Company Background

TDCX Inc. operates as an outsourced digital customer experience provider focusing on Omnichannel Customer Experience (CX), Sales & Digital Marketing, Content Monitoring & Moderation. CX solutions are provisions of services that enhance how a business interacts with a customer throughout the customer’s lifecycle, examples of this include: after-sales service and support; design and marketing of a company’s web platform.

Investment Merits

We Initiate coverage with a BUY rating and a target price of US$22.00 based on DCF valuation, with a WACC of 9.7% and terminal growth of 3%.

REVENUE

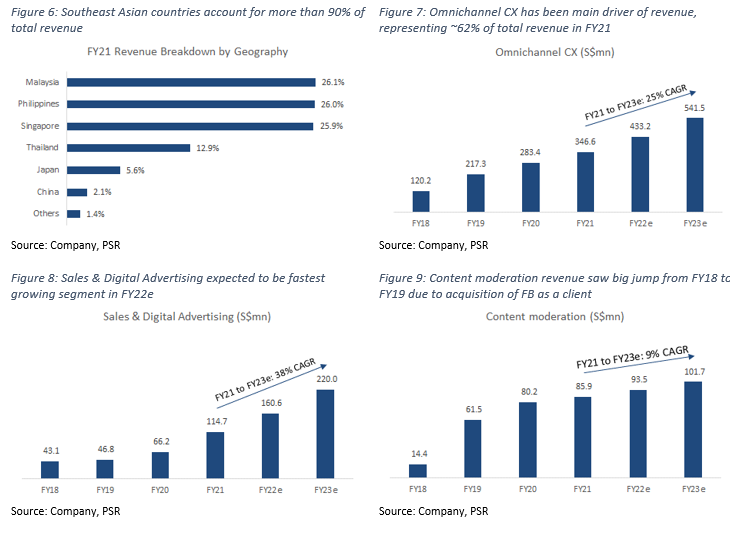

TDCX generates revenue from providing services and solutions in 3 main areas: 1) Omnichannel customer experience (CX); 2) Sales and digital marketing; 3) Content monitoring and moderation. 62% of all revenue is generated from omnichannel CX, with 22% from sales and digital marketing, and the remaining 14% from content monitoring and moderation (Figure 5). Southeast Asian countries like Singapore, Phillippines, Thailand, and Malaysia contribute about 91% of revenue, with 8% coming from north Asian countries like Japan and China, and the remaining 1% from the rest of the world (Figure 6).

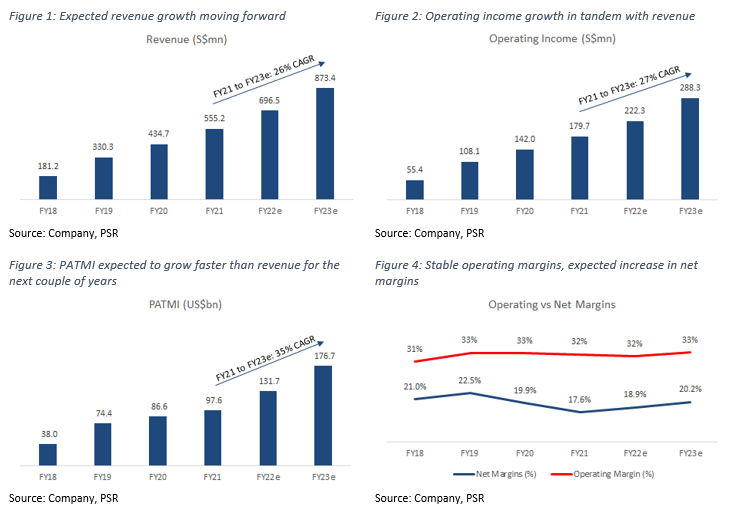

The company posted S$555mn in total revenue for FY21, representing a 28% YoY growth, below its 3-year CAGR of 45%. Also, FY21 was a very good year for TDCX as it added 20 new clients, compared with only 9 new additions in FY20, and ended the year with 52 total clients. TDCX has been aggressively adding clients in new verticals to its portfolio, particularly in FinTech, Gaming, Crypto, and Food Delivery. Revenue from FinTech and Gaming grew 67%, and 99% YoY respectively in FY21. Besides new verticals, the company has also focused on expanding into new geographies in countries like Colombia, Romania, India, and South Korea.

Omnichannel CX: This segment is the bread and butter of TDCX, contributing slightly over 62% of total revenue. Revenue from Omnichannel CX grew 22% YoY in FY21 to about S$347mn, and has been growing at a 3-year CAGR of 42%. We expect YoY growth to pick up slightly in FY22e to about 25%, led by a strong rise in new contracts over the last 2 quarters of FY21 (Figure 7).

Sales & Digital Marketing: This segment saw 73% YoY growth in FY21, posting revenues of S$115mn, in part due to a very strong rebound in the overall digital advertising industry after a weak FY20 plagued by budget cuts due to COVID-19. We do expect growth in this segment to temper slightly to around 40% YoY growth due to a moderation in the digital advertising market (Figure 8).

Content Monitoring & Moderation: Revenue from content monitoring and moderation only grew 7% YoY to S$8mn in FY21. Part of the slower growth rate in this segment is due to the fact the TDCX had only 1 social media client under this segment – Meta Platforms. However, the company recently acquired 2 new contracts from a gaming platform, and another social media company, which should help to boost growth in this segment moving forward. As a result, we expect growth in this segment to be around 9% for FY22e (Figure 9).

Revenue Growth: We expect revenue growth to come mainly from existing new economy clients, especially as revenues from new clients tend to start expanding only after about 2-3 years. We expect this growth to also be heavily supported by tailwinds in the overall Southeast Asian digital CX industry for new economy companies, which is expected to grow at a 5-year CAGR of 13%. We are buoyed by TDCX’s ability to continue adding new clients YoY, as well as growing revenue from its existing clients. For FY22e, we expect total revenue growth to increase slightly to 25% YoY, or around S$696mn, roughly in line with the company’s guidance of S$690mn-700mn, led to strong growth across all segments and verticals

RULE OF 40

The “Rule of 40” was first introduced as a benchmark to measure the balance between growth and profitability of SaaS companies, taking into account both revenue growth, as well as profitability (Revenue Growth + EBITDA Margins), with the addition of both metrics needing to exceed the 40% threshold. We have modified this slightly by averaging revenue growth over a 3-year period compared to just a single period growth rate. Adding together TDCX’s 3-year average revenue growth of 45.2% and its EBITDA margin of 32.4%, the total of 77.6% is > than our required threshold of 40%.

EXPENSES

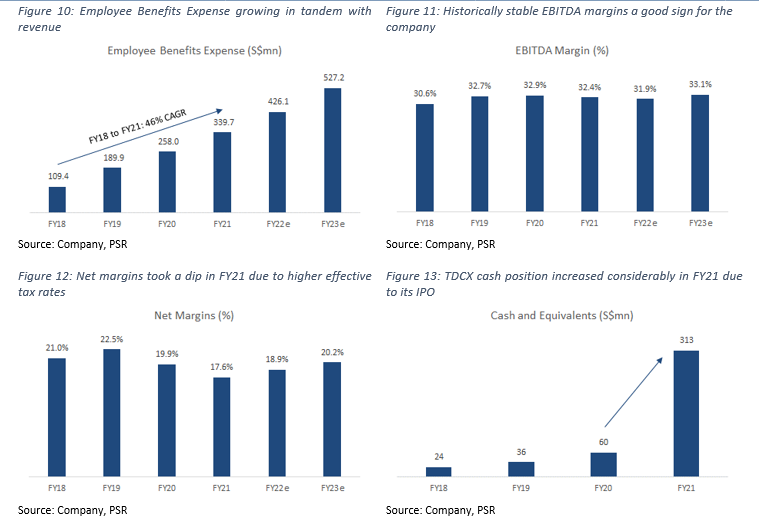

As a service provider, the bulk of TDCX’s expenses come from employee-related expenses which the company labels as “Employee Benefits Expense”. In FY21, the company recorded S$340mn in Employee Benefits Expense, which represents roughly 61% of revenue (Figure 10). This expense grew 32% YoY, slightly faster than revenue growth, and was primarily due to an increase in employee headcount to support business volume, and share-based expenses from the introduction and implementation of the company’s maiden performance share plan.

MARGINS

TDCX recorded gross profit margins of 38.8% for FY21, a slight decrease from 40.7% the year before, and was mainly due to an increase in Employee benefits Expense.

EBITDA margins for FY21 remained stable at around 32.4% (Figure 11), with a 4-year range of 30-33%. This is significantly higher compared with its peers: TaskUs (24.8%), Concentrix (16.2%), Teleperformance (15.1%), Telus International (24.6%)

Net margins for FY21 were 17.6% (Figure 12), and have been decreasing slightly over the last few years, this has been largely due to an increasing effective tax rate.

BALANCE SHEET

Assets: Cash and cash equivalents increased from S$60mn to S$313mn in FY21 (Figure 13), due to an inflow of capital from the company’s IPO listing. Receivables increased from S$49mn to S$106mn, and this was due to a couple of large clients that had some administrative challenges, leading to a backlog in billings. These receivables had been recovered during the middle of 1Q22. TDCX recorded total assets of S$582mn in FY21.

Liabilities: Short-term and long-term debt reduced by S$10mn and S$13mn respectively, and this debt was paid down using cash from the company’s IPO listing in FY21. Other payables were recorded at S$39mn for FY21, with lease liabilities (both current and non-current) amounting to S$36mn.

CASH-FLOW

TDCX recorded Free Cash Flow (FCF) of S$83mn in FY21, a 27% YoY decrease from FY20, largely in part from a S$58mn increase in receivables which were collected only in 1Q22. The company has been FCF positive since FY18, and we expect this trend to continue moving forward based on its highly stable, cash generative business model.

BUSINESS MODEL

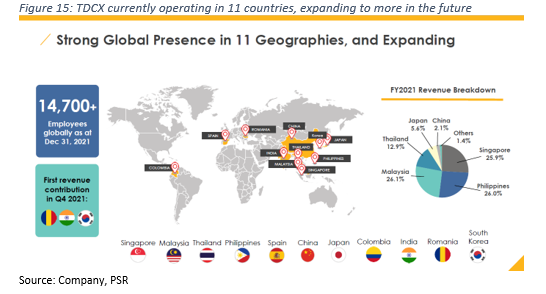

TDCX operates as an outsourced digital customer experience provider, with 3 main pillars of focus: Omnichannel Customer Experience (CX), Sales & Digital Marketing, Content Monitoring & Moderation. The company focuses predominantly on servicing fast growing new economy clients, particularly in the Southeast Asian region, while looking to other Asian and European markets for opportunities to expand. As of end FY21, TDCX had 52 clients, 20 of which were added in FY21 alone, and extend to a wide range of verticals ranging from travel and hospitality to fintech. Prominent clients of TDCX include leading social media platform, Facebook, leading travel & hospitality platform, Airbnb, and leaders in other high-growth verticals (Figure 14).

The company currently has almost 15,000 employees globally, with 3,000 additions in 4Q21 alone (Figure 15), and is constantly striving to keep up with the needs of its fast-moving clients. TDCX has a very extensive network of delivery centers both from a local level, and a regional level, with talent proficient in more than 20 languages and a deep understanding of high-growth verticals in the region – a key component when serving such a diverse group of geographies. From a strategic point on view, leverages on its expertise and presence in the different countries it operates in to help cross-border expansion of its clients.

TDCX leverages on technology like Artificial Intelligence and Machine Learning to improve the quality and efficiency of its services, they also deploy bots and robotic process automation (RPA) to drive productivity gains. As their business model is very labour reliant, TDCX has also developed a proprietary virtual recruitment platform, Flash Hire, to assist in speeding up its own hiring process, improving the company’s ability to scale and fulfil the requirements of its clients at a fast and efficient rate. According to the company, Flash Hire helped to reduce hiring time by almost 62%.

TDCX’s revenue stream comes mainly from service contracts it negotiates with its clients, which usually run from 1-3 years and are generally quite sticky in nature. Some of the terms in these contracts include clauses like variable relocation benefits, which allow TDCX to charge their clients accordingly if the cost of living fluctuates in a particular region.

Omnichannel Customer Experience (CX): This segment entails managing clients’ customer relationships by providing both inbound and outbound customer experience solutions, which also generally cover the entire life-cycle of the customer. The services that fall under this segment are also usually highly tailored to specific companies or verticals, and also involve more complexed interactions between agent and customer – technical end-user troubleshooting for software and consumer electronic devices, aftersales service and support, etc. TDCX uses metrics like average inbound holding time and percentage of first call resolution to measure its service levels.

Sales & Digital Marketing: It develops digital advertising campaigns for B2B and B2C clients to market their products and services. For B2B, this usually involves helping an advertising platform client grow and attract more advertising dollars, while B2C generally involves more sales and direct-marketing capabilities for clients. TDCX leverages on its analytical capabilities in this domain to provide valuable business insights to increase marketing efficiency. Return on advertising spend and conversion ratios are some metrics TDCX monitors to ensure performance of its marketing services.

Content Monitoring & Moderation: It assists clients in creating a safe and secure online environment for social media and gaming platforms through content monitoring and moderation services performed by an actual human.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Jonathan covers the US technology sector focusing on internet companies. Formerly a national and professional athlete, he graduated from the University of Oregon with a Bachelor’s Degree in Social Sciences.