Report type: Weekly Strategy

A Major SQ Anomaly Once More, Normalisation From Continuous Significant Interest Rate Hikes at the ECB

It was a week of confusion where the chain of U.S. regional bank failures spread to concerns of failure in the Swiss financial giant, Credit Suisse, due to management uncertainties. Although the Nikkei average rose steadily to the high of 28,734 points on the 9th, it plunged to the low of 26,632 points 5 business days later on the 16th.

Recently, it has become common for the market to fluctuate greatly in the short term from around the “Major SQ” for the whole of March, which determines the Special Quotation value (SQ value) involving the final settlement of futures and options. Aside from what will happen with regard to this point, it might have been necessary to take precautions.

In ‘22, ① in March, in response to the Russian invasion in February, after falling to last year’s low at 24,681 points on 9/3, it rebounded and rose to mark the recovery high of 28,338 points 12 business days later on 25/3. ② In June, after marking the recovery high of 28,389 points on 9/6, which was a day before Friday on the weekend of the Major SQ week similar to this time round, it fell to 25,520 points 7 business days later on the 20th. ③ In September, after shifting in a recovery rise to 28,530 points on the 13th, which was a Tuesday a week after the Major SQ week, it marked the low of 25,621 points 12 business days later on 3/10. ④ In December, after marking the recovery high of 28,195 points on the 14th, which was a Wednesday a week after the Major SQ week, it fell to the low of 25,661 points 13 business days later after the new year on 4/1. As seen from this, despite having a different direction from the rise in March and the decline in June, September and December, it can be observed that similar movements are indicated from around the Major SQ. In particular, for March, in addition to the stock market saying of the “equinoctial week bottom”, it seems that there may be a high chance of a similar “anomaly” (a rule of thumb in the market which lacks rationale but often comes true) occurring due to it being around the corner of the March full year business results for enterprises in Japan. For the time being, when there is a stock price drop towards late March, it could be an opportunity to buy towards the new fiscal year.

We have been reminded of the tendency of a downward pressure on stock prices due to an appreciation of the yen and high bonds (decline in the long-term interest rate) in response to a credit crunch in banks worldwide. In the midst of this, on the 16th, the European Central Bank (ECB) strongly set forth to eradicate inflation by hiking policy interest rates by 0.50 points in accordance with the initial forecast. Since the reasons for a bank credit crunch are different for each bank for the whole country, rather than easing money across the board, in terms of an ideal approach, carrying out the supply of liquidity specific to each case could be regarded as an appropriate approach. In Japanese stocks, we can expect a continued lookout for bank stocks that were bought from January to February, other low P/B ratio value stocks and those related to inbound tourism, etc.

For the Japanese bond market as well, the newly issued 10-year government bonds fell to 0.28% at the closing price on the 16th. The handover settlement date for long-term bond futures is on the 20th of each expiration month, and due to the need for sellers to make spot preparations, we ought to note that interest rates tend to decline due to purchasing pressure in the spot bond market.

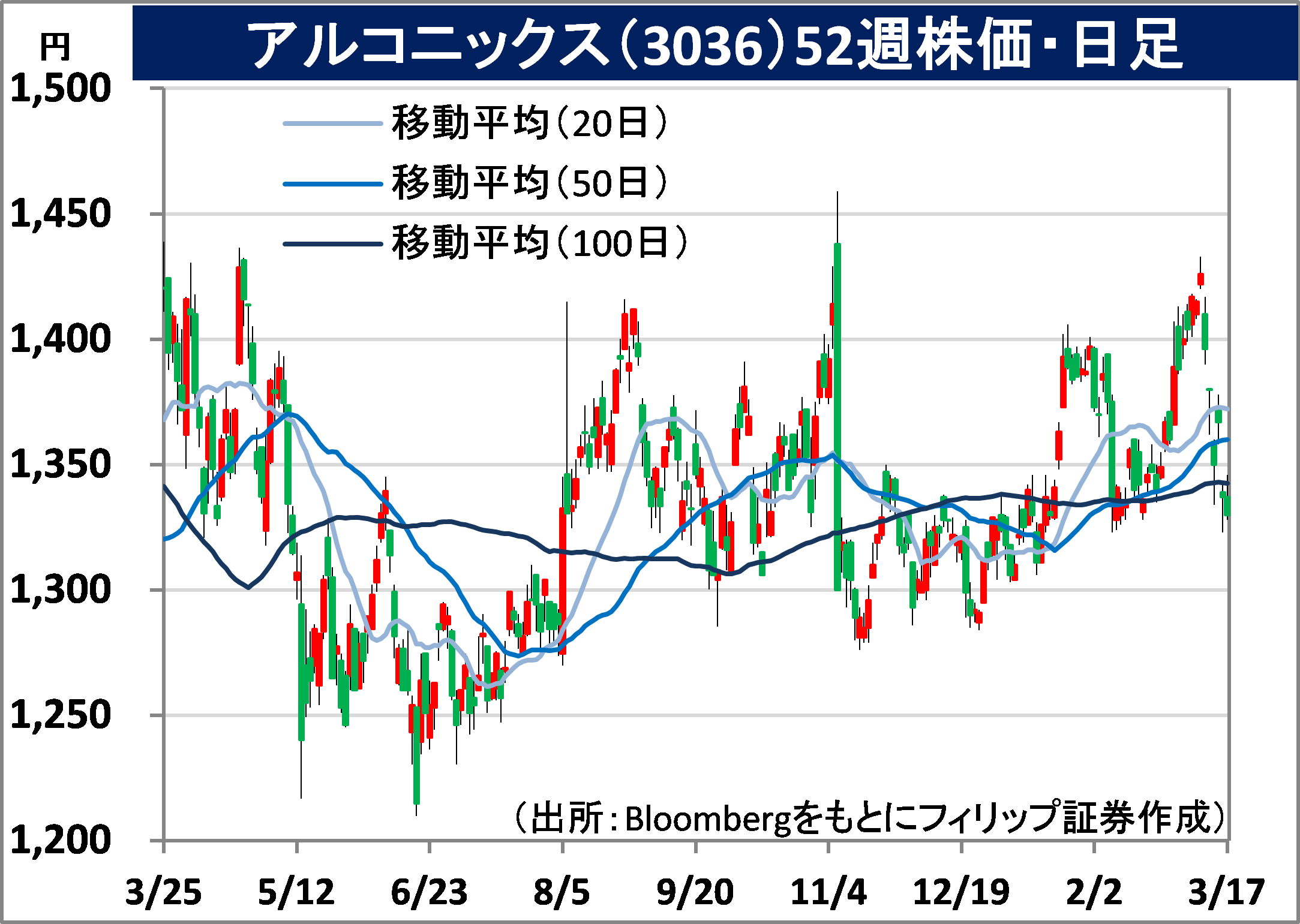

In the 20/3 issue, we will be covering Alconix (3036), Fukuoka Financial Group (8354), Konoike Transport (9025), and Daiei Kankyo (9336).

Alconix Corporation (3036) 1,330 yen (17/3 closing price)

・After establishing as Nissho Iwai Non-Ferrous Metals in 1981, they carried out an MBO in 2001. They are a nonferrous metals general enterprise that fuses trading company distribution (electronic functional materials and Aluminium bronze) and manufacturing (device materials and metal processing). They are characterized by proactive M&A.

・For 9M (Apr-Dec) results of FY2023/3 announced on 8/2, net sales increased by 18.9% to 135.712 billion yen compared to the same period the previous year and operating income decreased by 13.9% to 7.255 billion yen. All 4 key businesses had an increase in revenue, however, trading company distribution’s aluminium bronze and manufacturing’s device materials and metal processing had decreased in profit. An increase in selling, general and administrative expenses following the new acquisition of a consolidated subsidiary and a rise in procurement prices due to the weak yen have affected, leading to a decrease in operating income.

・For its full year plan, net sales is expected to increase by 8.8% to 170 billion yen compared to the previous year and operating income to decrease by 17.4% to 9.1 billion yen. Annual dividend is to remain unchanged at 52 yen. With the company having made 14 companies wholly-owned subsidiaries over 13 years by ’22, it has led to overall profit growth without once recording an impairment loss following acquisition. At the closing price on the 16th, their actual results P/E ratio was approx. 6 times and the P/B ratio was 0.63 times. Nidec (6594), which is similarly known to excel at M&A, had a P/B ratio of 2.4 times. There may be room for a review.

Fukuoka Financial Group, Inc. (8354) 2,576 yen (17/3 closing price)

・Established via an integration between Fukuoka Bank and Kumamoto Family Bank (presently renamed to Kumamoto Bank) in 2007. Integrated businesses with Shinwa Bank in the same year. After integrating businesses with Juhachi Bank in 2019, they started up as Juhachi-Shinwa Bank in Nagasaki Prefecture in 2020.

・For 9M (Apr-Dec) results of FY2023/3 announced on 31/1, core net operating profit increased by 10.4% to 82.712 billion yen compared to the same period the previous year, credit cost increased by 3.3 times to 3.036 billion yen and net income decreased by 26.1% to 32.649 billion yen. While there was an increase in core net operating profit due to the contribution from a decrease in expenses and an increase in net fees and commissions and net interest income, a decrease in gains/losses on bond transactions had affected, leading to a decrease in profit.

・Company revised its full year plan (on a combined basis of 3 bank units) downwards. Although core net operating profit is expected to increase by 6.7% to 104 billion yen compared to the previous year and annual dividend to have a 10 yen dividend increase to 105 yen, which remains unchanged from the original plan, as a result of proceeding with portfolio restructuring mainly in foreign bonds, net income is to decrease by 29.9% to 48.2 billion yen (original plan 73.2 billion yen). For the mobile-exclusive bank, “Minna Bank”, for the end of December compared to the end of September, number of accounts increased by 15%, deposit balance increased by 18% and loan balance increased by 64%.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: