Company Background

BHG Retail REIT was listed on the SGX on 11 December 2015. It has six retail properties strategically located in Beijing, Chengdu, Hefei, Xining and Dalian. Its six malls span 178,538 sqm of net lettable area. BHG distributed 100% of its distribution income in FY15, followed by at least 90% p.a. from FY16 onwards.

Highlights

About BHG Retail REIT

BHG Retail REIT was listed on SGX on 11 December 2015 at S$0.80 per unit. It has six retail properties spread out in five cities in China: Beijing, Chengdu, Dalian, Hefei and Xining, four of which are multi-tenanted and two are master-leased.

Sponsor Beijing Hualian Department Store Co. Ltd

Beijing Hualian Department Store Co. Ltd (000882.SZ, Not Rated) is part of the Beijing Hualian Group (Not Listed), which has interests in two publicly listed companies and several holding companies. An established Chinese home-grown retail-property operator, Beijing Hualian Department Store was one of the first companies to manage retail properties in China, with a focus on the ownership and management of community retail properties.

Assets

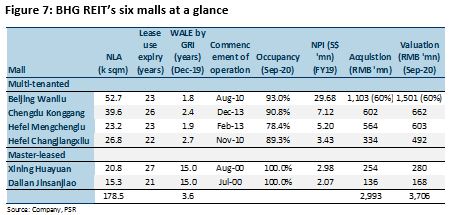

BHG REIT has six malls valued at RMB3,706mn or S$761mn:

Highlights

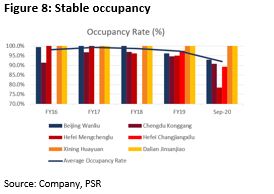

Committed occupancy remained healthy at 96.7% in FY19. The latest reported figure is 91.5% on 30 September 2020, still healthy. Lower occupancy rate of 78.4% was recorded at Hefei Mengchenglu due to ongoing tenancy rejuvenation.

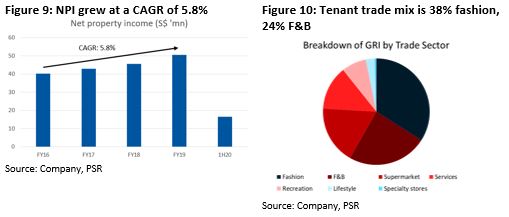

NPI grew at a CAGR of 5.8% from FY16 to FY19 (Figure 9). 1HFY20 NPI fell 34.5% YoY mainly due to Covid-19 measures at the start of the year. Its two malls in Hefei were temporarily closed from 7 February 2020 to 10 March 2020 while other malls remained open daily. Revenue from Hefei Changjiangxilu mall started in 1HFY19.

More than 65% of GRI and 80% of NLA are derived from the experiential segment, which typically requires consumers to visit the malls. Experiential offerings include pony and horse-riding training for children (Figure 11), an Amazing Art Space at Beijing Hualian mall and a flea market for children at Chengdu Konggang (Figure 12).

Rental renewals in FY20 were 80%, in line with pre-Covid figures. BHG had also provided rental rebates to certain tenants and all instalments were paid by end-FY20.

Defensive lease structure. About 95% of its leases are structured on the higher of fixed rents or percentage of gross turnover. This allows BHG REIT to benefit from upside while downside is capped by fixed rents. In FY19, more than 90% of its GRI was derived from base rents. Less than 10% was from variable rental income. Furthermore, more than 90% of its leases come with built-in rental escalation, allowing for organic growth.

BHG has been enhancing its assets continuously. It is on the constant lookout for opportunities to enhance its malls. It completed AEI at Hefei Mengchenglu in 2QFY19. Other new introductions included a container-style food lane outside its Chengdu Konggang mall, which has enhanced the mall’s attractiveness and visibility to nearby communities (Figure 14).

2. Tapping China’s economic fundamentals

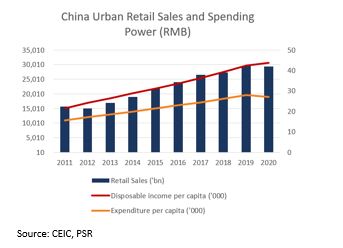

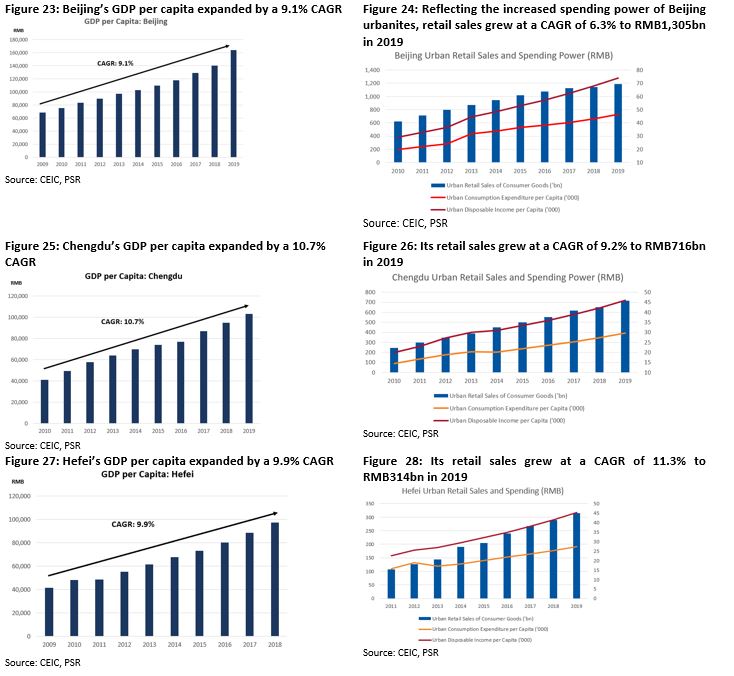

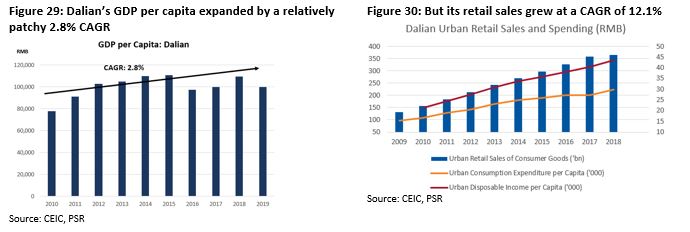

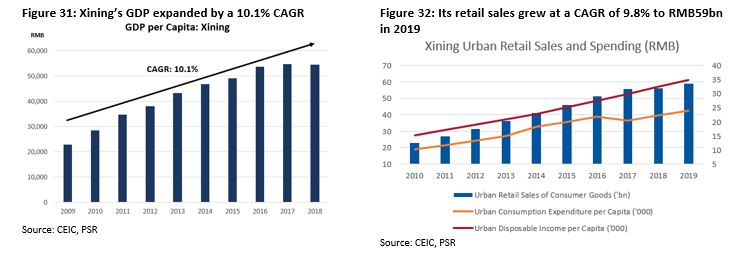

Disposable income and the expenditure of urban residents in China have been steadily increasing in the past decade, at CAGRs of 7.4% and 5.7% respectively (Figure 15). Urban retail sales grew at a CAGR of 6.5% to reach RMB29,424bn by end-2020.

Figure 15: Steadily growing disposable income and expenditure per capita of urban residents

3.M&A growth opportunities

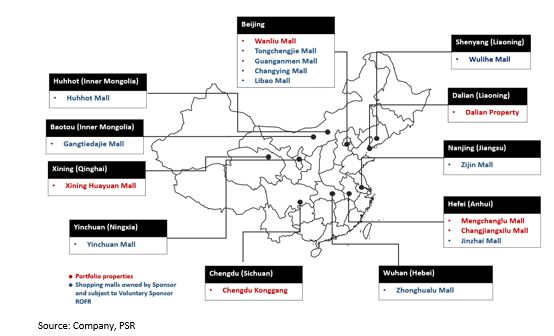

Sponsor, Beijing Hualian Department Store Co. Ltd, has a pipeline of ROFR properties. Of these, BHG completed its acquisition of the Hefei Changjiangxilu mall in April 2019 for RMB334.0mn. The mall added NLA of 26,826 sqm and accounts for 13.3% of its portfolio valuation.

Under its ROFR agreement, BHG could potentially acquire 11 properties in various cities (Figure 18).

Figure 18: ROFR assets located in various cities

The REIT also continues to explore opportunities among third-party quality income-producing retail properties.

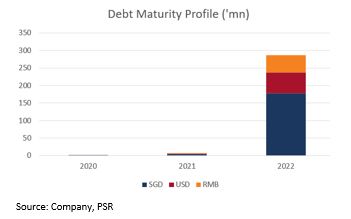

Gearing was 35.7% as of 30 September 2020. Borrowings of S$284.2mn were drawn down in FY19. Debt headroom for acquisitions remains comfortable, with a gearing limit of 45%. More than 80% of borrowings are offshore loans denominated in S$ and US$. About 60% of these offshore loans have been hedged using interest-rate swaps.

Figure 20: No major refinancing until 2022

Risks

Income support coming to an end. Its sponsor had waived its entitlement to dividends since IPO in December 2015. The amount of distributions waived, attributable to strategic investor units has been gradually falling from FY16 to FY20. In FY18 and FY19, total distributions waived amounted to S$5.3mn and S$3.6mn respectively or 25% and 15% of the REIT’s total units. The final distribution waiver was in FY20, during which distributions for 5% of total units were waived. For FY21, the drop in DPU and distribution yield from FY20, that is due to the distribution waiver falling off, would be minimal. Moving forward, on the back of continued economic growth, the REIT is poised for growth.

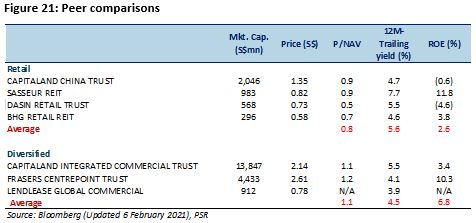

Comparables

BHG REIT’s FY19 DPU yields with and without distribution waiver were 6.8% and 5.8% respectively.

It is trading at a 4.6% yield vs 5.5-7.7% for comparables like Dasin Retail Trust (DASIN SP, Buy, TP S$0.90), Sasseur REIT (SASSR SP, Not Rated) and CapitaLand China Trust (CLCT SP, Not Rated) (Figure 21)

.

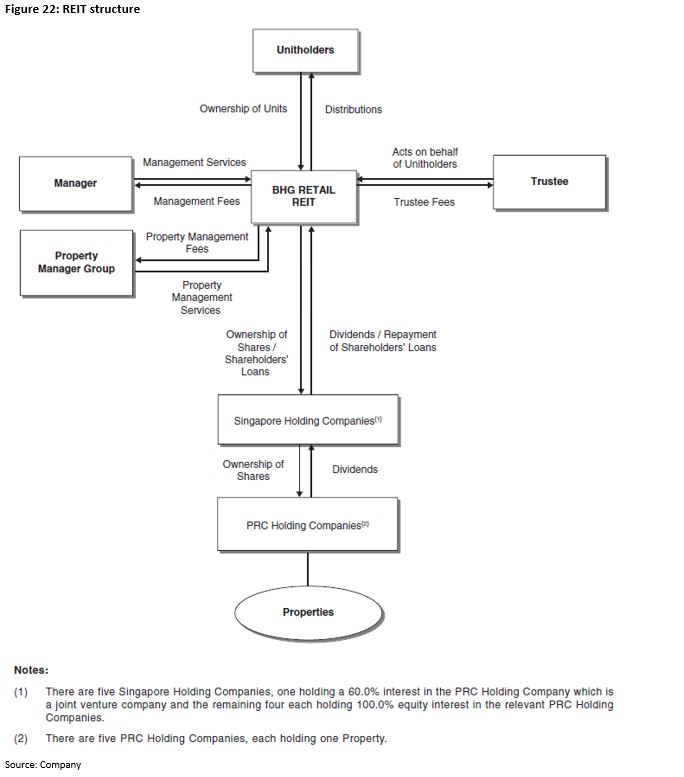

Appendix 1: REIT structure

Appendix 2: Overview of cities

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: