The Nikkei average, which temporarily recorded a high value of 24,448.07 points on 2/10, last seen about 27 years ago on 11/1991, rose from its recent low on 7/9 by 2,275.17 points (+10.3%) in only less than a month. In the US, trade negotiations with Canada have reached an agreement, while Italy has made a partial concession to the EU and cut the deficit target to GDP in 2020 and 2021, which caused a growing movement in risk-taking by investors worldwide. On 3/10, Dow hit record high for second day and the US dollar rapidly strengthened against the Japanese yen to 114.55 points on 4/10 from 110.38 points on 7/9.

However, on 4/10, the NY Dow temporarily plunged from 356 points and ended the fall of 200.91 points (0.74%) from the previous day. On 4/10, the US 10-year bond yields rose temporarily by 3.23% in 7 years and 4 months ago since 5/2011, which has caused investors’ caution. A speech by Fed Chairman Powell on 3/10 made references to a possibility of more rate hikes that will go beyond a neutral, which has greatly pushed up interest rates. In the FOMC held at the end of September, the Fed hiked the neutral interest rate from the previous 2.90% in June to 3.00%.

September’s ISM Non-Manufacturing Index announced in early October rose to 61.6 which was the highest since 62.0 in 8/1997, and September’s ADP employment statistics announced the employment increased by 230k in the private sector compared to the previous month, which was the highest in 7 months. The US economy is looking very good, as the Fed’s PCE core that estimates the rate of consumer prices, has already hit its target of 2%. Employment statistics in Aug have confirmed wage rate growth, inflation indexes such as the September’s PPI core to be announced on 10/10 (excluding food and energy, market prediction has gone up by 2.6% as compared to the same month of the previous year) and the September’s CPI core to be announced on 11/10 (excluding food and energy, similarly gone up by 2.3%), are expected to gather much attention.

Japanese stocks may see a temporary readjustment, but it is likely the heated market will cool down due to a healthy correction. Many corporations, such as Itochu Corporation (8001), are expected to revise their annual performance upwards. As the Nikkei’s average’s current term P/E ratio is still low at the upper end of 13.0, there is a lot more room for Japanese stocks to rise. The Apr-Jun supply and demand gap announced on 3/10 by the Bank of Japan increased by 1.86%, widening the gap of the demand’s excess, and the continuous increase in 7 quarters has brought it back to the level of 10-12/2007. We want to pay attention to reevaluate value stocks which P/E and P/B is relatively undervalued, such as trading companies and banks.

In the 9/10 issue, we will be covering Edion Corporation (2730), Isuzu Motors, Ltd. (7202), Mitsubishi Corporation (8058), Nippon Gas Co., Ltd. (8174), Mitsubishi UFJ Financial Group, Inc. (8306) and K.R.S. Corporation (9369).

Selected Stocks:

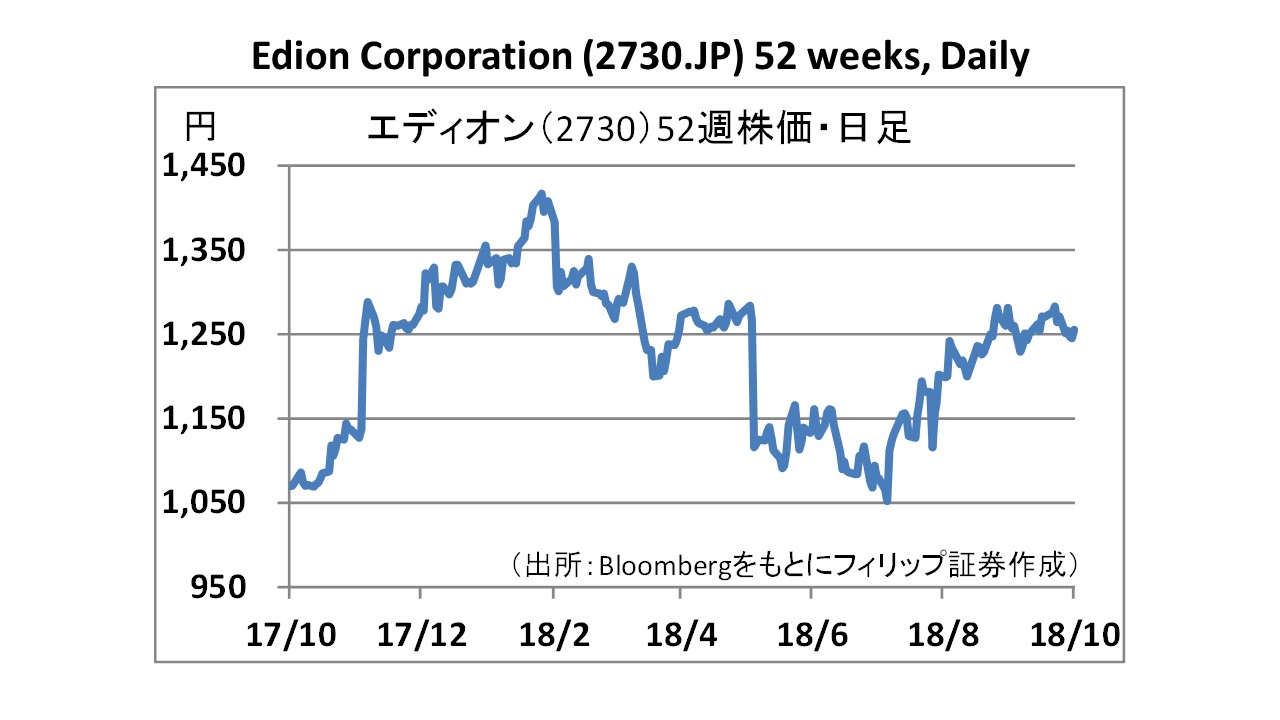

Edion Corporation (2730)

・Established in 2002 via a merger between DEODEO Corporation based in Chugoku, Shikoku and Kyushu region, together with Edion Corporation based in Chugoku region. Selling household appliances as its main business, it has expanded with its household appliance retail stores spanning a wide area from Hokkaido to Okinawa. It runs businesses such as stores specializing in the sale of mobile phones, e-commerce and internet service provision, etc.

・For 1Q (Apr-Jun) of FY2019/3, net sales increased by 4.8% to 157.154 billion yen as compared to the same period the previous year, operating income increased by 8.2 times to 1.09 billion yen, and net income increased by 7.5 times to 652 million yen. Sales of TVs increased due to the World Cup being held. In addition, the rise of temperatures from the later half of June led to favourable sales centred on high value-add products, such as air conditioners, refrigerators and washing machines.

・For FY2019/3 plan, net sales increased by 3.5% to 710 billion yen as compared to the previous period, operating income increased by 20.3% to 185 billion yen, and current income increased by 23.0% to 11 billion yen. Company announced on 1/10 of the opening of their biggest store “Edion Namba Store”, in Namba, Chuo Ward, Osaka City, which will open in summer 2019. Range of products offered are also geared towards tourists visiting Japan.

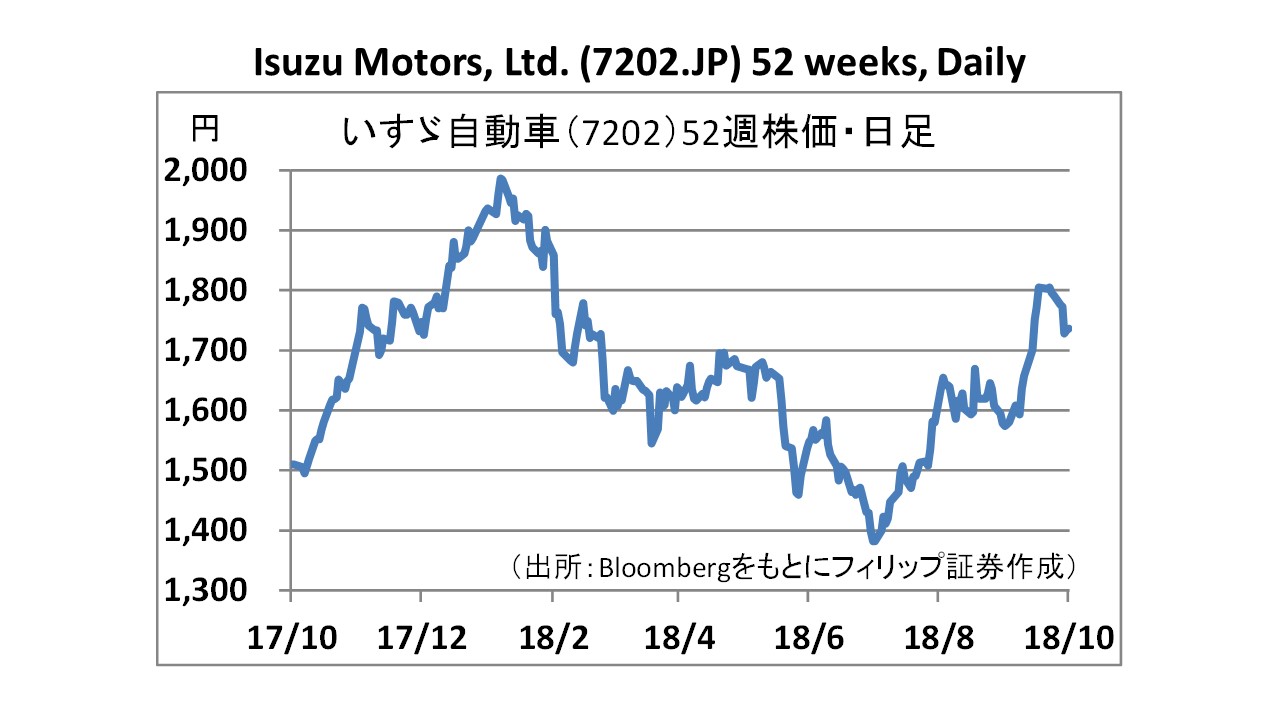

Isuzu Motors, Ltd. (7202)

・Founded in 1916, established in 1937. At present, it boasts the longest history among automobile manufacturers in Japan. Company deals with commercial vehicles with a focus on trucks/buses and pickup trucks, in addition to LCV and engine/components. Employing Diesel technology, its commercial vehicle technology is of the highest standard in the world. Retails its products in hundreds and several tens of countries and regions.

・For 1Q (Apr-Jun) of FY2019/3, net sales increased by 5.2% to 488.119 billion yen as compared to the same period the previous year, operating income increased by 32.4% to 52.444 billion yen and net income increased by 16.0% to 38.103 billion yen. Although domestic sales of automobiles fell by 6.8% to 15,473 units, overseas vehicle unit sales based in Asia and Africa rose by 6.6% to 118,932 units.

・For FY2019/3 plan, net sales increased by 3.4% to 2.14 trillion yen as compared to the previous period, operating income increased by 5.5% to 176 billion yen, and current income increased by 4.1% to 110 billion yen. On 4/10, company announced a business tie-up with Cummins, Inc. on the powertrain project, and will see a joint development on the next-generation diesel engine which will feature low environmental impact.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: