Report type: Weekly Strategy

The Expanding Inbound Tourism Consumption, the Strong Yen Threat Theory and Expectations of a Recovery in the Latter Half of the Year

Driven by the rise in stock price as a result of good financial results in Fast Retailing (9983), the Nikkei average broke through 28,500 points at one point on the 14th. The company’s stock has the largest weight (approx. 11% at the closing price on the 13th) against the index among the Nikkei average’s index components. Also in “Uniqlo” expanded by the company, sales in its China business recovered from January onwards following the end of the zero-COVID policy.

China’s consumption has pushed up the 1st quarter performance (announced on the 12th) of LVMH Moët Hennessy Louis Vuitton, a widely-known luxury brand in Europe as well. Just at that point, on the 5th, the Japanese government eased border control measures for entrants from China, such as not requiring proof of a negative test within 72 hours prior to departing the country, which was mandated for all persons entering Japan from Mainland China via direct flights. Inbound tourism consumption is expected to expand and shift into high gear towards Golden Week.

Ueda, the new Bank of Japan governor, held a press conference for his appointment on the 10th. He mentioned that “it is appropriate to continue” the current large-scale monetary easing policy and indicated an understanding that a framework revision to the policy is not being considered for the time being. In response to this, despite the exchange rate moving towards a depreciation of the yen at one point, in the domestic bond market, the newly issued 10-year government bonds shifted to around 0.45%, which was close to the 0.5% said to be the maximum permissible range of fluctuation for the long-term interest rate under the “Yield Curve Control (YCC)” policy, which indicates a sense of caution towards a revision to the monetary easing policy.

The depreciation of the yen following monetary easing pushing up Japanese stocks and the appreciation of the yen bringing about a fall in Japanese stocks is regarded by the market to be partly common sense, and the viewpoint of a revision to the current monetary easing policy bringing about an appreciation of the yen in the exchange rate leading to Japanese stocks being sold off is also partly a “formulation”. However, when it comes to European stocks since last year, the strong Euro from October onwards is becoming a factor for pushing up blue-chip stocks in the Euro area. We can consider the background for it to be a tendency for an easing of import inflation pressure following the strong currency to have a good influence on the economy. From a foreign investor’s perspective, in addition to a rise in stock price, by also aiming for exchange rate profits, perhaps there is a chance of it leading to an influx of large-scale investment funds. Perhaps the relatively strong performance in European stocks is suggesting a possibility that the strong yen exchange rate will encourage global money purchases of Japanese stocks.

Regarding semiconductor-related stocks, even with a deficit last since 3 years 10 months ago at a 15.4% decrease in net sales for March this year compared to the same month the previous year for Taiwan Semiconductor Manufacturing Company (TSMC), the world’s largest manufacturer of semiconductor consignments, there has been strong performance due to the announcement of a decrease in production by the Korean Samsung Electronics, leading to expectations of a recovery in the semiconductor market condition in the latter half of the year. Also, despite machine tool orders for March announced by the Japan Machine Tool Builders’ Association having a 3-month consecutive deficit at a 15.2% decrease compared to the same month the previous year, it had a 13.6% increase compared to the previous month. Movements of a lookout for machine tool-related stocks have begun to emerge as a result of expectations of bottoming out in the state of orders received. Perhaps there may be room to aim for a rebound from overselling.

In the 17/4 issue, we will be covering Komehyo Holdings (2780), User Local (3984), Fujikura Composites (5121), and Orix (8591).

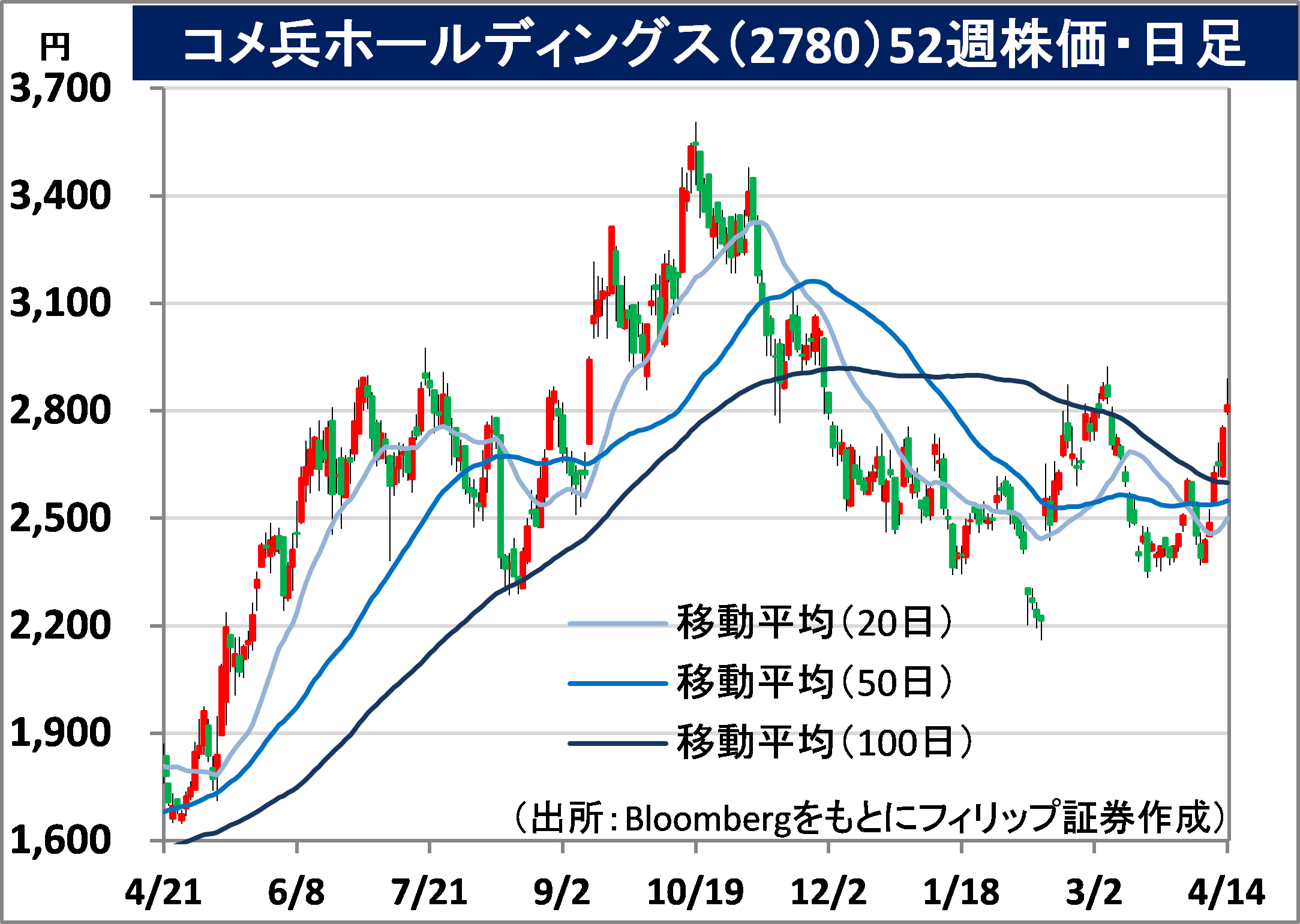

Komehyo Holdings Co., Ltd. (2780) 2,815 yen (14/4 closing price)

・Established in 2014 by means of share transfers from Kanto Natural Gas Development Co., Ltd. (established in 1917) and its subsidiary, Otaki Gas Co., Ltd. Operates a Gas business that handles everything from natural gas development to supply, and an Iodine business that uses brine, a byproduct of natural gas production.

・For FY2022/12 results announced on 13/2, net sales increased by 60.7% to 106.2 billion yen compared to the previous year, and operating income increased by 85.5% to 7.304 billion yen. Results by segment are as follows: Sales in the Gas business increased 64% YoY to 89.9 billion yen, and operating income increased 12% YoY to 5.3 billion yen. Sales in the Iodine business increased 60% YoY to 8.8 billion yen, and operating income increased 2.9x YoY to 4.7 billion yen.

・For FY2023/12 plan, net sales is expected to decrease by 8.6% to 97.1 billion yen compared to the previous year, operating income to decrease by 9.6% to 6.6 billion yen, and annual dividend to increase by 2 yen to 34 yen. On 4/4, PM Kishida announced at the “Ministerial Council on Renewable Energy, Hydrogen and Related Issues” that he plans to promote the use of thin, lightweight, bendable “perovskite solar cell” panels by 2030. Japan produces about 30% of the world’s iodine, the main material for such solar cell panels. Company is one of the world’s leading suppliers.

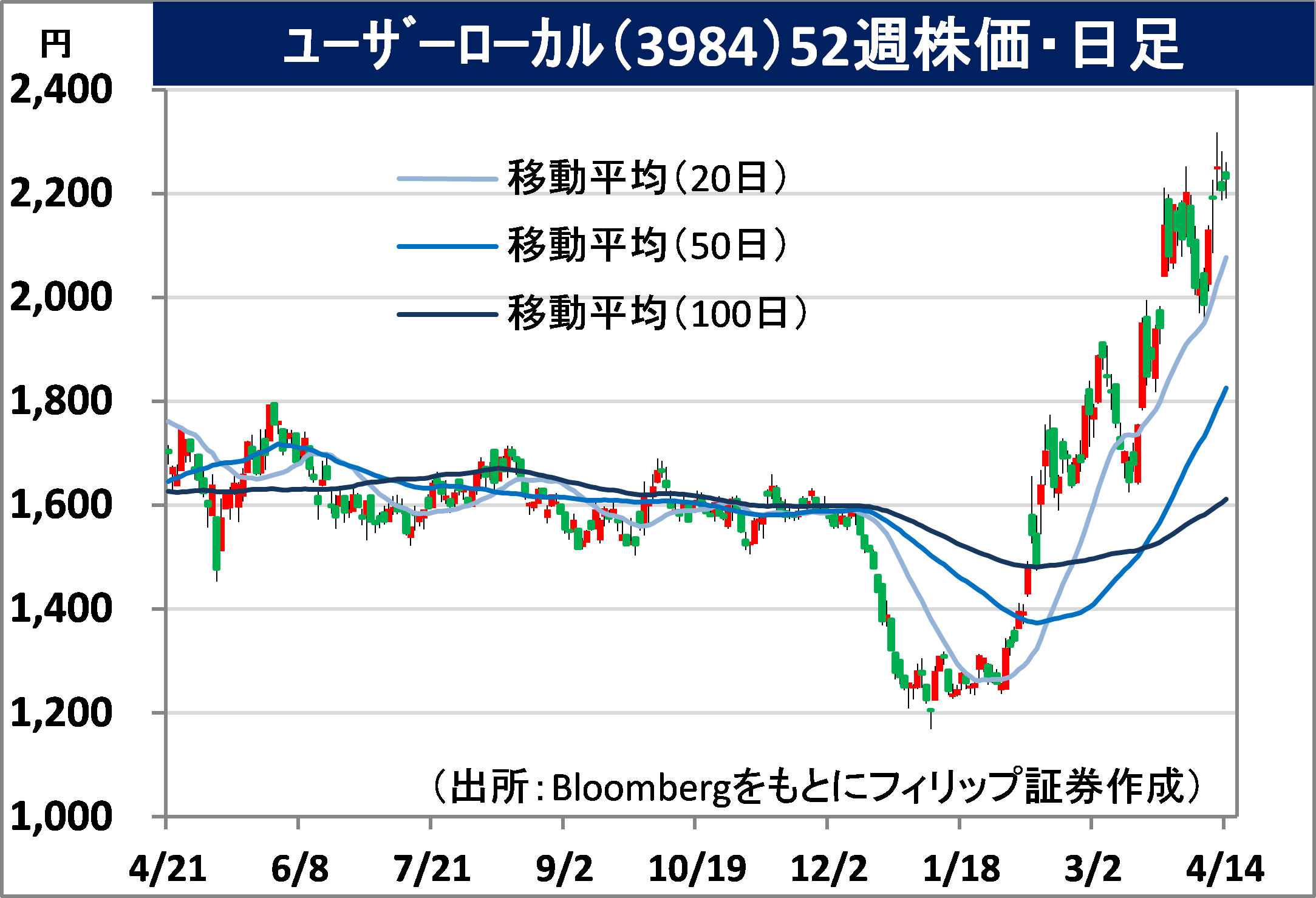

User Local, Inc. (3984) 2,230 yen (14/4 closing price)

・Established in 1907. A conglomerate consisting of the Wireless Comms, Microdevice, Automobile Brakes, Precision Instruments, Chemicals, Textiles, Real Estate, and Other business segments. Aiming to become an “Environment and Energy Company”.

・For FY2022/12 results announced on 10/2, net sales increased by 1.1% to 516.085 billion yen compared to the previous year, and operating income decreased by 29.2% to 15.435 billion yen. Segment profit in the Microdevice business grew 2.1x YoY to 8.947 billion yen due to growth in EV and semiconductor manufacturing equipment applications, but profits declined in the Wireless Comms business and the Automobile Brakes business, impacting results.

・For FY2023/12 plan, net sales is expected to increase by 7.9% to 557.0 billion yen compared to the previous year, operating income to increase by 55.5% to 24.0 billion yen, and annual dividend to increase by 2 yen to 36 yen. Sales and profits in the Mobility segment of the Wireless Comms business had declined in the previous fiscal year due to a decrease in ITS (Intelligent Transport Systems) for automobiles. However, company has advanced technology that simultaneously detects 3D position and speed information by combining camera images and millimeter-wave radar. Ban on “Automated Level 4” driving on public roads was lifted on 1/4.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: