Report type: Weekly Strategy

“Japanese Stocks after the FOMC, Stocks that are Undervalued Compared to U.S. Stocks and Nagoya”

Conflicting movements were indicated between the U.S. stock market and the Nikkei average futures (after-hours trading) due to the U.S. FOMC (Federal Open Market Committee) statement release from 3:00am on the 3rd in Japan time and from the press conference with FRB (Federal Reserve Board) Powell which followed from 3:30am. In the statement release, it was said that the “cumulative effect” of monetary tightening was considered, and as a result of hints towards a possibility of a reduction in the range of interest rate hikes in the FOMC from December onwards, the U.S. stock market responded with a significant rise. However, the U.S. stock market fell significantly as a result of mention in the press conference with Chair Powell from 3:30am that “the ultimate level of policy interest rates will be higher than previously expected” and an emphasis on the Hawkish policy in “it being premature to consider pausing interest rate hikes”. On the 4th after the public holiday in Japan, the Nikkei average also fell to 27,032 points at one point compared to the closing on the 2nd at 27,663 points.

In contrast to stock indices that are unable to overcome the rising trend, for the quarterly results of major enterprises, enterprises that were greatly impacted by the slump in China’s economy as a result of the aftermath of the zero-COVID policy, such as Toyota Motor (7203) in addition to Toyota Group and FANUC (6954), could not avoid a profit decrease, however, for the most part, it appeared that there was a string of favorable results which were backed by improvements in business performance following the reopening of the economy since the COVID-19 pandemic, the absorption of rising costs via price increases and the effect of the weak yen following overseas sales.

Stock prices have been increasing for consecutive days since the day after the results announcement for Panasonic Holdings (6752), which was said to have a possible tax credit occurrence in their U.S. battery factory in terms of their results announcement if the U.S. “Inflation Reduction Act” is enforced, as well as for Hitachi (6501), where a fight for global leadership is unravelling for the platform creation of IoT (internet of things) between the German Siemens.

Also, a distortion in individual stocks is becoming evident when comparing the stock prices of Japanese stocks and U.S. stocks, such as in construction machines, where Komatsu (6301), which follows the American Caterpillar (CAT), is significantly undervalued in terms of their forecasted dividend yield and forecasted P/E ratio (price-earnings ratio) compared to Caterpillar, and the stock price of McDonald’s Holdings Company (Japan) (2702) shifting to a plateau range close to approx. 5 years ago compared to the stock price of the American McDonald’s (MCD), which is currently renewing its all-time record high. Compared to the American J&J (JNJ), which is being praised for its consumer business spinoff policy next year, it looks like it would be the same for Takeda Pharmaceutical (4502), which has already sold off its consumer business 2 years ago and is in the process of selection and concentration.

Studio Ghibli, which boasts immense popularity with foreigners as well, opened its theme park on the 1st within “Aichi Commemorative Park” in Aichi Prefecture. It takes about 33 minutes from Chubu Centrair International Airport to Nagoya Station via the Meitetsu μSKY Limited Express train, about 28 minutes from Nagoya Station to Fujigaoka Station via the municipal subway’s Higashiyama Line, and about 13 minutes from Fujigaoka Station to Aichi Commemorative Park Station via the Linimo line. There are also direct buses by Meitetsu departing from Centrair.

In the 7/11 issue, we will be covering Mirait One (1417), Hitachi (6501), Sompo Holdings (8630) and Nagoya Railroad (9048).

Mirait One Corporation (1417) 1,410 yen (4/11 closing price)

・Established in 2010 as a joint holding company via business integration between 3 companies which are Daimei, Commuture and Todentsu. Integrated businesses with TKK from Sendai as well in 2018. They are the No.3 telecommunications construction operator in Japan and mainly focuses on those for NTT (9432).

・For 1Q (Apr-Jun) results of FY2023/3 announced on 10/8, net sales decreased by 5.2% to 95.336 billion yen compared to the same period the previous year and operating income fell into a deficit from 4.707 billion yen the same period the previous year to (1.147) billion yen. There was a decrease in merchandise sales in the ICT solutions business, mobile-related construction work and optical fibre outfitting work. Temporary factors had influenced, such as integrated expenses of consolidated subsidiaries in the profit aspect.

・For its full year plan, net sales is expected to increase by 14.8% to 540 billion yen compared to the previous year, operating income to decrease by 8.5% to 30 billion yen and annual dividend to have a 5 yen dividend increase to 60 yen. Orders received also increased by 3.6% to 540 billion yen, which was supported by 5G communications infrastructure development and ICT solutions demand involving digital transformation (DX), as well as digital infrastructure reinforcement that supports the government’s green growth strategy, etc. Although their stock price has been on a downward trend since Sep ’21, their forecasted dividend yield may be why they are gaining appeal.

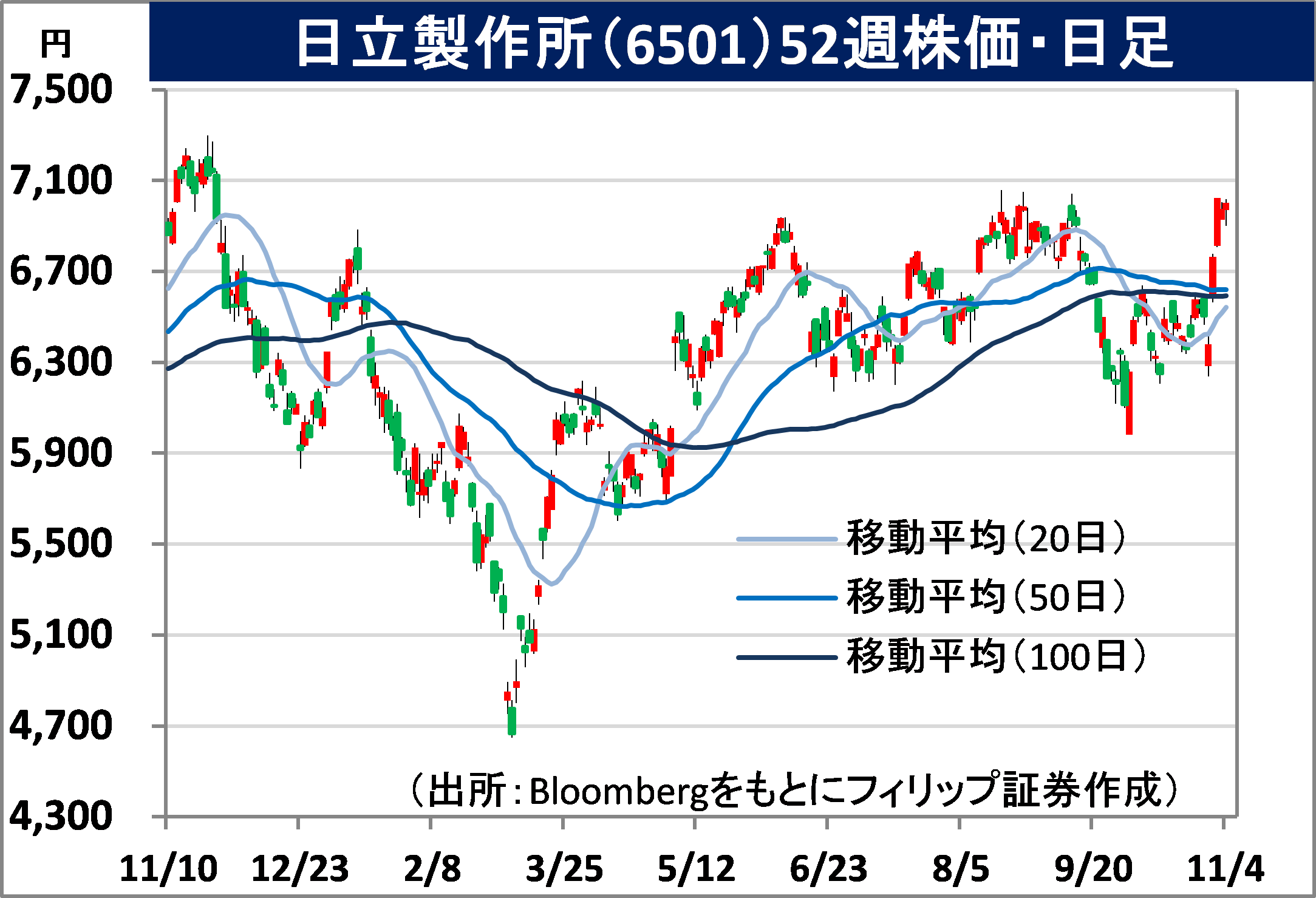

Hitachi, Ltd. (6501) 6,996 yen (4/11 closing price)

・A general electrical machinery manufacturer that established in 1910. Changed its “IT”, “energy”, “industry”, “mobility” and “life” segments to “digital systems & services”, “green energy & mobility” and “connective industries” from FY23 onwards.

・For 1H (Apr-Sep) results of FY2023/3 announced on 28/10, sales revenue increased by 12.1% to 5.4167 trillion yen compared to the same period the previous year and operating income after adjustment from deducting selling, general and administrative expenses from gross profit margin increased by 4.7% to 324.6 billion yen. There was growth in orders received in green energy & mobility, which was contributed by multiple large projects involving Hitachi Energy, as well as in digital systems & services, which was supported by DX demand.

・Company revised its full year plan upwards. With sales revenue having expected to increase by 1.3% to 10.4 trillion yen compared to the previous year (original plan 9.5 trillion yen) and operating income after adjustment to increase by 2.0% to 753 billion yen (original plan 700 billion yen), they have reversed from a forecast of a decrease in sales and income following the sale of a listed subsidiary to an increase in income and profit. Due to the contribution from the acquisition of the American GlobalLogic at approx. 1 trillion yen in July last year, in the “Lumada business”, which spans across various businesses that aim for digital transformation in social infrastructure, there was an increase in 1H with a 54% increase.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: