The Positives

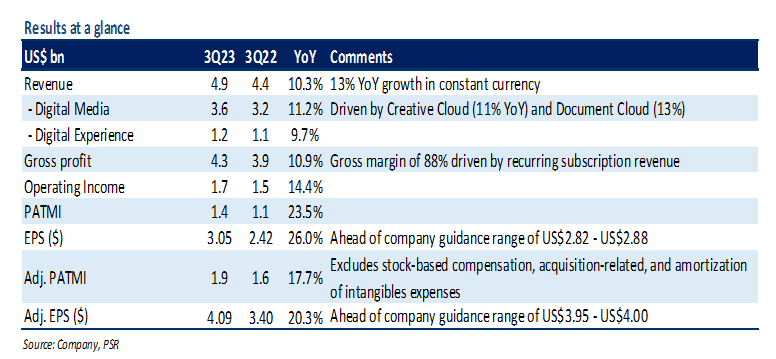

+ Creative Cloud momentum remained robust. Adobe’s Creative Cloud business comprises 81% of Digital Media segment revenues. Creative Cloud revenue grew 11% YoY to US$2.9bn (14% YoY in constant currency). Net New Creative Cloud annualized recurring revenue, or ARR, was US$332mn during the quarter, with a total Creative Cloud ARR of US$12bn. The growth was mainly led by strong demand for its photography and video editing applications due to a surge in both the creation and consumption of digital media. Management highlighted that the company has integrated its generative AI offering Firefly into flagship products Photoshop and Illustrator, with more than 3mn beta release downloads. Key customer wins for Creative Cloud in 3Q23 include Amazon, SAP, and Take-Two Interactive.

+ Continued strength in Document Cloud. Document Cloud sales grew 13% YoY to US$685mn, accounting for 19% of Digital Media revenues. Net new Document Cloud ARR was US$132mn, exiting the quarter with Document Cloud ARR of US$2.6bn. The growth was primarily driven by continued demand for Acrobat PDF solutions across computing devices and e-signature capabilities. Management highlighted that Acrobat Web monthly active users spiked by 70% YoY led by growth in documents opened through Chrome and Edge extensions. Key customer wins in 3Q23 include Citibank, GlaxoSmithKline, and Morgan Stanley.

The Negative

– FX impacted revenue growth. Adobe generates 40% of its total revenue from international markets. The company’s revenue was negatively impacted by the strengthening of the US dollar relative to most other currencies, including the Euro, British pound, and Japanese yen. In 3Q23, FX headwind to revenue was about US$125mn (~10% of PATMI).