Report type: Weekly Strategy

Despite the Cheaper Price Levels, There Is a Need to Keep an Eye on the Dollar/Yen Exchange Rate

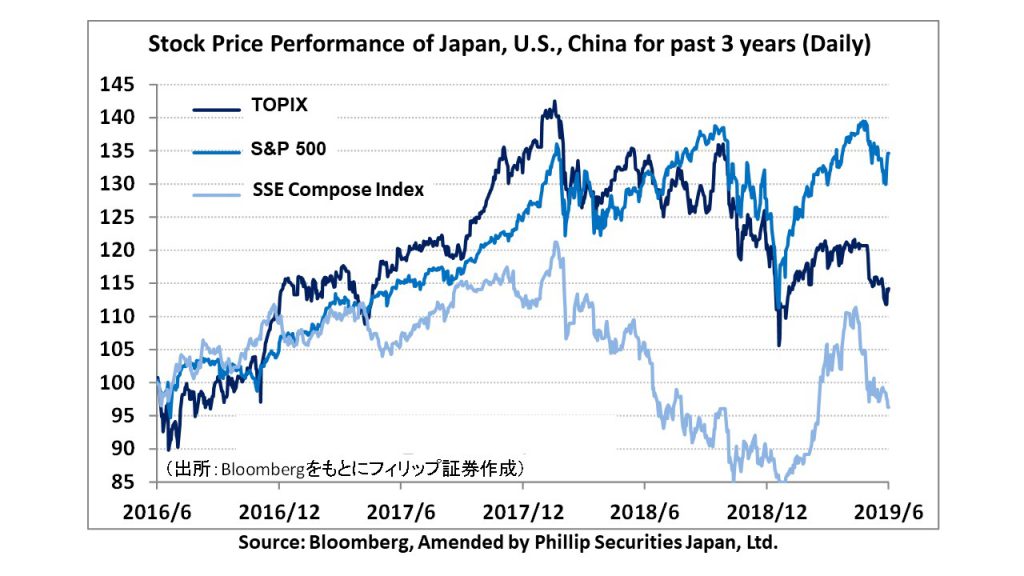

The Trump administration announced on 30/5 that additional tariffs would be imposed on all imports from Mexico, which shook the global stock market, however, the disturbance continued well after the weekend, with the Nikkei average falling to 20,289 points on 4/6. Due to growing concerns of a global recession from the intensifying trade friction surrounding the US, and the 10-year government bond yield falling under 2.1% in the US bond market, the dollar/yen exchange rate fell below 108 points, which saw the yen appreciating against the dollar. Following that, due to FRB Chief Powell’s remarks on 4/6 which included, “seriously accepting risks” and “taking appropriate actions towards the target of a 2% increase in prices and to maintain strong employment”, etc., caused the US stock market to turn towards a rebound, with the Nikkei average also increasing to a level of 20,900 points on 7/6.

Firstly, for the Nikkei average level at 20,289 points, the weighted average PBR (price-to-book ratio) of 225 stocks was approximately 1.03 times (at 4/6). The last time it was at 1.03 times and below at the Nikkei average closing price was on 25/12/2018 at 0.99 times (19,155 points) and 26/12 of the same year at 1.00 times (19,327 points), and prior to that, dating back to 24/6/2016 at 1.03 times (14,952 points, UK Brexit election day) and 12/2 of the same year at 0.99 times (14,952 points). In terms of economic fundamentals, the weighted average of 225 stocks representing Japan close to the breakup value can be regarded as a cheaper price level that is “oversold”.

Next, the trend of the US bond market is the key to the dollar/yen exchange rate, which is a factor that greatly impacts the Japanese stock market. Although in terms of interest rate, the decline in the US long-term interest rate is due to the sale of dollars, it could also be a clue towards a “risk-on” market due to improvements in the financing environment for US companies. Also, weak dollar or dollar-based decline in interest rates is an advantage for developing countries that have numerous debts in US dollars, and coupled with effects from US-China friction which accelerate the shifting trend towards emerging markets, such as the ASEAN region, which serve as a manufacturing base, it may be an advantage to invest in emerging markets. As long as there is no “risk-off yen appreciation”, the weak dollar is not necessarily a disadvantage.

For the Japanese economy, the plan to execute the “Council on Investments for the Future”, which discusses the Growth Strategy, was showed on 5/6, in addition, the “Big-boned Policy” (Basic Policy for Economic and Fiscal Management) is scheduled to be confirmed in late June. Within these topics, matters that generate domestic demand may arise through bills or budgeting. If we also take into account measures towards concerns of a strong yen due to it entering the cycle of US interest rate reductions, we will want to keep our focus on stocks which are resistant to influences from the US-China friction, and which have potential in supporting strategies for domestic demand.

In the 10/6 issue, we will be covering House Do (3457), Rakuten (4755), MRT (6034), Nagase (8012), Mos Food Services (8153), and Sumitomo Mitsui Trust Holdings (8309).

・Established in 1997. In addition to operating various online shopping websites, such as, “Rakuten Ichiba”, as well as an online cashback site, travel booking site, portal site, digital contents site, company also carries out communication services, manages professional sports, internet banks and securities, credit card-related services, life insurance, and electronic money services, etc.

・For 1Q (Jan-Mar) results of FY2019/12 announced on 10/5, sales revenue increased by 15.9% to 280.294 billion yen compared to the same period the previous year, operating income quadrupled to 113.662 billion yen, and net income increased by 6.0 times to 104.981 billion yen. Due to the expansion in their base of Rakuten card members and the extension of banking services, the FinTech business has grown. The 110.4 billion yen profit from the loss from valuation of securities following the IPO of Lyft have also contributed.

・For its FY2019/12 plan, excluding the securities services, sales revenue is expected to increase by 2 digits compared to the previous year. On 5/6, company announced the cooperation with JR East Japan towards the promotion of a cashless system. In spring 2020, using the Rakuten Pay app, in addition to the issuance of and the addition of funds to Suica, it will be available to be used as a form of payment in approx. 5,000 stations for rail, approx. 50,000 stops for buses, and in approx. 60,000 retail shops.

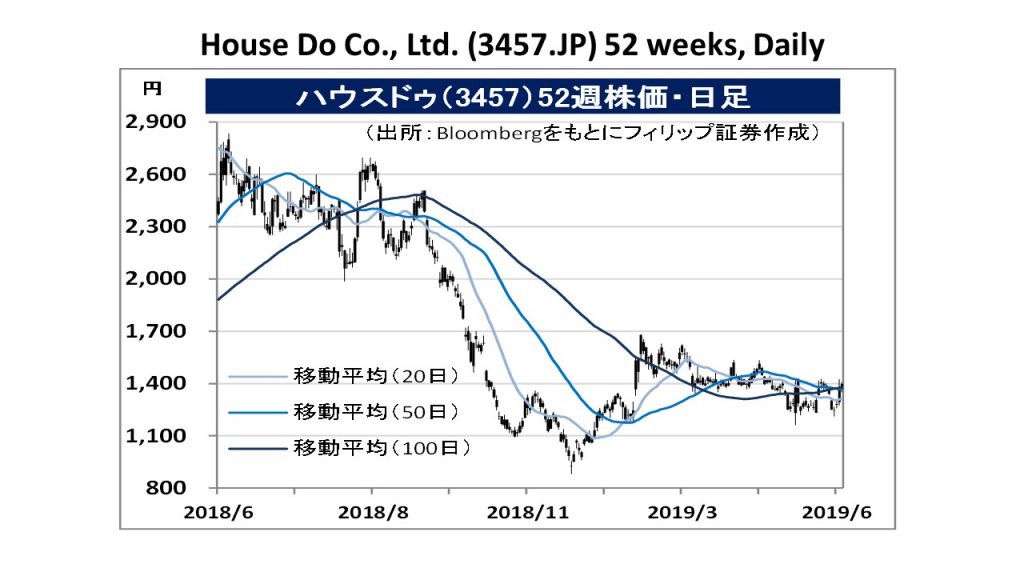

・Established in 2009. Their main business is the real estate sale / rental franchise. Characterised by their “House Leaseback” business, which enables selling off houses whilst living in them. Started a new real estate leasing franchise business, “Rent Do”, from Jan 2018.

・For 3Q (2018/7-2019/3) results of FY2019/6 announced on 13/5, net sales increased by 44.6% to 21.567 billion yen compared to the same period the previous year, operating income increased by 44.1% to 1.915 billion yen, and net income increased by 68.5% to 1.251 billion yen. Segment profits of the house leaseback business, which account for a net sales ratio of 38%, have expanded by 2.3 times to 1.055 billion yen due to an increase in the level of awareness.

・For its FY2019/6 plan, net sales is expected to increase by 22.1% to 27.499 billion yen compared to the previous year, operating income to increase by 53.4% to 3.246 billion yen, and net income to increase by 55.0% to 1.983 billion yen. On 3/6, the Financial Services Agency announced an estimation of “requiring 20 million yen in old age”. Regarding old age reserves, there will likely be an increase in focus on house leaseback. For the purpose of strengthening measures against vacant rooms, AirTripStay and Airbnb Japan began a comprehensive business tie-up on 6/6. There is a need to focus on businesses that meet societal demands.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: