|

Report type: Weekly Strategy |

How Will the Economic Measures and the Increase in Long-Term Interest Rates Affect the Market?

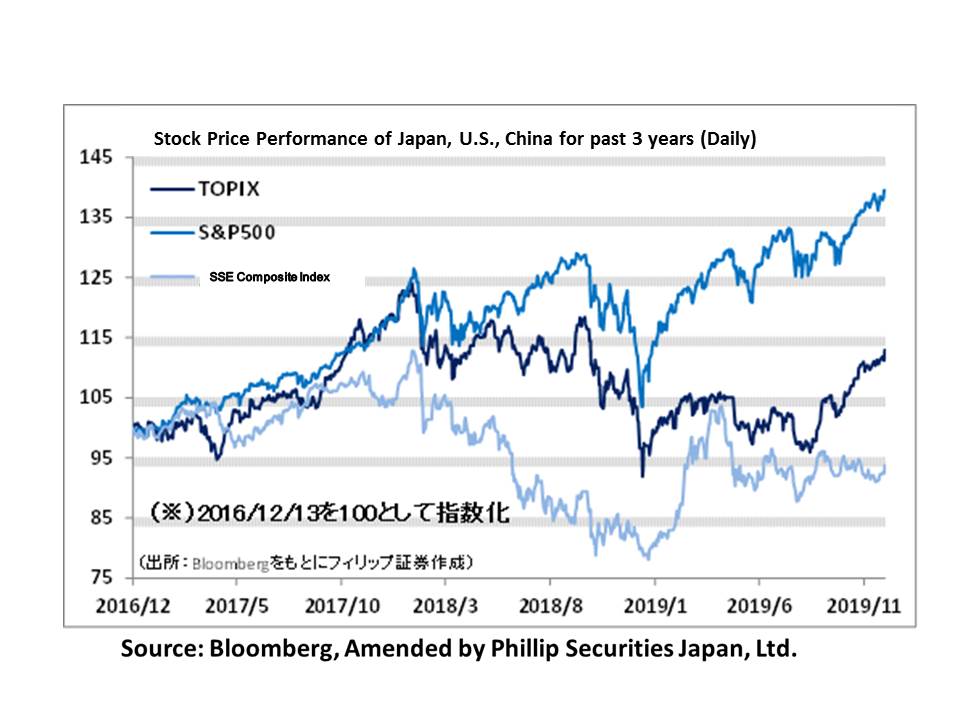

On the 13/12, the Major SQ date (date where there is an overlap of the settlement date for option transactions and futures transactions for the delivery date in March, June, September and December, where there are many trading units in stock index futures trading), the Nikkei average rose sharply to exceed the level of 24,000 points, which was a turning point from the previous day’s closing price of 23,424 points. US President Trump approving the phase-one trade deal with China and predictions of an aversion of the 160 billion dollars’ worth of imports from China scheduled to be invoked on 15/12 led to a favourable effect on the stock market.

Looking at the Japanese economy as of late, in the Japan Tankan for Dec announced on 13/12, with the diffusion index (DI) for large enterprises in the manufacturing industry worsening by 5 points from the previous survey to 0 and a 2-term consecutive worsening with a decline in both large enterprises in nonmanufacturing and personal consumption, etc., there appears to be a sense of foreboding regarding the future economic climate. In the midst of those, following the stimulus package announced by the government on 5/12, the ruling party launched policies which clearly distinguished priority areas and growth sectors, such as the new implementation of measures in the FY2020 tax system outline finalised on 12/12 which aims to lower corporation tax in order to encourage the spread of 5G telecommunication infrastructure. In addition, on 7/12, regarding the government’s aim to have 60 million foreign tourists visit Japan by year 2020, Chief Cabinet Secretary Suga announced a policy to “newly construct world-class hotels located in 50 locations across the country”. If the global economy is unable to avoid effects from the US-China trade friction even from 2020 onwards, companies that would benefit from domestic demand backed by the government’s budget can be considered as an important investment strategy for Japanese stocks.

On 10/12, the long-term interest rate (10-year government bonds) came out of a negative interest rate and rose to 0%, which was last seen 9 months ago. In the Diet in Nov, Kuroda, the Governor of the Bank of Japan replied that “there is plenty of room for deeper negative policy interest rates”, and there were concerns on the stock market due to effects on bank revenue from the implementation of maintenance fees on the accounts of depositors. The long-term interest rate increase seems to be able to temporarily ease concerns such as those. On the other hand, while the outstanding debt in companies and the government increase, there are also concerns that it would pose a negative influence on the economy as a result of the increased burden of interest payments. The long-term interest rate increase is not only limited to Japan, but since it is also indicated by the strong figures which greatly exceeded market predictions in the US, with their employment statistics for Nov announced on 6/12, as well as in Europe, with the German ZEW Indicator of Economic Sentiment for Dec, it seems to hint at the possibility of an improved forecast for the global economy. There is a need to continue to closely observe how effects of the increase in long-term interest rates will manifest in the future stock market.

In the 16/12 issue, we will be covering HOUSE DO (3457), MRT (6034), DISCO (6146), NEC (6701), Tokyo Dome (9681) and Senshu Electric (9824).

・Established in 2009. Their mainstay is the franchise business involving the purchase and sale / leasing of real estate. Their unique aspect is the “house-leaseback” business, which enables the purchase of the house while still allowing one to live in there. Launched their new real estate leasing franchise, the “RENT Do!” business, in Jan 2018.

・For 1Q (Jul-Sep) results of FY2020/6 announced on 5/11, net sales decreased by 0.3% to 6.061 billion yen compared to the same period the previous year and operating income decreased by 92.0% to 37 million yen. The 33.6% increase in selling, general and administrative expenses due to human resources and advertising costs for their mainstay business as well as the record of expenses related to the acquisition of Koyama Corporation in Saitama as a wholly-owned subsidiary in Aug 2019 have affected.

・For its FY2020/6 plan, net sales is expected to increase by 18.0% to 37.221 billion yen compared to the previous year and operating income to increase by 11.5% to 3.521 billion yen. Attention has been on the aspect of the acquisition of Koyama Corporation as a subsidiary as a business expansion strategy by acquiring community-based companies who are facing difficulties in finding a successor. The company’s subsidiary was registered as a financial instruments business operator (Type 2) on 4/12. Announced the asset securitisation of their house-leaseback on 9/12. We can look forward to growth in the areas that combine real estate and finance.

・Started in 2000 where it was made up of a cooperative association of doctors from the University of Tokyo Hospital. Expands a healthcare information platform business for doctors which focuses on the referral of part-time and full-time doctors through the use of the internet.

・Company revised their accounting period from 31/3 to 31/12 from FY2019 onwards. For 1H (Apr-Sep term) results of FY2019/12 announced on 12/11, net sales increased by 12.0% to 1.319 billion yen compared to the previous period, operating income increased by 18.0% to 172 million yen and net income decreased by 37.9% to 101 million yen. The profit decrease in their net income was a reactionary fall due to the gain on sales of affiliated companies (128 million yen) recorded in the previous period.

・For their earnings forecast for FY2019/12 (Apr-Dec), net sales is expected to be at 1.9 billion yen, operating income at 120 million yen and net income at 70 million yen. Rate of change compared to the previous year was not listed due to the change in their accounting period. Company is currently focusing on expanding the sales network of their smartphone-based online consultation service, “Remote Consultation Pocket Doctor” to healthcare facilities and enhancing awareness of the service. We ought to keep an eye on remote consultation as a service with a high change of popularisation due the 5G communication.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: