Key Highlights

i. Transaction: Share exchange agreement with Tokyo Century Asia (TCA). Yoma will acquire a 20% stake in Yoma Fleet for US$18.495mn. In exchange, Yoma will issue 137mn new shares (or 5.74% stake) to TCA at an issue price of S$0.135. TCA cannot

dispose the shares without consent of Yoma within 60 months after the completion of

the acquisition.

ii. Financial Impact: Yoma Fleet will become a wholly-owned subsidiary post-transaction. The share exchange will result in a decline in Mar24 NTA per share by 7.4% to US$0.1311. The implied valuation of Yoma Fleet is US$68.37mn.

iii. Tokyo Century Asia: TCA is a subsidiary of Tokyo Century Corporation, one of Japan’s largest leasing companies and listed on the Tokyo Stock Exchange.

iv. History of Yoma Fleet: Yoma Fleet was established in Myanmar on 15 January 2014. TCA acquired a 20% interest in Yoma Fleet for US$26.6mn on 30 April 2019.

v. Background of Yoma Fleet: The company is in the business of vehicles, equipment and other consumer products leasing and rental. It provides four types of services – operating lease, finance lease, daily rental and consumer product financing. Customers include multinationals, local corporations, small medium corporates and individuals.

vi. Rationale of transaction: Yoma views the valuation as attractive, and 100% interest will align the company with its future corporate plans. We expect an area of collaboration will be with Wavemoney. Wave Money is creating a lending platform for unsecured lending and buy now and pay later financing. Wave Money can create a credit score on its users' payroll, spending and location patterns. Lenders, such as Yoma Fleet, that join the platform can provide loans to users with the appropriate credit scores.

vii. Outlook for Yoma Fleet: The company will look to expand its operating fleet, especially through the second-hand market. Heavy equipment imports are still available. Leasing rates can also rise as available credit financing has shrunk due to fewer banks and

microfinance operators.

The Positive

+ 10-fold spike in property development profitability. Property sales jumped 105% to US$94mn in FY24. The profitability of the property division spiked 10-fold to S$22.9mn. Many projects launched enjoyed stellar responses and were fully sold out. The strategy towards a more affordable and differentiated offering has supported City Loft @ StarCity and Estella sales. Unrecognised revenue is US$147.1mn (FY23: US$33.8mn), which will be realized over the next 12-18 months.

The Negative

- Currency devaluation and Yoma Central losses. The decline in Myanmar kyat has impacted FY24 results at multiple levels. There are currency losses from trade payables in US dollar terms and translation losses on US dollar loans. On the flip side, there was a fair value gain on investment properties of US$45mn at Yoma Land Services. The subsidiary reports in kyat and weakness in the currency caused a fair value gain despite stable property value in US dollar terms. Yoma Central registered a net loss of US$23mn in FY24.

Outlook

We do not expect any major recovery in the Myanmar economy. ABD estimates Myanmar's GDP growth to be 1.2% in 2024 (2023: 0.8%).

The following are our expectations in FY25 for the 3 key divisions:

|

- We visited Yoma’s impressive office campus at Pun Hlang Estate in Yangon, which housed major business units such as Yoma Land, Wave Money and Yoma Fleet. The malls we visited had the usual traffic jams in the city centre. We also saw new infrastructure underway that will improve connectivity to their flagship StarCity project. - Preparation for the preliminary works on-site in the iconic Yoma Central project in the heart of Yangon is commencing after its suspension in 2021. The project's residential tower will be relaunched this year. - Operating challenges in the current environment include the long delivery time to import building materials, constant power disruptions, rising inflation, and availability of foreign currency. These challenges also meant opportunities. Demand for real estate for projects such as Yoma Land with quality materials and reliable power supply jumped as households hedged rising inflation and depreciating local currency. Yoma continues to capitalise on the demand for affordable housing. Another trend is the fast adoption of digital finance, supported by the central bank.

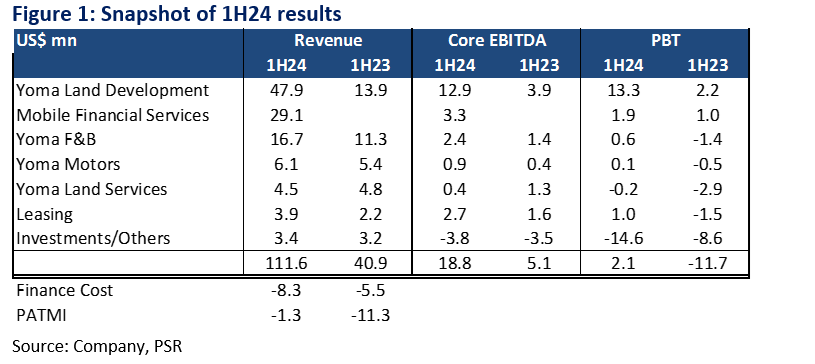

Company Background Listed on the SGX since 2006, Yoma is a leading conglomerate in Myanmar, with businesses spanning real estate, mobile financial services, leasing, F&B, automotive & heavy equipment and investments. In November 2019, Ayala Corporation acquired a 14.9% stake in Yoma at S$0.45 per share, valuing the company at S$1,055mn. In December 2022, Yoma, together with a consortium of investors, completed the acquisition of Telenor's 51% interest in Wave Money, raising Yoma's effective stake in Wave Money to 65%. In terms of EBITDA in 1H24, the key divisions are real estate (67%), wave money (18%) and food and beverage (13%).

VISIT HIGHLIGHTS

Day 1 - 8Jan24: Pun Hlaing (North of Yangon) / Wave Money / City Loft West · Pun Hlaing This is a 650-acre estate with a focus on low to mid-density luxury homes and an 18-hole golf course. We visited the Yoma campus (Figure 3), which houses key divisions such as Wave Money and Yoma Land (Figure 4). The site houses about 800 employees. The homes we visited in the area were semi-detached and luxury bungalows (Figure 5). The new launch was Lotus Hills, with selling prices of around S$800,000+. · Wave Money There are largely two major sources of revenue: 1) OTC: Around 70% of the revenue is from over-the-counter (OTC) money transfers, and the balance is 30% from digital transactions. OTC is currently more lucrative due to the commission structure, which is shared with the merchant. The demand for OTC is due to the low penetration of banking in the country. Only 20-30% of the population has a banking account. Furthermore, 60% of the population live more than one hour from a bank branch. Wave Money is the leader in OTC and relies on its 55,000+ agent network, 60% of which are in rural areas. 2) Digital: The growth in the business is now in the digital business. P2P wallet transfers by customers incur no fees. Revenue is generated from the float in the digital wallet and merchant fees. Other opportunities will come from lending, which will utilize payment data to credit score potential customers. The central bank is introducing a universal QR payment code whereby any of the current 16 payment wallets can be used to settle with the merchant. The differentiator for Wave Money is the customer can access cash with agents, especially in rural areas. KPay and WavePay have a combined market share of more than 90%. During the pandemic, the adoption of digital wallets spiked. However, during the coup, there was a 2-3 month period when the 4G network was shut down, thus negatively impacting the operations in 2021. However, operations have since recovered. · City Loft West Launched in mid-2023, this project has been a success, with 70% of the launched units sold within the first week. Of the two towers launched, 461 of the 494 units have been sold and booked as of 31 December 2023 (Figure 9). A third tower will be launched early this year. Each tower houses around 250 units. Key selling points of the project are the affordability and riverside living along the Hlaing River (Figure 10). The average selling price is MMK380,000 per sft (or S$60k per unit). Financing is available from multiple banks, including Yoma Bank. Units are sold off plans, and 30% is paid to the developer within one month of launch. Construction starts when 60-70% of units within a tower are sold. Yoma projects are known for their quality and imported materials (Figure 11).

Day 2 - 9Jan24: KFC (Junction City Mall) / Yoma Central (Yangon downtown) · KFC Launched in 2015, the initial expansion plan was 50 restaurants in five years to raise market share. Due to the pandemic, the number of outlets is currently down to 36, with around 1000 staff. KFC enjoys several thousand customers per day. The nearest fast-food competitor, Korean Lotteria, has around 40 stores. We tasted fried chicken when visiting the restaurant in Junction City Mall (Figure 13). It was delicious as fresh chicken was used. The price of the chicken is fixed for 12 months to reduce volatility. Localisation of the supply chain is slowly creeping up from 60% pre-pandemic to 70% currently. The imported items are mainly seasoning, packaging, and fries. The meals are priced around MMK8,000 per pax or MMK11,000 for two pax. Most outlets may face 6-8 hours of power cuts per day. Power generators are used to reduce disruption but can cost 10x more in utilities. The flip side of power cuts is households will dine out more as their ability to cook at home is affected. · Yoma Central * The planned iconic development is in central Yangon and comprises one residential block, one business hotel & serviced apartments, a 4-storey mall, and two office towers on a 6.3-acre land (Figure 15 to 17). There are hardly any other new developments in the downtown area. The project was suspended in early 2021. The focus is to relaunch the 112-unit residential towers, of which 20 of the 30 launched units have been sold and booked. The price range is US$1.2mn for a 2-bedroom to a US$5.5mn penthouse. The residential tower was launched in 2019 but was suspended when the coup occurred. Preparation of the preliminary works is commencing.

Day 3 - 10Jan24: StarCity (East of Yangon) · New bridge: To enter the 484-acre StarCity (Figure 18), we had to cross a congested bridge. However, we saw a new parallel 4-lane bridge being constructed (Figure 19), which will critically ease the traffic into StarCity. Other modes of transport included a ferry. Around 135 acres of StarCity are owned by Yoma Strategic. · Large sports facility: StarCity Sports City (SCSC), which was formerly part of Dulwich College, offers many sports and recreational facilities in StarCity. We saw football pitches (Figure 20), tennis courts, basketball courts, and F&B establishments. SCSC now has a membership sports club, which generates incremental recurring revenue. · Renting Galaxy Towers apartments: We visited some of the completed Galaxy Towers (Figure 22), and around 200 units are available for rent at a 4-5% rental yield. Some of the investment units in Galaxy Towers have been sold in 6M-Sept 2023 with a disposal gain. Yoma Land will look to commence construction for the third tower of this development. · Established neighbourhood. From barren land, Yoma created a flourishing township (Figures 23 and 24) with 7,000 residents, 4,000 plus homes, and a golf course.

|

Company Background

Listed on the SGX since 2006, Yoma is a leading conglomerate in Myanmar, with businesses

spanning real estate, mobile financial services, leasing, F&B, automotive & heavy equipment and investments. In November 2019, Ayala Corporation acquired a 14.9% stake in Yoma at S$0.45 per share, valuing the company at S$1,055mn. In December 2022, Yoma together with a consortium of investors completed the acquisition of Telenor's 51% interest in Wave Money, raising Yoma's effective stake in Wave Money to 65%. In terms of EBITDA in 1H24, the key divisions are real estate (67%), wave money (18%) and food and beverage (13%).

1H24 FINANCIAL RESULTS

YOMA LAND

The Positives

+ Held up by real-estate development; better-than-expected F&B and Motors. 3Q21 revenue in line, at 55% of our 2H21e estimate. This was held up by a 46% YoY increase in real-estate development, as construction resumed at StarCity and Pun Hlaing Estate. Conversion rates of bookings to sales at both Star Villas and City Loft @ StarCity were healthy. F&B and Motors performed better than expected, driven by a resumption of food delivery services and sale of automotive vehicles despite limited credit processing and the closure of dealer showrooms in April.

+ 3Q21 core operating EBITDA positive; cost-cutting in place. Core operating EBITDA remained positive in 3Q21, with gross profit covering interest expense. Yoma also paid down US$10mn of gross loans and extended several loans in 3Q21. It continued to cut operating expenses and defer non-essential capex. Staff costs were slashed by more than 60% through job cuts, furloughs and pay reductions. Consolidated cash balance improved QoQ.

The Negatives

- Lower real-estate service revenue. Revenue from real-estate services fell 5% YoY, attributable to lower occupancy at Pun Hlaing Estate as expatriate residents left. This was partially offset by higher leasing by locals, supported by lower rents, better amenities and security provided by the estate.

Outlook

The current third wave of Covid-19 in Myanmar could further disrupt business in the coming quarter. Public holidays were declared for 17 July-15 August 2021 and stay-at-home orders implemented in 86 townships in 10 regions and states. Only healthcare facilities, banks and shops selling essentials, medicines and medical supplies were allowed to remain operational. F&B establishments could only open for takeaways and/or deliveries.

These measures are expected to affect Yoma F&B and Motors. F&B sales are currently 30% below pre-pandemic levels. Most automotive showrooms were forced to close during this period. Revenue from real estate may be resilient as construction is still going on at StarCity, despite a slowdown in sales. Yoma financial services are likely to hold up as Yoma is looking at improving the efficiency of the asset base of Yoma Fleet. Wave Money’s monthly active users grew by double digits MoM in May, after the resumption of mobile 4G network services. However, people’s preference for physical cash in a tight credit environment is likely to affect transaction volumes for the coming quarter.

Yoma is rightsizing its restaurant platform to focus on its two main brands: KFC and YKKO. Previously guided at 30%, it is now looking to close around 25% of the restaurants permanently or temporarily if they can no longer be operated profitably. Yoma closed Little Sheep Hot Pot on 1 July 2021. Auntie Anne’s will cease operations by end-August. We are expecting revenue loss of about 1%. For Motors, Bridgestone tyres ceased operations as of end-July as the brand could no longer operate competitively in Myanmar after price hikes. Yoma Strategic has a 30% interest in the Bridgestone tyre business. We estimate that write-offs from closures will affect trade receivables and investments in associate companies by 10% and 5% respectively in 4Q21.

Maintain NEUTRAL with lower TP of S$0.129, from S$0.147. We roll over our estimates and lower our FY22e book value by 4.6%, after accounting for 10%/5% impact on trade receivables and investments in associate companies respectively due to write-offs from closures. This is partially offset by higher US$/S$ assumptions of 1.36 from 1.34.

Accordingly, our TP drops to S$0.129. This remains pegged at 0.45x P/BV, slightly above its 2007-2010 average P/B of 0.41x during major conflicts, political upheavals and natural disasters. What could turn us more positive are widespread Covid-19 vaccinations and a turnaround in Myanmar’s political situation.

What’s new

Just three months ago in November 2020, Aung San Suu Kyi’s National League for Democracy achieved a landslide victory in elections, bagging 83% of the 1,171 the seats available. On 1 February 2021, the military alleged discrepancies of more than 10mn votes. It has declared a state of emergency to take control of the country for one year and dismissed 24 ministers and deputies, making 11 new appointments in their place. It has also pledged to hold fair elections in a year.

What’s next for Yoma

Recommendation

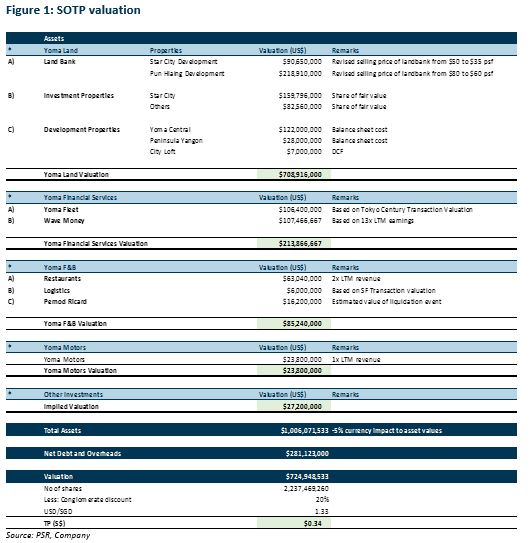

Maintain BUY with a revised SOTP TP of S$0.34, from S$0.46. The change in our TP mainly captures downward adjustments in land bank prices for Yoma Land (Figure 1) to the lower end of the range guided by management in 4Q20. This reflects slower property development and sales in the near term. In addition, we estimate a 5% impact on asset values, assuming a 10% depreciation of MMK/US$ to spot levels of 1,470-1,500 (Figure 2). Our 20% conglomerate discount is unchanged.

Developments to monitor:

The Positive

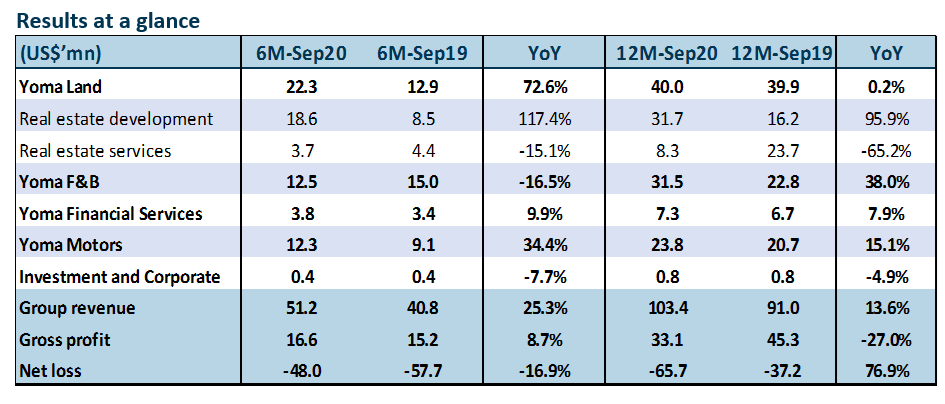

+ 6M-Sep 20 and FY20 topline met; core operating EBITDA remained positive. Despite Covid-19, revenue in 6M-Sep 20 increased 25% YoY. This was aided by real-estate development (+117% YoY) and automotive and heavy equipment (+34% YoY). Partially offsetting the gains was weakness in real-estate services due to competitive leasing and the consumer segment during lockdowns in April, May and September. Full year, the consumer segment held up, led by the consolidation of YKKO and KOSPA for the entire FY20. Real-estate service revenue was down 65% YoY due to lower operator fee income as a result of fair-value losses. 6M-Sep 20 and FY20 core operating EBITDA remained positive at US$2.9mn and US$2.6mn respectively.

The Negatives

- FX, impairment and associate losses. The bulk of 6M-Sep 20 losses came from subsidiaries’ conversion of US$ valuation into MMK (-US$34mn). An impairment loss on prepayments and operating rights for Yoma’s agricultural investments was also booked (-US$6mn). Netting off fair-value gains/losses and interest income, “other income” loss was US$16mn. Additionally, Yoma booked its share of losses from Memories Group, whose tourism operations were affected by Covid-19 and translation losses on borrowings (-US$7mn). All in all, net loss was US$48mn for the half year.

- FY20 double whammy from lower gross profit margins and net fair value losses. FY20 gross profit margins plunged from FY19’s 50% to 32%. This was blamed on lower real-estate service revenue. The segment contributes one of the highest gross profit margins to Yoma. Other culprits were lower-margin products at Star City and lower consumer margins following higher packaging and delivery costs. Coupled with net fair value losses of US$12mn vs net other gains of US$9mn in FY19, FY20 net loss increased 77% YoY.

Outlook

Myanmar is reeling from a second wave of the pandemic. Movements are now restricted within townships, with stay-home orders and prohibitions on restaurant dine-in. As the number of new cases slightly dwindles from its highs, the authorities are easing some of the measures. We are cautiously optimistic on a recovery in 2021

F&B and Yoma Motors are expected to be weak in the near term. That said, FY21 group topline should be supported by significant unrecognised revenue at Yoma Land and Yoma Motors. As of 9M-Sep 20, Yoma Motors had sold an estimated 200+ Mitsubishi units that are pending recognition (c.US$10mn). Over at Yoma Land, three out of its six City Loft buildings are 25-65% completed. Unrecognised revenue here amounts to c.US$12mn. Following its recent launch, Star Villas Phase 1 - Yoma’s first landed development in Star City - has sold 27 out of 32 units, accumulating c.US$15mn for recognition. Star Villas is expected to be completed in the next 12-15 months. Phase 2 will be launched in the coming months following the success of Phase 1. These projects are expected to support FY21’s topline.

We are looking at a turnaround in FY22, when Yoma Central and Star Hub will be completed. Yoma Central is in advanced leasing negotiations with anchor tenants for its office and retail space. Upon completion in mid-FY22, it is expected to generate US$90-110mn of recurring revenue - equivalent to FY20 revenue. Additionally, Yoma recently launched Star Hub, its first suburban commercial property at StarCity. Target date of completion is end-2021. Prominent technology and financial-service companies have already committed to more than 50% of its office space. Rental yields here are estimated in the mid-teens, to be generated from FY22.

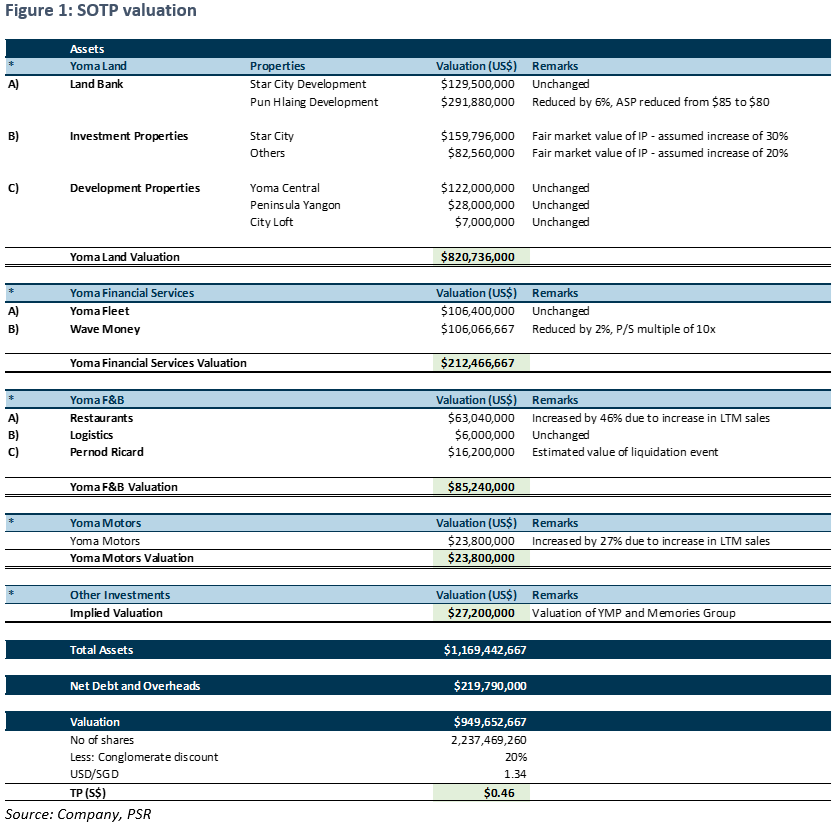

Maintain BUY and SOTP TP of S$0.460. We updated our segmental assumptions following Yoma’s latest valuation guidance. Our valuation metrics and TP remain largely unchanged, including our 20% holding-company discount. Yoma Land constitutes 86% of its total valuation after net debt and overheads.

The report is produced by Phillip Securities Research under the ‘Research Talent Development Grant Scheme’ (administered by SGX).

The Positives

+ Yoma Land’s revenue is well supported by backlog of unrecognized revenue. Although sales were minimal this quarter (8 units of CityLoft and 1 unit of Peninsula Residence) amidst cautiousness in big-ticket expenditure and delays in paperwork, Real Estate Development registered a 45.5% YoY revenue increase. It is largely attributable to the revenue recognized from the completion of City Loft. Unrecognised revenue now amounted to US$17mn as at 3Q20 vis-à-vis more than US$20mn in 2Q20. Real Estate Services revenue was lower YoY due to lower occupancy levels and rental rates at Pun Hlaing Estate and StarCity. However, the lower rental rates and the amenities and services offered amidst COVID-19 had driven a partial recovery in occupancy levels in recent months.

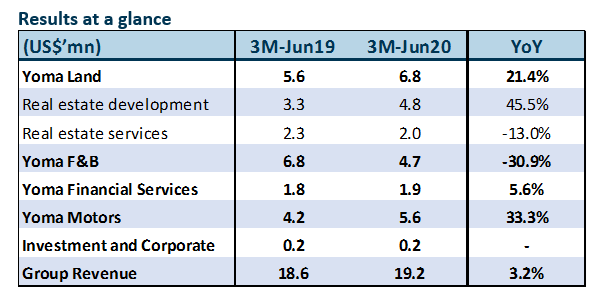

+ Yoma Motors registered revenue growth of 33.3% largely attributable to the Heavy Equipment segment; Passenger and Commercial Vehicles (PCV) segment held up. Despite the COVID-19 impact from border closures and falling crop prices, more tractors and implements were sold due to pent up demand after many quarters of weaknesses arising from the exceptionally heavy monsoon last year. New Holland sold 124 tractors in the quarter compared to 61 tractors in 3M-Jun2019. Higher PCV revenue was driven by the sale of 16 Volkswagen vehicles and 22 Ducati motorbikes. Mitsubishi and Hino also saw significant improvements with 184 Mitsubishi vehicles (65 vehicles in 3M-Jun19) and 26 Hino trucks (9 trucks in 3M-Jun19) being sold. Mitsubishi sales were boosted by the popular Xpander model and there remains c.US$7.5mn backlog of unfilled orders.

+ Revenue from Yoma Financial Services increased by 5.6% YoY underpinned by an enlarged finance lease portfolio in Yoma Fleet; Wave Money remains EBITDA positive despite weaker transaction numbers. Vehicle numbers for Yoma Fleet grew by 11.1% year-on-year to 1,290 vehicles and third-party assets under management stood at US$45.6 million as of 30 June 2020. As finance leases carry higher gross profit margins, we are expecting a larger flow-through from Yoma Fleet to the bottom line in 2H20.

Due to the Thingyan holidays amidst the Myanmar New Year in April and COVID-19 measures, Wave Money’s OTC business was largely affected, which resulted in a decline in revenue and transaction numbers of 16.5% and 25.3% respectively from the previous quarter. However, its e-wallet business continued to record double digit growth rate month-on-month as more people opt for cashless transactions and is on track to reach its 1.3 million MAUs target by December 2020. EBITDA for Wave Money remained positive due to economies of scale and cost control.

The Negatives

- Yoma F&B revenue was down 31% YoY due to COVID-19 measures. 3Q20 revenue declined 31% YoY due to government-imposed lock downs, curfews and prohibitions on dine-in between April to mid-May and temporary store closures in severely affected trade zones. The month of April was most affected as revenue fell 50% YoY. During the initial stages of COVID-19 there was a large shift towards delivery, which mitigated some of the shortfall in dine-in revenue. Delivery accounted for 40% of the total sales in April at the peak, which normalised to 15%-20% as restrictions eased and some of these customers return to restaurants. June recorded a smaller decline of c.25% YoY since the Myanmar government allowed restaurants to resume operations conditional upon adherence to certain guidelines at the end of May.

Outlook

Pre-COVID, CityLoft has been recording a healthy booking rate at >50 units per month. Amidst COVID-19, interest in the property remained high as the team continued to engage customers through virtual show flats. However, CityLoft’s booking rate slowed significantly from April to May. As the economy started to reopen at the end of May, buying interest noted a recovery. Booking rate was nearing half of pre-COVID levels by July.

According to World Bank’s June report, the agriculture sector had been resilient and is expected to grow by 0.7% for the year. This is mostly due to an increase in production of crops, such as rice, and beans and pulses. Meanwhile, the Myanmar government and NGOs are also supporting the agricultural industry by providing lower-interest loans for buying inputs and giving greater flexibility on loan repayments. These initiatives will spur demand for tractors which is beneficial for Yoma Motors.

During this period, Wave Money will continue to work with various organisations such as Myanmar Agricultural development to disburse loans for farmers and Social Security Board to disburse medical and COVID-19 quarantine relief through the adoption of Wave Pay. We are expecting the growth of the e-wallet business to be fast-tracked by these schemes to make up for fewer transactions in the OTC business.

Yoma F&B witnessed improved performance MoM as business starts to recover in the coming quarter. Sales for July was nearing-pre-COVID level with same store sales growth recorded in certain days. The accelerated adoption of delivery services positioned Yoma F&B better to capture sales thwarted due to dine-in prohibitions. Yoma’s target of opening 2-3 KFCs by the end of 2020 remains unchanged.

Maintain BUY with an unchanged TP of S$0.460. Our target price translates to a total upside of 58.6%. Property and financial services will constitute 68% and 19% of the valuation respectively. A conglomerate discount of 20% has been applied (Fig.1).

The report is produced by Phillip Securities Research under the ‘Research Talent Development Grant Scheme’ (administered by SGX).