The Positives

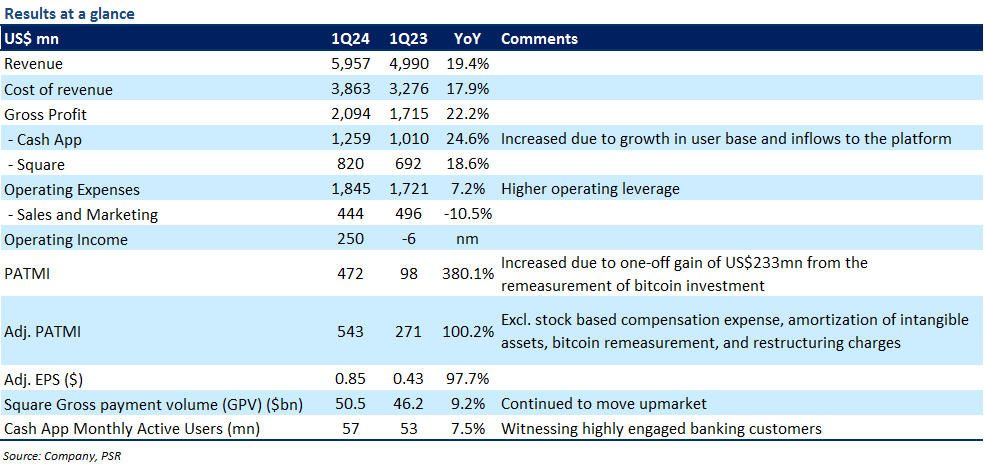

+ Cash App business sees strong growth. In 1Q24, Block’s Cash App segment, which offers peer-to-peer payment, banking, and investment services to individuals, generated revenue growth of 23% YoY to US$4.2bn (ex-bitcoin was up 18% YoY to US$1.4bn) and gross profit growth of 25% YoY to US$1.3bn. The growth was supported by a 7% YoY surge in monthly transacting active users to 57mn, of which 24mn (+20% YoY) used a Cash App debit card. In addition, inflows per transacting active user grew by 11% YoY to US$1,255, leading to wider adoption of its products and services, including ATM withdrawals, bitcoin investments, Cash App Borrow, and Cash App Pay.

+ Strength in Square segment. In 1Q24, Block’s Square segment, which enables merchants to accept payments, reported gross profit growth of 19% YoY to US$820mn (1Q23: 12% YoY) despite the company’s guidance for a slight moderation. The gross profit growth was supported by strength in its banking products (Square Loans and Instant Transfer) and international markets. Meanwhile, Square’s gross payment volume (GPV) grew by 9% YoY to US$50.5bn as consumer spending remained resilient.

+ Cost-cutting measures boost earnings. Block expanded its adj. net profit margin by 4% points YoY to 9%, while adj. PATMI more than doubled to US$543mn. This was mainly because the company continued to focus on improving cost efficiencies through measured hiring (headcount cap of 12,000) and reductions in corporate overhead expenses. Sales and marketing expenses fell by 11% YoY to US$444mn. We raise our FY24e adj. PATMI by 3% on higher operating leverage.

The Negative

– Nil