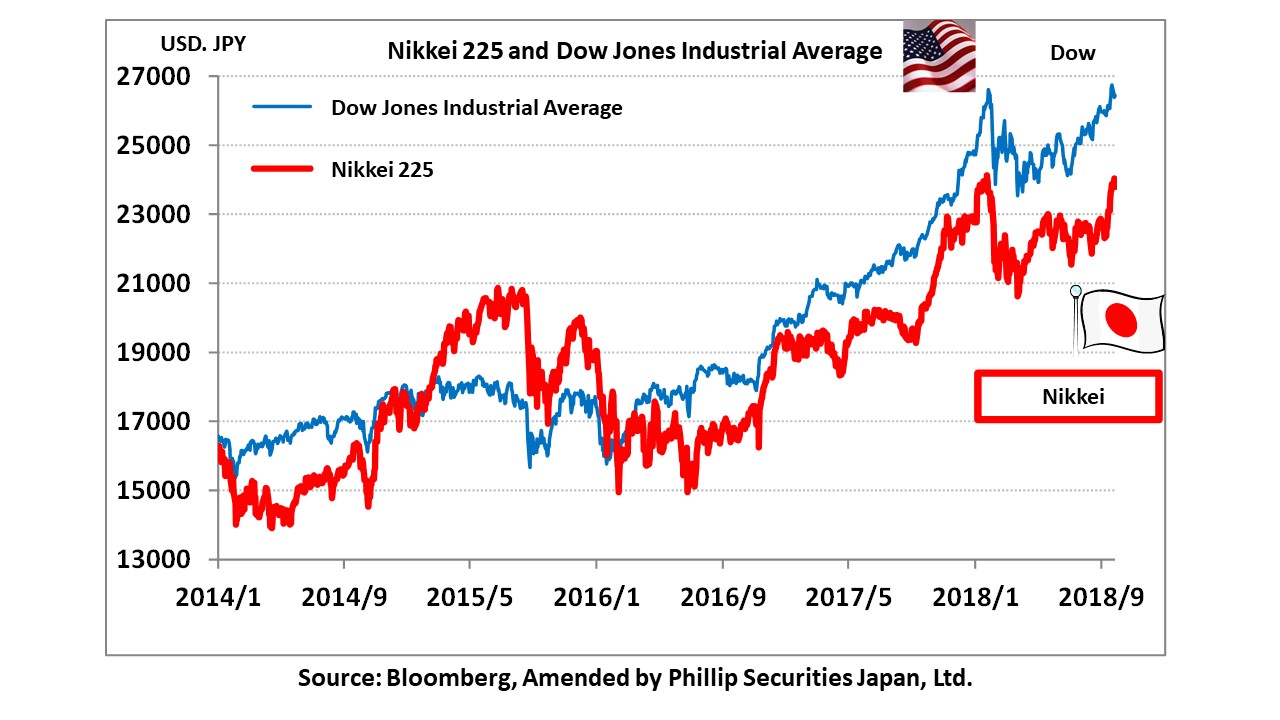

On 26/9, the Nikkei average rose for the 8th consecutive session since 12/9, bringing its gains to 1,429.18 points (+6.32%). After a slight retreat on 27/9, the following day of 28/9, the index temporarily rose to a high level not reached since 14/11/1991, 26 years and 10 months ago, and closed at 24,120.24 yen which was close to the year’s high on 1/23. In forex, the US dollar continues to appreciate against the yen, giving a rise in momentum of the Nikkei average.

The dollar-yen went from 113.17 yen/dollar on 19/7 and bottomed out at 109.78 yen/dollar on 21/8, then momentarily rose to 113.64 yen/dollar on 28/9, about 9 months since 21/12/2017, greatly pushing up stock prices. The pace of this rally is similar to the rise in market prices in September the previous year. Last year, the Nikkei average strengthened from a low of 19,239.52 yen on 8/9/2017 to a high of 24,129.34 yen on 23/1/2018 in consecutive sessions. The dollar-yen bottomed out at 107.32 yen/dollar on 8/9/2017 and depreciated to 114.73 yen/dollar on 6/11/2017.

It appears market trends will track the dollar-yen. The rise in US stock prices and positive business indicators may encourage investors to reduce their risk aversion, and the dollar to appreciate against major currencies. In addition, Italy, which has been grappling with financial problems has its coalition government faced with the budget for the next fiscal year, and will find it difficult to reduce the vast financial deficit pledged to the EU thus far, which has resulted in Euro weakness. Short-term buying and short covering movements in the market are expected. In the beginning of Oct, major US economic indicators such as the September’s ISM Report on Business and employment statistics, etc., are expected to register positive statistics. It is expected that yen depreciation is maintained at the higher level than assumed by domestic companies.

However, major stock price indices such as the Nikkei average, etc., show signs of overheating from major upper divergences, etc. from the RSI, up-down ratio and moving average line, so a short-term correction is expected. It is likely that the trade negotiations between US and China, and the NAFTA between US and Canada will continue to face difficulties. On the other hand, for US and Japan, in a trade conference between the two countries, an agreement was reached in the early stages of negotiation on the Trade Agreement on Goods (TAG), and during the conference, it has been confirmed that US will not invoke additional tariffs on automobiles. The worst scenario to be feared is a recession. China has announced cuts on individual income tax up to 320 billion yuan (about 5.1 trillion yen) yearly from October, and a reduction in average tariff rates on machinery, textiles, paper products, etc. from November. While securing profits in the rise in market prices, adopt the stance of buying the dips focusing on major blue chip stocks.

In the 10/1 issue, we will be covering Besterra (1433), Asahi (3333), Niitaka (4465), Toyo Business Eng. (4828), Fujitsu (6702), and Unicharm (8113).

Selected Stocks

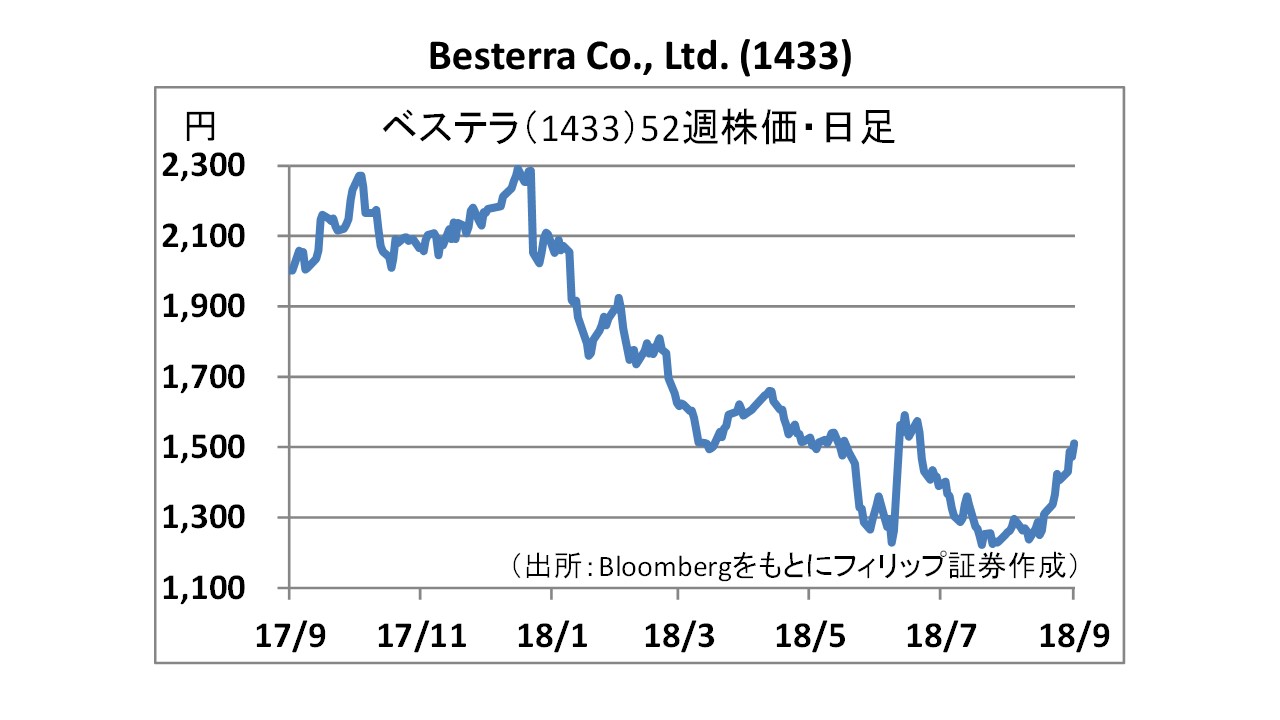

Besterra Co., Ltd. (1433)

・Founded in 1947, established its company in 1974. Carries out the dismantling of plants involving steelworks, electrical, gas and fuel, etc. Possesses knowledge and experience regarding the removal of harmful substances such as PCB, asbestos, dioxin, etc., and has unique dismantling methods, such as the “apple skin peeling method” and “boiler dismantling method”. Also offers recruitment services and 3D measurement services, etc.

・For 1H (Feb-Jul) of FY2019/1(*), net sales decreased by 3.3% to 2.11 billion yen compared to the same period the previous year, operating income decreased by 12.2% to 139 million yen, and net income decreased by 14.9% to 90 million yen. The lag time between the timing of recording of the sales and cost price has resulted in a decrease in profits.

・Company has also decided to sell real estate held as assets for leasing. Extraordinary profits are expected to be recorded, and company has revised its 2019/1 plan(*) upwards. Net sales increased by 13.4% to 5.1 billion yen compared to the previous period, and although operating income increased by 9.3% to 422 million yen and was unchanged, current income doubled to 540 million yen (originally plan 286 million yen).

(*) As the consolidated financial statement from 1Q (Feb-Apr) of FY2019/1 is being compiled, the rate of change from the same period last year, and from the previous period are reference values.

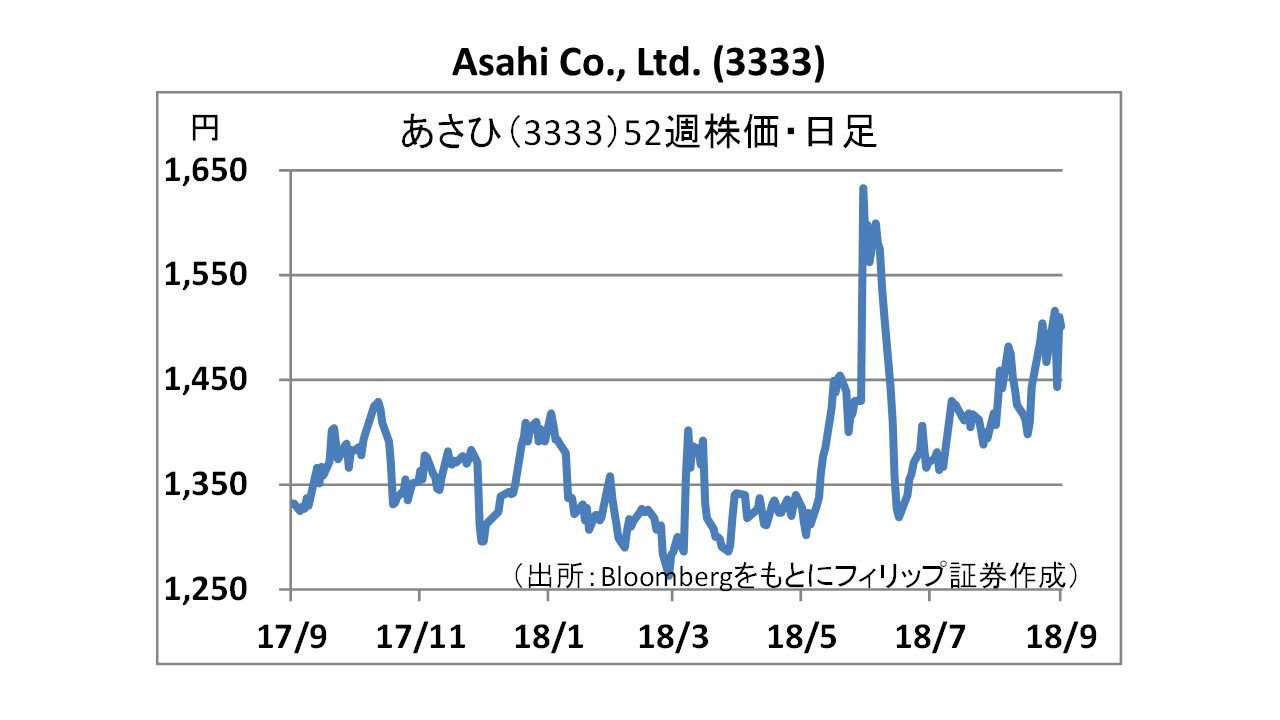

Asahi Co., Ltd (3333)

・Established in 1975. Sells automobiles and the related products such as parts and accessories, etc., and also provides ancillary services such as servicing or repair of various parts. In addition to having 435 directly-managed stores, they have expanded to 24 FC shops and runs an e-commerce (end 2018/2). Also runs a business supplying commodities to retailers or online businesses based in Beijing, China.

・For 1H (Mar-Aug) of FY2019/2, net sales increased by 6.5% to 33.915 billion yen as compared to the same period the previous year, operating income increased by 7.5% to 4.256 billion yen, and net income increased by 8.0% to 2.89 billion yen. The practice of ‘ordering online and picking up in-store’ has been favourable. Sales of high value-added products such as sports bicycles and electrically-assisted bicycles, etc. are growing and average spend per customer has seen a significant increase.

・ For FY2019/2 plan, net sales increased by 9.8% to 58.87 billion yen compared to the previous period, operating income increased by 20.3% to 4.12 billion yen, and current income increased by 35.6% to 2.781 billion yen. Although the rate of progress has exceeded the operating income and net income by 100%, the tendency to focus on automobile repair and inspection in-store during the average year’s most crucial period in Spring, has resulted in a standstill.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: