The Positives

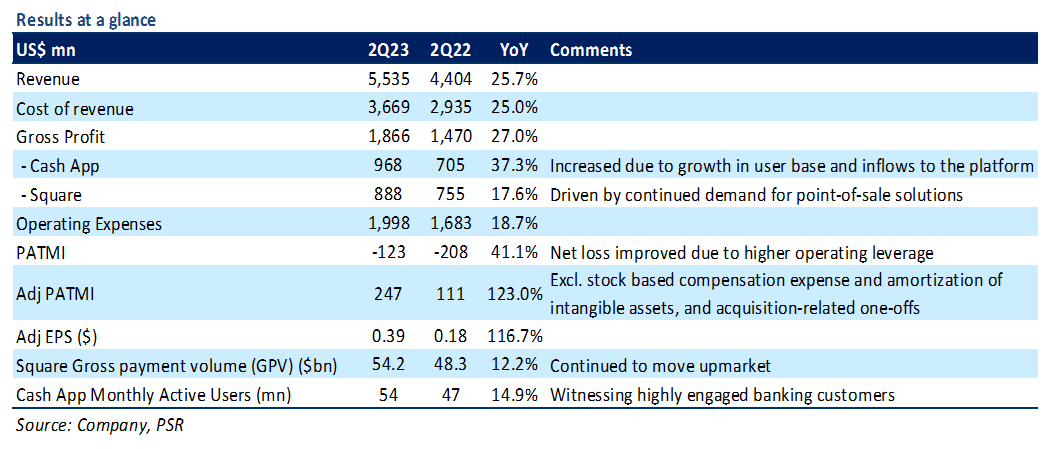

+ Cash App strength continues. Block’s Cash App segment, which offers peer-to-peer payment and consumer banking services, reported revenue growth of 36% YoY to US$3.6bn (39% YoY ex-bitcoin) and gross profit growth of 37% YoY to US$968mn. This growth was mainly driven by 15% YoY growth in Cash App’s monthly transacting active users to 54mn and 8% YoY growth in inflows per transacting active user to US$1,134. The greater inflows led to wider adoption across the Cash App ecosystem, including debit card, crypto trading, tax filing, and direct deposit.

+ Improvements in profitability. The net loss for Block improved by 41% YoY to -US$123mn in 2Q23 compared with -US$208mn in 2Q22. The improvement was mainly driven by higher operating leverage, including careful sales and marketing spend, and lower headcount growth. YoY headcount growth for FY23e is now expected to be below the 10% targeted range earlier this year (vs. 46% growth in FY22).

The Negative

– Deceleration in gross payment volume. In 2Q23, Square’s gross payment volume (GPV) grew 12% YoY to US$54.2bn compared with 17% growth rate in 1Q23 and 25% in 2Q22. Management said that the deceleration was primarily because processing volumes at existing sellers has fallen due to weak trends in global e-commerce and cuts to consumer discretionary spending.