Report type: Weekly Strategy

“Ukraine Tensions, Substitute Russian Demands and BOJ Appointments?”

Western countries have taken the most severe economic sanctions, locking out leading Russian banks from the international payments network SWIFT. The decision to also sanction the Russian Central Bank to restrict its use of foreign exchange reserves (approximately $630 billion), including US dollars and Euros, prevented Russia from buying up the ruble through currency intervention. Although it was hoped that these economic sanctions would make Russia more open to a cease-fire, on the contrary, it has intensified its military incursion into southern Ukraine. Amidst these situations, reports of a fire caused by a Russian military attack at Europe’s largest nuclear power plant in Zaporizhia shook the Japanese stock market on 4/3. Two rounds of ceasefire negotiations between Russia and Ukraine were held until 3/3, but apart from an agreement to establish a “humanitarian corridor” for the evacuation of civilians and others, a path to a solution/resolution has not been found.

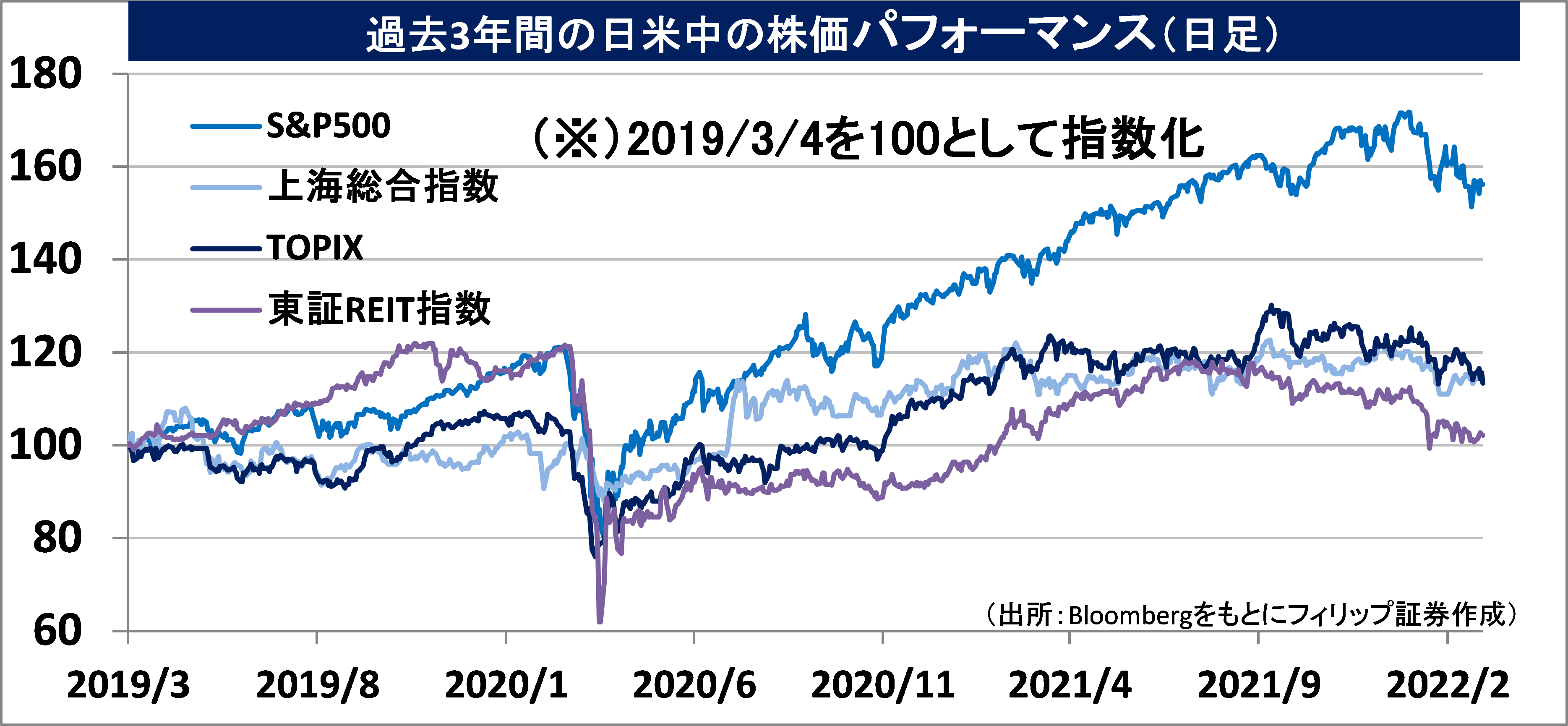

We may enter a phase in which the market will test a recovery in anticipation of the third round of negotiations to be held in the near future. However, if no progress is seen in the negotiations, the market is likely to be hit by a sell-off. The Nikkei Average as of the close on 3/3 had a P/B ratio (Price-to-Book ratio) weighted by market capitalization of 1.18x, which is slightly below the average level of around 1.2x for the past 10 years or so. In the short term, it may be necessary to lower the lower limit of the assumed range for the Nikkei Average weighted average P/B ratio to some extent.

In terms of Russia’s global market share in 2020, crude oil and natural gas accounted for about 12% and 17% respectively of energy supply, while industrial diamonds and palladium are market share leaders, accounting for more than one-third of the market. Furthermore, nickel, gold and platinum are also over 10%. Wheat, corn, and sunflower oil account for about 30%, 20%, and 80% respectively of agricultural exports, while fertilizer ammonia and potassium also exceed 10%. Companies that are likely to benefit from price hikes due to tight supply and demand will therefore be in the spotlight.

On 1/3, the Japanese government presented to the Diet a personnel proposal to appoint Mr Takata and Mr Tamura to replace BOJ board members Mr Kataoka and Mr Suzuki, whose terms will expire on 23/7. While Mr Kataoka is a “reflationist” who advocates aggressive monetary easing, Mr Takata is more concerned about the side effects of monetary easing, and this may influence the appointment of the BOJ governor, an event which is expected to be in full swing later this year, after spring next year. An exit strategy for monetary easing, if discussed, is expected to be accompanied by a recovery in the economy. This would be a boon for bank stocks linked to improved earnings due to net interest margin expansion. In particular, regional banks, with the scope of their business expanding with the revision of the Banking Law that came into effect last November, are strongly expected to play a central role in “regional development,” which is linked to the theme of the upcoming election. There may therefore be room to consider investments in such stocks for the latter half of the year.

In the 4/3 issue, we will be covering Healthcare & Medical Investment (3455), ENEOS Holdings (5020), Ferrotec Holdings (6890) and Juroku Financial Group (7380).

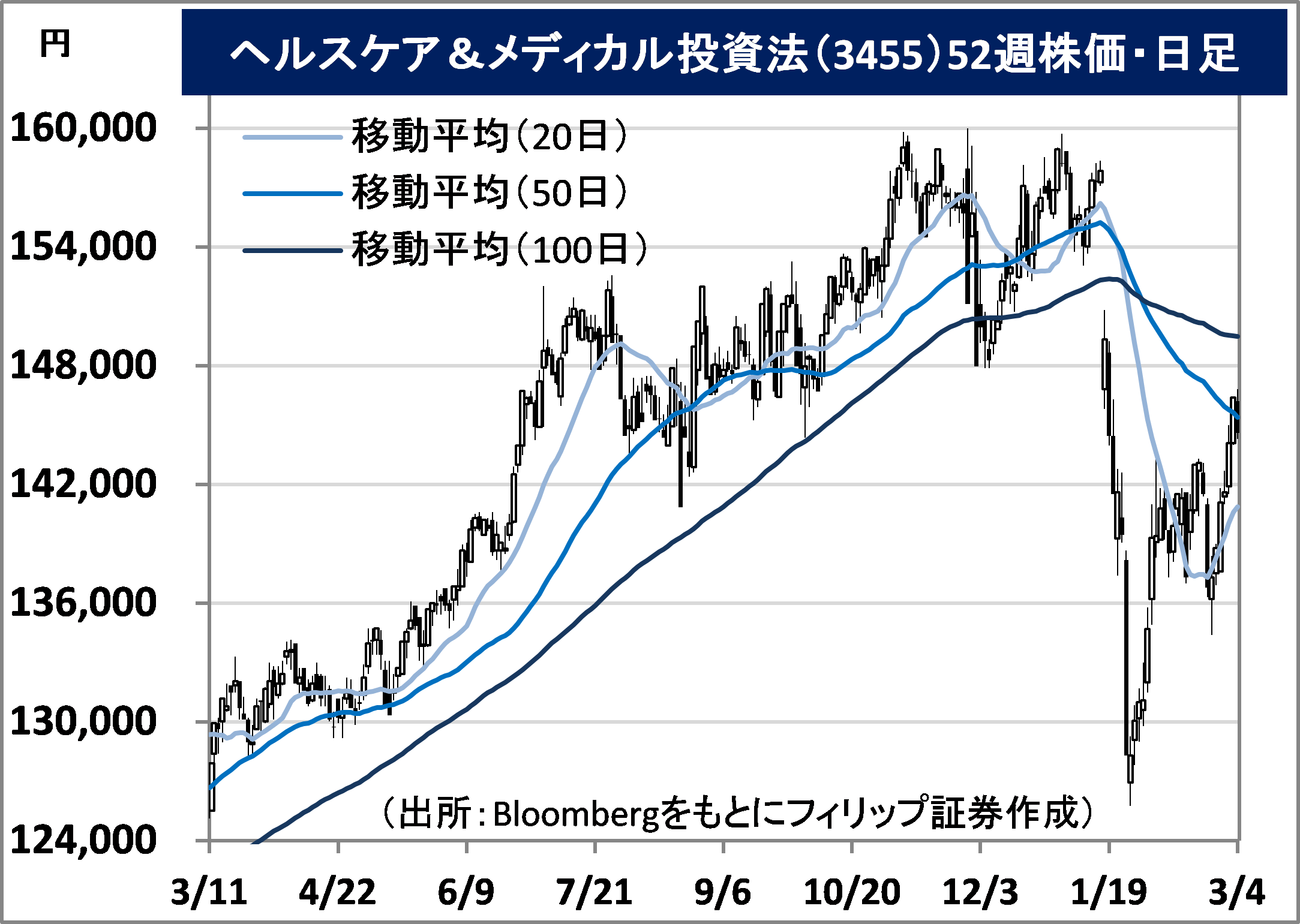

・A healthcare-focused J-REIT that has Sumitomo Mitsui Banking Corp and NEC Capital Solutions as major sponsors in addition to Ship Healthcare Holdings (3360), which engages in the nursing care business. Acquired a J-REIT-first hospital asset in 2017/11.

・For FY2021/7 (Feb-July) results announced on 14/9, operating revenue increased by 0.7% to 2.073 billion yen compared to the previous period (FY2021/1), operating income increased by 1.0% to 1.078 billion yen, and distribution per unit increased by 1.2% to 3,266 yen. Acquired “Nichii Home Nishikokubunji” for 720 million yen last March. Compared to the end of the previous period, the number of properties held at the end of July last year increased by one to 37, and the occupancy rate was 100%.

・Company has revised its FY(2022/7) plan (Feb-July) upwards on 17/1. Operating revenue is expected to increase by 14.3% to 2.37 billion yen (original plan 2.08 billion yen) compared to the previous period (FY2021/7), operating income to increase by 16.8% to 1.259 billion yen (original plan 1.061 billion yen), and distribution per unit to increase by 2.5% to 3,347 yen (original plan 3,238 yen). The distribution yield (based on the closing price on 3/3) based on the company forecast for FY2023/1 is 4.53%. After Russia’s invasion of Ukraine, US Treasury yields are trending lower, which will be a tailwind for J-REITs.

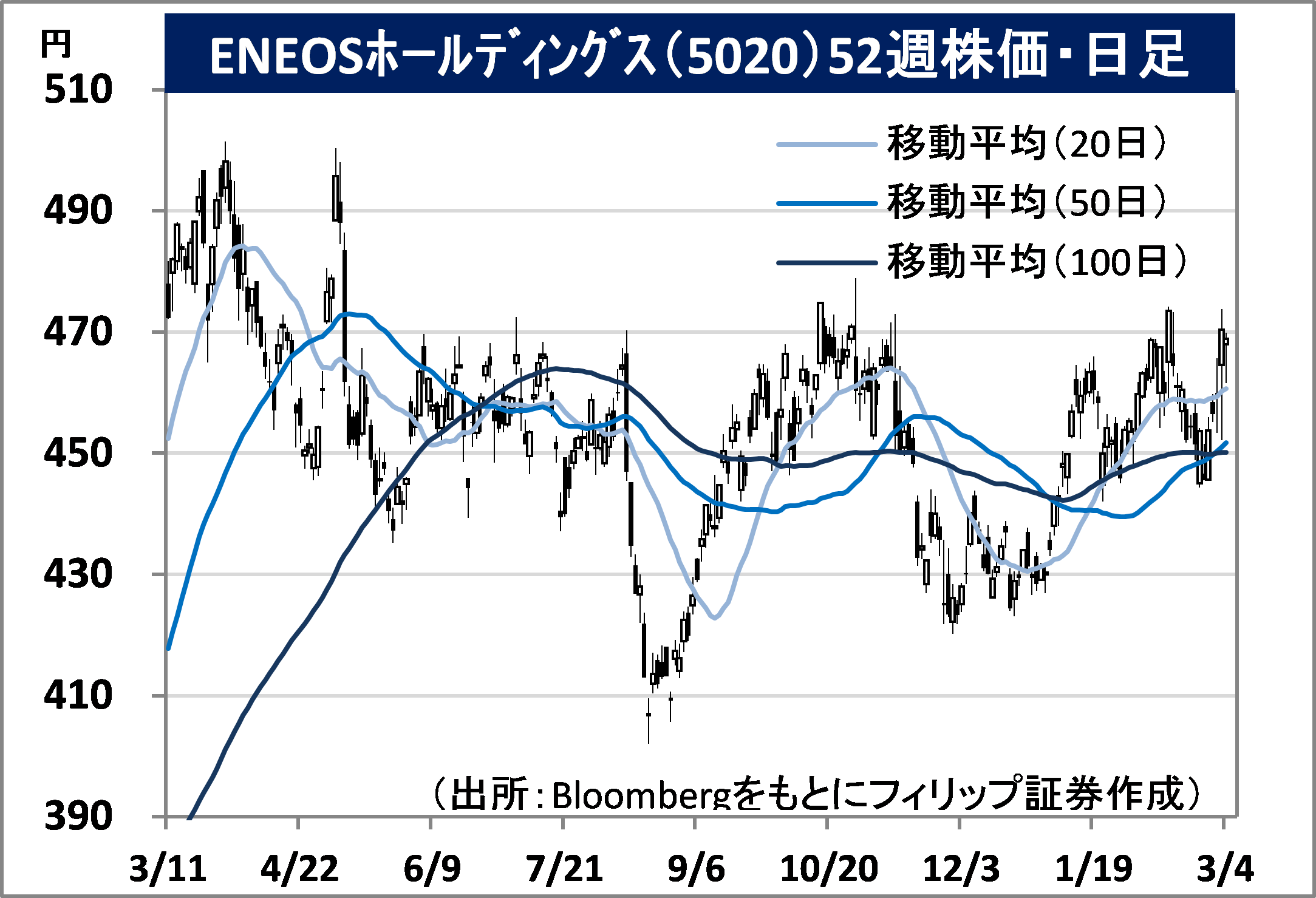

・Established as JX Holdings in 2010 through the business integration of Nippon Oil Corp and Nippon Mining Holdings. Merged with TonenGeneral Sekiyu in 2017 and changed its name to the current one in 2020. Leading petroleum wholesaler with 50% domestic market share.

・For 9M (Apr-Dec) results of FY2022/3 announced on 10/2, net sales increased by 42.2% to 7.6313 trillion yen compared to the previous period, and operating income increased 4.0 times to 530.1 billion yen. Among the three main business segments, sales in “Energy” increased 46.9% Y-o-Y to 6.1689 trillion yen, “Oil / Natural Gas Development” increased 2.1 times to 161.4 billion yen, and “Metals” grew 28.5% to 983.5 billion yen.

・For its full year plan, net sales is expected to increase by 34.5% to 10.3 trillion yen compared to the previous year, operating income to increase by 84.9% to 470.0 billion yen, with annual dividend of 22 yen. In addition to the expected benefits of soaring crude oil prices, company completed the acquisition of renewable energy company Japan Renewable Energy in January of this year. During this period when global supply and demand for aircraft titanium are expected to tighten due to economic sanctions against Russia, company has under its umbrella Toho Titanium (5727), a major titanium smelter.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: