Company Background

Dual-listed on the Singapore Exchange and Philippine Stock Exchange, Del Monte Pacific Limited (DMPL) produces and markets packaged vegetable and fruit, beverage and culinary products (refer to Appendix 1).

In the US, DMFI is ranked first in canned vegetables and second in canned fruits, as consumers continue to turn to trusted brand names for meal preparation and healthy snacks. DMPI’s dominant market shares in the Philippines of as high as 90% in key categories have continued to rise. Retailers are carrying fewer brands and focused on the largest.

Investment Merits

Significant undervaluation of DMPL. DMPL is trading at FY22e P/E of 8.2x, far below the industry average of 16x. The company had been underperforming since the acquisition of US subsidiary DMFI in 2014. Over the years, the new management has turned DMFI around successfully, steering towards innovation to address shifting consumer habits and expanding distribution into key growth areas. We believe another reason for the undervaluation is the debt level of US$1.3bn, resulting in high interest expenses of US$111mn, which we expect to wind down gradually. We apply a 20% discount to the industry average, due to its gearing level which is higher than peers and smaller market capitalization.

REVENUE

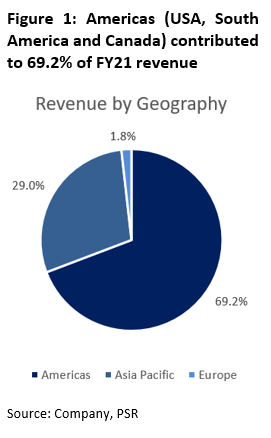

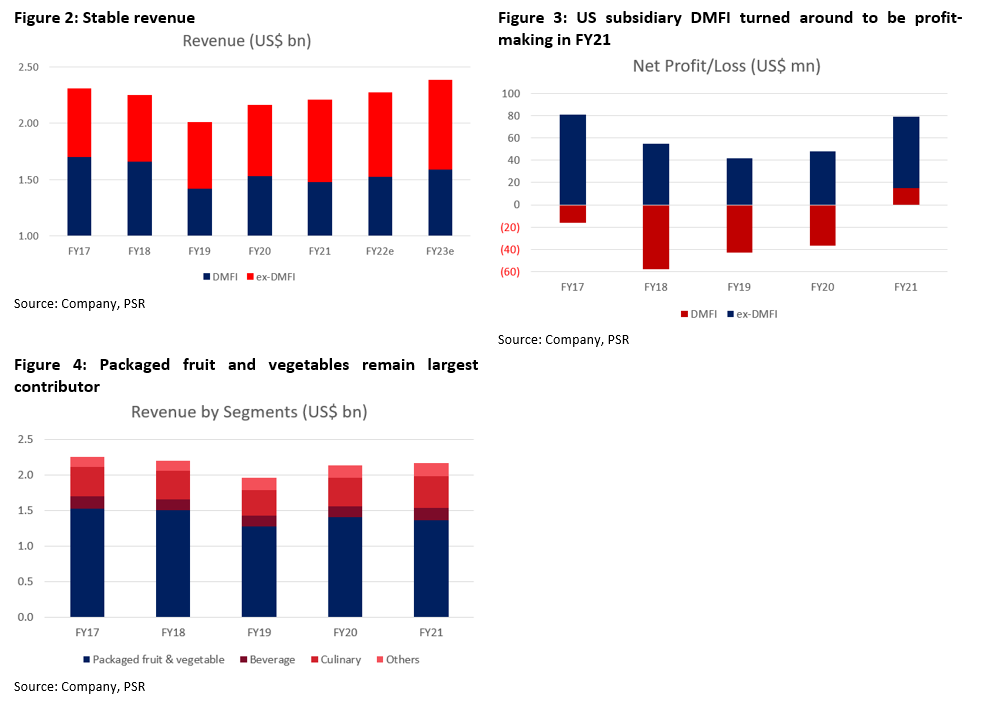

Del Monte Foods Inc (DMFI). DMFI is Del Monte’s US subsidiary, under which they have both branded and private retail sales. This segment was acquired in 2014 and is mainly present in the US. It has been accounting for the bulk of DMPL’s revenue, and made up 70% of FY21 revenue, driven by branded retail sales (Figure 2). The majority of sales under the Americas segment are sold under the Del Monte brand but also include products under the Contadina, S&W, College Inn and other brands. This segment also includes sales of private label food products. Sales are distributed in all channels serving retail markets, and to certain export markets, the food services industry and other food processors.

Del Monte Philippines Inc (DMPI). This is DMPL’s second-largest and most profitable subsidiary. In the Philippines, sales are derived from general trade, modern trade and food services. General trade (GT) includes retailing to a network of retailers, wholesalers, and dealers. Modern Trade (MT) includes the distribution of goods to supermarket chains. Food services include selling through restaurants. The GT and MT combined grew by 13.4% in FY21, delivering record sales of US$705.8mn.

DMPI products are also exported to Europe and S&W markets. This includes exports of fresh and packaged pineapples. Sales increased from higher sales of fresh pineapples in China, Japan and South Korea, and packaged pineapple, mixed fruit and juice drinks.

EXPENSES

Costs primarily include metal packaging, packaging and raw material costs. DMPL has introduced various cost cutting measures over the years.

DMPL has high levels of borrowing, with net debt of US$1.3bn in FY21. This also comes with interest burden of US$111mn. The company has progressively reduced net debt over the past five financial years. It may take another three years before reduction of interest expenses to below US$100mn, as we expect repayment of some short-term borrowings.

In 2017, DMPL completed the offering and listing of 20mn Series A-1 and 10mn Series A-2 preference shares, both at an offer price of US$10 per share in the Philippines, at a fixed rate of 6.625% and 6.5% per annum. We have factored in assumptions that Series A-1 and A-2 preference shares would be redeemed by FY22 and FY23 respectively.

MARGINS

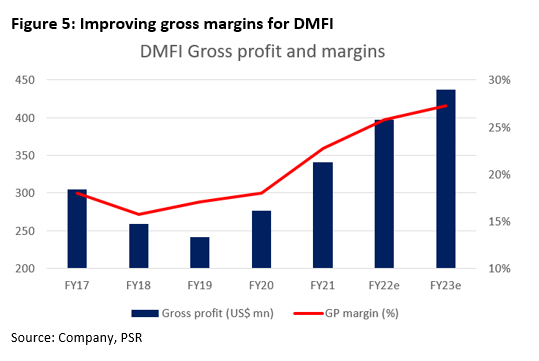

DMFI generated a gross profit margin of 22.6% in FY21, up from 17.6% in FY20. This was driven by higher sales from branded retail, combined with lower promotional trade spend and cost improvement including lower cash discounts. There were also lower packing costs from the asset light strategy, with production outsourced. Plant closures in FY20 generated savings, in line with DMPL’s asset-light strategy.

We expect DMFI gross margins to climb further in FY22e and FY23e. Levers to raise margins to include reducing overhead and trade spending, and capacity expansion in packaging. To alleviate recent cost pressures, DMFI raised product prices in May and September this year. We believe the strength of the brand will keep volumes resilient despite the higher prices.

DMPL generated an average gross profit margin of 21.8% over the past five financial years, and EBITDA margin of 13.3%, which we expect to remain stable.

BALANCE SHEET

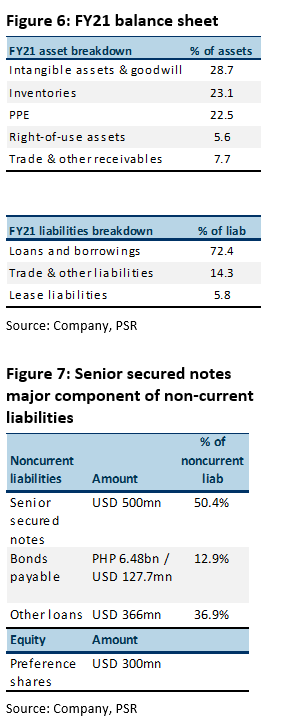

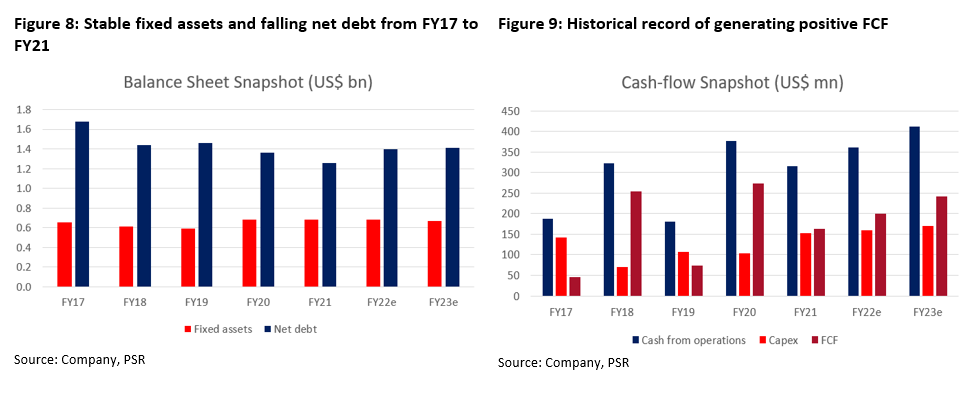

Assets. Fixed assets have remained largely stable over the past five financial years from FY17 to FY21, at US$680mn. DMPL has adopted IFRS 16 since 1 May 2019.

Intangible assets and goodwill is the biggest component of DMPL’s assets, consisting of trademarks, including the right to use the “Del Monte” trademarks in connection with the production, manufacturing, sales and distribution of food products, in various markets (Figure 6).

As of 30 April 2021, DMPL carries goodwill of US$203.4mn and indefinite life trademarks of US$408mn, with US$394mn relating to DMFI.

Liabilities. DMPL has been gradually reducing its net debt, to US$1.3bn in FY21 (Figure 8), and gearing was lowered from 2.4x to 2.0x equity.

DMFI issued US$500mn of 11.875% Senior Secured Notes on 15 May 2020. They will mature on 15 May 2025 and are redeemable at the option of DMFI beginning in May 2022. The Notes make up 50.4% of total non-current liabilities (Figure 7). Interest paid under this loan in FY21 was US$29.7mn, accounting for 27% of total interest expense.

Recently, S&P Global Ratings raised credit rating on DMFI to ‘B’ from ‘B-‘, and issue-level rating on its debt to ‘B’ from ‘B-‘. This is on the back of continued deleveraging, with 11% revenue growth and high profitability in 1QFY22, with EBIT margin of 9.3%. This resulted in improvement in leverage from 10x to about 3.5x for 12 months ending 1 August 2021.

Cash flow. DMPL has been generating positive operating and free cash flows from FY17 to FY21. Operating cash flow was lower in FY21 due to higher working capital. Capex has remained relatively stable at an average of US$115mn over the past five financial years (Figure 9).

DMPL’s dividend policy is to distribute a minimum of 33% of net profit. In FY21, DMPL paid 37% of PATMI in FY21, and 50% of PATMI in FY19. In FY20, although it was a loss-incurring financial year due to plant closures resulting in one-off expenses, DMPL declared a special dividend due to the one-off gain generated from the sale of a 13% stake in DMPI. Preferred dividends were also paid.

INVESTMENT MERITS

KEY RISKS

INDUSTRY

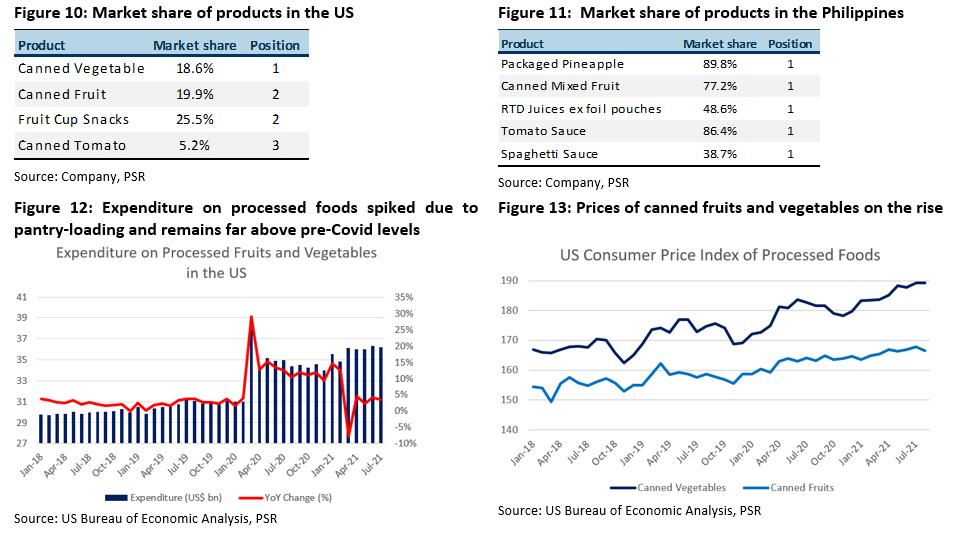

Del Monte Pacific ranks among the top players in the US (Figure 10) and has a dominant share in the Philippines (Figure 11).

Increasing interest in culinary home meal preparation has accelerated due to Covid-19. As a result, more consumers are looking for quick, convenient and healthy food options, and they are turning to strong brands, including Del Monte.

The personal consumption expenditure on processed fruits and vegetables in the US was recording steady growth until the Covid-19 pandemic hit in early 2020, and spiked in March 2020 (Figure 12). Consumers had to prepare their meals at home during the lockdowns, which led to pantry loading and higher demand for meal preparation products. This has also led to steady growth in the prices of processed foods (Figure 13). DMFI has also raised prices over the year.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: