Company Background

Sembcorp Industries (SCI) is a leading energy and urban development group, operating across multiple markets worldwide. As an integrated energy player, SCI is uniquely positioned to support the global energy transition. SCI’s urban arm is a recognised Asian developer, and has saleable land of 2,600 hectares of saleable industrial, business, commercial and residential land.

Investment Merits

Outlook

We are positive on the Group’s outlook. We believe the deconsolidation of a SCM will unlock value for SCI shareholders through disciplined capital allocation and systematic capital recycling, and allow both companies to drive long-term value creation in their respective fields.

Initiating coverage with a BUY rating and target price of $2.72

We initiate coverage on SCI with a BUY recommendation and a target price of $2.72. We peg SCI to a P/BV of 0.7x FY21e, which is a slight discount to their 10 year historical average equity value (ex. SCM). SCI shareholders will also receive 4.911 of SCM shares for every 1 share held. Based on SCM’s last closing price of $0.199 on the 7 September, SCI shareholders could realise a total of $2.72/share ($1.75 + (4.911 x $0.199). We expect SCI to see improved profitability and generate positive operating CF of $854mn and $1.2bn for FY21e and FY22e respectively, which will strengthen their balance sheet and puts them in a good stead to ride out the current crisis.

Background

Sembcorp Industries is a leading energy and urban development group, operating across multiple markets worldwide. They have three main business arms, energy, marine and urban.

On the 8 June 2020, SCI and Sembcorp Marine (SCM) (Not rated) announced the deconsolidation of their respective businesses. SCM provides innovative engineering solutions in the global offshore, marine and energy industries. Headquartered in Singapore, the SCM Group has close to 60 years of track record in the design and construction of rigs, floaters, offshore platforms and specialised vessels, as well as in the repair, upgrading and conversion of different ship types. Its solutions focus on the following areas: Gas value chain, renewable energy, process, advance drilling rigs, ocean living and maritime security.

As a diversified energy and urban player, SCI is uniquely positioned to provide integrated solutions to meet their stakeholders’ needs. Leveraging technology and digital innovation, the draw on their deep understanding across their business and global track record to provide a suite of integrated energy and urban solutions that support the energy transition and sustainable development.

Key Business Segments

The Energy segment’s activities are in the provision of power and water to industrial, commercial and municipal customers. Key activities in the power sector include power generation, process steam production, as well as natural gas importation. In the water sector, the business offers wastewater treatment as well as the production of reclaimed, desalinated and potable water for industrial use. In addition, the business also provides on-site logistics, solid waste management and specialised project management, engineering and procurement services

The Marine segment focuses on providing integrated solutions for the offshore and marine industry. Key capabilities include rigs & floaters, repairs & upgrades; offshore platforms and specialised shipbuilding. From the fourth quarter of FY20e, this will be deconsolidated from SCI.

The Urban segment owns, develops, markets and manages integrated urban developments comprising industrial parks as well as business, commercial and residential space in Asia.

The Others/Corporate segment comprises businesses mainly relating to minting, design and construction activities, offshore engineering and others.

Investment Merits

Initiating coverage with BUY rating and target price of $2.72.

We initiate coverage on SCI with a BUY recommendation and a target price of $2.72. We peg SCI to a P/BV of 0.7x FY21e, which is a slight discount to their 10 year historical average equity value (ex. SCM). SCI shareholders will also receive 4.911 of SCM shares for every 1 share held. Based on SCM’s last closing price of $0.199 on the 7 September, SCI shareholders could realise a total of $2.72 per share ($1.75 + (4.911 x $0.199). Following the deconsolidation of SCM, we expect SCI to see improved profitability and generate positive operating cash flow of $854mn and $1.2bn for FY21e and FY22e respectively, which will strengthen their balance sheet going forward.

The Transaction: Enhancing shareholder value and increased strategic focus

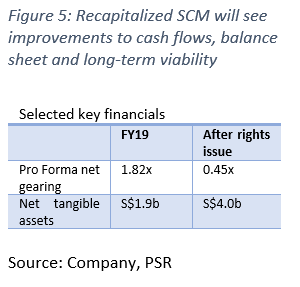

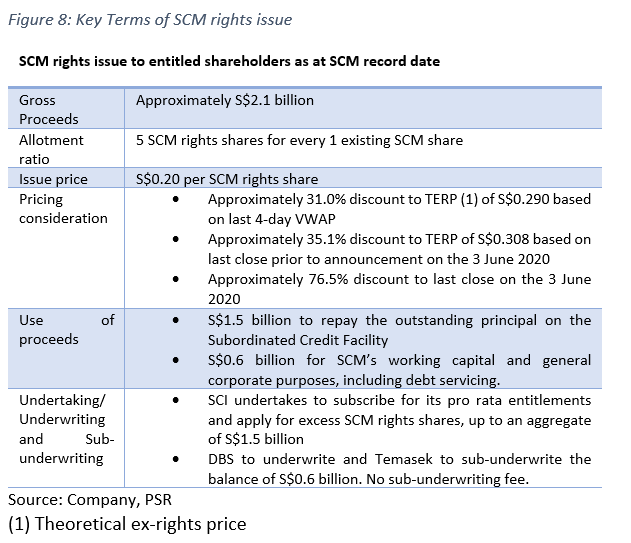

Recapitalised rights in SCM. SCM raised S$2.1bn in equity via a 5-for-1 renounceable rights issue of 10,463,723,020 new ordinary shares at S$0.20 per rights share. SCI undertook to subscribe for up to S$1.5b of SCM rights shares by setting off the outstanding principal of S$1.5bn under the subordinated loan facility extended to SCM, while Temasek Holdings has sub-underwritten the remaining S$0.6bn. With the proceeds, SCM has repaid SCI’s S$1.5bn subordinated loan facility, improving their overall net gearing for proforma FY19 to 0.45x from 1.82x.

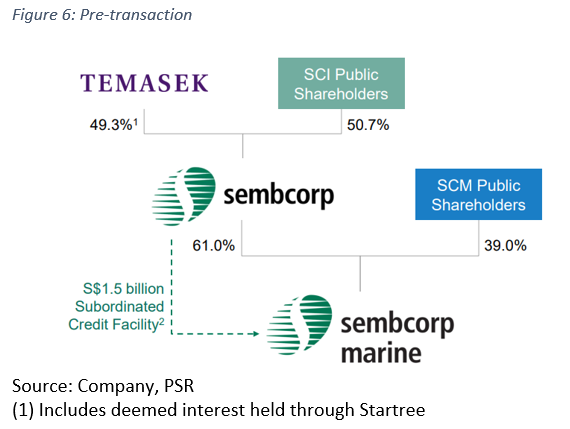

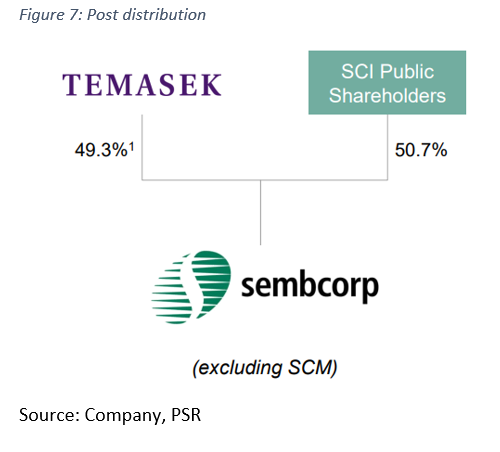

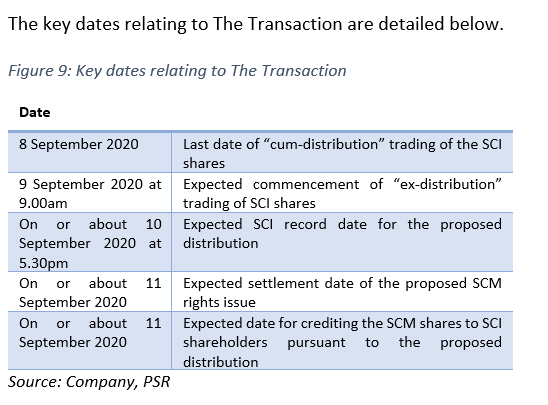

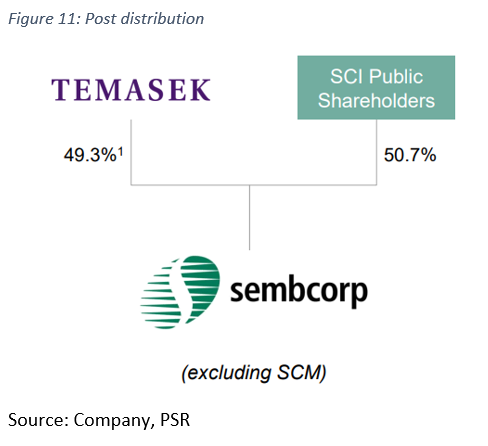

Following the completion of SCM’s rights issue, and SCI’s subscription of 7,500,000,000 rights shares, representing approximately 72% of the 10,462,690,870 rights share available under the rights issue, SCI will distribute 4.911 SCM shares per every 100 SCI shares held by shareholders on the last date of “cum-distribution” trading of SCI shares. (see Figure 6 for pre-transaction and Figure 7 for post distribution). No payment is required from SCI shareholders to receive shares in SCM. SCI shareholders will have direct shareholdings in two focused companies, with Temasek alongside as a direct and significant shareholder. Importantly in our view, SCI shareholders now gain the flexibility to calibrate their holdings in the two companies based on their own investment objectives and strategy.

The Transaction: Enhancing shareholder value and increased strategic focus

The key terms of SCM’s rights issue are summarised below.

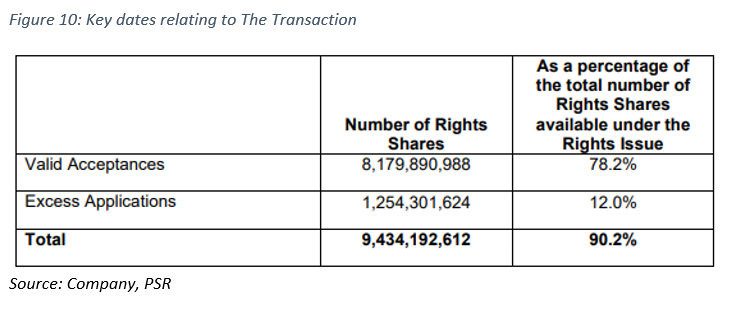

On the 7 September, SCM announced the successful completion of the rights issue. The company announced that valid acceptances and excess applications were received for 9,434,192,612 rights shares, representing approximately 90.2% of the 10,462,690,870 rights shares available under the rights issue.

The Transaction: Enhancing shareholder value and increased strategic focus

Details of the valid acceptances and excess applications received for the rights shares are shown below (Figure 10):

Pursuant to the sub-underwriting agreement, Startree, a wholly-owned subsidiary of Temasek, has subscribed for the balance of 1,028,498,258 unsubscribed rights shares.

With the proceeds, SCM has repaid SCI’s S$1.5bn subordinated loan facility, improving their overall net gearing for proforma FY19 to 0.45x from 1.82x and net tangible asset from S$1.9bn to S$4.0bn.

The Transaction: Enhancing shareholder value and increased strategic focus

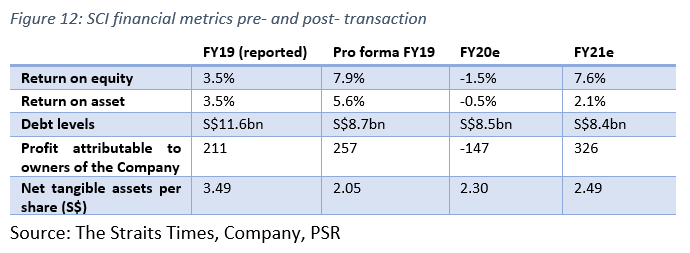

Following SCI’s subscription of 7,500,000,000 rights shares, representing approximately 72% of the 10,462,690,870 rights share available under the rights issue, SCI will distribute 4.91 SCM shares per every 100 SCI shares held by shareholders on the last date of “cum-distribution” trading of SCI shares. We have also detailed the financial metrics of SCI post-transaction in Figure 12 below.

We see a number of positives in the move to separate SCI’s core business from their marine interest in SCM. The primary benefit we believe is that the move will unlock value for SCI shareholders by creating two focused companies. New demand patterns emerging in the energy sector require SCI to be focused on competing effectively, and focused on their core businesses (Energy and Urban). However, SCI’s future growth may be constrained by the SCI Group balance sheet which consolidates SCM’s debt.

The settlement of SCM’s subordinated loan with SCI and the proposed distribution delivered a clean demerger with an immediate deleveraging of SCM, which will benefit shareholders of SCM. SCI shareholders will receive SCM shares, with no cash outlay, in a recapitalised SCM with a significantly reduced net gearing from 1.82x to 0.45x due to the settlement of the subordinated loan with SCI and the improved cash position arising from the rights issue. SCI’s profitability and returns profile will also improve going forward. We expect SCI to see an improvement in their profit from a loss of $147m in FY20e to $326m and $449m for FY21e and FY22e respectively.

Lastly, the demerger will create two focused companies, allowing SCI to focus on their core competency. The demerger also delivers a clear investment proposition and makes SCI more comparable to their peers, and also reduce the conglomerate discount attached to SCI. This is expected to lead to a potential positive re-rating of SCI.

Revenue

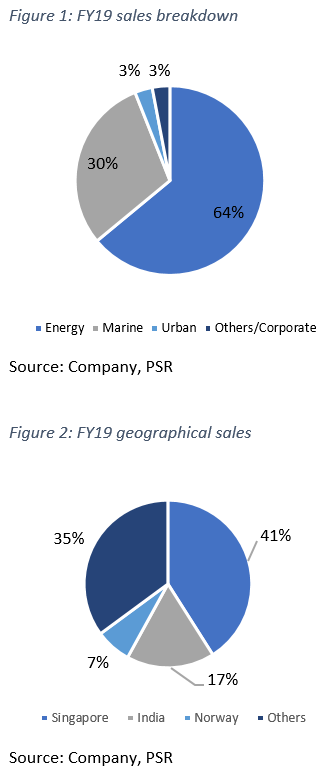

Energy comprises 64% of FY19 revenue. SCI’s energy business continues to undergo business transformation, as energy production continues to shift away from a reliance on fossil fuels to renewable energy. Over the years, SCI has been reshaping their energy portfolio mix into one that has a greater focus in renewable energy. Since 2016, net profit from their renewable business has increased nearly five-fold to S$80 million.

In their recent 1H20 results, turnover from this segment declined 19% compared to last year. The lower turnover was mainly due to the decrease in energy demand and prices from the reduction in economic activity and lockdowns arising from COVID-19. This adverse impact was mitigated by plants with long-term contracts where revenue is based on plant availability. For FY20e, we expect SCI to report S$5.3bn (-13% y-y) in revenue from this segment as the impact of COVID-19 and the reduction in economic activity as a result of lockdowns in multiple markets led to a decrease in energy demand and prices.

Going forward, Energy is expected to make up 97% of SCI’s revenue from FY21e following the deconsolidation of SCM. We expect the recovery in this segment to be driven by a recovery in economic activity in Singapore, India and the UK as lockdowns in these markets ease resulting in a recovery in energy demand.

Marine comprises 30% of FY19 revenue. 2019 continued to be a challenging year for the Marine business with intense competition and continued low work volume adversely impacting overall performance. In their latest 1H20 results, turnover decreased 41% y-y while SCI’s share of Marine net loss (before exceptional items) came in at S$117mn vs. the loss of S$6mn from the same period last year. Even though there has been no cancellation of any existing projects to date, there has also been no significant new orders this year. We expect SCM to continue reporting losses in FY20e and FY21e as intense competition and continued low work volume continue to weigh on their operations.

Following the deconsolidation of SCM, this segment will no longer contribute to the financial performance of SCI from FY21e.

Urban comprises 3% of FY19 revenue. SCI’s urban businesses comprise mainly associates or joint ventures which are accounted for under the equity method, turnover of the business is therefore not material. In their latest 1H20 results, net profit of S$38mn was S$20 mn higher than the corresponding period last year. The improvement was largely due to the higher contribution from Nanjing’s residential land sale and Kendal Industrial Park. Total land sales in 1H20 was 85 hectares, slightly lower than 1H19, and this is mainly due to lower land sales in Vietnam, offset by higher land sales in China and Indonesia.

For FY20e, we expect the profitability of the urban business to be lower vs. FY19 due to lower contribution from projects in China and Vietnam. COVID-19 has resulted in land property sales to be impacted, the uncertain economic outlook has led to lower take-up and demand, as well as delayed launches for some of the business’ integrated developments and properties. We expect land and property sales to recover in FY21e as regulatory and other approvals resume following delays earlier in the year.

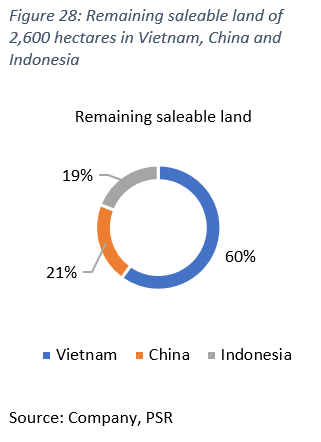

The Urban business still has a significant landbank of 2,600 hectares of saleable industrial, business, commercial and residential land. The integrated urban developments in Vietnam, China, and Indonesia, and that will underpin its future performance. The stabilisation of the economic outlook is expected to improve take-up for the business’ integrated developments and properties.

Balance Sheet

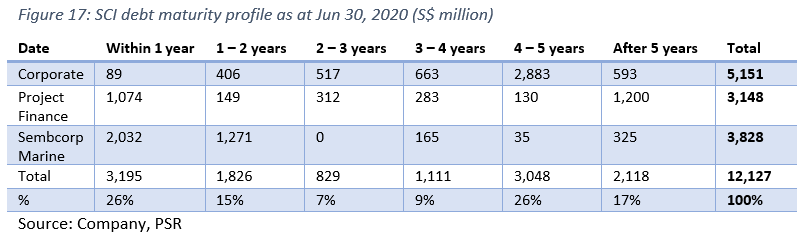

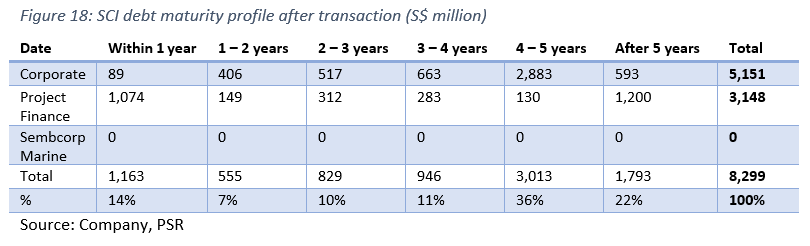

Based on their 1H20 results, SCI has a gross gearing and net gearing of 1.9x and 1.6x respectively. More than half (52%) of this is in bank loans, another 22% of this is in bonds while the remaining 26% is in project finance loans. SCI borrowings have a weighted average debt cost of 3.5%, of which 64% is fixed.

Following the rights issue by SCM, SCI’s obligation to pay the SCM rights subscription amount has been offset against an equivalent amount of the principal amount outstanding and due and owing to SCI by SCM under the subordinated credit facility. We have detailed SCI’s debt maturity profile after the transaction below.

We estimate the proforma book value of SCI for FY20e to be S$4.1bn, or S$2.30 per share following the rights issue from SCM. We believe the market could ascribe a 0.7x P/Bv for SCI (ex.SCM) to account for its energy and urban development business. Even though our estimates suggest the forward ROE for FY21e and FY22e to be 7.6% and 9.6% respectively, we think confidence in the management’s ability to execute will take time to realise, resulting in a discount in their overall net asset value.

While we acknowledge that the overall net gearing level will increase from 120.6% in FY19 to 187.1% for FY20e due to the lower equity base and the distribution-in-specie to SCI shareholders. We argue that the demerger will actually result in lower capital requirements gong forward as SCI will be able to focus on their core businesses without having capital tied up in SCM. Moreover, SCI’s debt servicing ability will also improve post de-merger, and we expect that SCI will be able to reduce the debt load going forward. For FY21e and FY22e, we expect SCI’s net gearing to be reduced to 176% and 155% respectively.

Cash Flow

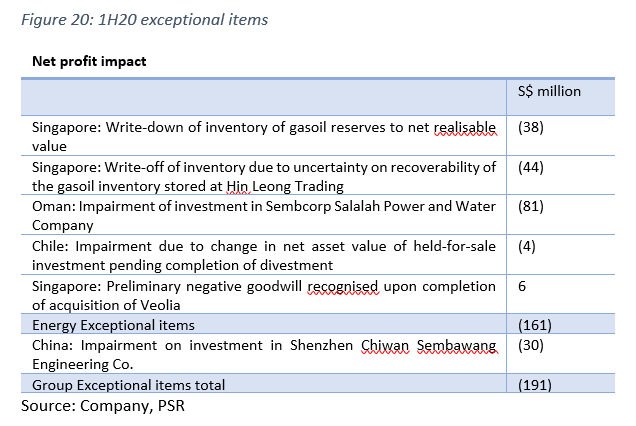

Full year FY20e loss expected, but operating cash flow to remain positive. We expect SCI to report a loss of S$92mn for FY20e due to the expected continuing losses at SCM and the exceptional items amounting to S$191mn (Figure 20) recorded in 1H20. That said, we still expect SCI to report positive operating cash flow for FY20e.

Moving forward, we expect SCI to generate positive operating cash flow of S$853mn and S$1.2bn for FY21e – FY22e. Without the drag of SCM’s negative cash flow, we expect a substantial improvement of SCI’s operating cash flow from FY21e. The Energy and Urban businesses generate relatively stable long-term cash flow streams and the demerger with SCM will allow SCI to allocate capital solely to its core businesses.

While SCI has no fixed dividend policy in place, they have paid out dividends of between 4 and 5 Singapore cents for FY17- FY19, representing 24 – 42% dividend payout ratio. The Group’s decision to suspend the interim dividend for 1H20 and to defer this to the full year reflects the challenging environment the Group is facing. With the demerger of SCM now completed and our expectation for the Group to report a positive operating cash flow for FY20e, we think the Group could pay out a dividend in for the full year FY20e. In our forecasts though, we have forecasted zero payout for FY20e to be prudent.

Notwithstanding the economic outlook beyond FY20e, we think the demerger of SCM will reduce the capital requirement of SCI as they focus capital on their respective businesses. For FY21e and FY22e, we expect SCI to report free cash flow of S$53mn and S$377mn respectively, which should support the resumption of their dividend payout.

IPO of Sembcorp Energy India Ltd to crystalise value of India business

SCI could crystalise the value of their India business by listing their energy unit in India, Sembcorp Energy India Limited. SCI first filed its draft red herring prospectus lodged into the Securities Board of India in 2018, but subsequently withdrew this as it was injecting new equity into the business. SEIL further announced that it intends to refile a revised prospectus at “an appropriate time.., taking into consideration market conditions.”

SCI first entered the India market in 2010, establishing itself as a reliable independent power producer in the country focused on growing a clean energy portfolio. With a presence across nine states, SEIL owns and operates 35 assets, adding up to a total power capacity of 4,370MW including 1,730MW of renewable energy. The outlook for the India market remains positive, energy consumption is expected to see an increase of over 100% from 2015 to 2035.

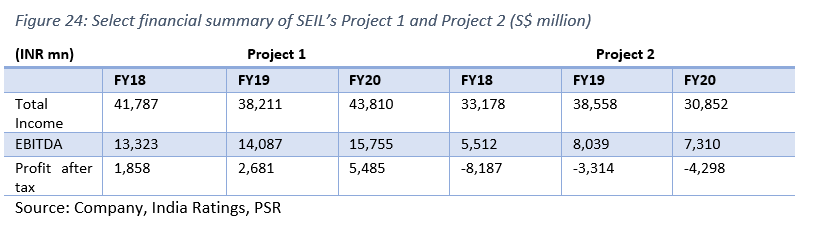

SEIL owns and operates 2,640MW of thermal power projects consisting of Project 1 and Project 2. SEIL’s bank facilities have a AA- rating, with a stable outlook awarded by India Ratings (a wholly-owned subsidiary of the Fitch Group).

Going forward, we believe SEIL will pursue longer-term power purchase agreements (PPAs) as these guarantee a stable tariff higher than the spot rate and also gives them access to domestic coal supply where prices are lower and more stable than imported ones. Unlike the short-term PPAs which suffer from thin or even negative spark spread, long-term PPAs provide more profit visibility for plants. For FY19, India posted a net profit of S$100mn (accounting for 48% of their FY19 profit) vs. S$47mn in 2018 mainly due to the higher contribution from its thermal power plants as well as improved operating performance by its renewable energy assets on better wind resources and new capacity addition.

IPO of Sembcorp Energy India Ltd to crystalise value of India business

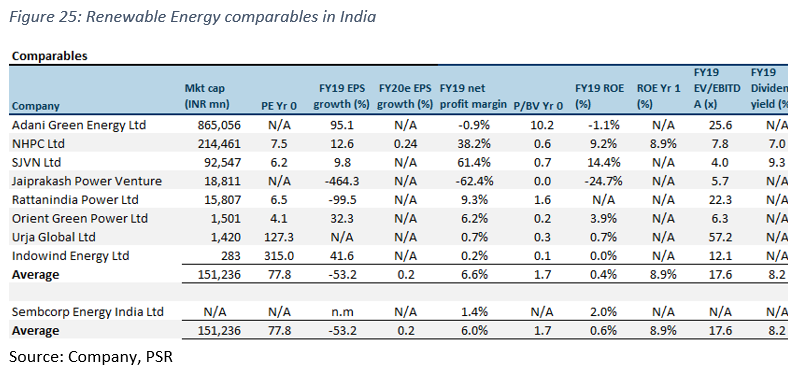

Renewable energy companies in India trade at about 1.7x of their book value, based on SEIL’s FY19 book value of INR65.4bn, this implies a market capitalisation of about INR111.2bn (or about S$2.1bn). We impute a slight discount to the sector average P/BV to account for SEIL’s lack of a listing track record to arrive at a valuation of INR98.1bn or S$1.8bn (~1.5x FY19 P/BV).

While the timing of SCI’s India Energy IPO remains uncertain, we believe SCI’s acquisition of the remaining 5.95% stake in SEIL for INR4.6bn (approximately ~S$77mn) in December last year (implying a 1.2x FY19 P/BV or a market capitalisation of INR77.3bn or S$1.5mn) will allow SCI to have the flexibility as sole owner to evaluate and pursue a full range of growth opportunities in the renewables segment, while at the same time seeking the right equity window to list its India business or to pursue other capital-recycling options.

Future plans

Going forward, we think SCI’s future focus will centre around the following themes set out below:

SCI transformed into a focused Energy and Urban business. SCI’s move to deconsolidate SCM will allow SCI to focus their resources and efforts on repositioning its Energy and Urban business, and capturing growth opportunities to provide solutions that support the energy transition and sustainable development. To that end, we believe SCI will focus on growing their renewables capacity, and reach approximately 4,000 megawatts by 2022.

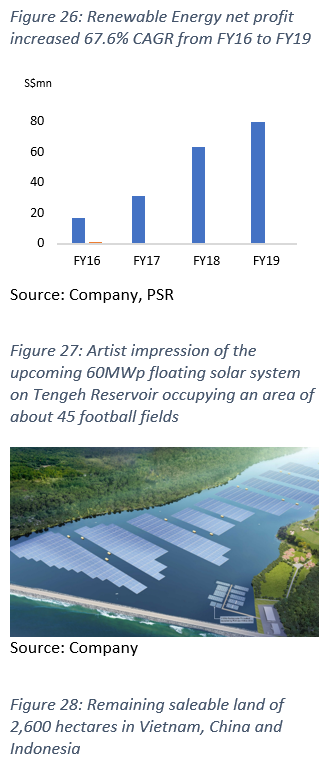

Net profit from SCI’s renewable energy portfolio has increased by a CAGR of 67.6% per year from FY16 – FY19. As a proportion of total net profit from Energy, this has increased from just over 2% to 8.4% in FY19. Going forward, we expect SCI to grow their renewables energy footprint in key markets in Singapore, China, India and the UK. In Singapore, construction of the 60 MWp floating solar photovoltaic system on Tengeh Reservoir (see Figure 27) commenced last month. The project is expected to begin full commercial operations next year with a 25-year power purchase agreement signed with PUB, Singapore’s National Water Agency.

The Energy and Urban business has historically generated relatively stable long-term cash flow streams, even with the Energy market exposed to the merchant market. We think the demerger will allow SCI to allocate capital solely to its core businesses. We expect their balance sheet and cash flows to improve post deconsolidation from SCM as the capital requirement falls. We expect net gearing to be reduced from 187% in FY20e to 177% and 155% for FY21e and FY22e respectively.

For their Urban business, SCI still has remaining saleable land of 2,600 hectares of saleable industrial, business, commercial and residential land (see Figure 28). In our view, SCI is positioned in key growth areas in Vietnam, China and Indonesia. In Vietnam, they have nine projects strategically located in the southern, central and northern economic zones. In China, they are situated in key growth regions, and are well placed to benefit from the shift towards central-western China development. In Indonesia, central Java is expected to benefit from spillover investments from Jakarta.

We see a number of synergies in SCI’s Energy and Urban business, and we believe SCI will focus on capturing trends like urbanisation, electrification and decarbonisation.

The listing of SEIL will recycle capital and crystalise value on SCI’s India Energy portfolio. While the timing of SEIL’s listing remains uncertain, we think this will happen sooner rather than later.

SCI’s move to acquire the remaining 5.95% stake in SEIL last December (implying a 1.2x FY19 P/BV or a market capitalisation of INR77.3bn or S$1.5mn) will give the company more flexibility as sole owner to evaluate and pursue a full range of growth opportunities in the renewables segment, while at the same time seeking the right equity window to list its India business or to pursue other capital-recycling options.

Valuation

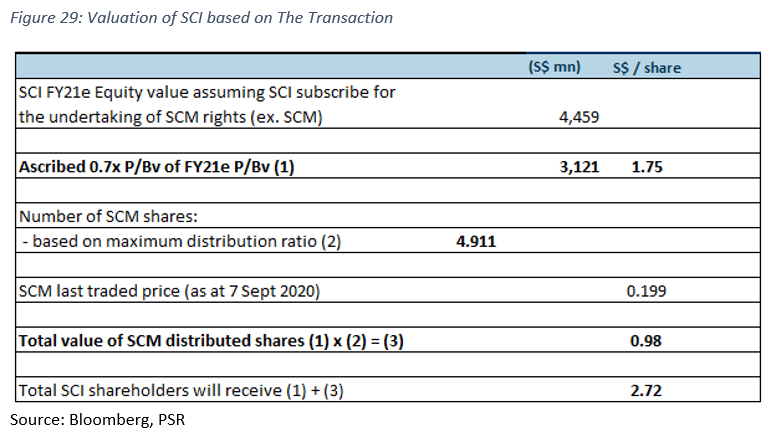

We initiate coverage on Sembcorp Industries with a BUY recommendation and a target price of $2.72. We peg SCI (ex. SCM) to a P/Bv of 0.7x FY21e, and 4.911 distributed shares in SCM to calculate the SCM shares to be distributed to SCI shareholders. In total, we expect that SCI shareholder could get $2.72 based on our assumptions below.

We believe the market could assign a 0.7x P/BV for SCI (ex. SCM), a slight discount to the 10 year historical average of the implied SCI (ex. SCM) P/BV to account for their Energy and Urban business to S$1.75 a share. Based on the 7,500,000,000 rights shares which SCI had subscribed for in accordance with the SCI undertaking agreement, this means that 4.911 of SCM shares will be distributed to SCI shareholders. Based on SCM’s last closing price of S$0.199 on the 7 September, SCI shareholders could receive a total of S$2.72 (Figure 29). Our forecast of SCI does not include a valuation on SCM.

The recapitalisation of SCM, followed by a demerger to create two focused companies will allow SCI to focus on their core competency. The demerger also delivers a clear investment proposition and makes SCI more comparable to their peers. The deconsolidation of SCM will transform SCI into a focused Energy and Urban business. SCI will now be able to focus their resources on capturing growth opportunities in two of their key segments independently of SCM. Even though the conglomerate discount attached to SCI should narrow or disappear, we think this might take time as investor’s confidence in the management could take time to rebuild. For FY21e and FY22e, we expect SCI to see ROE improve to 7.6% and 9.6% respectively, potentially leading to a positive re-rating of SCI.

Risks

Continued lockdowns in SCI’s key markets like Singapore, China, India and UK due to COVID-19 resulting in decrease in energy, demand and prices. With little signs of COVID-19 cases worldwide abating, any lockdowns or extensions in lockdowns in SCI’s key markets like Singapore, China, India and UK will result in a reduction in economic activity, resulting in a decrease in energy, demand and prices. In 2Q20, energy demand in Singapore, India and the UK have all declined by approximately 5% to 20%, compared to the same period last year.

Uncertain economic outlook could affect take-up and demand for SCI’s integrated developments and properties. Measures undertaken by various governments to contain the COVID-19 pandemic can result in delays in regulatory and other approvals required for the Urban business’ projects. These delays in approvals accompanied with the uncertain economic outlook will have a negative impact on the overall take-up and demand for the Group’s integrated developments and properties.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Terence specialises in the consumer, conglomerate and industrials sector. He has over five years of experience as an analyst in the buy- and sell-side. As an institutional fund management analyst, he sat on the China-Hong Kong desk. Terence was ranked top 3 for Best Analyst under the small caps and energy category in the Asia Money poll 2018.

He graduated from the Singapore Management University with a major in Finance (Honours), and is the honoured recipient of the CFA scholarship.