Report type: Weekly Strategy

”Stock price highs since August 1990 and semiconductor market outlook”

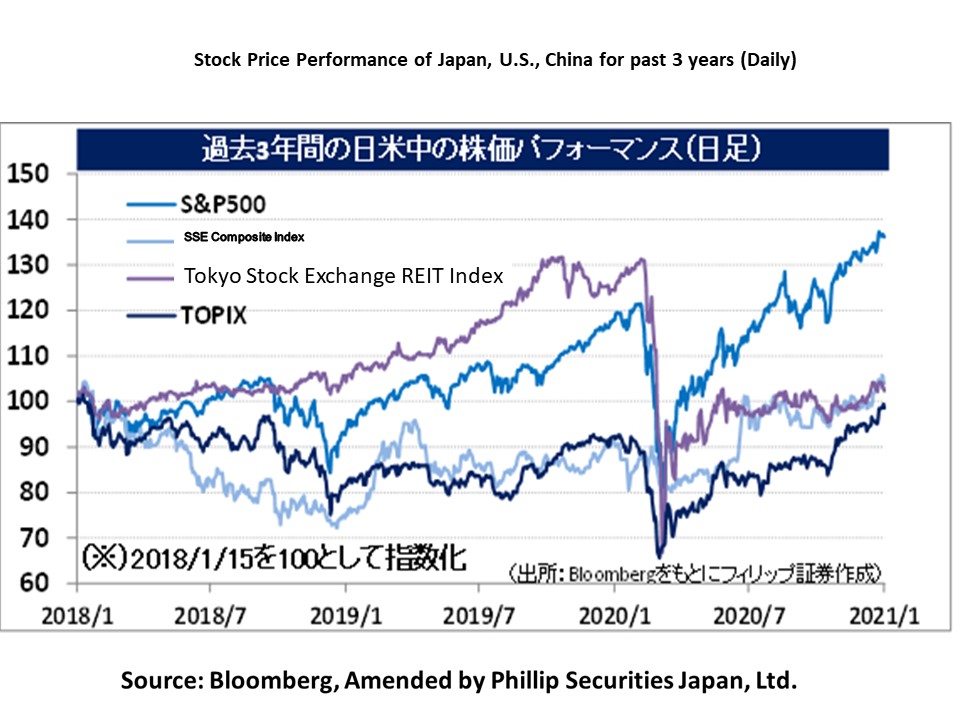

The Nikkei Average rose to 28,979 points during trading hours on 14/1, the highest level since August, 1990. August, 1990 was the time when, after the Iraqi forces invaded Kuwait, the UN Security Council adopted a resolution condemning the invasion and imposed economic sanctions on Iraq with a total embargo. At that time, there were headwinds in the stock market due to the intermittent tightening of monetary policies since the official discount rate hike in May, 1989. Currently, the BOJ under Governor Kuroda is continuing its unconventional monetary easing, and the weighted average net asset price (BPS) of the Nikkei Average, based on market capitalization, is hovering around 22,500 points. This is different from the “Heisei bubble” period when the Nikkei Average and its weighted average BPS were far apart.

On top of that, according to Bloomberg, comparing the current return on equity (ROE) of the Nikkei Average and TOPIX, that for the Nikkei Average and TOPIX was 6.02% and 4.25% respectively in 2020. In 2021, that for the Nikkei Average and TOPIX is expected to be 9.92% and 5.63% respectively. From a fundamental standpoint, it can be said that the Nikkei Stock Average is likely to outperform TOPIX.

At present, there is a noticeable trend in the Japanese stock market of a shift from focus until the end of last year on stocks related to hydrogen and EVs (electric vehicles) aiming at reducing greenhouse gas emissions, to stocks related to semiconductor manufacturing equipment which contribute significantly to the Nikkei Average due to semiconductor shortages and supply concerns. According to the latest forecast of the World Semiconductor Trade Statistics (WSTS), the year-on-year growth rate of the overall semiconductor market is expected to be 5.1% in 2020 and accelerate to 8.4% in 2021. According to the 2021 product forecast, discrete, optical-semiconductors, sensors, and ICs (integrated circuits) are all expected to grow by more than 7% year on year. In terms of IC category, analog, logic, and memory will grow by 8.6%, 7.1%, and 13.3% respectively, while microprocessors will grow by only 1.0%. In particular, shipments of 5G-compatible smartphones in 2021 are expected to more than double from the previous year. The manufacturing of SoCs (system-on-chips) for 5G smartphones will require 5nm (nano-meter) or 7nm miniaturization processes. The production capacity of Taiwan Semiconductor Manufacturing Company (TSMC), a semiconductor foundry, and ASML, an EUV (Extreme Ultraviolet) lithography equipment manufacturer, may therefore encounter supply constraints.

In ASEAN, harvesting has been delayed due to restrictions on the movement of foreign workers, and soaring market prices of agricultural products and vegetable oil due to supply shortages have boosted the performance of agricultural-related companies. If the acquisition of low-wage foreign workers through aggressive immigration policies becomes less likely in the future, we may see an end to deflation and an increase in inflation in a wide range of industries in many countries.

In the 18/1 issue, we will be covering NS Solutions (2327), Mitsubishi Chemical Holdings (4188), CYBERDYNE (7779), and AEON Financial Service (8570).

・Established in 1980 with Nippon Steel as the parent company. Company is a systems integrator of the Nippon Steel (5401) group, but about 80% of its sales come from systems development and consulting for companies and government agencies other than its parent company.

・For 1H (Apr-Sep) results of FY2021/3 announced on 27/10, net sales decreased by 12.9% to 119.068 billion yen compared to the same period the previous year, and operating income decreased by 21.4% to 11.149 billion yen. Both sales and profits decreased due to the negative repercussion from the large PCB project in the same period of the previous year, but 2Q (Jul-Sep) sales increased 10.2% QoQ and operating income increased 18.5% due to the success of responding to remote and non-contact IT needs.

・For its full year plan, net sales is expected to decrease by 7.2% to 255.0 billion yen compared to the previous year, and operating income to decrease by 15.8% to 23.9 billion yen. In addition to working on the digitalization of the telework environment and contract / decision-making operations, company has also begun verifying the application of a self-operated wireless network for local 5G at the Muroran Works of Nippon Steel, with the aim of realizing digital transformation (DX) at manufacturing sites. President Morita said, “2021 will be the dawn of full-fledged DX,” and company is aiming to provide DX support to customers in a wide range of industries.

・Established in 2005 through a joint stock transfer between Mitsubishi Chemical and Mitsubishi Pharma. Has subsumed Mitsubishi Plastics, Mitsubishi Rayon, Taiyo Nippon Sanso, Mitsubishi Tanabe Pharma and others as wholly-owned subsidiaries. Operates three business fields, namely Performance Products, Industrial Materials, and Healthcare.

・For 1H (Apr-Sep) results of FY2021/3 announced on 4/11, sales revenue decreased by 17.7% to 1.5048 trillion yen compared to the same period the previous year, and core operating income excluding non-recurring factors decreased by 58.2% to 54.639 billion yen. Sluggish demand, especially for automotive applications, had a negative impact. 2Q (Jul-Sep) QoQ sales rose 8.2% on the back of a recent pickup, and core operating income rose 2.6 times.

・Company has revised its full-year plan downwards on 4/11. Core operating income remains unchanged at 140.0 billion yen, down 28.1% Y-o-Y, but sales are expected to fall 11.3% Y-o-Y to 3.175 trillion yen (original plan 3.334 trillion yen) due to lower-than-expected market conditions for MMA, an acrylic resin raw material. In addition to promoting a project utilizing CO2 as a resource through artificial photosynthesis using photocatalysts, the 3D printing resin business is also expected to expand in Europe and the United States.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: