|

Report type: Weekly Strategy |

“A Resolution to the Sense of Being Overvalued, the Ongoing Adjustment in Margin Debt Balance and the IMF World Economic Outlook”

For the global stock market, following growing tension in the Ukraine situation concerning Russia, the uncertain state of mind of market participants appears to have been exacerbated by the close entwinement of concerns on whether there will be an increase in global inflation risks due to the increase in the market price of grains, such as wheat, and the increase in energy prices via concerns on the supply of natural gas; and concerns of a balance sheet reduction and the increase in interest rates to curb inflation by the FRB through the press conference with U.S. FRB Chair Powell and the U.S. FOMC (Federal Open Market Committee) statement announcement on 26/1.

The Japanese stock market turned out to be a bearish market between the 24th and 27th where the Nikkei average lowered its daytime highs and lows day after day, and the closing price on the 27th ended up falling greatly by 841 points compared to the previous day to 26,170 points. One of the reasons that can be considered is the concentration in selling in the Japanese stock market from the perspective of liquidity with the large-scale holiday, the Chinese Spring Festival (Chinese New Year), from 1/2, and that it was the last business day at the end of the month. The Nikkei average at this level has a 1.19 times P/B ratio (price-to-book ratio), which is a weighted average such as of market capitalisation, which more or less coincides with the average level of the past 10 years excluding March 2020. Also, even when judging from a period of 6 years until around February 2020, a P/E ratio lower than 13 times in weighted average can also be considered as an undervalued level that is lower than average.

The “ratio of margin balance”, which is obtained by dividing the margin debt balance of system margin trading by the margin selling balance, reversed to increase after declining to under 2.0 times in March 2020 and increased up to 5.7 times on the basis of 21/1. This is a high level that was last seen in Mar-Apr 2018 and the amount of the margin debt balance is also of a high level similar to the latter half of 2018. Although there has been progress in adjustment in the unsettled buying balance and unsettled selling balance of arbitrage trading involving the Nikkei average’s futures and options trading, it is thought that a major factor was that there had yet to be progress in adjustment in the supply and demand aspect in margin transactions.

For the 2022 World Economic Outlook by the IMF announced on 25/1, while there was a downward revision across the board with worldwide GDP decreasing by 0.5 points compared to the previous round (as of October) to 4.4%, the U.S. decreasing by 1.2 points to 4.0%, the Euro area decreasing by 0.4 points to 3.9% and China decreasing by 0.8 points to 4.8%; Japan had an upward revision of 0.1 point to 3.3%. Although there was the aspect of a reactionary increase from restrictions in behaviour, such as repeated measures to prevent the spread and declarations of a state of emergency last year, while monetary tightening became mainstream in terms of the response towards inflation following global economic expansion, the Bank of Japan’s demonstration of their stance in continuing economic support via vigorous monetary easing is also being reflected. Perhaps there is an increasing possibility of global money, which does not favour inflation risks, escaping to low inflation markets. As of now, we believe that there would be no need to change the outline in the “2022 Stock Market Forecast” indicated in the 27th December 2021 (year-end special) issue of our weekly report.

In the 31/1 issue, we will be covering BASE (4477), Toei Animation (4816), Furuya Metal (7826)and Canon Marketing Japan (8060).

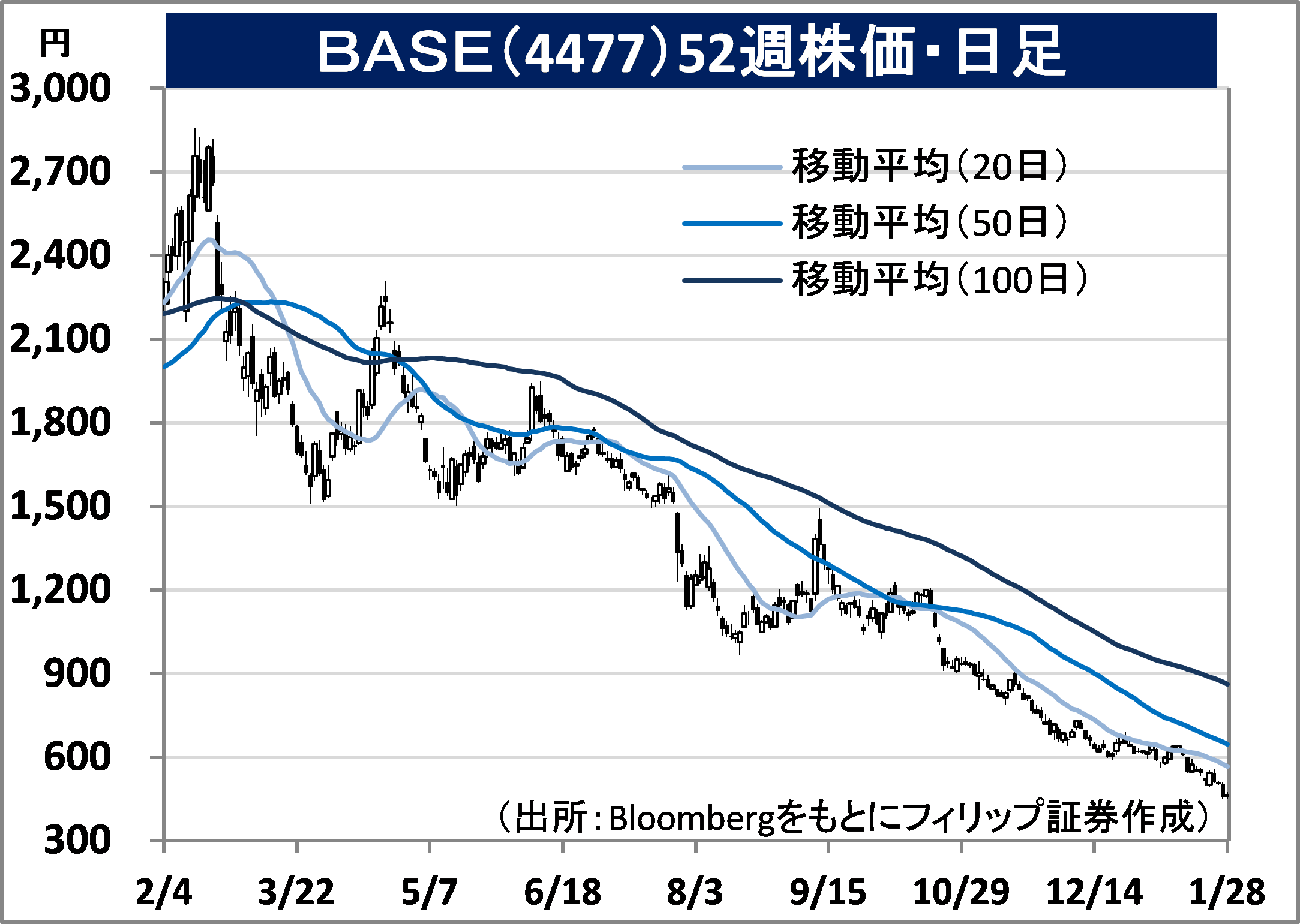

・Established in 2012. Operates “BASE”, an e-commerce (EC) platform for individuals and small-scale business operators. Runs a financing service (debt purchasing), online payment service (the PAY business) and an EC platform (the BASE business).

・For 9M (Jan-Sep) results of FY2021/12 announced on 12/11, net sales increased by 0.9% to 9.6 billion yen compared to the same period the previous year and operating income increased by 5.4% to 2.186 billion yen. Despite there being movements involving postponements and reductions in some projects due to intermittent announcements of a declaration of a state of emergency, measures involving the expansion and continuance of existing projects and new project acquisitions, etc. have been successful, which secured an increase in income and profit.

・For its full year plan, net sales is expected to increase by 4.8% to 13 billion yen compared to the previous year and operating income to increase by 20.1% to 2.929 billion yen. In September last year, they partnered with “TikTok”, a short film video platform reinforcing their influence on consumption. They are aiming for BASE member stores to carry out smooth sales promotion and customer attraction by utilising TikTok. There will likely be expectations of an increase in the transition of business operators from mall-type EC, such as Rakuten and Amazon, to in-house direct sales EC using the company’s or Shopify’s system.

|

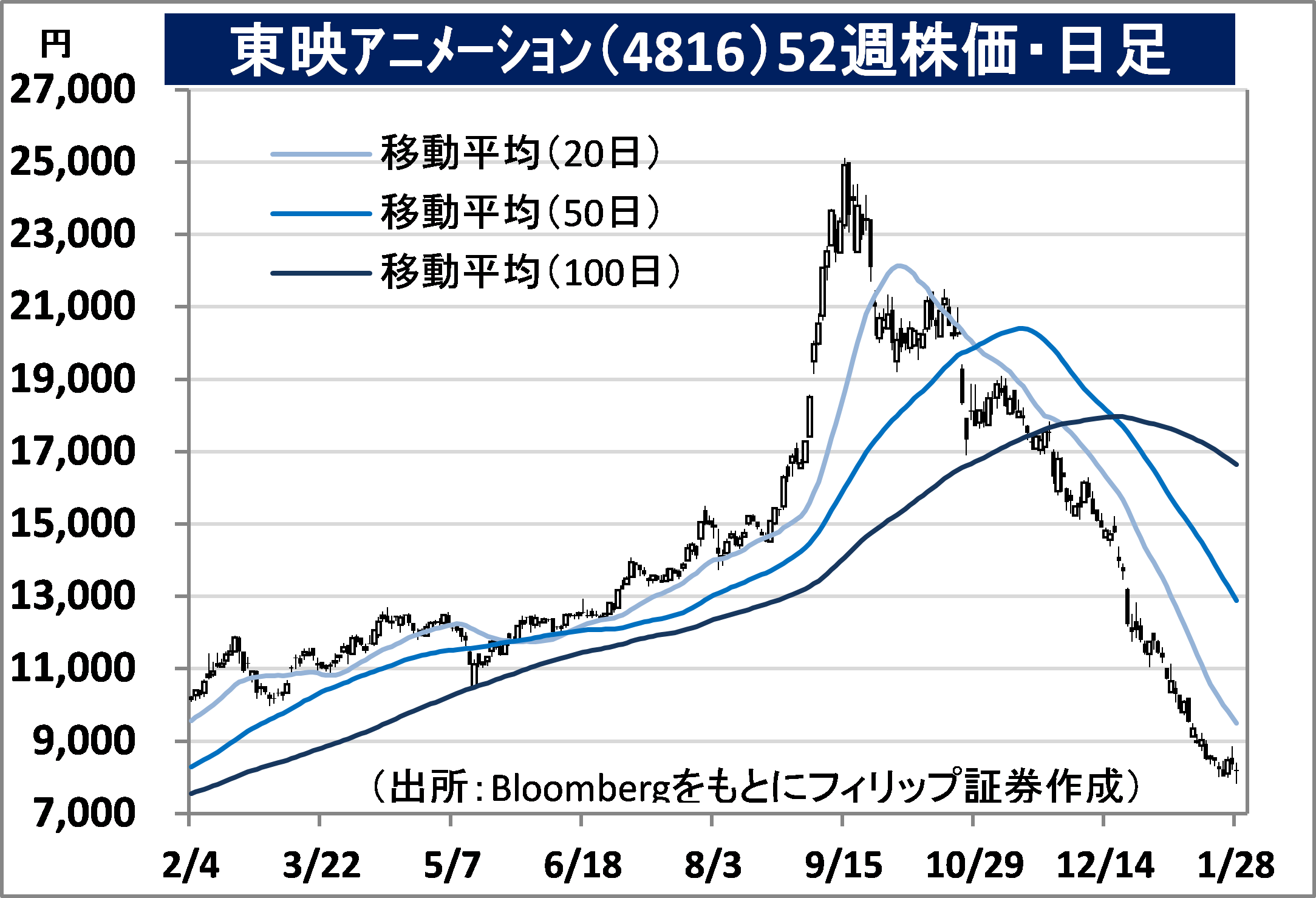

² Toei Animation Co., Ltd. (4816) 8,170 yen (28/1 closing price) ・Established in 1948. Handles the video production and sales business involving planning, production and the sale of broadcasting rights of various anime works, the copyright business which grants licenses of characters and obtains royalties, and the product retail business involving the sale of character products. ・For 9M (Apr-Dec) results of FY2021/3 announced on 27/1, net sales increased by 13.0% to 42.522 billion yen compared to the same period the previous year and operating income increased by 20.4% to 14.331 billion yen. Good performance in operation of the highly-profitable video distribution in Japan and overseas as well as the increase in sales of merchandising rights and rights to the creation of games of “Dragonball” and “One Piece” in the overseas copyright sector have contributed to business performance. ・Company revised its full year plan upwards. In response to good performance in the sale of distribution rights of popular series in Japan as well as overseas in the copyright business, net sales is expected to increase by 6.8% to 55.1 billion yen compared to the previous year (original plan 51 billion yen) and operating income to increase by 8.4% to 16.8 billion yen (original plan 14.5 billion yen). TV Asahi Holdings (9409) began the sale of digital trading cards using Toei robot animation works, such as “Chodenji Robo Combattler V”, as NFTs (non-fungible tokens). |

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: