|

Report type: Weekly Strategy |

■F&B sector transformation, activist season, semiconductor review

A major holiday period is approaching, with up to 10 consecutive holidays from the 29/4 to 8/5. At a 20/4 meeting of the expert panel that advises the Ministry of Health, Labour and Welfare on measures against Covid-19, it was reported that the number of newly-infected persons nationwide during the past week had declined for the first time in four weeks. At the same time, there were signs of increasing interest in travel and leisure-related stocks, which have become more visible since the lifting of quasi-emergency measures to prevent the spread of the disease. In the US, major airlines like United Airlines and American Airlines are expecting to return to profitability in the April-June period according to their Jan-Mar 2022 earnings announcements. This may have implications for Japan’s travel and leisure trends in the near future.

In this regard, the F&B sector is drawing attention. As stores were forced to shorten their operating hours due to the pandemic, companies have found ways to survive by taking advantage of takeout and delivery services through the use of apps, and have also sought to improve operational efficiency by introducing food delivery robots and other means. If the flow of people returns and customer traffic recovers to pre-Covid levels, profits are expected to greatly exceed those during pre-Covid levels through significant improvements in profit margins.

Activists (shareholders who speak out) are increasingly investing in companies with fiscal years ending in March which are preparing for their annual shareholder meetings in June. This month, City Index Eleventh, a former Murakami Fund affiliate, increased its purchases of Daiho Corp (1822), Cosmo Energy Holdings (5021), and Central Glass (4044), companies which had already submitted large shareholding reports. City Index Eleventh also newly appeared as a major shareholder with more than 5% of holdings in Credit Saison (8253) and Sumitomo Osaka Cement (5232). Such activities are being watched as moves to demand shareholder returns from undervalued stocks with high cash holdings, or as a way to reorganize an industry such as the cement industry, which is expected to encounter a tighter profit environment due to the tight supply and demand of Russian coal. It is also worth considering an investment strategy of stocking up on unpopular undervalued stocks with high cash holding ratios and letting them remain inactive in the market for a long time.

There is also growing momentum for a review of semiconductor related stocks. The trigger may be the Jan-Mar 2022 earnings announcements of Taiwan Semiconductor Manufacturing Company (TSMC), the world’s largest semiconductor contract manufacturer, and ASML of the Netherlands, the world’s largest semiconductor lithography equipment manufacturer. TSMC expects to increase its capex for FY2022 to $40-$44 billion from $30 billion in the previous year, and ASM’s CEO said, “We are seeing unprecedented strong demands”. The fact that governments are attracting semiconductor factories to their own countries amid rising geopolitical risks is also a push factor. Demand for manufacturers of semiconductor production and inspection equipment is therefore secure for the time being. In particular, in the area of EUV (Extreme Ultraviolet) lithography systems, besides Lasertec (6920), JEOL (6951), a semiconductor electron beam lithography system manufacturer, and Nikon (7731), its partner and a long-established lithography system manufacturer, will be the next stocks to watch.

In the 25/4 issue, we will be covering Torikizoku Holdings (3193), Solxyz (4284), Serverworks (4434) and ROHM (6963).

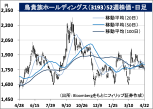

Torikizoku Holdings (3193) 1,753 yen (22/4 closing price)

・Opened the first “Torikizoku” store in Higashiosaka City in 1985 as part of a chain of yakitori restaurants. Operates in the Kansai, Kanto, and Tokai regions, with 615 stores at the end of July 2021. Characterized by offering products at uniform prices for all items. Transitioned to a holding company in February 2021.

・For 1H (Aug-Jan) results of FY2022/7 announced on 11/3, net sales was 8.184 billion yen (10.831 billion yen in the previous year before the transition to a holding company), operating income was a loss of 1.856 billion yen (a loss of 1.217 billion yen in the previous year), and ordinary income was 808 million yen (a loss of 1.035 billion yen in the previous year). Sales declined and operating income was a loss due to government requests to shorten business hours and refrain from serving alcoholic beverages. However, managed to turn to a profit for ordinary income thanks to a subsidy income of 3.1 billion yen.

・The full-year company plan is as yet not finalised due to the uncertain impact of the Covid-19 pandemic on the company’s performance. Announced a 7% price increase for the first time in 4 years for “Torikizoku” products starting 28/4. All drinks and food items will be increased uniformly (including tax) from 327 yen to 350 yen. In addition, “TORIKI BURGER”, a chicken burger specialty restaurant, was opened in August last year as the second mainstay business of the company after its yakitori izakaya business. Expected to capture post-Covid demand changes such as take-out and home delivery demands.

SOLXYZ Co., Ltd (4284) 393 yen (22/4 closing price)

・Established in 1981. With SBI Holdings (8473) as its largest shareholder, company operates as an independent system integrator (SI), dealing with software development and digital signage businesses. Main customers are from the financial sector.

・For FY2021/12 results announced on 10/2, net sales increased by 5.6% to 13.922 billion yen compared to the previous year, and operating income increased by 30.3% to 1.105 billion yen. Growth in software development business for the financial and telecommunications industries and edge computing (embedded) consulting business had offset the decline in financial performance arising from the sale of the digital signage business. Improved profitability contributed to higher income.

・For its FY2022/12 plan, net sales is expected to increase by 11.3% to 15.5 billion yen compared to the previous year, and operating income to increase by 17.6% to 1.3 billion yen. While its tradable market cap as of the end of June last year was only 6.56 billion yen against the listing maintenance standard of 10 billion yen, the company announced its “Plan for Compliance with Listing Maintenance Standards” with the submission of its application for selection to the TSE Prime Market in November last year. Basic policy is to expand into the stock-type business with recurring billing and the ASEAN market.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: