Report type: Weekly Strategy

“Semiconductor manufacturing process and inbound consumption-related issues”

Since October, the Japanese stock market has remained firm since the Nikkei Average closed on 3/10 at 25,778 points, but has been stalled around 28,000 points at the moment. Foreign investor trading trends by investment category released by the Japan Exchange Group showed that for five out of the six weeks since October, foreigners were net buyers, for a cumulative total of 1.0579 trillion yen over that period, indicating that the underlying tone is resilient. One of the reasons for the persistent stalemate is that the market is divided into two groups, viz one group of stocks centering on semiconductor manufacturing and inspection equipment, such as Tokyo Electron (8035), Advantest (6857), and Lasertec (6920), and another group of stocks related to inbound demand, mainly from foreign tourists, following the relaxation of Covid-19 movement restrictions, with trading targets changing on a daily basis.

In the semiconductor industry, fearing a deterioration in market conditions at the time of earnings announcements by US companies, Micron Technology (MU), a semiconductor memory manufacturer, announced production cuts and additional reductions in capital expenditures. On the other hand, Applied Materials (AMT), which manufactures semiconductor production equipment, has made progress in meeting demand as a result of easing of supply chain constraints, and is also benefiting from the fact that its customers, such as Taiwan Semiconductor Manufacturing Company (TSM) and Intel Corp (INTC), are having to build new plants due to semiconductor export controls imposed by the US administration in the wake of the US-China conflict. Also, Berkshire Hathaway, led by Warren Buffett, a prominent investor known for his value stock investments, made a large purchase of approximately $4.1 billion in ADR shares of TSMC from July to September. Among Japanese stocks, in addition to those that have been the focus of much speculation, there is a possibility that trading will intensify in small- and mid-cap stocks such as niche companies of which the technologies are considered indispensable in the semiconductor manufacturing process.

Air and land transportation, travel, leisure, retail and department store sales in relation to year-end parties, shopping and other winter tourist season activities, as well as inbound consumption by foreign tourists, whose purchasing power has increased owing to the weak yen this year, are expected to increase. Against this backdrop, the number of foreign visitors to Japan in October, announced on 16/10, reached 498,600, 2.4 times the number in September. In the absence of Chinese tourists, the numbers were 80% less than those for October, 2019, but further growth is expected. On the other hand, the “8th wave” of new Covid-19 infections is believed to have arrived, and with reports of a new dominant mutant strain, “BQ.1”, replacing current strains, concerns are arising of a possible increase in voluntary movement restraints. Although some inbound consumption-related sectors are expected to perform well, such as department store-related sectors that have strength in external sales of high-end products to wealthy consumers, the market is still likely to be pushed by profit-taking sales until signs of a resurgence in Chinese tourists.

In the 21/11 issue, we will be covering ENEOS Holdings (5020), FUJI (6134), Canon Electronics (7739) and SoftBank Group (9984).

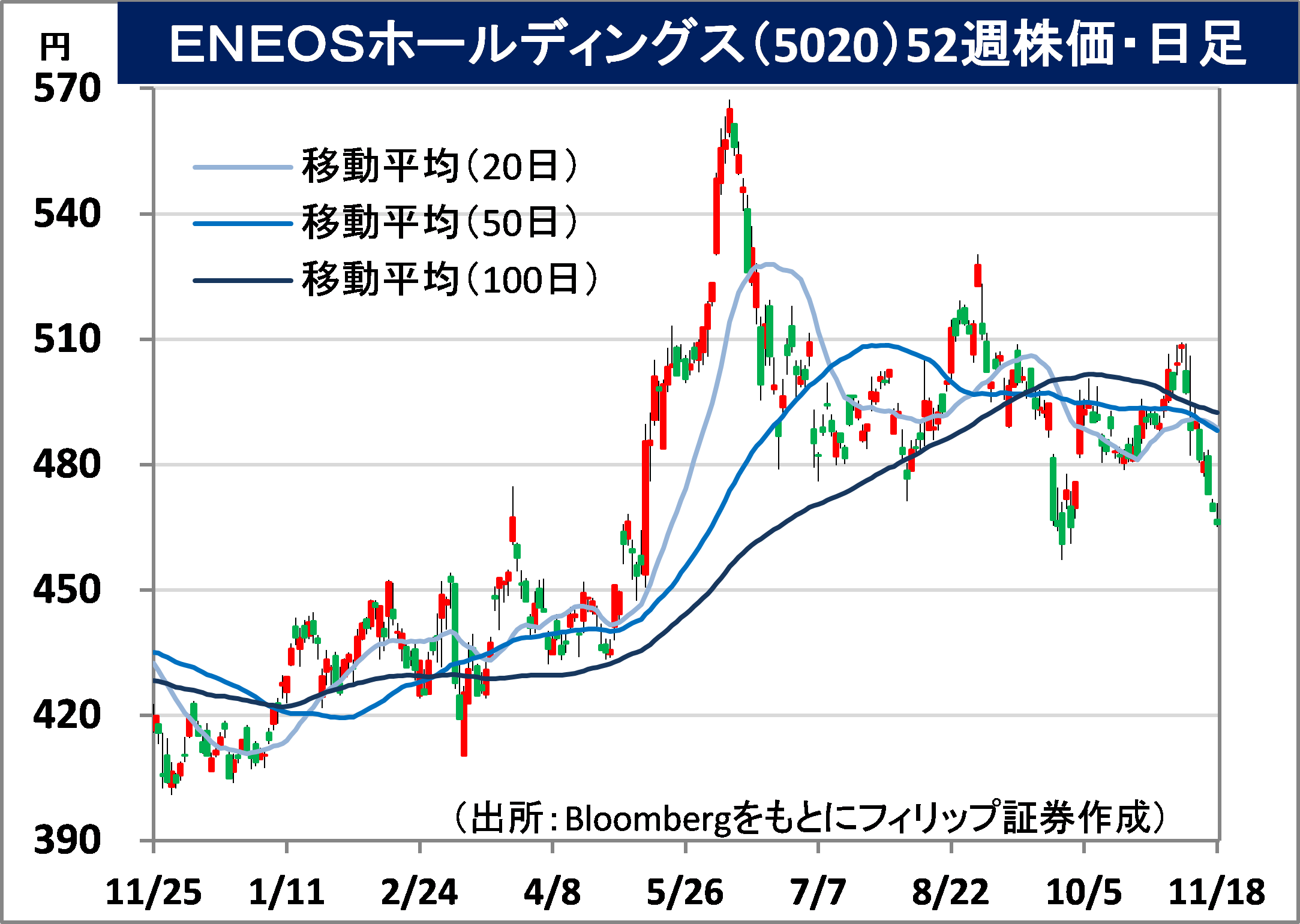

ENEOS Holdings, Inc (5020) 466 yen (18/11 closing price)

・Established as JX Holdings in 2010 through the business integration of Nippon Oil Corp and Nippon Mining Holdings. Merged with TonenGeneral Sekiyu in 2017 and changed its name to the current one in 2020. Leading petroleum wholesaler with 50% domestic market share.

・For 1H (Apr-Sep) results of FY2023/3 announced on 10/11, net sales increased by 56.3% to 7.394 trillion yen compared to the same period the previous year, and operating income increased by 16.8% to 394.7 billion yen. Among the three main business segments, sales in “Energy” increased 65.1% YoY to 6.2606 trillion yen, “Oil/Natural Gas Development” increased by 2.3% to 97.7 billion yen, and “Metals” grew 28.4% to 819.8 billion yen.

・Company has revised its full year plan upwards. Net sales is expected to increase by 36.4% to 14.9 trillion yen (original plan 12.8 trillion yen) compared to the previous year, and operating income to decrease by 28.7% to 560.0 billion yen (original plan 340.0 billion yen). Annual dividend to remain unchanged at 22 yen. JX Nippon Mining & Metals, its subsidiary, holds approximately 60% of the world market share for “sputtering targets”, a material used to make disc-shaped parts made of high-purity metals and ceramics, which are indispensable for semiconductor manufacturing involving the miniaturization of semiconductors.

FUJI Corp (6134) 2,096 yen (18/11 closing price)

・Established Fuji Machine Mfg in 1959. Headquartered in Chiryu City, Aichi Prefecture. Main business segments are “Robot Solutions” for electronic component mounting robots and semiconductor manufacturing equipment, and “Machine Tools” for machine tools for automotive parts.

・For 1H (Apr-Sep) results of FY2023/3 announced on 7/11, net sales increased by 8.4% to 78.67 billion yen compared to the same period the previous year, and operating income decreased by 6.5% to 13.803 billion yen. Sales increased due to capital investment in automotive, industrial equipment, and telecommunication infrastructure, mainly in Europe and the US, as well as higher demand as a result of automotive-related capital investment, mainly in North America, but soaring component prices and supply shortages affected profits.

・Company revised down its full-year forecast for orders to 148.0 billion yen (from 161.0 billion yen), down 9.5% YoY, due to uncertainties in China and other markets, although sales are expected to increase 11.4% YoY to 165.0 billion yen, as previously planned. On the other hand, operating income was revised upward to 30.0 billion yen (original plan 29.2 billion yen), an increase of 5.4% YoY. Annual dividend was maintained at 80 yen per share, up 10 yen from the previous year. With overseas sales accounting for about 90% of the company’s total sales, increased demand for production automation in response to tight labor supply and demand is expected.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: