The Positives

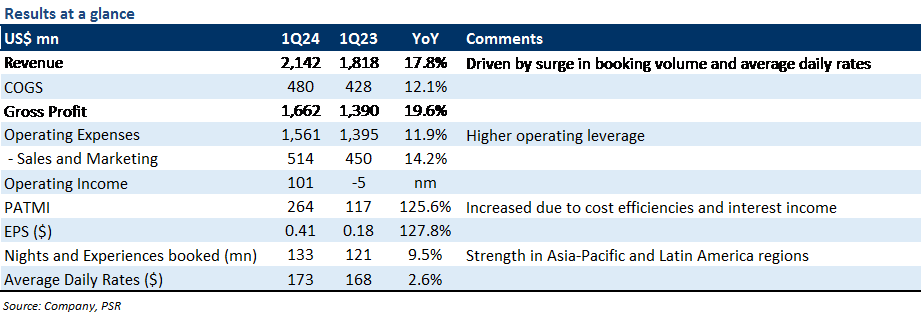

+ Revenue for 1Q24 showed strong growth. 1Q24 revenue grew 18% YoY to US$2.1bn, which was 4% above the top end of the company guidance. This outperformance was primarily driven by a 10% YoY increase in booking volumes to 133mn, a 3% YoY improvement in the average daily rates to US$173, and a shift in the Easter holiday this year. Airbnb reported a 21% YoY growth in bookings in the Asia-Pacific region and a 19% YoY growth in Latin America. Meanwhile, the number of cross-border nights booked grew by 10% YoY, representing 46% of total booking volumes in the quarter.

+ Net margin improved on lower costs and higher interest income. Airbnb expanded its net profit margin by 6% points YoY to 12%, while PATMI more than doubled to US$264mn. The margin improvement was mainly due to top-line upside, higher operating leverage, and 38% YoY increase in interest income to US$202mn. The sales and marketing expenses grew by 14% YoY to US$514mn (1Q23: 30% YoY).

The Negative

– Soft 2Q24e revenue guidance. For 2Q24e, Airbnb expects total revenue to grow 9% YoY to US$2.7bn (2Q23: 18% YoY). The significant slowdown is mainly because of unfavourable foreign exchange rates and holiday-related stays being pulled forward to 1Q24, as the Easter holiday fell in March instead of April this year.