Report type: Weekly Strategy

Additional Monetary Easing by the Bank of Japan and the COVID-19 Drug

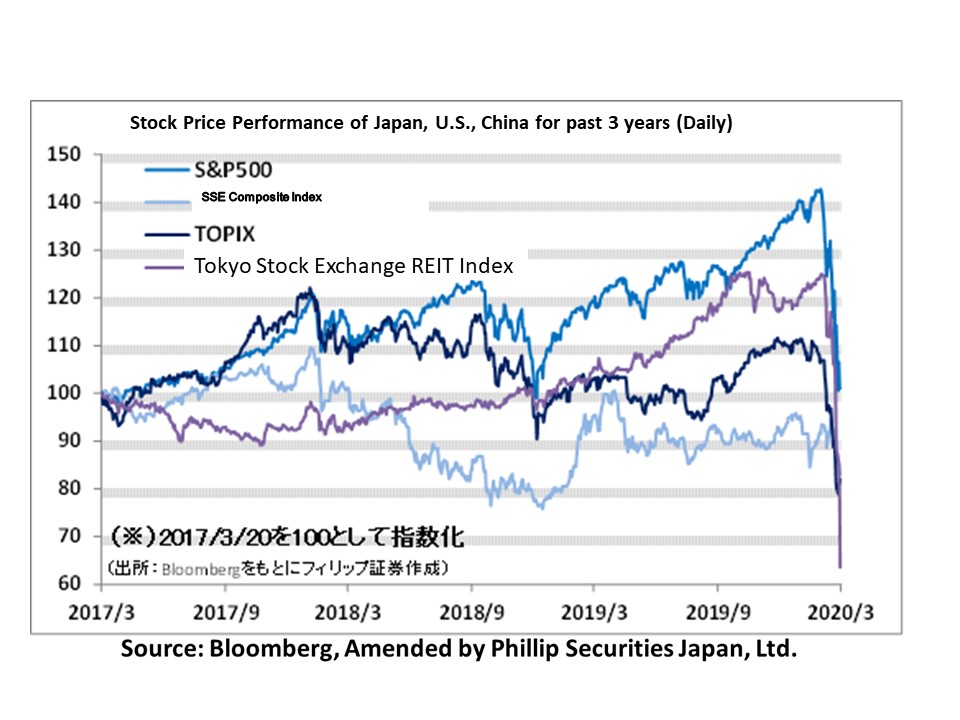

There are concerns that severe measures against the spread of the COVID-19 infection especially in the U.S. will cause consumption and service demand to vanish at once. Also, in the Japanese stock market, during trading hours in the Tokyo market, it saw a situation where the fluctuation in prices was stopped at the limit down level with a 5% drop from reference values on consecutive days during the late-night trading of futures in the Dow Jones Industrial Average (Dow Futures) for U.S. stocks. As a result, Japanese stocks also saw the Nikkei average fall to the 16,300 point level on 17/3 and 19/3.

The Bank of Japan’s Monetary Policy Meeting was brought forward and held on 16/3, which saw the decision to carry out additional easing with a doubling of both the ETF (exchange-traded funds) purchasing target, which was raised from 6 trillion yen to 12 trillion yen annually and the J-REIT (Japan’s listed real estate investment trusts) purchasing target, which was raised from 90 billion yen to 180 billion yen annually. Since the TOPIX market capitalisation is big compared to the Nikkei average and from the viewpoint that an increase in ETF purchase amounts will benefit TOPIX more than the Nikkei average, a change is beginning to take place in the flow of the “Nikkei average dominance / TOPIX subordination”, which had been continuing in the Japanese stock market. The NT, which is obtained by dividing the Nikkei average by TOPIX, fell from 14.18 times on 9/3 to 13.16 times on 18/3. Even among TOPIX components, we are beginning to see growing prominence in the rate of increase in stock prices of stocks which have high “influence”, which is obtained by dividing the purchase amount for each stock in the Bank of Japan’s ETFs by the annual trading value in the past year. Among these, there has been a lookout for food wholesale, such as Kato Sangyo (9869) and Mitsubishi Shokuhin (7451), which is likely to benefit from stockpiling movements as a result of effects from the spread of the COVID-19 infection, as well as Nippon Telegraph and Telephone (9432) and Nippon Densetsu Kogyo (1950), etc., which can be easily associated with a demand in communication network infrastructure development due to the increase in working from home. On the other hand, there has been a distinct decline in stock prices of blue chip stocks, such as Fast Retailing(9983), etc., which have a high contribution rate to the Nikkei average.

With existing anti-coronaviral drugs known to be a promising cure for COVID-19, there has been growing attention on the Ebola haemorrhagic drug, Remdesivir, as well as the influenza drug, Avigan. For Avigan, its administration to COVID-19 patients depending on the doctor’s judgment has already been acknowledged in Japan and is currently waiting to receive official approval as a cure for COVID-19. The government has stockpiled a quantity of Avigan for approx. 2 million people. Prime Minister Abe expressed “a desire to overcome the spread of the infection and hold the Olympics as scheduled”, whereas U.S. President Trump mentioned that “the coronavirus crisis may last until July or August, or perhaps even longer than that”. With doubts that the Tokyo Olympics would be held, there is also the possibility that Avigan’s official approval would serve as the ace for the Japanese government. The deadline for the International Olympic Committee (IOC)’s decision to hold the event is in late May.

In the 23/3 issue, we will be covering Yokohama Reito (2874), FUJIFILM Holdings (4901), Ride On Express Holdings (6082), and Nintendo (7974).

・Established in 1948. Carries out the cold storage / frozen storage business involving seafood products and agricultural and livestock products, etc., the foodstuff retail business involving processing, retail and import and export, etc. as well as real estate leasing, etc. Owns distribution centres in Osaka (Yumeshima), the proposed IR site, and Yokohama.

・For 1Q (Oct-Dec) results of FY2020/9 announced on 13/2, net sales decreased by 15.5% to 31.667 billion yen compared to the same period the previous year and operating income decreased by 5.0% to 1.156 billion yen. Despite an increase in revenue from storage fees due to the maintenance of high storage standards especially for livestock products, a fall in market prices due to an increase in domestic storage of salmon and trout and a fall in market price for crab in the foodstuff retail business have affected, which led to a decrease in sales and income.

・For its FY2020/9 plan, net sales is expected to decrease by 2.2% to 143 billion yen compared to the previous year and operating income to increase by 13.1% to 5.4 billion yen. In addition to the continued increase in meat imports brought forward due to the spread of the African swine flu (ASF) in China, there has been a prominent lack of cold storage warehouses due to the increased amount of meat imports with lowered tariffs as a result of the effectuation of TPP and EPA. The company is predicting demand in goods to Tokyo and has set up a large-scale cold storage warehouse in Tsukuba City, Ibaraki Prefecture, in Feb 2020.

・Established in 1934. Its 3 main business pillars are Imaging Solutions, which involve photographs and images, Healthcare & Material Solutions, which involve the health of people (prevention, diagnosis and treatment) and the Fuji Xerox business.

・For 3Q (Apr-Dec) results of FY2020/3 announced on 6/2, net sales decreased by 4.0% to 1.7283 trillion yen compared to the same period the previous year and operating income decreased by 4.2% to 151.635 billion yen. Despite growth in medical systems, bio CDMO and the regenerative medicine business, sluggish growth in photo imaging, optic / digital imaging and the document business have led to a decrease in sales and income.

・Company revised its full year plan downward. Net sales is expected to decrease by 2.5% to 2.37 trillion yen (before revision: 2.435 trillion) compared to the previous year and operating income to increase by 4.8% to 220 billion yen (before revision: 240 billion yen). On 17/3, it was announced that the efficacy of Avigan as a treatment for the COVID-19 infection, which is developed by Toyama Chemical, a subsidiary of the company, had been confirmed in clinical studies by the Chinese Ministry of Science and Technology. It is predicted that its mass production by the Chinese pharmaceutical company granted with the license will shift into high gear.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: