The Positives

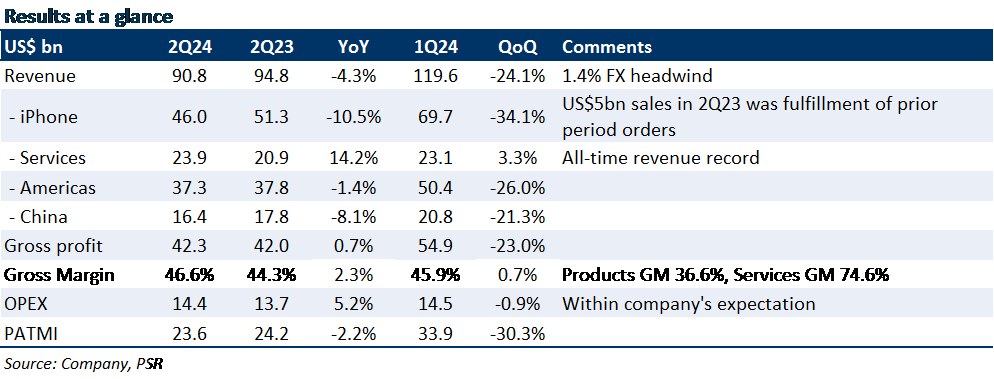

+ Strong gross margin delivery. AAPL’s 2Q24 gross margins of 46.6% (+2.3% YoY), beat its guided 45-46% range, despite a decline in revenue. The margin expansion is driven by 1) a higher mix of Services (e.g., Google payment, with practically 100% gross margin) and 2) a higher mix of Products (customers preferring premium models). Product margin declined by 10bps, mainly due to the decrease in iPhone revenue.

The Negatives

– Weakness persists in revenue performance. AAPL reported revenue of US$90.8 bn, marking a 4.3% YoY decline, reflecting persistently low demand for its products. iPhone sales have declined for the second consecutive quarter, dropping by 10.5% YoY. This decline is primarily attributed to weak performance in the Chinese market, with a decrease of 8.1% YoY, influenced by China’s slowing economy and increased competition from local rivals like Huawei. Although the decline was less than expected, AAPL’s revenue performance overall has been sluggish. Compared to 2Q21, its revenue in 2Q24 has only increased by 1.3%. The company’s guidance for 3Q24 also remains weak, with an expected revenue growth of low single-digit YoY. We estimate iPhone to remain flat or decline by single digit YoY in 3Q24e based on guidance.

– AI strategy still shrouded in mystery. Unlike other Big Tech rivals who are very transparent with upcoming AI features, AAPL lags behind with clearer AI strategies. Despite assuring investors that AI has been deeply embedded within its software and services, the company has not made a big splash in the AI space yet. Management has indicated plans to unveil more details in the ‘weeks ahead,’ presumably waiting until its Worldwide Developers Conference on June 10th. Whether AAPL can capitalize on the AI boom and unveil new AI features in the upcoming iPhone will influence the short & long-term outlook for AAPL.

Helena covers Hardware/Marketplaces/ETF. Helena graduated with a master degree in Financial Technology from Nanyang Technological University