Report type: Weekly Strategy

” Rise in Interest Rates Under Monetary Easing and Attention on Stocks Related to Boeing”

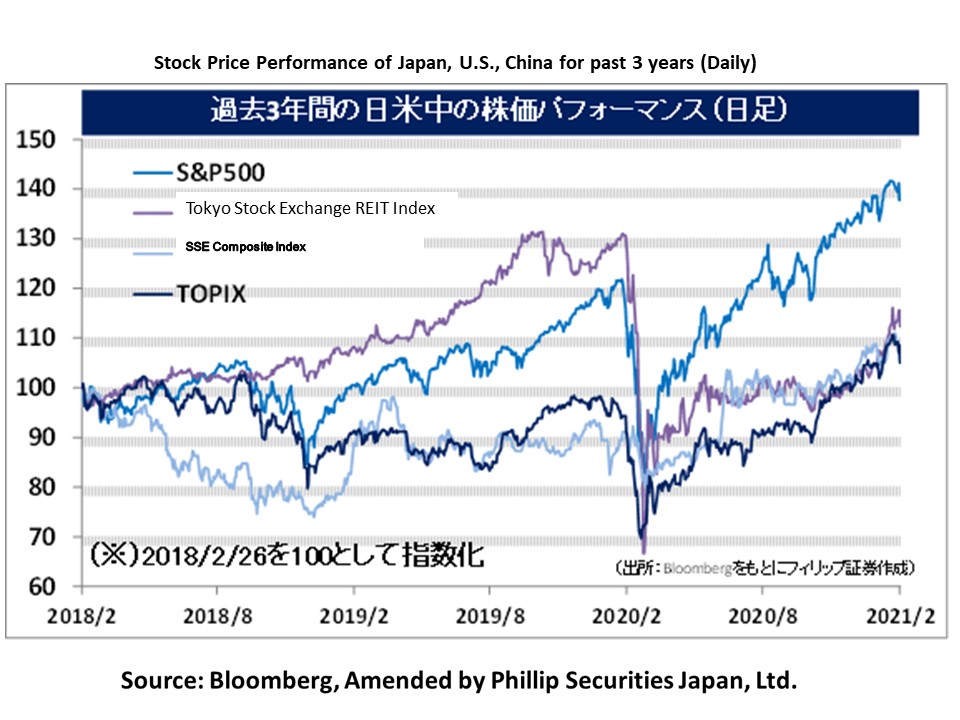

In the previous week’s 22nd February 2021 issue of our weekly report, we mentioned that there is an aspect where the conditions are met for the stock market to shift to an adjustment decline due to the Nikkei average’s weighted average P/B ratio (price-to-book ratio) reaching a high level that exceeded 1.3 times which was last seen 3 years ago on 2nd February 2018, and the accelerated increase in U.S. long term interest rates similar to 3 years ago. With the growing prediction in the market on early monetary tightening as a result of the emergence of risks of a price upturn in the U.S., U.S. FRB Chair Powell stressed in his testimony at Congress on 23-24/2 that there will be no changes to the monetary policies until there are clear improvements in the economy. Regardless, it did not stop the increasing yield trend in the U.S. bonds market, with U.S. 10-year government bonds reaching 1.6% at one point on 25/2. Perhaps we can perceive the significant increase even in the short-term 2-year and 5-year bonds, which tend to be linked with the FRB’s monetary policies and policy interest rates, to be excessive risk-off sentiment. The rise in risk-off sentiment also influenced the Japanese stock market, and the closing price for the Nikkei average fell drastically by 1,202 points to 28,966 points on 26/2 compared to the previous day.

In contrast to the gentle monetary easing stance taken by the U.S. FRB in 2018 to reduce the total amount in the balance sheet, currently, they are keeping a strong stance on monetary easing in order to increase the total amount in the balance sheet via bond purchasing. In that sense, for Japanese stocks, even if an adjustment decline occurs in the stock market, there is a high chance that it will end in the short-term earlier than that in Spring 2018. If there is an overlap of a decline due to seasonal factors, such as selling off in order to review holdings of cross-shareholdings as a measure for the end of period settlement in March, etc., it could be taken as an opportunity for investors to buy from the middle of the year to the year end.

The increase in U.S. long term interest rates which brought about fluctuations in the stock market is a reflection of expectations towards a normalisation of the economy from the popularisation of the COVID-19 vaccine and the conclusion of additional large-scale economic measures in the U.S. In that sense, for the future stock market, it is believed that there will be a high likelihood of focus on the increase in demand for aircrafts along with a travel demand. Amongst them, regarding aircraft demand, it is said that aircraft production is an extensive industry similar to automobiles with many corporations in charge of the manufacture of its components and parts, and eventually forms the industry structure that assembles Boeing and Airbus. Especially for Boeing, there are numerous stocks that are called “Boeing-related”, such as 3 Japanese companies which are Mitsubishi Heavy Industries (7011), Kawasaki Heavy Industries (7012) and Subaru (7270), which develop and manufacture the wings of Boeing aircrafts and a large percentage of its airframe, in addition to Toray Industries (3402), which carries out a joint development of carbon fibres for main structural parts, etc. There is a possibility that the recovery in aircraft demand will become a driving force for improvement in business performance for Japanese corporations that have had their business performance affected by the fall in demand for aircraft components.

In the 1/3 issue, we will be covering Future (4722), Nihon Dempa Kogyo (6779), ShinMaywa Industries (7224), and Furuya Metal (7826).

・Established in 1989. Mainly handles digital transformation (DX) for client corporations with a focus on work systems, and expands the IT consulting & services business and the business innovation business.

・For FY2020/12 results announced on 4/2, net sales decreased by 2.4% to 44.311 billion yen compared to the previous year and operating income decreased by 19.8% to 5.235 billion yen. Although there was an increase in income and profit in their business innovation business due to an expansion of online teaching and indoor training demand, IT investment curbs in some clients, etc. in their IT consulting & services business influenced the decrease in sales and income.

・For its FY2021/12 plan, net sales is expected to increase by 7.2% to 47.5 billion yen compared to the previous year and operating income to increase by 36.6% to 7.15 billion yen. Their subsidiary, Future Architect, implemented the financing support system “FutureBANK” successively to Chiba Bank in addition to the member bank, “TSUBASA Alliance”, which consists of 11 banks with The Gunma Bank becoming a member in December last year. Also, on 15/1, the subsidiary announced a business alliance with SBIHD (8473) on the development of an accounting system for local banks.

・Established in 1948. Carries out the integrated manufacture and retail of crystal oscillators, crystal devices such as crystal equipment, etc. and their applied equipment, as well as crystal-related products, such as crystal blanks (planks) and synthetic crystals. Company is No.2 in global shares for crystal devices.

・For 9M (Apr-Dec) results of FY2021/3 announced on 5/2, net sales decreased by 4.7% to 28.327 billion yen compared to the same period the previous year and operating income returned to profit from (5.48) billion yen the same period the previous year to 2.789 billion yen. Although in-vehicle net sales saw a sudden recovery in 3Q (Oct-Dec), the decline in 1Q (Apr-Jun) influenced the decrease in revenue. The reaction from carrying out a structural reform the same period the previous year contributed in terms of profit.

・For its full year plan, net sales is expected to decrease by 1.4% to 38.9 billion yen compared to the previous year and operating income to return to profit from (8.286) billion yen the previous year to 2.4 billion yen. In addition to an upward revision of net sales due to a continuous increase in orders received for in-vehicle, operating expenses are predicted to record 600 million yen as a result of bringing forward the structural reform. There is an expected increase in demand for crystal devices for 5G communication standards following the popularisation of 5G service worldwide. Current stock price is approximately at the level of 1/10 of its high in October 2007.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: