Venture Corporation Ltd – Here comes the AI bump

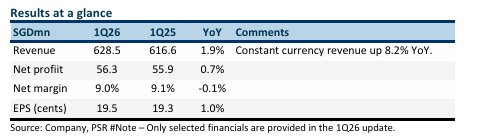

- 1Q26 revenue/net profit were within expectations at 24%/22% of our FY26e forecast. 1Q is seasonally weaker. Revenue faced a 6.3 percentage-point drag from the weaker US dollar. AI-related infrastructure products drove 11% YoY revenue growth. However, consumer lifestyle and related categories declined by 12% YoY .

- Venture’s guidance emphasised new shoots appearing in 2026. We believe it is benefiting from the massive global build-out of data centres. Key products include network interface cards in servers and semiconductor equipment components. Revenue returned to growth after 12 consecutive quarters of decline.

- We upgrade our recommendation to BUY from ACCUMULATE. Our FY26e PATMI is unchanged. We raised our target price to S$22.10 (prev. S$16.80), or 25x FY26e PE, as we move away from historical valuations toward US-listed peers trading at 33x forward PE. Earnings growth for FY26e/FY27e will be led by AI products to support the massive deployment of data centres globally. 4Q26e will be driven by the launch of new consumer lifestyle products. Net cash on the balance as at 1Q26 was disclosed as in excess of S$1bn.

The Positive

+ Revenue returns to growth. 1Q26 revenue rebounded with a 1.9% YoY growth (or 8.2% constant

currency). It is a turnaround from 12 consecutive quarters of YoY decline. Driving growth was the

11.2% improvement in AI-related infrastructure products. It included products in test and

measurement, networking cards, sensors, controllers and semiconductor equipment.

The Negative

- Weak consumer lifestyle. The portfolio of products that include consumer lifestyle declined

12.4% YoY to S$212mn. Improvements to the product increased its lifespan and lengthened its

lifecycle.

Venture Corporation Ltd – Bottom in sight

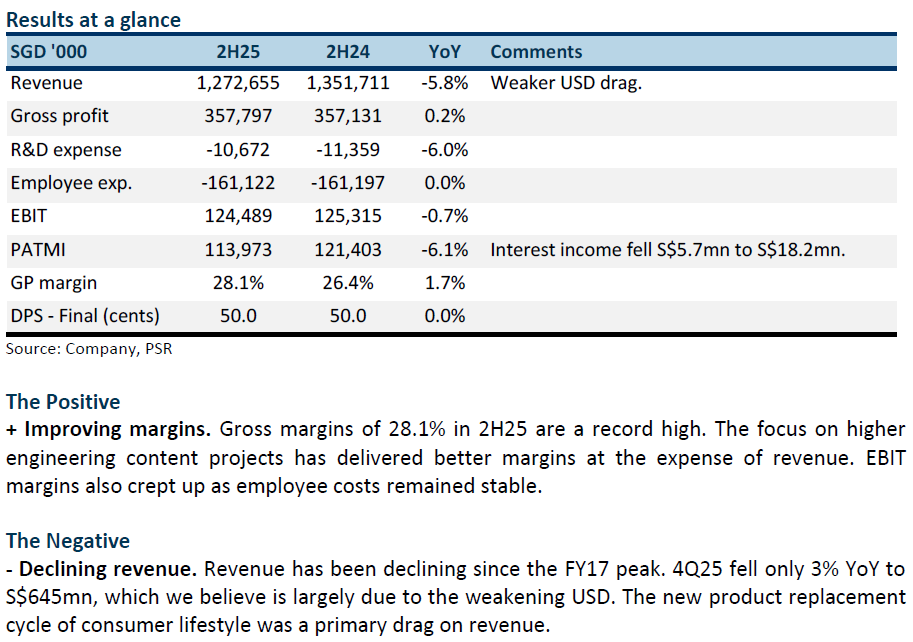

- FY25 results were within expectations. Revenue/PATMI were 101%/99% of our FY25e forecast. 2H25 PAMI declined 6% YoY to S$114mn, dragged down by a similar 6% fall in revenue. The pace of contraction in 4Q25 revenue was slower at 3% YoY. FY25 dividend of 80 cents was 5 cents higher due to the interim special announced earlier.

- Venture’s guidance reflected a more positive trajectory. There were more identifiable product initiatives to accelerate the growth momentum into 2026. The areas of growth were consumer lifestyle, semiconductors and network equipment in data centres.

- We upgrade the recommendation to ACCUMULATE from NEUTRAL. We inch up our FY26e PATMI by 3% to S$256mn. The target price is raised to S$16.80 (prev. S$13.00). Our target PE ratio is increased to 19x from 15x, toward the higher quartile of the 5-year average. We expect earnings to recover in FY26. The major driver will be the new generation consumer lifestyle product launch in 2H26. down by 1% on account of lower interest rates and foreign exchange. Global rollout of data centres will benefit its networking, communications, instrumentation and semiconductor divisions. The dividend yield of 5.1% (or S$230mn payout) is backed by free cash flows of S$200-300mn p.a. and net cash balance sheet of S$1.28bn.

Venture Corporation Ltd – More time needed to recover

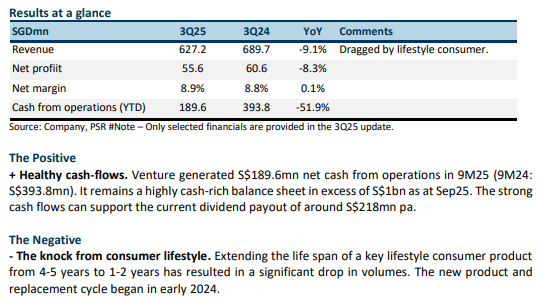

- 3Q25 results were within expectations. Both 9M25 revenue and PAT were 76% of our FY25e forecast. Net profit in 3Q25 fell 8.3% YoY to S$55mn. The shorter replacement cycle of the key lifestyle consumer product was a significant drag on revenue.

- Venture’s guidance points to new product wins in network connectivity products for hyperscaler data centres and new product launches in lifestyle consumer. Both categories will only contribute meaningfully likely in 2H26. Tariffs have also made Singapore a more attractive manufacturing destination for the US market.

- We nudge our FY25e PATMI down by 1% on account of lower interest rates and foreign exchange. Our NEUTRAL recommendation is maintained. The target price is raised to S$13.00 (prev. S$11.80) as we roll over our valuations to FY26e as the recovery year. The PE ratio is also increased to 15x, in line with its 5-year average. The dividend yield of 5.5% and the strong net cash balance sheet of S$1.2bn have been the attraction. Operationally, we expect challenging conditions until 2H26 when new products materially ramp up. The stock is trading at a steep valuation of 18x PE FY25e.

Venture Corporation Ltd – Coping under challenging conditions

- 1H25 results were within expectations. Revenue and PATMI were 51%/49% of FY25e expectations. 1H25 PATMI net profit declined 8.6% YoY to S$112.9mn, in-line with revenue contracting 8.8%. A special dividend of 5 cents was announced in addition to an unchanged interim dividend of 25 cents.

- Venture’s outlook commentary shared little on near-term operating conditions. The company emphasised its long-term relationship, investments, and strong balance sheet. Nevertheless, we believe 2H25 earnings will remain weak – (i) the replacement cycle of its key consumer lifestyle product has been extended due to product design changes; (ii) uncertainty over drug pricing has scaled back big pharma capex; and (iii) cuts in US research funding grants further pulling down demand for life science equipment.

- We maintain our FY25e revenue and PATMI but believe there is downside risk to our forecasts. Our NEUTRAL recommendation is maintained, but we raise our TP to S$11.30 (prev. S$10.40) or 14x PE FY25e, a slight premium to the 2-year average of 13x. The attractive yield of 6% backed by huge S$1.26bn net cash warrants our improvement in valuations.

Venture Corporation Ltd – 2025 looks tough

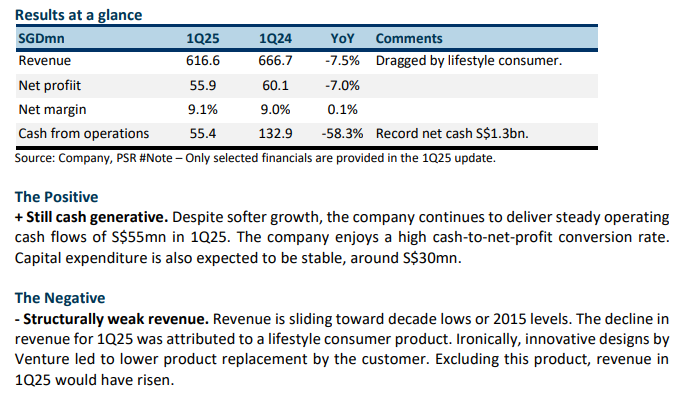

- 1Q25 results were below expectations, with revenue and PATMI at 23% of our FY25e forecast. Net profit in 1Q25 declined 7.0% YoY to S$55mn. Quarterly revenue is the lowest in a decade or since 1Q15. Lower contribution from a key lifestyle consumer product impacted revenue.

- Venture’s guidance remains cautious for the rest of the year. The company mentioned that there is significant uncertainty in the global economic environment due to tariffs, and there is no clear visibility in the tariff landscape over the next 12 months.

- We lower both our FY25e revenue and PATMI by 5%. Our NEUTRAL recommendation is maintained, but we have lowered our TP to S$10.40 (prev. S$11.80) and 13x PE FY25e, in line with the 2-year average. We expect another year of sluggish growth in FY25e. Nevertheless, Venture pays an attractive yield of 6.7% backed by net cash of S$1.3bn with aggressive share buyback plans.

Venture Corporation Ltd – Policy headwinds

- FY24 results were below expectations. Revenue and PATMI were 96% of expectations. 4Q24 net profit declined 9.2% YoY to S$61.2mn as revenue contracted 10.1% YoY. Earnings are at 8-year lows. DPS of 75 cents was maintained at a record payout ratio of 89% (FY23: 81%).

- Venture’s guidance is “short-term business environment is deemed uncertain”. We believe the new US administration policies have resulted in (i) Customers turning more cautious in their orders due to tariff uncertainty and (ii) Proposed cuts in the US National Institute of Health budget will curtail spending on life science equipment from research institutes and labs.

- We lower our FY25e revenue and PATMI by 12% and 10%, respectively. Our NEUTRAL recommendation is maintained, but we have lowered our TP to S$11.80 (prev. S$13.00) to 14x PE FY25e, a slight premium to the 2-year average of 13x. The company is targeting growth in FY25. However, similar to last year’s guidance, it may be revised downwards due to the current uncertain environment. The dividend yield of 5.8%, net cash of S$1.3bn, and 8.3mn share buyback plan is supportive of the share price.

Venture Corporation Ltd – Paid for gazing at the horizon

- 9M24 results were below expectations. Both revenue and PATMI were 69%/68%, respectively, of our FY24e forecasts. 3Q24 net profit declined 3.8% YoY to S$60.6mn as revenue declined 2% YoY. Earnings are expected to contract to 7-year lows in FY24e.

- Venture has lowered its 2H24 revenue guidance from stronger to relatively stable compared to 1H24. The company said that good opportunities from life science and AI data centres are on the horizon. However, we are not clear how far this horizon is.

- We lower our FY24e revenue and PATMI by 5% and 6%, respectively. Our NEUTRAL recommendation is unchanged. We have maintained our S$13.00 as we roll over to an FY25e PE ratio of 14x, a slight premium to the 2-year average of 13x. We believe earnings have stabilised, but growth is dependent on a pick-up in customer orders from consumer lifestyle, life science, and AI data centres. We find the dividend yield of 5.9% attractive, supported by a net cash hoard of S$1.19bn.

Venture Corporation Ltd – Some stability creeping up

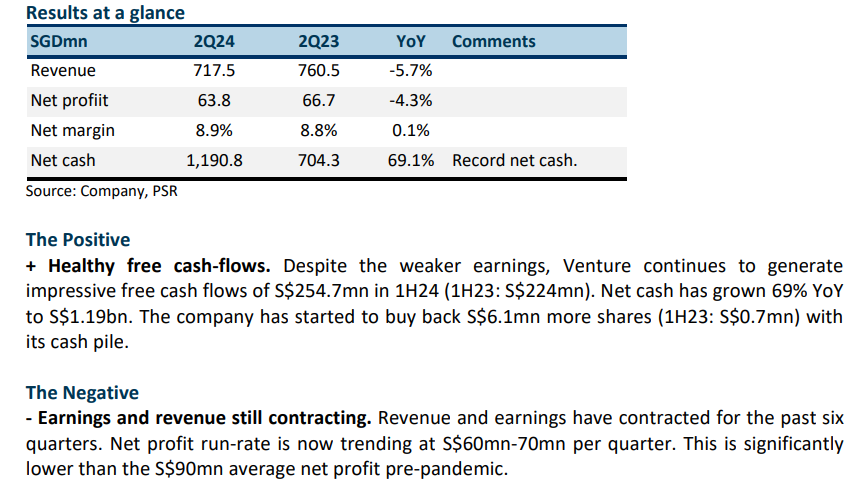

- 1H24 results were below expectations. Both revenue and PATMI were 44%/43% respectively of our FY24e forecasts. 2Q24 net profit declined 4.3% YoY to S$63.8mn, with revenue contracting 6% to S$717mn. The pace of revenue contraction is the slowest after six quarters.

- Venture is guiding revenue to be stronger in 2H24 compared to 1H24. We believe some of the growth domains the company is pursuing include optical transceivers for data centres and consumer lifestyle products.

- We lower our FY24e revenue and PATMI by 4% and 5% respectively. We maintain our NEUTRAL recommendation. We are nudging up our target price from S$12.75 to S$13.00 as we push up valuation to 14x from the 2-year historical PE ratio of 13x. There are some positive takeaways. The pace of revenue decline is slowing, fixed cost (staff and depreciation) is stabilising and several growth products were highlighted. If these new programmes were to ramp-up, we expect significant operational leverage. The dividend yield of 5.8% is attractive and well backed by record net cash of S$1.19bn.

Venture Corporation Limited – Worst performance since 2016

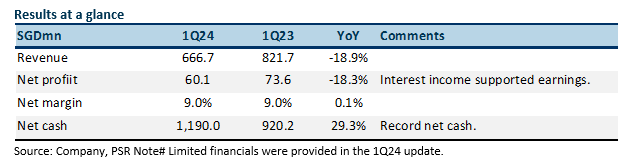

- 1Q24 results were within expectations. Both revenue and PATMI were 21% of our FY24e forecast. Net profit declined 18% YoY to S$60.1mn. We believe earnings were supported by strong interest income.

- Revenue in 1Q24 declined around 19% YoY to S$666.7mn, the weakest in eight years or 2016. The weakness was attributed to destocking in the life science, network, and communications segments.

- We maintain our FY24e earnings. We expect seasonality in demand to raise earnings sequentially in the coming quarters. Our NEUTRAL recommendation and target price of S$12.75, based on a 2-year historical PE ratio of 13x, is unchanged. The dividend yield of 5.6% is well supported by record net cash of S$1.19bn. Share buybacks is another avenue the company will pursue to return capital to shareholders.

The Positive

+ Cash piling up. Venture piles up net cash to record S$1.19bn (1Q23: S$920mn). Management said the cash improvement is due to working capital optimisation. We think it is also due to the lower sales performance. We believe the high cash levels is now the biggest growth driver with increased interest income.

The Negative

- Revenue plunging to 8-year lows. Revenue has dialled back down to 2016 levels. 1Q24 revenue of S$666.7mn is modestly above 1Q16 S$630.7mn. The near-term weakness was attributed to de-stocking in life science, network and communications segments.

Venture Corporation Ltd – Recovery back-loaded

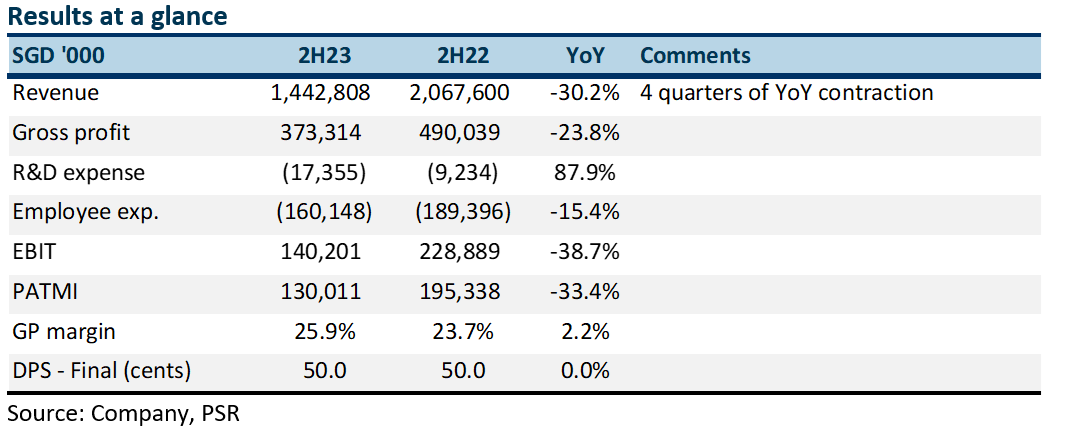

- 2023 results were within expectations. Both revenue and PATMI were 99% of our FY23 forecast. Earnings weakness persisted into the 4Q23, with PAT declining 25% YoY to S$67.4mn. The final dividend was unchanged at 50 cents and full-year at 75 cents.

- The outlook provided by the company, we believe, is for revenue softness to persist into 1H24 before recovery in the later part of the year. We believe driving growth will be new products by customers in semiconductor equipment, data centres connections, and medical and luxury consumer products.

- We nudge our FY24e earnings to be 2% higher and maintain our NEUTRAL recommendation. Our target price is raised modestly to S$12.75 (prev. S$12.50), based on a 2 year historical PE ratio of 13x. The dividend yield of 5.5% is reasonable, and the balance sheet is healthy, with record cash holdings of S$1bn. Visibility to earnings growth is poor and depends on customer confidence to launch new products.

The Positive

+ Record net cash. Free cash flow generated was a record S$478mn (FY23: S$236mn). The large jump in operating cash was from the decline in inventories of S$220mn. Net cash on the balance sheet surged to record S$1.05bn. Inventory is beginning to normalise to S$822mn but remains higher than pre-pandemic levels of S$706mn, despite the lower revenue. Interest income has almost tripled to S$28mn, accounting for 8% of earnings.

The Negative

- Sluggish revenue and earnings. The net profit for Venture is at a seven-year low. An inability to capture higher growth products plus delays in new product introductions and laclustre ramp-up in volumes have been major reasons for the multi-year decline in earnings.

Outlook

The company's outlook is for 2H24 to be stronger than 1H24. This is not new and has been the typical seasonality for Venture. We believe it implies softer revenues in the near term and a possible ramp-up later in the year. Visibility is poor as it depends on customer confidence and the ability to launch new products. Growth segments for Venture will include semiconductor equipment, data centres connections, and medical and luxury consumer products.

Maintain NEUTRAL with a higher TP of S$12.75 (prev. S$12.50)

Our FY24e earnings are raised a marginal by 2% to S$287mn.

Get access to all the latest market news, reports, technical analysis

by signing up for a free account today!

Login

The full article is only available for premium content subscribers. To continue reading this article, please log in:

Not a Premium Content Subscriber yet? Sign up here!

- Home >

- Phillip Research Report