• 3Q20 was a tough quarter. The market was down 4.7%, chalking up a 23.4% loss for the year.

• The Singapore economy has bottomed as its lockdown eases. However, after the initial lift-off, recovery has been on an upward grind.

• We expect uneven sector performances until borders are reopened or a vaccine is found. Sectors we favour are land transportation, property, electronics and REITs.

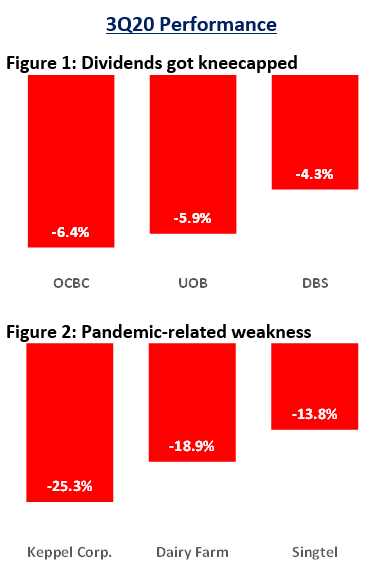

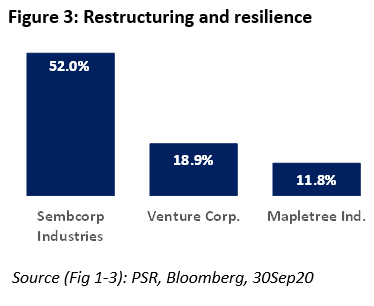

Review: 3Q20 was a tough quarter. The market was down 4.7%, chalking up a 23.4% loss for the year. STI has again underperformed most of its regional peers. Only a third of its component stocks made gains this quarter. The pandemic continued to weigh on the earnings of multiple sectors except consumer staples, healthcare (gloves) and electronics. Banks gained some price momentum for their attractive yields, but share prices were later kneecapped (Figure 1) by limitation of their dividends this year to 60% of last year’s level.

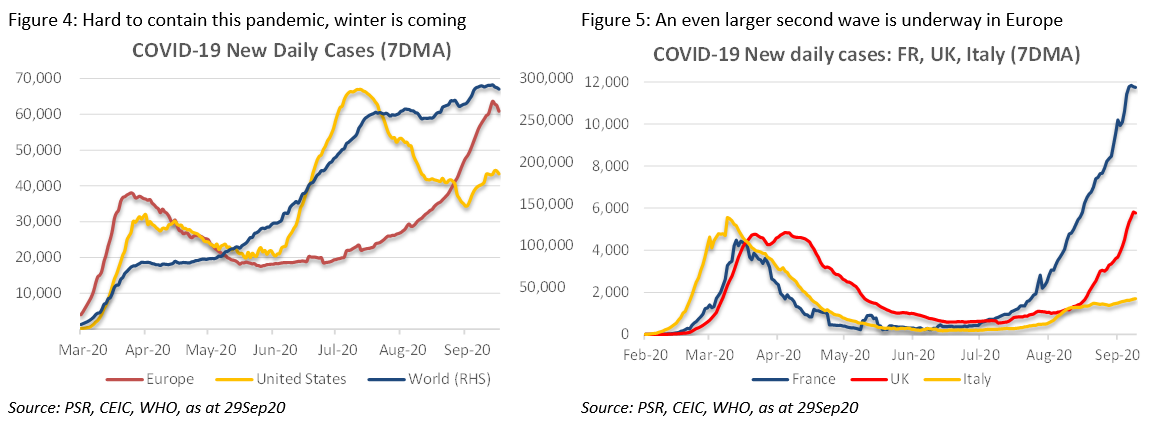

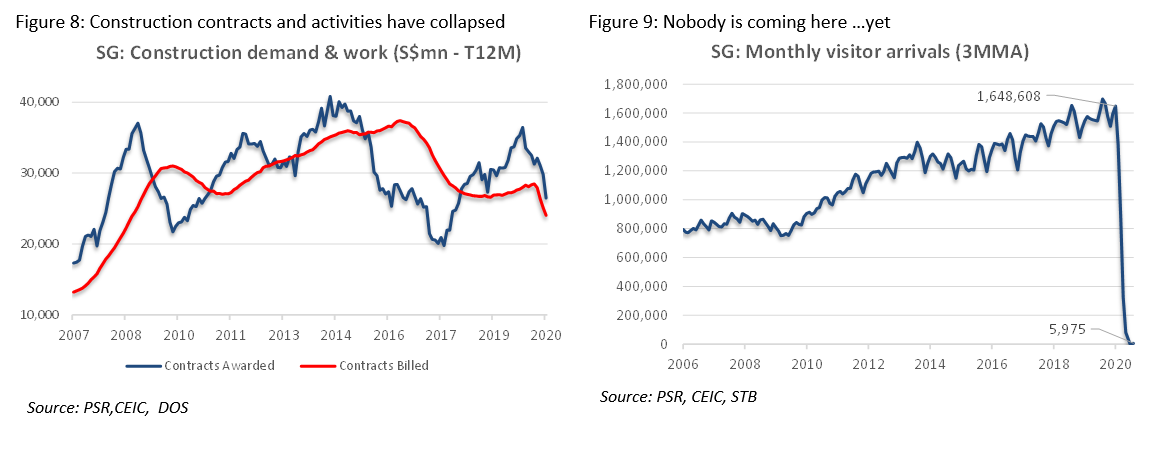

Outlook: The Singapore economy has bottomed as its lockdown eases. However, after the initial lift-off, recovery has been on an upward grind (Figures 7-8). Restrictions in international travel are expected to impede the recovery (Figure 9). Earnings for multiple sectors are expected to remain depressed without tourism. These include aviation, hospitality, healthcare, gaming, telecommunications and retail. The combined exposure of stocks to these sectors on the STI is around 20%. An added headwind for the STI could come from banks. This segment is facing a triple whammy of low interest margins, spikes in credit provisioning and restrained dividends. Banks account for 40% of the STI. Thus, at least two-thirds of STI’s component stocks will struggle with earnings this year.

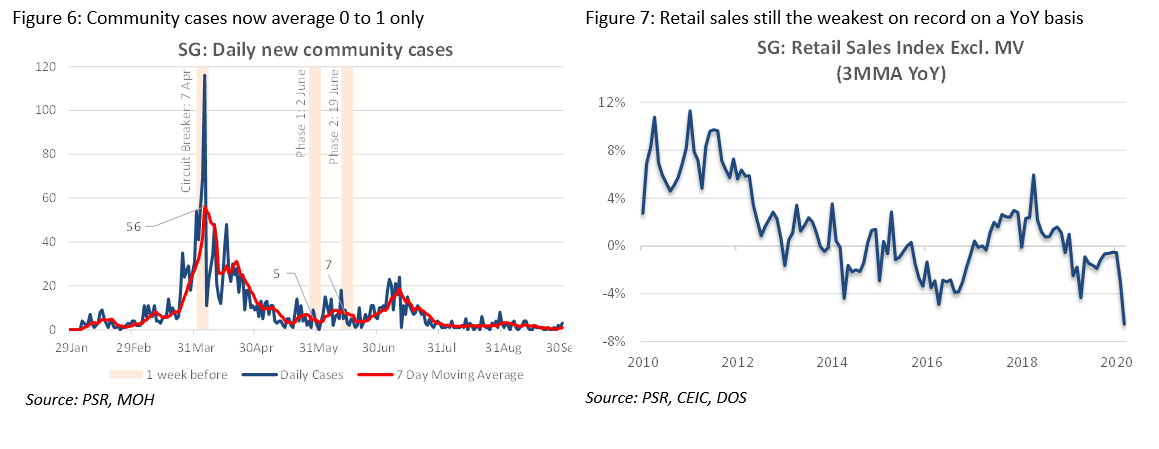

But let us not despair. There are bright spots for the market. Community cases in Singapore have collapsed to a weekly average of one. We can expect further relenting of the lockdown through green lanes and larger group gatherings. Record-low interest rates have also made the dividend yields of the Singapore market stand out in this yield-starved environment. While U.S. elections may produce some near-term jitters, especially with a contested election, current betting odds – and yes, polls – favour a Biden win. A Biden win will be positive for Asian assets and currencies. It will likely mean less belligerent foreign and trade policies.

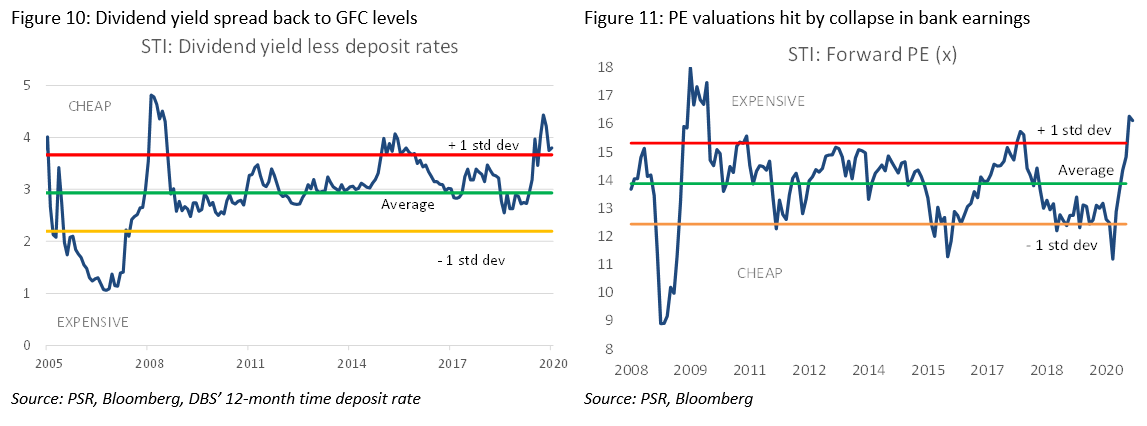

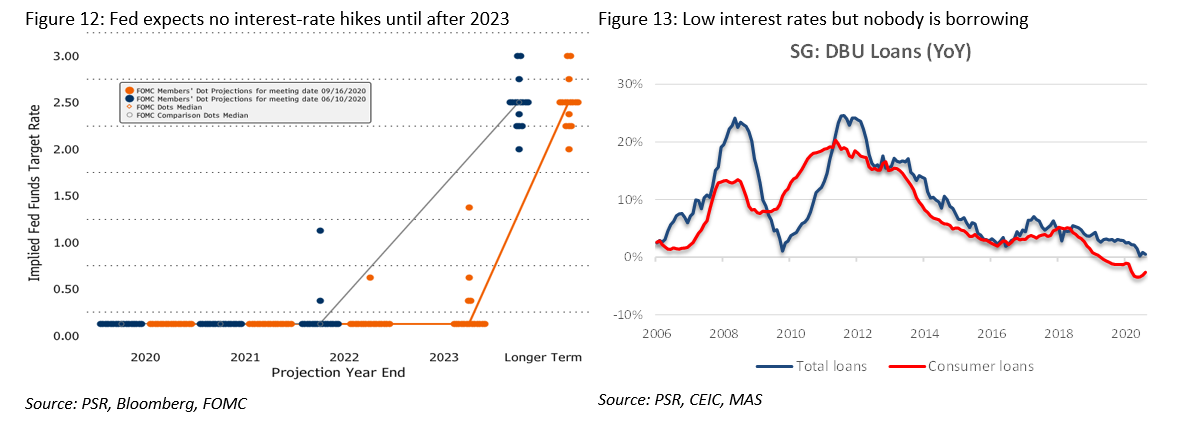

There will always be something to worry investors. But with interest rates so depressed, equities are the most viable investment option. Rates for 12-month Singapore dollar time deposits hover at 0.15% – 0.25%. In comparison, forecast dividend yields for the STI stand at 4%. This difference between deposit rates and dividend yields reveals one of the cheapest equity markets since the GFC (Figure 10). Furthermore, depositors will be stuck on these measly rates for some time (Figure 12). In contrast, corporate dividends can grow. Only 45% of corporate earnings are paid as dividends. The remaining 55% is retained for growth, historically at 8% which is the STI’s ROE. Another margin of safety available for investors is the STI’s 23.4% retreat this year. To our minds, dividends can only recover after this nasty recession.

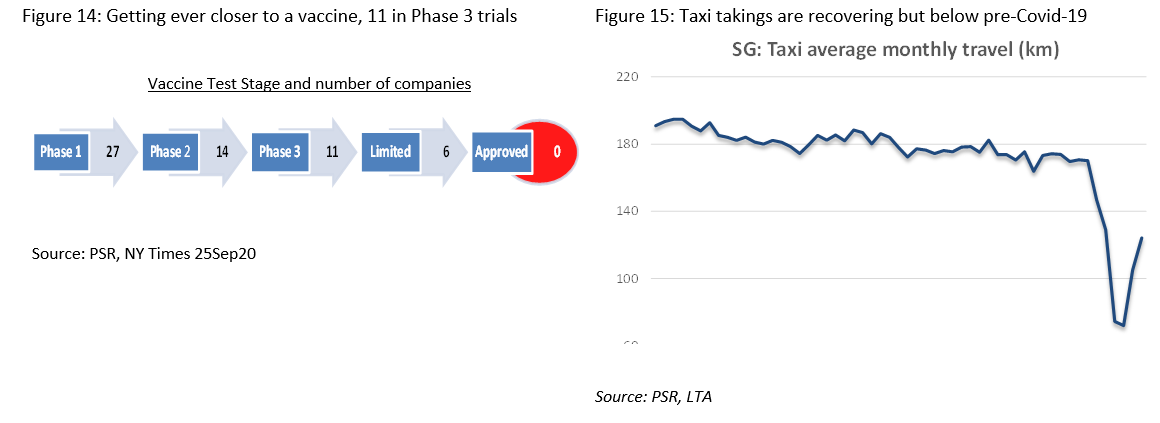

Recommendation: We expect uneven sector performances until borders are reopened or a vaccine is found (Figure 14). In all likelihood, businesses reliant on cross-border travel will remain moribund and we are underweight. Sectors we favour are land transportation, property, electronics and REITs. As the economy reopens in Singapore, the immediate beneficiary should be land transport. More group gatherings are expected to lead to more travel for business, classes, work, leisure and worship. The property sector has been surprisingly resilient with new units sales rising modestly this year. Developers have been more sanguine on product pricing. Electronics has been a growth sector even in these recessionary conditions. The work-at-home economy has boosted demand for cloud, edge and mobile computing. Other structural drivers that remain for electronics are a ramp-up in 5G infrastructure, the further electrification and automation of cars and accelerated migration of the supply chain from China to SE Asia. On REITs, the 8% yields offered by Singapore-listed US REITs look the most compelling. These REITs enjoy long leases, quality tenants and Class A buildings. So far, office tenants are the least exposed to the current spate of job losses in the U.S.

Phillip Absolute 10

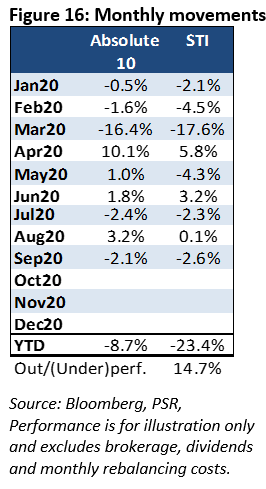

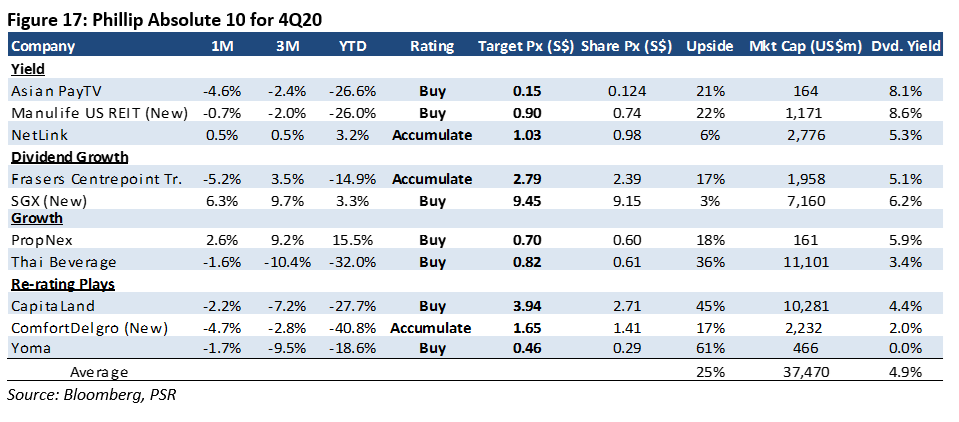

Our Phillip Absolute 10 outperformed the STI in 3Q20 (Figure 16) with a decline of 1.4% against the STI’s 4.7% loss. However, outperforming STI with capital losses “does not pay the bills”. We will look for more alpha with the following changes in 4Q20:

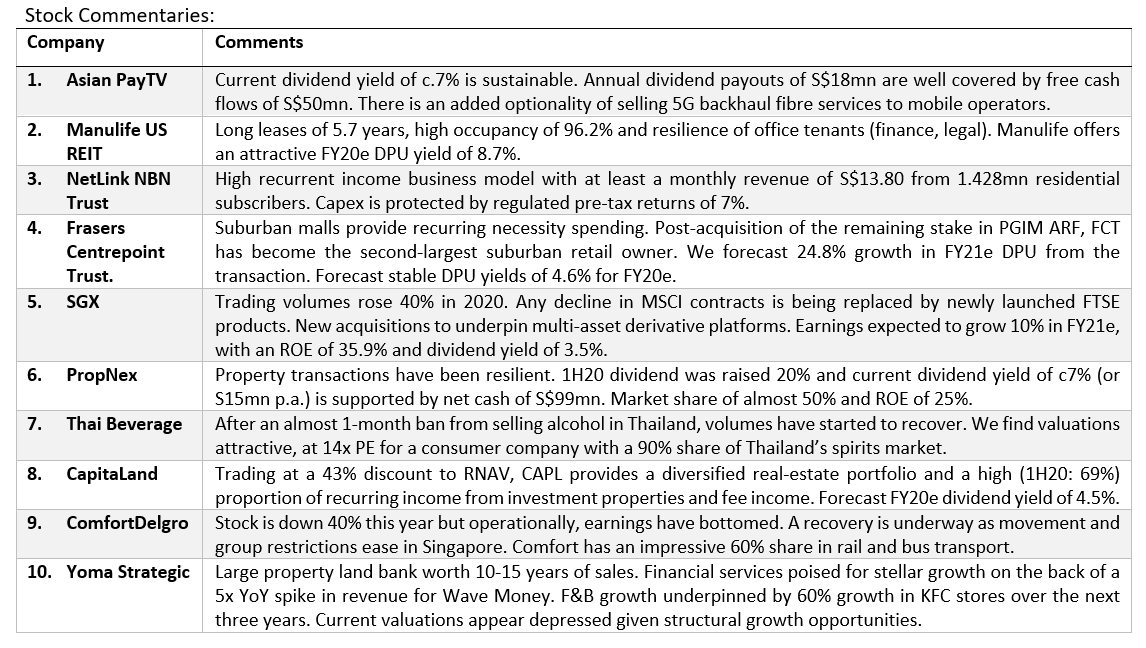

1Q20 – Add: Venture Corp., PropNex; Delete: ComfortDelGro, APAC Realty

2Q20 – Add: Thai Beverage; Delete: SingTel

3Q20 – Add: Yoma Strategic, Asian PayTV, DBS; Delete: Starhub, Sheng Siong, UOB

4Q20 – Add: ComfortDelGro, Manulife US REIT, SGX; Delete: Ascott REIT, DBS, Venture Corp.

Strategy commentary: Economic weakness is expected to persist in the medium term. Border closures likely mean tepid and uneven growth. This implies there is no beta trade and just bottom-up alpha stock picks. Our portfolio is centred on high and sustainable dividend-yielding stocks. A tactical trade for increased travel from lockdown relaxation is the inclusion of ComfortDelgro. For high yields, we have added Manulife US REIT and SGX to provide a balance of growth and yields.

Deletions from our model: We removed Ascott REIT, as the second wave of the pandemic in Europe could further delay any recovery in the hospitality industry. DBS has also been taken out due to multiple headwinds for its earnings this year. The outlook for Venture Corp is positive but the share price has already breached our target price.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Paul has 20 years of experience as a fund manager and sell-side analyst. During his time as fund manager, he has managed multiple funds and mandates including capital guaranteed, dividend income, renewable energy, single country and regionally focused funds.

He graduated from Monash University and had completed both his Chartered Financial Analyst and Australian CPA programme.