Company Background

Block (SQ), which changed its name from Square in Dec. 2021, operates as a financial services and digital payments company. Block’s two primary business segments are Square (29% of FY21 revenue), which offers point-of-sale (POS) hardware, software, and financial services to micro/small merchants, and Cash App (70%), a personal finance app for individuals that offers peer-to-peer (P2P) money transfers, debit card services, and investing (equities & Bitcoin). The US accounts for the majority (>95%) of revenue.

Investment Highlights

We initiate coverage with a NEUTRAL rating. Our target price is US$70 based on a DCF valuation with a WACC of 7.1% and terminal growth of 4.0%.

|

REVENUE Block generates revenue through four sources: 1) transaction-based revenue (27% of total revenue in FY21), which is calculated as a percentage of GPV; 2) subscription and services-based revenue (15%), earned from Instant Transfer fees charged to Cash App users and Square retailers, web hosting and domain name registration services, and servicing fees on Square Loans; 3) hardware revenue (1%), which is generated from sales of Square’s POS devices including contactless, EVM chip readers, and Square Stand; 4) bitcoin revenue (57%), which is recognized when Cash App customers purchase bitcoin at the cost of sale. In order to provide bitcoin to customers, the company typically buys the cryptocurrency from private brokers/dealers and charges a small margin before selling it to customers.

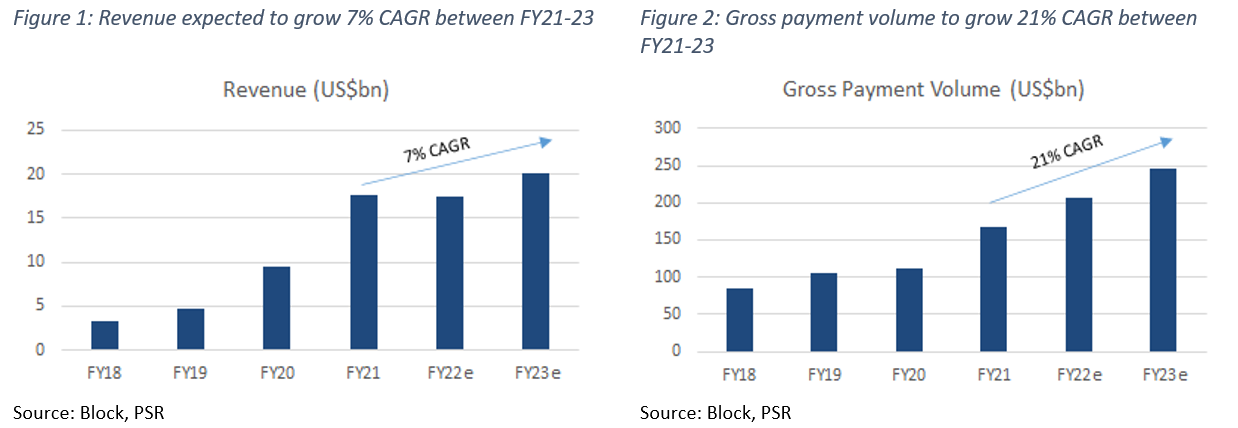

Block posted US$17.7bn in revenue for FY21 – increasing 86% YoY (Figure 1), with 70% of its total revenue coming from its Cash App segment and 29% from its Square segment. Square provides POS solutions to small merchants, while Cash App is a personal finance app for individuals. Block’s total revenue expanded at 75% CAGR in the past three years mainly driven by a surge in number of active Cash App customers and the number of business accounts. In FY21, Block’s GPV rose 49% to US$167.7bn (Figure 2) as retailers witnessed a significant rebound in sales activity post the COVID-19 vaccine roll-out, specifically from brick-and-mortar channels that had been adversely impacted by lockdowns in FY20. The US accounts for the majority (>95%) of revenue.

Revenue growth: We forecast total revenue of US$17.5bn in FY22e, which would represent a fall of 1% YoY, mainly due to weak consumer demand for Bitcoin and decline in cryptocurrency prices. Revenue from the Cash App segment in FY22e is expected to reach US$10.5bn (15% YoY drop), primarily from decline in Bitocin revenue slightly offset by growth in Cash for Business and Cash App Instant Deposit. Excluding Bitcoin, Cash App’s revenue is expected to grow by 46% YoY to US$3.4bn in FY22e. Square revenue is expected to grow by 30% YoY to US$6.8bn, on the back of increasing Square gross payment volume, origination volumes of Square Loans, as well as software subscriptions.

|

RULE OF 40

The “Rule of 40” was first introduced as a benchmark to measure the balance between growth and profitability of SaaS companies, taking into account both revenue growth, as well as profitability (Revenue Growth + EBITDA Margins), with the addition of both metrics needing to exceed the 40% threshold. We have modified this slightly by averaging revenue growth over a 3-year period compared to just a single period growth rate. Adding together Block’s 3-year average revenue growth of 77% and its adjusted EBITDA margin of 6%, the total of 83% is > than our required threshold of 40% (Figure 3).

|

RULE OF 40 The “Rule of 40” was first introduced as a benchmark to measure the balance between growth and profitability of SaaS companies, taking into account both revenue growth, as well as profitability (Revenue Growth + EBITDA Margins), with the addition of both metrics needing to exceed the 40% threshold. We have modified this slightly by averaging revenue growth over a 3-year period compared to just a single period growth rate. Adding together Block’s 3-year average revenue growth of 77% and its adjusted EBITDA margin of 6%, the total of 83% is > than our required threshold of 40% (Figure 3).

EXPENSES Block’s cost of sales grew 96% YoY in FY21 to US$13.2bn, above the total revenue growth of 86%. Cost of sales (75% of total revenue in FY21) includes transaction-based costs (processing fees and bank settlement fees), hardware costs consisting of product costs related to the company’s POS devices (Figure 4), and bitcoin costs comprising the amounts paid by Block to purchase Bitcoin.

Cash App cost of sales grew 116% YoY to US$10.2bn (58% of FY21 revenue) driven by growth in Cash App Instant Deposit, Cash for Business, and bitcoin costs. Square cost of sales grew 42% YoY to US$2.9bn (16% of FY21 revenue) primarily due to growth in GPV and growth in both card-present volumes and higher priced card-not-present transactions that occur over the phone, internet, or mail.

Operating expenses include product development (8% of FY21 revenue); sales and marketing (9%); general and administrative (6%); transaction and loan losses (1%); and bitcoin impairment losses (0.4%). Total operating expenses as a percentage of revenue have reduced from 41% in FY18 to 24% in FY21. We expect operating expenses as a percentage of revenue to be 37% in FY22e due to ongoing product innovation and sales and marketing spend to attract users to its platform.

MARGINS In FY21, Block’s revenues nearly doubled, but at the same time, its cost of sales also doubled. The company’s high cost of sales significantly lowers margins. Gross margins declined from 40% in FY18 to 25% in FY21 as expenses outpaced revenue growth. Gross margins from Cash App are down from 45% in FY18 to 17% in FY21, mainly due to the company’s bitcoin operations. Bitcoin is a negligible 2-3% gross margin business for Block. Meanwhile, Square’s gross margin is up from 39% to 45% over the same period due to increasing gross payment volumes.

In FY21, operating margin was at 1%, up from -0.2% in FY20, driven by lower operarting expenses. Block recorded net profit margin of 1% for FY21, a decrease from 2% the year before, and this was mainly due to lower other income. In FY21, Adjusted PATMI grew by 111% YoY to US$898mn, which mainly excludes stock-based compensation expense, amortization of acquired intangible assets, and bitcoin impairment losses.

We anticipate Block to continue generating small margins on revenues due to ongoing product innovation and growth investments.

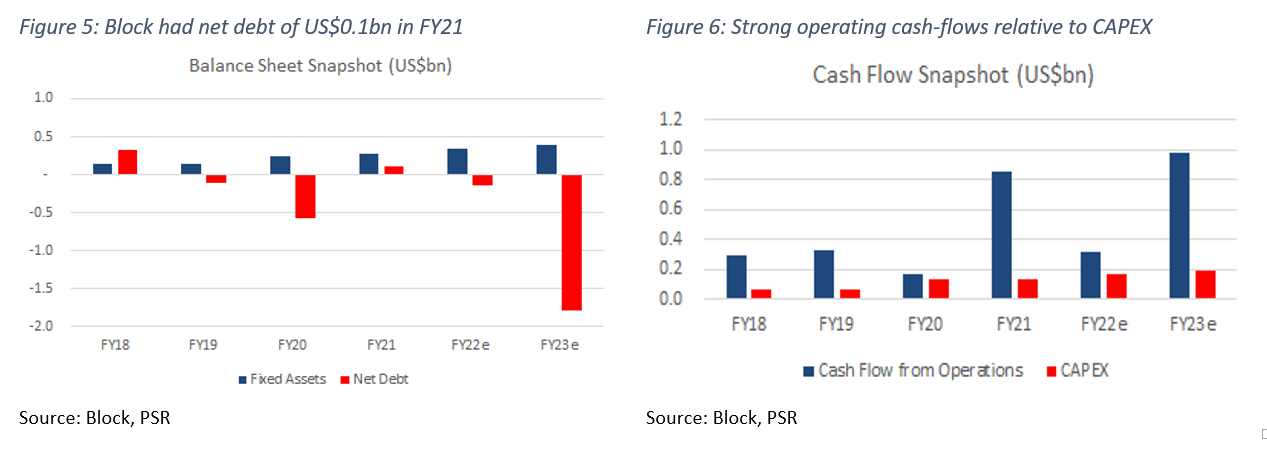

BALANCE SHEET Assets: In FY21, cash and cash equivalents increased by 41% YoY to US$4.4bn. Customer funds accounted for US$2.8bn (up 39% YoY) of assets in FY21, and are attributed to the customers stored balances that they could later use to make payments or send money. Block is a relatively asset-light business and doesn’t need heavy investments in fixed assets. In FY21, the company reported fixed assets of US$282mn. Block’s current ratio for FY21 is 1.9x.

Liabilities: Current liabilities for FY21 were US$5.4bn, almost US$1.3bn more than FY20. This increase was mainly due to a rise in customer payable balances. Non-current liabilities saw a surge of US$2.1bn in FY21. Block had a net debt position of US$0.1bn in FY21 (Figure 5). Block’s debt-to-equity ratio is 1.4x.

CASH-FLOW Cash-flow from operations has steadily risen from US$295mn in FY18 to US$848mn in FY21 (Figure 6). CAPEX for FY21 was US$134mn (1% of revenue), in line with the previous year. The company generated US$714mn in free cash flow in FY21. This translates to a 4% free cash flow margin.

|

BUSINESS MODEL

Block has two reportable segments: Cash App and Square. Cash App helps individuals transact and manage their money, while Square helps sellers start, manage, and grow their businesses.

Cash App (70% of FY21 revenue): Block drives most of its revenue through its mobile application Cash App. The application allows consumers to send and receive P2P (peer-to-peer) money for free, but charges about 3% fees on transactions involving credit cards (Figure 7). Cash App also allows consumers to deposit funds, invest in stocks and bitcoin, and use its debit card (Visa Cash Card), that is linked to customer stored balances, to withdraw funds from an ATM or to make purchases. Consumers can also directly deposit checks and store money in accounts. Cash App reported 44mn monthly active users as of FY21 (up 22% YoY).

In FY21, Cash App generated US$12.3bn in revenue, up 106% from the prior year. The primary drivers were growth in bitcoin revenue, Cash App Instant Deposit, Cash Card, and Cash for Business. Cash App gross profit was US$2.1bn in FY21, which is an increase of 69% compared to US$1.2bn in FY20. The segment’s gross profit accounts for about 47% of the company’s overall gross profit.

Bitcoin revenue will fluctuate based on customer demand as well as changes in the bitcoin market price. While bitcoin accounted for 57% of total revenue in FY21, it contributed only 5% of total gross profit. Revenue from Cash App segment in FY22e is expected to reach US$10.5bn (15% YoY drop), primarily from the decline in Bitocin revenue slightly offset by growth in Cash for Business and Cash App Instant Deposit (Figure 8).

Square (29% of FY21 revenue): The Square segment allows merchants of all sizes to accept debit and credit card payments through its point-of-sale (POS) products. Square charges a standard processing fee of 2.6% plus US$0.10 for most transactions regardless the type of card or size of merchant. However, transactions entered through a terminal manually will incur a fee of 3.5% plus US$0.15. Square’s product suite includes POS hardware (card reader and Square stand) and software (inventory tracking), scheduling services, invoicing, e-commerce solutions, payroll, and business loans. This suite of products enables merchants to work with Square to run and grow their businesses in an integrated and seamless manner instead of working with multiple vendors.

In FY21, Square generated US$5.2bn in revenue, up 47% from the prior year. This was primarily driven by growth in GPV attributable to higher consumer spending fueled in part by resumed in-person activity at sellers and broader macro economic recovery. Square gross profit was US$2.3bn in FY21, which is an increase of 54% YoY. The segment’s gross profit accounts for about 52% of the company’s overall gross profit. Square revenue is expected to grow by 30% YoY to US$6.8bn in FY22e (Figure 9), on the back of increasing Square gross payment volume, origination volumes of Square Loans, as well as software subscriptions.

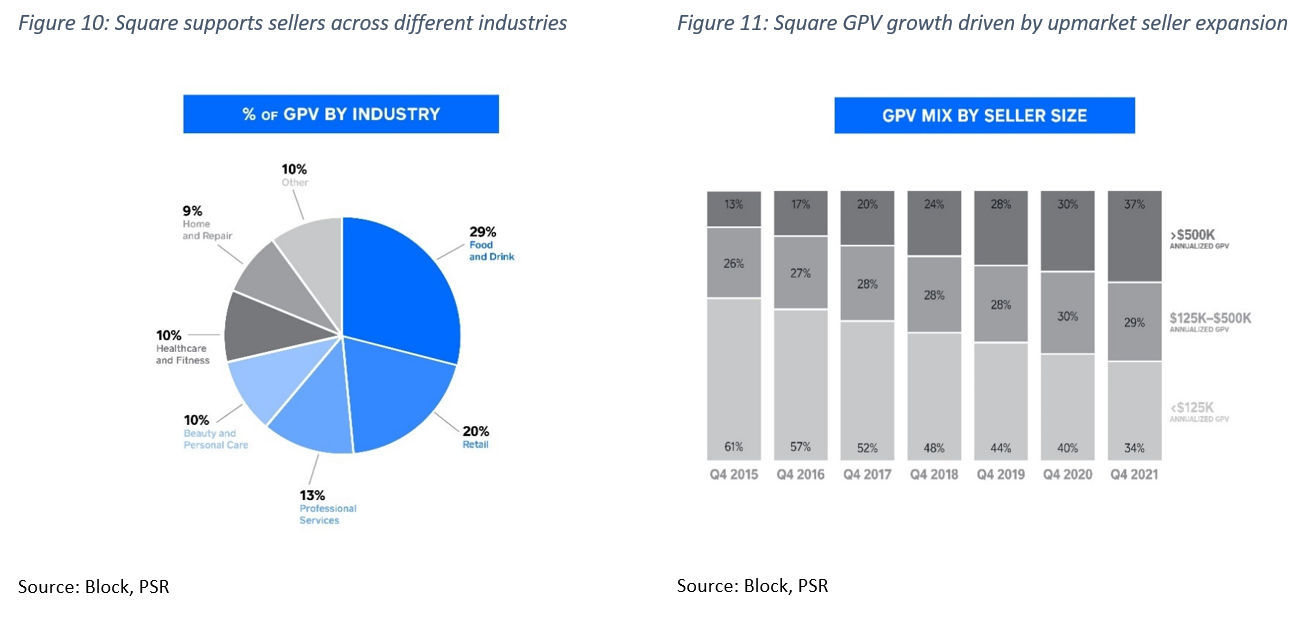

The Square segment serves merchants across several industries including Food & Drink, Retail, Professional Services, Healthcare and Fitness, and others (Figure 10). Square started out serving micro sellers but over time has been expanding upmarket to serve mid-market sellers (larger merchants that generate annualized GPV of >US$500K). In 4Q21, mid-market sellers accounted for 37% of total GPV for Square, up from 30% in 4Q20 (Figure 11). The growth was mainly driven by targeted product development (adding valuable new services) to create a unique experience for merchants. Block has also significantly expanded its business operations over time through acquisitions, notably acquiring buy now pay later (BNPL) company Afterpay, website builder Weebly, and music streaming service TIDAL.

|

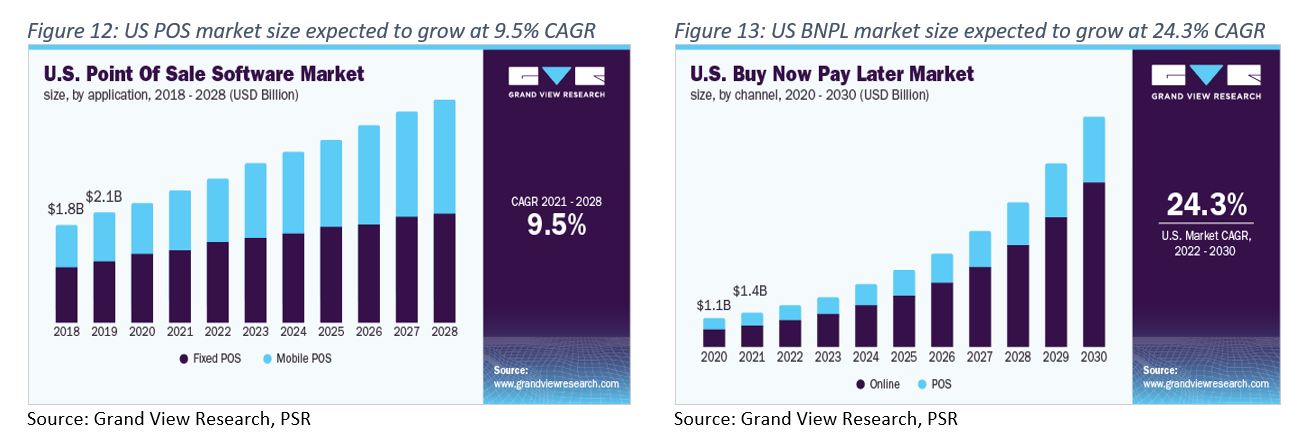

INDUSTRY Block is mainly part of two markets; point-of-sale (POS) system and payment processing solutions. A POS system enables businesses to accept payments from customers, keep track of sales, create receipts, inventory management, and more. According to Grand View Research, the global POS software market size, valued at an estimated US$10.4bn in 2021, is set to reach US$19.6bn in value by 2028, which indicates a 9.5% CAGR. The US POS software market size is also expected to see a CAGR of 9.5% (Figure 12). The main growth drivers for the market include rising interest in cashless transactions among customers, brick-and-mortar sales rebounding after the pandemic, and businesses transitioning to cloud-based POS systems from legacy hardware. In the POS market, Block competes with Lightspeed, PAR Technology and Toast. Lightspeed operates both in the retail and hospitality space, while Toast and PAR focuses on serving restaurants.

A payment processor communicates financial transaction information between the merchant, the bank that issued a customer’s credit or debit card, and the merchant’s bank. The payment processor ensures that the funds are transferred to the merchant’s account, and in turn earn revenues from transaction fees. According to Grand View Research, the global payment processing solutions market size, valued at an estimated US$38bn in 2020, is set to reach US$98bn in value by 2027, which indicates a 14.5% CAGR. The major growth drivers for the market are continued growth in the number of merchants seeking integrated payment processing solutions; high penetration of smartphones; and rising demand for online payments. In the payment processing services market, Block competes with PayPal, Stripe, and Global Payments. While PayPal has a competitive advantage in the payment processing solutions market, Block is the leader in the POS market. PayPal operates a two-sided payment network with 392mn active consumer accounts and 34mn active merchant accounts across 200 markets (compared with Block’s 80mn annual active Cash App users). PayPal has a market share of 41.9% in the online payment processing solutions worldwide.

With the acquisition of Australian payment platform Afterpay for US$29bn on Jan 31 2022, Block got access to the buy now pay later (BNPL) market. BNPL is a payment method that enables customers make purchases both online and in-store without having to pay the full amount upfront. According to Grand View Research, the global BNPL market size, valued at an estimated US$6.2bn in 2022, is set to reach US$39.4bn in value by 2030, which indicates a 26% CAGR. The US BNPL market size is expected to see a CAGR of 24.3% (Figure 13). The main growth drivers for the market are digitization, rising merchant adoption, and the increasing repeat usage among younger consumers. Young consumers prefer using BNPL services as it provides interest-free financing for buying high cost electronic devices, clothes, paying tuition fees and stationery products, and other items for general use.

|

|

RISKS 1. Consumer spending and economic pressure. Block’s operations are closely linked to the changes in consumer discretionary spending. A deterioration in the macroeconomic environment or a sudden surge in the unemployment rate could reduce consumer sentiment and spending, and adversely impact Block’s revenue growth and profitability. In addition, Block is exposed to greater degree of cyclical risks due to its disproportional exposure to micro merchants.

2. Intense Competition. Block faces competition from several players in the payment processing and peer-to-peer payment markets, including PayPal, Shopify, Apple Pay, Google Pay, and Stripe. With the acquisition of Afterpay, Block also directly competes against BNPL service providers such as Affirm. As a result, Block will need to keep strengthening its network effects and upgrade its products to maintain its historical growth rate.

3. Exposure to Bitcoin. Block is exposed to bitcoin price volatility through Cash App and company investments worth US$220mn. The cryptocurrency’s long-term adoption is still uncertain. For its investments in bitcoin, Block recognizes any decline in the market price below the original cost as an impairment charge as the cryptocurrency is an indefinite-lived intangible asset. |

|

VALUATION We initiate coverage of Block Inc with a NEUTRAL rating and a price target of US$70.00. Our valuation is based on DCF valuation, using a 7.1% WACC and a 4.0% terminal growth rate (Figure 14).

|

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: