Outlook

The Positives

The Negatives

Investment Action

We maintain Overweight on the Land Transport sector, on the basis of regulatory reviews and changes that address profitability and sustainability.

We have a “Buy” rating on ComfortDelGro Corp with a target price of $2.50. We forecast earnings to have bottomed in FY17, with the Public Transport Services segment largely driving earnings going forward. Regulatory changes on fare formula and licencing of private-hire car companies could be catalysts for a re-rating of the stock.

Taxi outlook

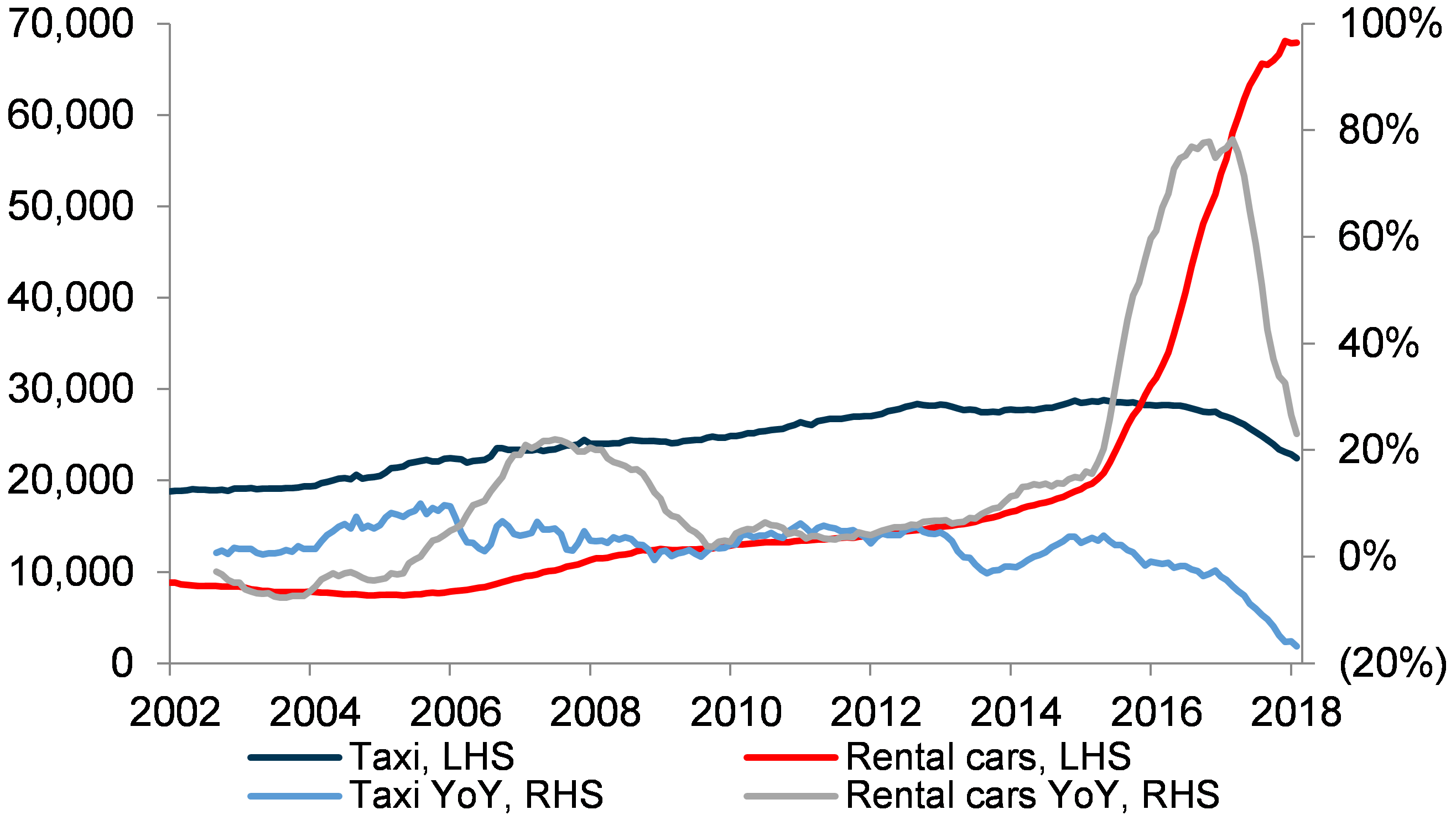

We had first highlighted in our 2018 Strategy piece (Dec 18, 2017) that Rental cars population growth was moderating and the equilibrium between Taxi and Rental cars populations could be near.

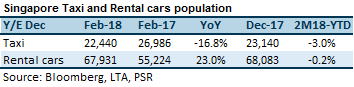

Rental car population YoY growth had peaked at high-70% in 4Q 2016 and tapered down during 2017. Rental car population had accordingly started to stagnate in 2H 2017. YoY growth for February 2018 has further moderated to 23%.

Figure 1: Monthly Taxi and Rental cars population

Source: Bloomberg, LTA, PSR

Not only has Rental cars YoY population growth tapered, but the population has contracted -0.2% YTD. For context, Taxi population had a larger contraction of -3.0% YTD. This could be an early indication of an oversupply of Rental cars and an impending rationalisation of its population, thus supporting our view that the equilibrium could be near. We would like to see the monthly YoY contraction in Taxi population start to moderate as well, to serve as an additional indicator that the worst could be over for the Taxi segment.

CNBC first reported on Feb 16 that Uber was in the process of selling its Southeast Asian business to Grab. Both firms have denied such reports as “speculation”. Uber’s Asia Pacific chief business officer subsequently said that was no plans to sell its Southeast Asian business to Grab.

Amid media reports again in early-March that a deal was being finalised, Uber on Mar 14 launched its carpooling app, Uber Commute. Uber Commute is conceptually similar to GrabHitch, though with some differences. Uber Commute is widely believed to not have a material impact on profits for Uber.

During the recent Singapore Budget debate, Second Minister for Transport Ng Chee Meng had expressed the government’s desire for the transport market to remain “open and contestable”. Thus signalling a monopoly is not ideal – having a dominant transport operator may not be in the best interest of commuters.

We do not speculate on whether a takeover of Uber by Grab in Southeast Asia would materialise. However, we offer two cases on how it could be beneficial or detrimental to the Taxi segment. Bull case: more rational pricing of commuter fares and driver incentives for private-hire cars, would shift some demand back to Taxis. Bear case: monopoly by Grab over the private-hire car business in Singapore, would put it in a better position to compete against Taxis.

Mr Ng had also commented that regulating and licencing of such companies could be possible in the future, as the population of Rental cars has grown unabated. Licencing would require private-hire car companies Grab and Uber to pay for a licence to operate in Singapore. At present, the regulatory regime extends only to drivers and their vehicles. The concern is congestion caused by the private-hire cars, and the government’s intent is to have the ability to exercise control over the private-hire car population. This could be beneficial to the Taxi segment, should the government decide to curb private-hire car numbers.

Bus outlook

Bus revenue for SBS Transit is expected to be higher YoY in 2018, mainly due to contribution from the Seletar package after taking over operations since Mar 11 this year. The contract was awarded in April 2017 through a competitive bidding process. The contract value of the package is $480mn over the five-year contract period, with an option for LTA to extend the contract term for an additional two years. Prior to this, the package was a combination of services operated by both SBS Transit and SMRT Buses under the negotiated price agreement.

SBS Transit was also awarded the Bukit Merah package in February 2018 through a competitive tender process. The contract value is $472mn over the five-year contract period, with an option for LTA to extend the contract term for an additional two years. The package will commence in 4Q 2018. Any upside from the package will be limited, as SBS Transit is the incumbent operator of the package under the negotiated price agreement.

The package is currently operated by SMRT Buses for four-years under the negotiated price agreement. It should conclude in 3Q 2020.

Rail outlook

DTL has been loss-making since the commencement of Downtown Line Stage 1 (DTL1) in December 2013. We estimate accumulated losses for DTL came up to ~$150mn as at end of December 2017, with highest ever quarterly loss of ~$16mn in 4Q 2017. Losses over the years were due to start-up costs, as the DTL was progressively opened in three stages.

However, with the commencement of revenue service for DTL3 in October 2017, the full DTL is now operational and losses are expected to narrow as ridership ramps up to the normalised level.

The Land Transport Authority stated in a News Release on Feb 10, 2018 that daily weekday ridership on DTL has grown from 300k to 470k since DTL3 opened. This resulted in an average ridership of 279k for DTL in 2017. The normalised ridership level that is being projected for DTL is 500k.

With the fare reduction of -2.2% that was effective Dec 29, 2017, ComfortDelGro management expects DTL to only turn profitable in 2019. This is contingent on achieving 500k average daily ridership and pending the outcome of the fare adjustment at the end of 2018. A fare reduction at the end of 2018 would further delay DTL turning profitable. (Fare adjustments have historically come into effect at end-December.)

The PTC had announced on Apr 5, 2017 that it had commenced a review of the current fare formula. The current fare formula was adopted in late-2013 and it incorporates core Consumer Price Index, Wage Index, Energy Index and Productivity Extraction to derive the fare adjustment. The fare reduction experienced in the last few years was largely due to lower energy costs.

Transport Minister Khaw Boon Wan commented during the recent Singapore Budget debate that the current formula is “inadequate” and cheap fares are “not sustainable”. Costs have been rising, but fares have reduced – and he said that the current fare formula “can be improved to better track total costs”.

We highlight that only the Rail segment remains on a fare-revenue model, while the Bus segment has transitioned on Sep 1, 2016 to the government bus contracting model where a service fee is awarded through a competitive bidding process.

The LTA announced on Feb 14 that the NEL and SPLRT will transit to the NRFFF on Apr 1. SBS Transit will pay a Licence Charge to operate the rail lines, and that will go into the Railway Sinking Fund for the renewal of operating assets.

The Licence Charge Structure for SBS Transit’s NEL and SPLRT is identical to that of SMRT Trains. Recall that SMRT Trains’ North-South and East-West Lines (NSEWL), Circle Line (CCL) and Bukit Panjang LRT (BPLRT) had transitioned to the NRFF in 2016.

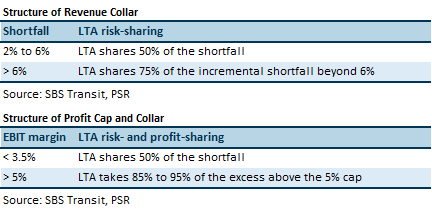

The transit to the NRFF will relieve SBS Transit from heavy capital expenditure and large fare-revenue risks. Large fare-revenue risk will be mitigated through a risk-sharing revenue collar. However, margin for NEL is expected to be lower going forward, due to the profit-sharing cap and collar structure of the NRFF. EBIT margin will be capped at 5%, with substantial profit-sharing to the LTA above the 5% cap. The current NEL EBIT margin is not disclosed, but we believe it to be in the mid- to high-teens. The LTA’s sharing of risk is limited to the amount of Licence Charge payable.

SBS Transit will sell the relevant operating assets of NEL and SPLRT it currently owns to the LTA at net book value. The assets are worth $28.8mn, which is 6.4% of the net asset value of SBS Transit as at Dec 31, 2017. SBS Transit intends to use the sale proceeds to repay borrowings which stand at $181mn as at Dec 31, 2017.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Richard covers the Transport Sector and Industrial REITs. He graduated with a Master of Science in Applied Finance from the Singapore Management University. He holds the CFTe and FRM certifications and is a CFA charterholder.

He was ranked #2 Top Stock Picker (Asia) for Real Estate Investment Trusts in the 2018 Thomson Reuters Analyst Awards, and ranked #2 Top Stock Picker (Singapore) for Resources & Infrastructure in the 2016 Thomson Reuters Analyst Awards.