|

Report type: Weekly Strategy |

“From the Perspective of Extended “Semi-emergency Coronavirus Measures”, Sports Betting and Japanese Stocks”

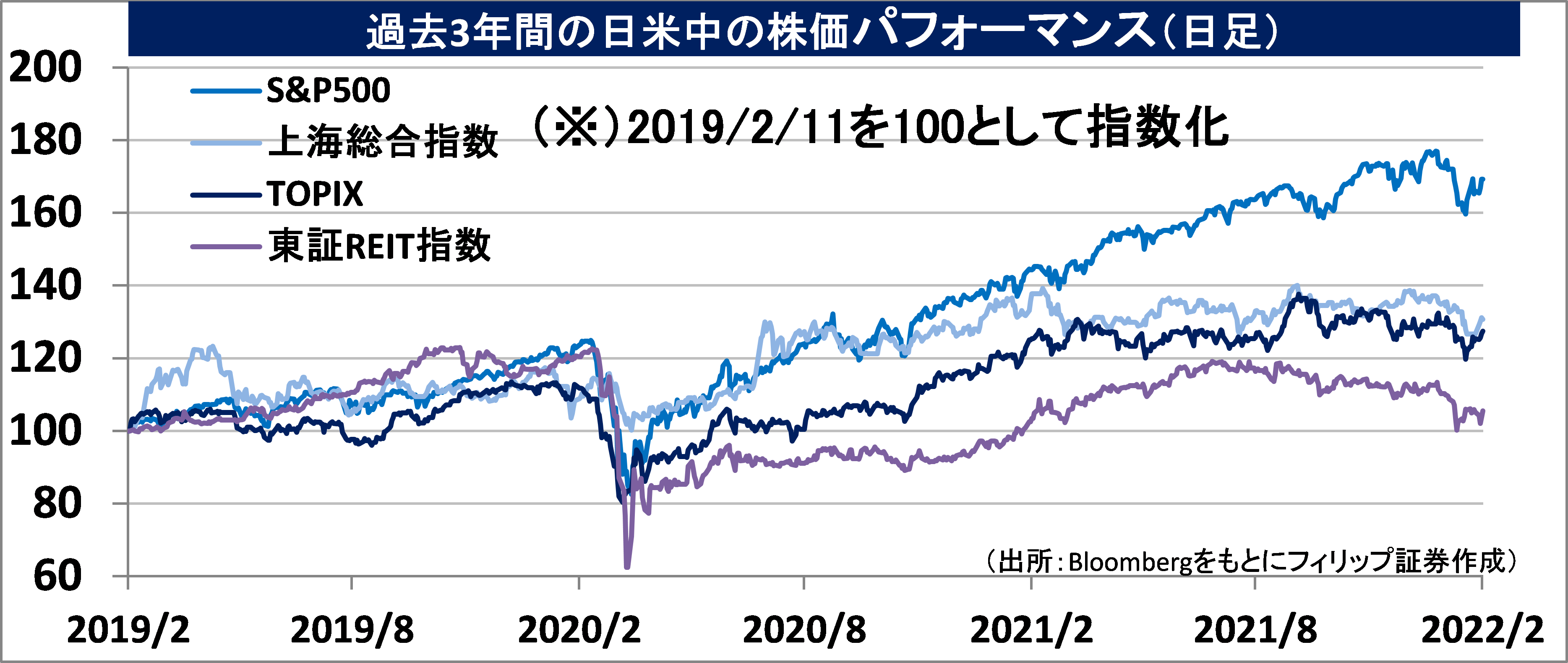

On 9/2, in response to the spread of infection of the COVID-19 Omicron variant, the Japanese government extended the deadline for the “semi-emergency coronavirus measures” for 13 prefectures such as Tokyo to 6/3, which was also additionally applied to Kochi prefecture. Although up to last year, in response to news such as this, the Japanese stock market had a strong tendency of being sold from concerns on the negative impact on the Japanese economy and delays in the normalisation of economy, the current situation appears different. Against the backdrop of difficulties in further significant sale in the supply and demand aspect, such as the unsettled buying balance of arbitrage and unsettled selling balance of arbitrage of the Nikkei average shifting to low levels, firstly, we can consider one of the factors for it to be that the prefectures are fully cooperating with F&B outlets, etc. on the call for cooperation on rules, such as on reduced operational hours and the provision of alcoholic beverages, etc., and risks of bankruptcy are being reduced due to the provision of assistance funding to business operators that meet the provision criteria. This is why business operators are somewhat able to accept the semi-emergency coronavirus measures and declarations of a state of emergency, etc.

Next, in the U.S., as of 8/2, the number of COVID-19 infections on a 7-day moving average fell to under 1/3 of the level of the peak in mid-January. With state after state removing the mandate for masks to be worn in schools and outdoors, another factor that can be considered is that travel and leisure-related stocks are being bought. This is why in Japanese stocks as well, enterprises that run F&B outlets, izakayas, karaokes and amusement parks, etc. and enterprises that easily benefit from increased travel and leisure, such as public transport and the air transport industry, also tended to have an influx of anticipated purchases. While there are mitigated risks in terms of business performance due to benefits and subsidies from the government, perhaps there is room to consider investment in stocks that will benefit from the resumption of the economy.

With the growing tendency of trends in stocks to buy in the U.S. stock market reflecting in Japanese stocks as well, from the perspective of Japanese stock investment, there is also an increasing need to observe trends in U.S. stocks. In the U.S., since the decision by the Supreme Court of the United States to leave the decision on the legalisation of sports betting (gambling) to each state in 2018, in January this year, New York was the 18th state in the U.S. to officially approve it. Voting on its legalisation in California, which has the largest population in the U.S., is expected to take place next year as well. Professional American football NFL is also designating their official betting partner. The “Superbowl” held on 13/2 is also a subject of betting and will likely be more hyped than previous years. Also, enterprises conducting sports commentary data and analysis services will also likely be promising.

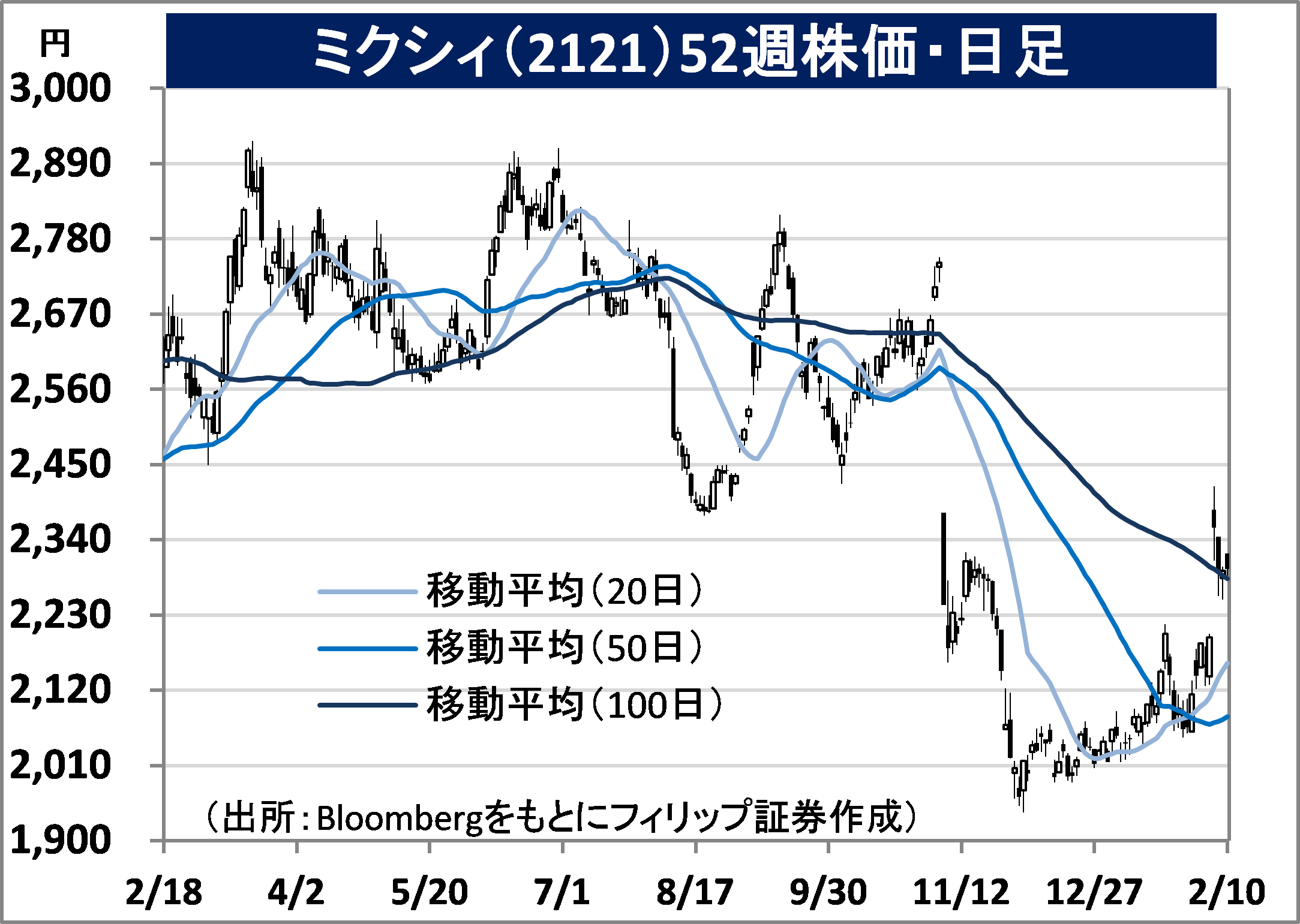

In Japan as well, there has been an emergence of enterprises, such as mixi (2121), that focus their efforts on the platform management of national bicycle race and auto race ticket betting. The company’s proactive efforts, such as the acquisition of local 5G radio communication system licenses for the purpose of broadcasting exciting footage from bicycle race events, have gone beyond even U.S. online casino enterprises and is garnering attention.

In the 14/2 issue, we will be covering mixi (2121), Komeda Holdings (3543), UACJ (5741)and Japan Pulp and Paper Company Limited (8032).

・Operates the social media service “mixi” after its establishment in 1996. Has been offering the “Monster Strike” mobile game since 2013. Operates the digital entertainment business, sports business and lifestyle business.

・For 9M (Apr-Dec) results of FY2022/3 announced on 4/2, net sales decreased by 7.6% to 81.089 billion yen compared to the same period the previous year and EBITDA decreased by 33.9% to 12.289 billion yen. Despite their mainstay digital entertainment business being sluggish, the sports business involving sports entertainment and national games had a 45% increase in revenue and the lifestyle business that involves image and video sharing apps, etc. had a 43% increase in revenue.

・Company revised its full year plan upwards. Net sales is expected to decrease by 6.1-3.1% to 112-115 billion yen compared to the previous year (original plan 105-110 billion yen) and EBITDA to decrease by 48.4-44.7% to 14-15 billion yen (original plan 6-9 billion yen). They are expecting cost reduction in their sports business by increasing marketing strategy efficiency in the app “TIPSTAR”, which has 365-day live videos, etc., as well as bicycle racing, the new bicycle race PIST6 and auto race online betting for smartphones which are being rolled out in partnership with JKA.

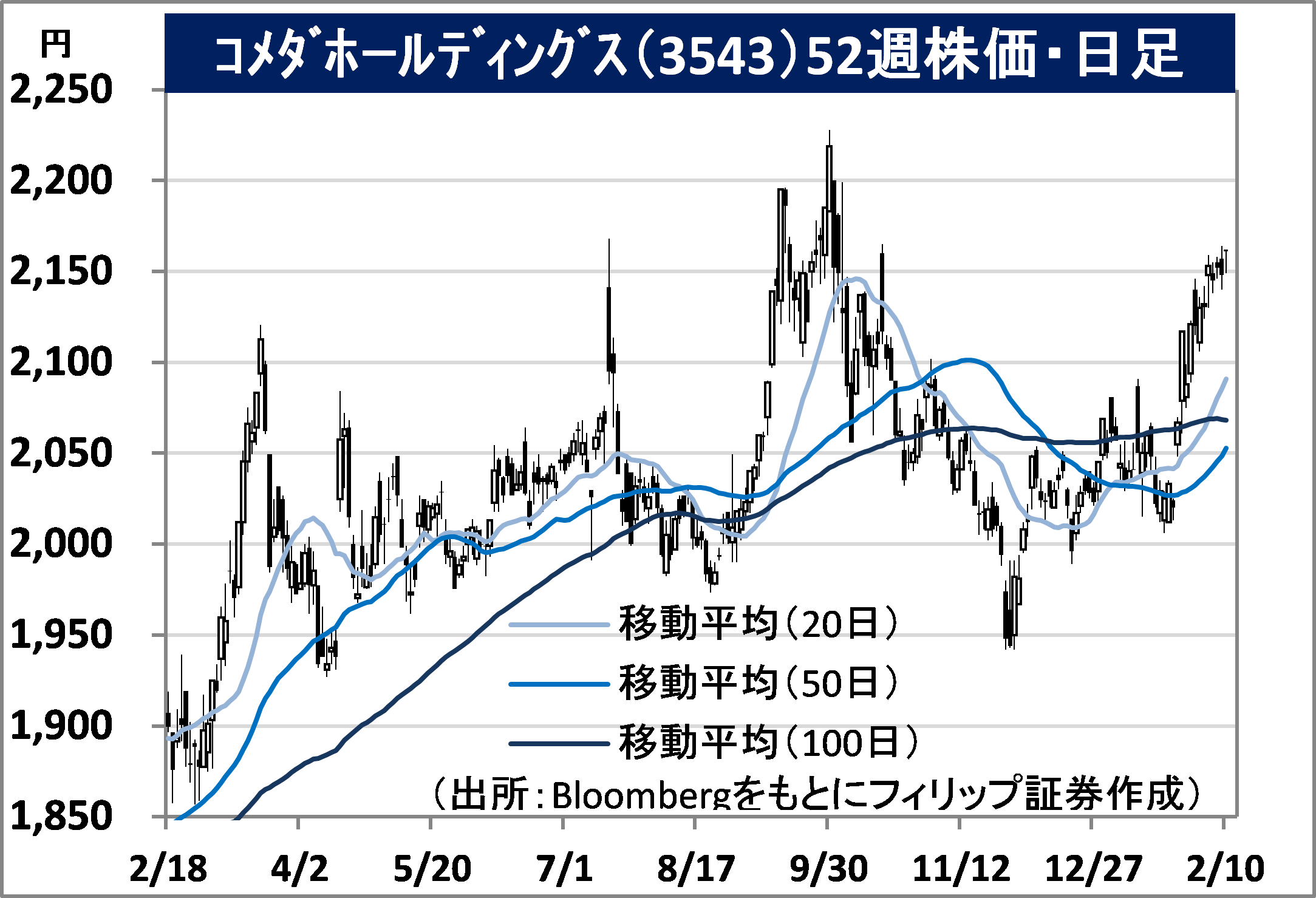

・Began in 1968 as a coffee shop that opened in Nagoya. Expands a franchise chain business across Japan and owns brands such as “Komeda Coffee Shop”, “Okagean”, “Soft & White Coppe-pan”, “Komeda Stand” and “Bakery Ademok”.

・For 9M (Mar-Nov) results of FY2022/2 announced on 12/1, sales revenue increased by 16.1% to 24.652 billion yen compared to the same period the previous year and operating income increased by 36.8% to 5.847 billion yen. Also due to the introduction of new products that use trending ingredients, same-store sales involving wholesale sales in franchise chain stores increased by 12.7%. Number of stores across all brands at end November last year increased by 35 compared to the previous year-end to 949 stores.

・For its full year plan, sales revenue is expected to increase by 14.2% to 32.9 billion yen compared to the previous year and operating income to increase by 31.6% to 7.25 billion yen. According to Tokyo Shoko Research, the number of corporate bankruptcies in 2021 was the lowest in the past 50 years which was contributed by financial support from the government, however, the number of coffee shops that went out of business has hit a record high. The company is attempting to accelerate expansion of their market share. They have a stable supply of coffee beans from their capital and business partner, the Singaporean agricultural produce trading company, Olam, under Mitsubishi Corporation (8058).

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: