal risk for 2018 limited to 6.7% of GRI. Furthermore, there are no master leases expiring for the rest of year. The next master lease expiry in the portfolio is at Precise Two (15 Gul Way) on March 31, 2019.

Current aggregate leverage of 38.5% to be further reduced to 35.2%. Hi-Speed Logistics Centre (40 Alps Ave) is pending divestment for S$73.8mn and net proceeds will be used to repay current portion of borrowings. At 35.2% aggregate leverage, we estimate a debt headroom of S$108mn available (assume 40% gearing) to grow the pro forma AUM of S$1.32bn by 8%.

The Negatives

Updated portfolio occupancy as at April 12 is lower than the 97.3% reported as at March 31. This is due to the conversion of CWT Commodity Hub from master lease to multi-tenancy on April 12. Committed occupancy at the property is 86%, with CWT retaining 61%. Committed occupancy of 86% was below our expectation and we had lowered our estimates accordingly in our most recent update report (April 13).

Distribution income to unitholders was eroded by distribution to perpetual securities holders. Underlying distributable income was only 5.5% higher YoY, despite 10% higher net property income. We highlighted in an earlier update report (Jan 19) that the use of perpetual securities would give only slight DPU accretion, despite a much larger AUM.

Outlook

The outlook is stable. While the manager did not disclose the rental reversions during the quarter, we think it is reasonable to assume it was high single-digit negative or worse. Nonetheless, the portfolio is expected to be stable for the remainder of the year, with renewal risk limited to 6.7% of GRI against a backdrop of tapering supply of new space. Positive catalyst from the utilisation of available debt headroom to acquire; and negative surprise from worse than expected demand for space, delaying the recovery in rents.

Maintain Accumulate; unchanged target price of $0.91

No changes to our estimates. Our target price represents an implied 1.28x FY18e P/NAV multiple.

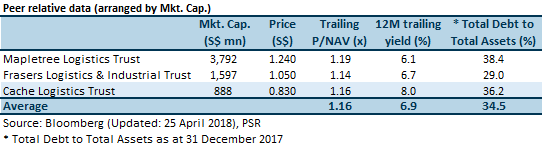

Relative valuation

Cache Logistics Trust is fairly valued relative to logistics peers in terms of P/NAV multiple. But it has a higher than average trailing yield, which suggests that there is room for yield to compress.

Subscribe

0 Comments

Inline Feedbacks

View all comments

About the author

Richard Leow Research Analyst Phillip Securities Research Pte Ltd

Richard covers the Transport Sector and Industrial REITs. He graduated with a Master of Science in Applied Finance from the Singapore Management University. He holds the CFTe and FRM certifications and is a CFA charterholder.

He was ranked #2 Top Stock Picker (Asia) for Real Estate Investment Trusts in the 2018 Thomson Reuters Analyst Awards, and ranked #2 Top Stock Picker (Singapore) for Resources & Infrastructure in the 2016 Thomson Reuters Analyst Awards.