The Positives

+ Plans to monetize vessels. Valuations for 2nd hand vessels remain stable. Uni-Asia sold a 49% joint venture vessel in March 2023. We estimate the gain on sale is US$3-4mn. Vessel owners are hesitant to order new vessels. There is uncertainty over the fuel type that meets future emission standards. Larger bulk carrier orders are gravitating towards methanol as the dual fuel with fossil fuel. However, Handysize vessels are too small to accommodate both fuel types.

+ Alero pipeline refreshed. Uni-Asia’s pipeline of residential projects in Tokyo (called Alero) in 1Q23 is improving to 13 ongoing or new sites. This compares with 9 ongoing sites a year ago. The number of projects sold has declined from 4 to 2.

The Negative

- Weakening freight rates. The Baltic Exchange Handysize Index is down 27% this year. Despite the re-opening in China, the rebound has been slower than expected. In 1Q23, industry data pointed to increased volumes for iron ore post emission controls in China during the Beijing Winter Olympics last year. Coal volumes also performed better after the Indonesia export ban in 2022. Minor bulk and grain loading have been weak.

The Positives

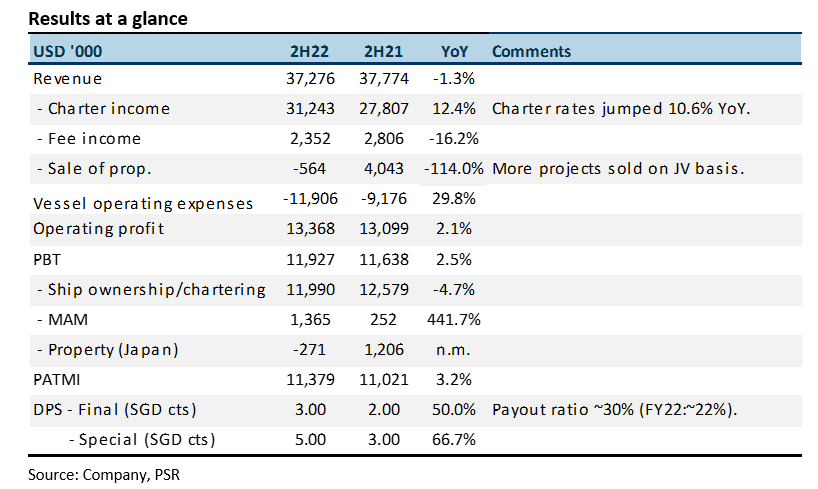

+ Growth in charter revenue. Charter revenue in 2H22 grew 12% YoY to S$31.2mn as the average charter rate per day expanded 10.6% to US$18,256. The company managed to lock in attractive rates in 1H22 despite a weaker environment. Uni-Asia wholly owns 10 dry bulk ships with another 8 as investments (~18% ownership stake in each vessel).

+ FY22 dividends more than doubled. Final and special dividends in FY22 jumped a combined 60% YoY to 8 cents per share. FY22 dividends more than doubled from 7 cents to 14.5 cents (or S$11.4mn). The payout ratio was around 30% (FY21: ~22%)

Phillip Securities Research has received monetary compensation for the production of the report from the entity mentioned in the report.

The Negative

- Decline in property sales. 2H22 property revenue declined significantly due to weaker Japanese currency and most of the projects sold were on a joint venture basis. We estimate the number of Alero projects sold in 2H22 was 5, down by 10 in 2H21. To recap, Uni-Asia will purchase land, builds 4-5 storey buildings with 10-30 unit apartments in Tokyo (named Alero), secures tenants and disposes the building to investors with a rental yield.

Outlook

From the recent peak in March 2022, the Baltic Exchange Handysize Index has corrected by 60% to current levels of around 700 (Figure 1). Any renewal of charters at spot rates by Uni-Asia in 1Q23 will be the weakest in more than 2 years. A positive has been the gradual rise in rates this year since the lows in January. The company has also been able to lock in medium-term charters at rates far higher than spot. It is a possible indication of higher rates in 2H23 as the recovery and re-opening of China builds momentum.

Supply of new handysize vessels remains muted. An issue is uncertainty over fuel type when ordering new vessels. If dual fuel is used for a vessel, it implies two tanks on the ship -1 fossil fuel and 1 alternative fuel (e.g. methanol or ammonia). However, there is insufficient space to accommodate both tanks. If only alternative fuel is deployed, vessel owners worry about sufficient supply or refuelling centres for such fuel. Another impediment to new vessels is the tightening of financing conditions and higher interest rates.

In the property division, no new funds will be deployed into Hong Kong before realizing proceeds from the existing five projects. Total investments in these five projects are US$23mn. On Alero, we expect a recovery in units sold as on-going projects (or pipeline for eventual sale) is 12 (FY21: 10).

The Positives

+ Attractive charter rates locked in. There were no financials provided in the 3Q22 update. The key data point disclosed was Uni-Asia’s average daily freight rate in 3Q22. With charter rates jumping 37% YoY in 3Q22 to US$19,609/day, we expect a similar jump in revenue. The dry docking of four vessels in 3Q22 may dampen some of the growth.

+ Progress made in property division. Hong Kong commercial projects have made progress in sales in 3Q22. It was disclosed that the 4th project sold 11% and the 5th project sales rose from 1/3 to 1/2. The pipeline for new Alero residential projects in Japan has also improved to 7 from 3 in the previous quarter.

The Negative

- Major decline in freight rates. Freight rates were weak in 3Q22, plunging 45% YoY, as indicated by Baltic Exchange Handysize Index. Unless rates recover in 1Q23, there is risk in our FY23e forecast.

Outlook

The Baltic Exchange Handysize Index began to slide in June (Figure 1). Rates in November are now close to 2020 levels, representing a drop of 55% YoY. Uni-Asia has managed to lock in attractive rates (Figure 2) but there is risk in the next renewal cycle for its fleet. We believe the next renewal cycle will be from 1Q23 onwards. Shipping lines are cautious due to the lack of visibility in demand for commodities in China and are not willing to commit to any forward charters.

The medium-term outlook for charter rates is favourable. Supply is constrained by tight shipyard capacity earmarked for containers and LNG carriers. Demand for new vessels is subdued due to uncertainty over the fuel types. New environmental regulation next year is expected to spur slow steaming of bulk vessels, further tightening the effective supply of vessels.

The Positives

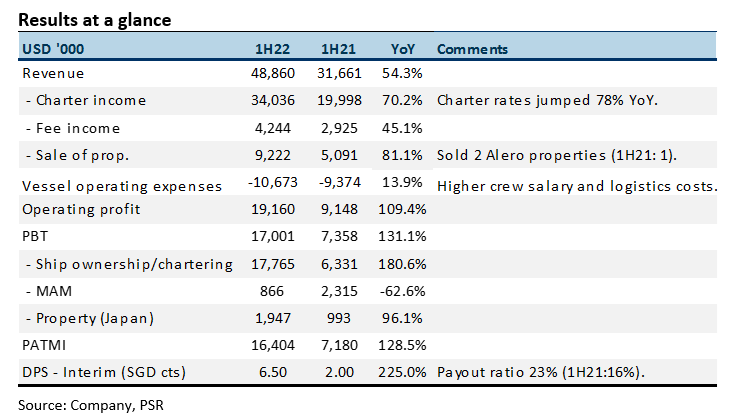

+ Surge in charter rates. Charter revenue rose 70% YoY to US$34mn, driven by a 78% jump in average daily charter hire rates to US$19.4k. Vessel operating days were 5% YoY lower due to a containership that was disposed of in 1Q21. Margins expanded as vessel operating expenses rose only 14% YoY to US$10.6mn. Higher cost was from crew salary, crew logistics and other expenses. Fuel cost is borne by the shipping company, not Uni-Asia.

+ Returning spike in cash flow to shareholders. FCF in 1H22 tripled to US$20.9mn (1H21: US$7.2mn). There are no current plans to order vessels. Net debt has halved to US$31mn (1H22: US$61mn) from a year ago. Uni-Asia announced an interim dividend of 6.5 SGD cents per share, a payout ratio of 23% (or S$5mn).

The Negative

- Lower pipeline of properties in Japan. In 1H22, Uni-Asia sold 2 units of its residential projects (i.e. Alero) located in Tokyo. The pipeline or ongoing projects is down to 8 from 13 a year ago. This implies fewer available projects to lease or for sale in the coming quarters.

Phillip Securities Research has received monetary compensation for the production of the report from the entity mentioned in the report.