Report type: Weekly Strategy

2nd Wave Risks Are Triggering a Shift Towards the Era of the Regional

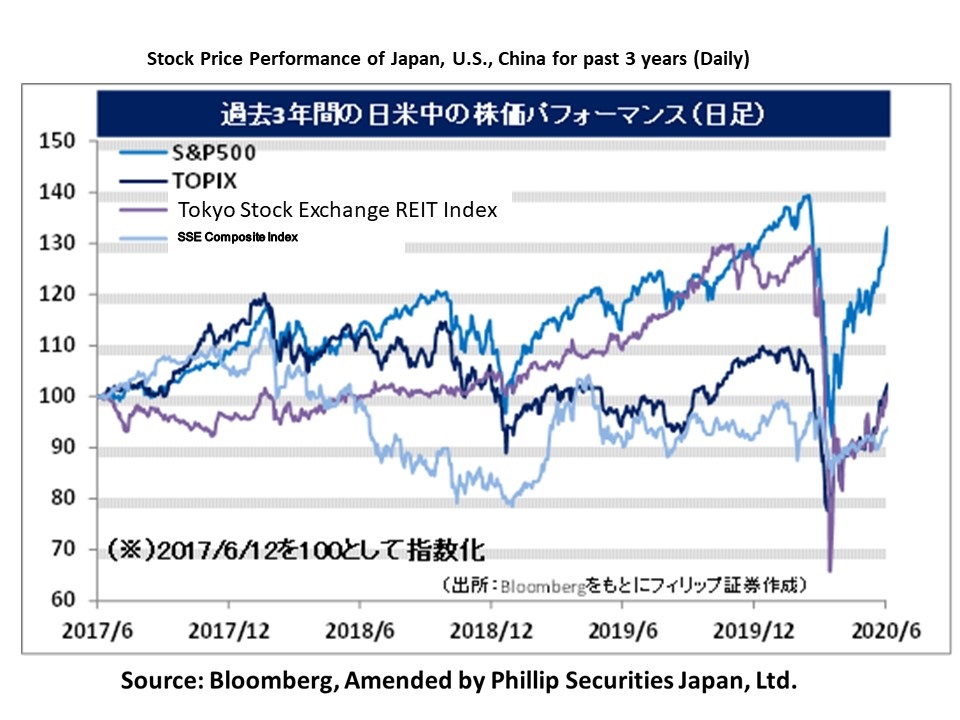

As a result of significant improvements to the unemployment rate and nonfarm payroll employment in the U.S. employment statistics for May announced on 5/6 which defied market predictions, in the Japanese stock market, the Nikkei average rose to 23,178 points on 8/6. Following the global resumption of economic activities, despite there being a lookout for mainly stocks that are sensitive to the economy, the Nikkei average closed at under 22,500 points on 11/6, and on 12/6, taking over the sharp decline of 1,861 points in the U.S. Dow Jones Industrial Average on the previous day, it fell to 21,786 points after opening, etc., which was shift that incorporated the possibility of violent fluctuations.

With the increase in the number of COVID-19 infections in the U.S. mainly in states which decided to reopen the economy in the early stages, it is said that the rising alert towards the 2nd wave was the main reason for the sale of U.S. stocks. On the other hand, in Japan, Tokyo made the decision to lift the “Tokyo Alert” on 11/6 and announced the transition to “Step 3” in the roadmap towards easing the suspension of businesses. Based on the guidelines drawn up by the country’s policies and industry organisations, the call for business suspension was completely lifted from 19/6. In addition to the relatively low death count from COVID-19 infections in Japan, even after lifting the state of emergency across the country on 26/5, there has been no prominent increase in the number of infections. If overseas stocks other than U.S. stocks are sold due to 2nd wave risks, there is the possibility that Japanese stocks would be chosen as a place of refuge.

However, as long as 2nd wave risks remain in major developed countries, we are unable to expect an active flow in the freedom of people, things and money in the global economy as it was before the COVID-19 catastrophe, and is likely to be in stagnation for the time being. The flow of capital in the stock market is also changing from “global to local”, and we can possibility expect a growing trend in the lookout for domestic demand stocks with low P/B ratio (price-to-book ratio). Also, we are seeing various changes in Japan in order to avoid the “3 types of proximities”, and it looks like it may take time for the “New Way of Life” to begin to take root. This could mean that aside from simply wearing masks or face shields and installing partition panels in restaurants, etc., people may also start to favour the life in local regions over the life in the city with mounting living expenses from a high population density. In particular, with some corporations continuing with telecommuting even after the state of emergency being lifted and people doubting the benefits of living close to their workplace, there is the possibility of the local-oriented mindset becoming a major trend.

If we look at local regions, in addition to the vitalisation of start-ups of regional trading company businesses by regional banks, power companies are being called to separate their power transmission and distribution business as a result of the Electricity System Reform implemented in Apr 2020, and demands have been made for fair purchases of renewable energy produced and consumed locally. We can then perhaps see a demand for advancement in movements involving regional sovereignty in terms of politics.

In the 15/6 issue, we will be covering Iida Group Holdings (3291), Rengo (3941), Information Services International-Dentsu (4812), and SBI Holdings (8473).

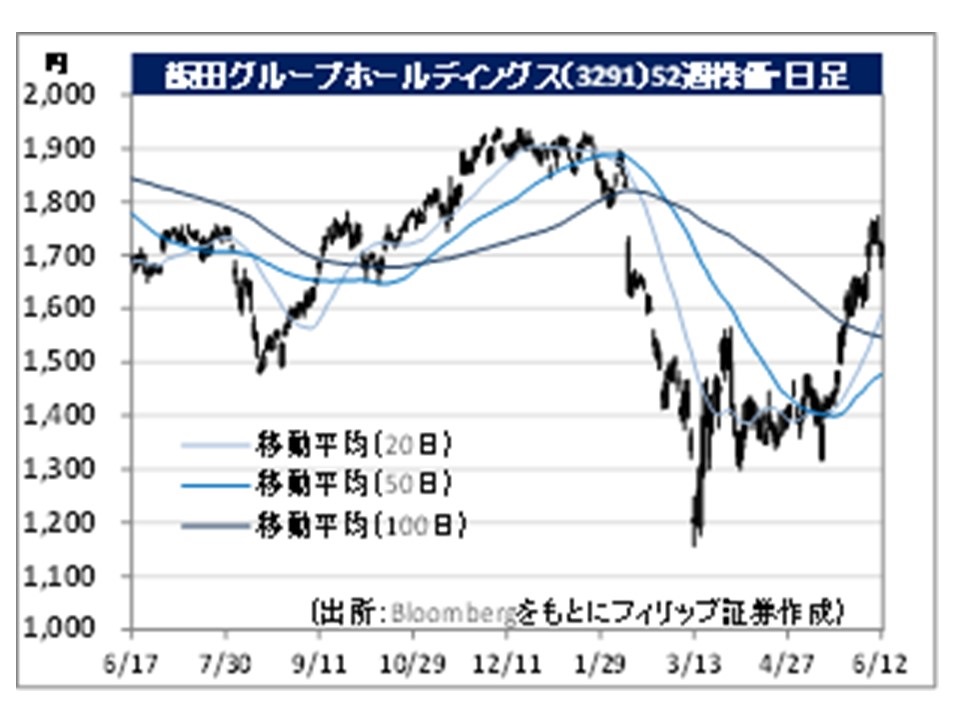

・Started in Oct 2013 as a joint stock holding company from a merger of 6 listed housing companies, which are Hajime Construction, Iida Sangyo, Touei Housing, Tact Home, Arnest One and ID Home. Holds approximately 30% of shares in the country for detached housing lots.

・For FY2020/3 results announced on 15/5, sales revenue increased by 4.2% to 1.402 trillion yen compared to last year and operating income decreased by 14.0% to 83.513 billion yen. Despite success in insourcing for the housing-related business and an expansion of the service area through an effective expansion of their operating base which led to an increase in revenue, there were also expenses following development of infrastructure to secure new revenue sources, which led to a decrease in profit.

・Their FY2021/3 plan is undecided due to the inability to reasonably calculate effects from COVID-19 at the moment. With apartment prices in the city centre remaining at a high, as a result of telecommuting becoming commonplace due to the COVID-19 catastrophe, while more time is spent with the family, there is also the need to secure space for work, and demand is beginning to recover for detached houses in the suburbs with relatively cheaper retail prices. This would likely benefit the company who holds the top shares in the market.

・Founded when Teijiro Inoue started the first cardboard business in Japan in 1909. Manages the paperboard and paper processing-related business which handles paperboard and cardboard, as well as the soft packaging-related business, the heavy packaging-related business, the overseas-related business and other businesses.

・For FY2020/3 results announced on 13/5, net sales increased by 4.7% to 683.78 billion yen compared to the previous year and operating income increased by 63.0% to 41.227 billion yen. Demand for online retail and home delivery of cardboard and demand for daily necessities, foodstuff with soft packaging and paper containers performing strongly, in addition to lowered raw material prices and a revision in product prices, etc. have led to an increase in income and profit.

・For its FY2021/3 plan, net sales is expected to increase by 3.3% to 349 billion yen compared to the previous year and operating income to increase by 5.8% to 20 billion yen. Company is developing and producing partitions made of cardboard which can be used in the classrooms of schools, etc. It would be used by folding it in three and placed standing up, with large holes on the right, left and front attached with a transparent film to enable viewing of the other person’s face. With the reduction in the “3 types of proximities” in schools and offices, etc., we can expect an increase in demand for cardboard which is in line with the “New Way of Life”.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: