The Positives

+ Revenue growth excluding top-5 clients still healthy. Revenue contribution excluding TDCX’s top 5 clients continued to grow (29% in 3Q23 vs 18% in 3Q22), while growing 52% YoY as newer campaigns in verticals like travel, gaming, FMCG, and e-commerce start to expand. New client campaigns for 3Q23 include: 1) global mobile messaging app; 2) leading global airline based in Asia.

+ Net margin improved on lower costs and higher interest income. Net margins expanded 150bps YoY as a result of: 1) 4% YoY reduction in employee expenses; 2) lowered tax expense due to a re-instatement of a tax incentive in PH; 3) ~2.5x increase in interest income on its S$434mn cash balance. PATMI improved 2% YoY.

The Negatives

- Lower seat volume from its top-2 clients was a big drag on growth. Revenue from its top 2 clients (47% of total revenue) declined -21% YoY on reduced seat volumes, even as these companies recorded very upbeat 3Q23 earnings. Near-term outlook also remains cloudy, with uncertainty around when these clients will begin to contribute meaningfully again to overall revenue growth. We reduce our FY24e revenue forecasts by ~4% as a result. Revenue excluding TDCX’s top-2 clients grew 14% YoY.

The Positives

+ Increasing revenue diversification. TDCX grew its client count 52% YoY, with client revenue mix excluding its top 5 contributors increasing to 27% (2Q22: 17%, 1Q23: 24%). In addition, its 1H23 expansion into Indonesia and Brazil have been a success, with Brazil amassing >100 pax headcount and receiving increasing inquiries from potential clients. Brazil is geographically important as it allows TDCX to cover the 2 most common languages in Latin America – Portuguese and Spanish, enabling the company to serve a wider range of cross-border international clients. TDCX also expanded into a new vertical – HealthTech, and added an established global e-commerce platform as well.

The Negatives

- Key digital advertising client cut volumes. One of TDCX’s key clients in the digital advertising vertical cut seats for the rest of FY23e as part of ongoing cost-cutting measures. This is expected to negatively impact revenue for TDCX’s Omnichannel CX and Content, Trust & Safety segments.

- Travel & Hospitality vertical disappointed. The expected growth from travel & hospitality – one of TDCX’s largest verticals, did not materialise due to continued weakness in China outbound travel. The outlook for this vertical was weak, with no expectations of significant improvement in 2H23e.

- Reduced FY23 revenue and margin guidance. TDCX reduced its FY23e revenue growth outlook to 2-4% in constant currency, from its prior guidance of 3-8%. This downward revision was led by a lengthening sales cycle, delays in deals closing, and cautious spending by clients. In addition, positive earnings results from some of its key clients have not translated immediately into seats volume. On the margin side, TDCX reduced the top end of its adj. EBITDA margin guidance to 25-27% (from 25-29%), citing clearer visibility on expenses related to new initiatives as the main reason for the revision.

Outlook

Guidance: TDCX reduced its FY23e revenue growth range to 2-4% in constant currency, down from its prior guidance of 3-8%, citing longer sales cycles, a slower-than-anticipated velocity on closing, and continued cautious spending by clients as the reasons for the revision in guidance. Recovering profitability in some of TDCX’s key clients have also not translated immediately into seats volume, with uncertainty surrounding when these clients would start to increase their spending again. However, TDCX also said that is starting see more complex inquiries coming in from clients, indicating that there are some early signs of a potential rebound in FY24.

On the margin side, TDCX reduced the top end of its adj. EBITDA margin guidance to 25-27% (from 25-29%), citing clearer visibility on expenses related to new initiatives as the main reason for the revision. We view the company’s strategic expansion to be significant as it provides: 1) greater linguistic capabilities for more efficient cross-border services; 2) faster ramp-up in campaigns for clients wanting to expand geographically.

The Positives

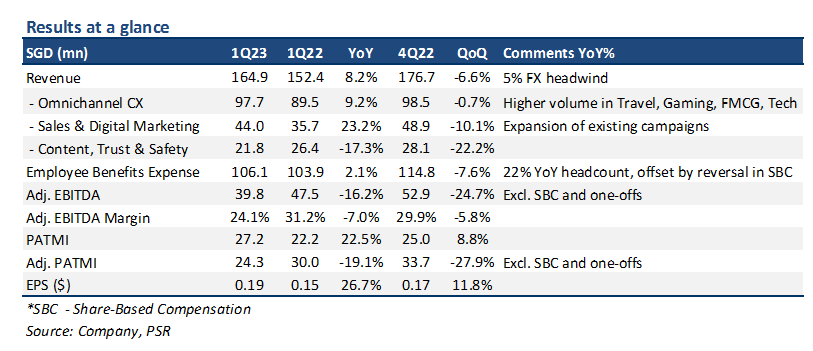

+ Continued diversification in revenue mix. Revenue, excluding its top 5 clients, grew 45% YoY. Top 5 clients’ revenue contribution as a % of total revenue stood at 76% in 1Q23 (1Q22: 83%). Newer geographies incorporated in 2021 (South Korea, Colombia, Romania) are also starting to show meaningful contributions, with revenue growing >4x in 1Q23 vs 1Q22.

+ Travel & hospitality continued to be a bright spot. Revenue from the company’s 2nd largest vertical was up 34% YoY, more than offsetting the slight contraction in YoY revenue from the company’s largest vertical (Digital Advertising & Media). Growth in this vertical was boosted by continued rebound in cross-border travel, with an expectation for this trend to continue as outbound China travel increases.

+ Leveraging AI for growth. ~70% of TDCX’s business is B2B, with many of these clients looking for increasingly complex business solutions. TDCX recently launched TDCX AI, a new specialised consulting division to meet this need – using AI insights and tools to deliver highly personalized and complex customer experience (CX) solutions for clients at a faster pace. Additionally, TDCX is also investing in generative AI tools for improved operational efficiency.

The Negative

- Margin dip due to business expansion. 1Q23 Adj. EBITDA margins were down 7% point YoY to 24.2%. There were several reasons for this: 1) absence of non-recurring government grants from 1Q22; 2) increase in general overheads (hiring and training of new staff) due to expansion into 2 new geographies; 3) increase in group corporate costs excluding SBCs.

The Positives

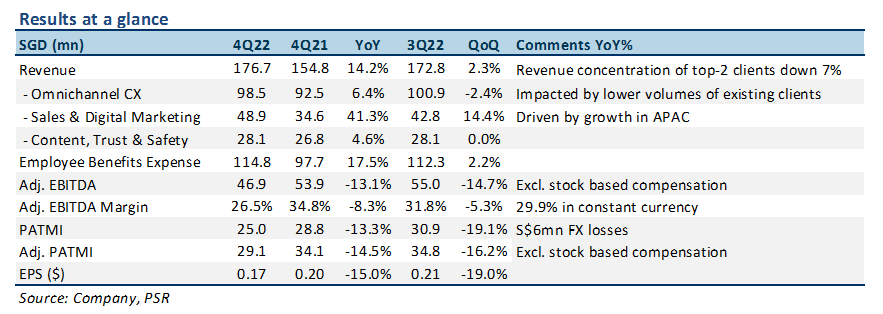

+ Revenue growth driven by digital advertising vertical. TDCX’s 4Q22 revenue grew 14% YoY, driven by a double-digit growth from clients in the digital advertising and media vertical – 54% of total revenue. The company’s second largest vertical - travel & hospitality, also saw strong 26% YoY growth with travel rebounding globally. TDCX’s net revenue retention rate was at 117%, demonstrating a healthy incremental revenue pipeline from existing clients.

+ Expansion over last 2 years starting to bear fruit, reduction in revenue concentration risk. TDCX’s expansion into 7 new geographies over the last 2 years is starting to pay off, with clients added from this expansion contributing ~10% of revenue growth in FY22e. For 4Q22, TDCX added 10 new clients, and also launched 12 new client campaigns, increasing its total client campaign count by 62% YoY. In addition, these new clients aided in reducing the overall revenue concentration risk of the company, with its top-2 clients as a percentage of total revenue down 700bps to 52%.

The Negatives

- Soft FY23e guidance due to limited visibility. Macro uncertainty continues to impact client headcount requirements in the near term, with the digital advertising vertical affected the most severely. As a result, expected volume flattening from clients in this vertical (58% of total revenue) dragged down FY23e revenue guidance.

- Margins declined due to combination of over-hiring and continued investments to support business growth. 4Q22 adj. EBITDA margins contracted 830bps from 4Q21 to 26.5% as a result of over-hiring in anticipation of volume growth that did not materialise, and increased costs to support continued business growth.

Downgrade ACCUMULATE with a reduced target price of US$14.80

FY23e revenue growth of 15% YoY is still the fastest amongst CX peers, with the average around 8-10%. Adj. EBITDA margins of ~31% are similar to FY22e levels, and in line with the company’s expectations as it continues expanding geographically. We downgrade to ACCUMULATE with a reduced DCF target price of US$14.80 (prev. US$15.50), a WACC of 10.4%, and a terminal growth rate of 3.0%.

The Positive

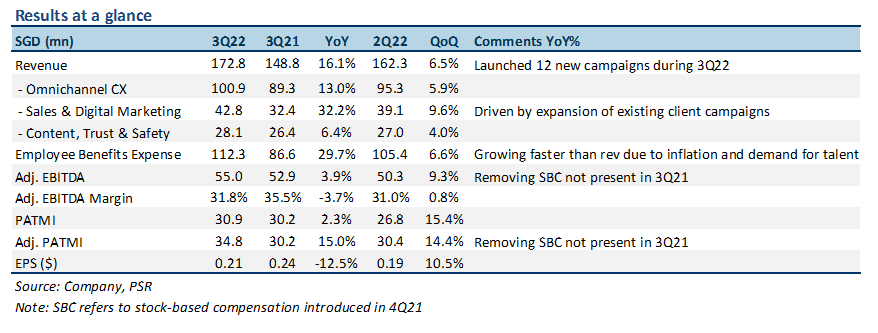

+ Travel and hospitality rebound providing growth tailwinds. Revenue from TDCX’s travel & hospitality vertical grew about 29% YoY for 3Q22, boosted by higher contributions from existing clients, and new revenue from clients added over the last several quarters. Revenue from this vertical has returned to pre-pandemic levels, with potential reopening of countries in North Asia providing optimism for further growth in this vertical. Travel and hospitality remain the company’s 2nd largest vertical in terms of revenue contribution.

The Negatives

- Revenue growth decelerating sequentially. TDCX recorded 3Q22 revenue growth of 16% YoY, down sequentially from 27% and 24% over the first 2 quarters of this year. Growth is expected to continue trending downwards for the rest of this year given inflation fears and significant pullback in expenses spending by many new economy companies. 4Q22e revenue growth is expected to be around only 13% YoY – taking the midpoint of the company’s FY22e guidance.

+ Adj. EBITDA margin down almost 4% YoY. Stripping out share-based compensation that did not occur in 3Q21, TDCX’s Adj. EBITDA margin for 3Q22 was down 370bps to 31.8%. Several reasons for this including: 1) significantly higher business volume in 3Q21 vs 3Q22; 2) a catch-up revenue reduction related to a warrants agreement with Airbnb; 3) increasing corporate overhead costs due to business expansion; and 4) 30% higher employee benefits expense YoY due to increasing demand for talent. 9M22 Adj. EBITDA margin was at 31.4%, within the company’s FY22e guidance range of 30-32%.

The Positives

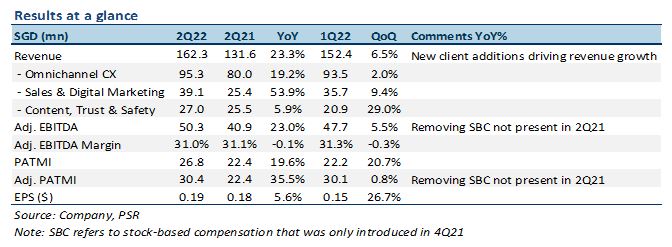

+ 15 client additions in 2Q22, 25 for 1H22; more than triple 1H21. The new clients included a leading regional airline, a leading integrated car e-commerce platform, three FinTech companies and one insurance company. New client additions drove revenue up 23% YoY for the quarter, and also strengthened TDCX’s leadership in the e-commerce, travel, and FinTech verticals. TDCX also saw a 40% YoY increase in launched client campaigns, demonstrating an increasing ability to accelerate campaign growth, while maintaining low levels of revenue churn.

+ Benefitting from rebound in travel & hospitality sector in the region. Revenue from TDCX’s travel & hospitality vertical grew about 25% YoY, boosted by upward momentum in travel due to global re-opening over the summer period. Although revenue from this vertical is still about 16% shy of its pre-pandemic peak, the potential reopening of countries in North Asia – China, Japan, etc -- does provide optimism for increasing revenue contribution from travel & hospitality in the near-term.

+ Expansion of Adj. Net Margin amidst tougher macro environment, mainly due to reducing expenses. Stripping out share based compensation that did not occur during 1H21, TDCX managed to expand their adj. net margins for 1H22, increasing by 1.4% YoY, from 17.8% in 1H21 to 19.2% in 1H22. One of the main reasons for this was a sharp decline in interest expenses as a result of the company paying off a significant portion of its short-term, and all of its long-term debt. Adj. EBITDA margins remained relatively flat YoY at 31%.

The Negatives

- Higher-than-expected tax rate due to suspension of tax reliefs in MY and PH. TDCX recorded an effective tax rate of about 27% in 2Q22, up from about 21% in 2Q21, mainly due to a one-off “prosperity tax” in Malaysia, and the suspension of a tax holiday in the Philippines.

The Positives

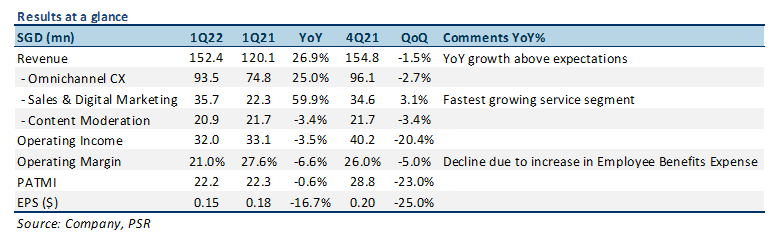

+ Higher-than-expected 1Q22 revenue growth compared to our estimates. TDCX’s YoY revenue growth of 27% was slightly higher than our estimate of about 25%. Sales & Digital Marketing was the main driver of growth – 60% YoY, and we expect this to continue for FY22e as more companies turn to outsourced specialised services like TDCX to maximize their marketing budgets. Revenue contribution from new economy clients remained at 93%, similar to 4Q21.

+ 10 new client additions for 1Q22, more than double 1Q21. TDCX added 10 new clients in 1Q22, including a leading global short-form video platform, and a leading Southeast Asian e-commerce platform. The company started its partnership with offices in Singapore and Barcelona for the short-form video platform, and offices in Malaysia for the e-commerce platform, serving both clients across its Omnichannel CX and Sales & Digital Marketing services segments.

The Negatives

- Decline in margins YoY due to increase in equity share payments included in employee benefits expense. Employee Benefits Expense jumped 39% YoY for 1Q22, increasing by 6% points to 68% of total revenue for the quarter. The main reason for this was an S$8mn equity share payment related to the company’s Performance Share Plan that was introduced in 4Q21. Removing this would result in a 28% YoY growth in Employee Benefits Expense, in line with revenue growth. This also led to contracting Operating Margins from 28% to 21% YoY.

- Reduced FY22e revenue guidance due to increasing macroeconomic uncertainty and weakness. TDCX revised its FY22e revenue guidance down by slightly more than 5%, to S$650mn-675mn, representing a 19% YoY increase taking the midpoint. The company cited a general weaker and uncertain macroeconomic environment, and slower-than-expected expansion of some of its clients as reasons for this revised guidance.

Company Background

TDCX Inc. operates as an outsourced digital customer experience provider focusing on Omnichannel Customer Experience (CX), Sales & Digital Marketing, Content Monitoring & Moderation. CX solutions are provisions of services that enhance how a business interacts with a customer throughout the customer’s lifecycle, examples of this include: after-sales service and support; design and marketing of a company’s web platform.

Investment Merits

We Initiate coverage with a BUY rating and a target price of US$22.00 based on DCF valuation, with a WACC of 9.7% and terminal growth of 3%.

REVENUE

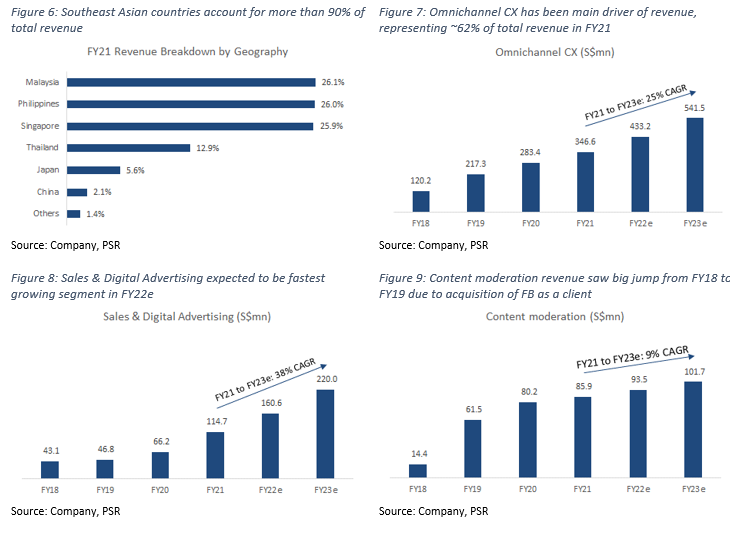

TDCX generates revenue from providing services and solutions in 3 main areas: 1) Omnichannel customer experience (CX); 2) Sales and digital marketing; 3) Content monitoring and moderation. 62% of all revenue is generated from omnichannel CX, with 22% from sales and digital marketing, and the remaining 14% from content monitoring and moderation (Figure 5). Southeast Asian countries like Singapore, Phillippines, Thailand, and Malaysia contribute about 91% of revenue, with 8% coming from north Asian countries like Japan and China, and the remaining 1% from the rest of the world (Figure 6).

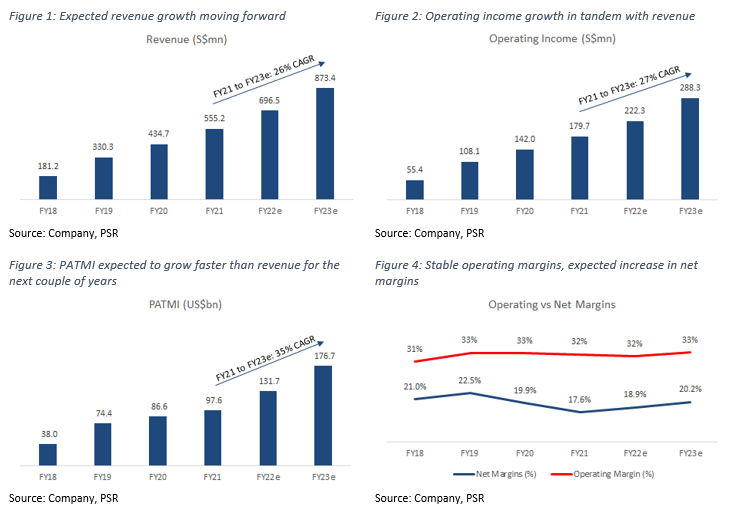

The company posted S$555mn in total revenue for FY21, representing a 28% YoY growth, below its 3-year CAGR of 45%. Also, FY21 was a very good year for TDCX as it added 20 new clients, compared with only 9 new additions in FY20, and ended the year with 52 total clients. TDCX has been aggressively adding clients in new verticals to its portfolio, particularly in FinTech, Gaming, Crypto, and Food Delivery. Revenue from FinTech and Gaming grew 67%, and 99% YoY respectively in FY21. Besides new verticals, the company has also focused on expanding into new geographies in countries like Colombia, Romania, India, and South Korea.

Omnichannel CX: This segment is the bread and butter of TDCX, contributing slightly over 62% of total revenue. Revenue from Omnichannel CX grew 22% YoY in FY21 to about S$347mn, and has been growing at a 3-year CAGR of 42%. We expect YoY growth to pick up slightly in FY22e to about 25%, led by a strong rise in new contracts over the last 2 quarters of FY21 (Figure 7).

Sales & Digital Marketing: This segment saw 73% YoY growth in FY21, posting revenues of S$115mn, in part due to a very strong rebound in the overall digital advertising industry after a weak FY20 plagued by budget cuts due to COVID-19. We do expect growth in this segment to temper slightly to around 40% YoY growth due to a moderation in the digital advertising market (Figure 8).

Content Monitoring & Moderation: Revenue from content monitoring and moderation only grew 7% YoY to S$8mn in FY21. Part of the slower growth rate in this segment is due to the fact the TDCX had only 1 social media client under this segment – Meta Platforms. However, the company recently acquired 2 new contracts from a gaming platform, and another social media company, which should help to boost growth in this segment moving forward. As a result, we expect growth in this segment to be around 9% for FY22e (Figure 9).

Revenue Growth: We expect revenue growth to come mainly from existing new economy clients, especially as revenues from new clients tend to start expanding only after about 2-3 years. We expect this growth to also be heavily supported by tailwinds in the overall Southeast Asian digital CX industry for new economy companies, which is expected to grow at a 5-year CAGR of 13%. We are buoyed by TDCX’s ability to continue adding new clients YoY, as well as growing revenue from its existing clients. For FY22e, we expect total revenue growth to increase slightly to 25% YoY, or around S$696mn, roughly in line with the company’s guidance of S$690mn-700mn, led to strong growth across all segments and verticals

RULE OF 40

The “Rule of 40” was first introduced as a benchmark to measure the balance between growth and profitability of SaaS companies, taking into account both revenue growth, as well as profitability (Revenue Growth + EBITDA Margins), with the addition of both metrics needing to exceed the 40% threshold. We have modified this slightly by averaging revenue growth over a 3-year period compared to just a single period growth rate. Adding together TDCX’s 3-year average revenue growth of 45.2% and its EBITDA margin of 32.4%, the total of 77.6% is > than our required threshold of 40%.

EXPENSES

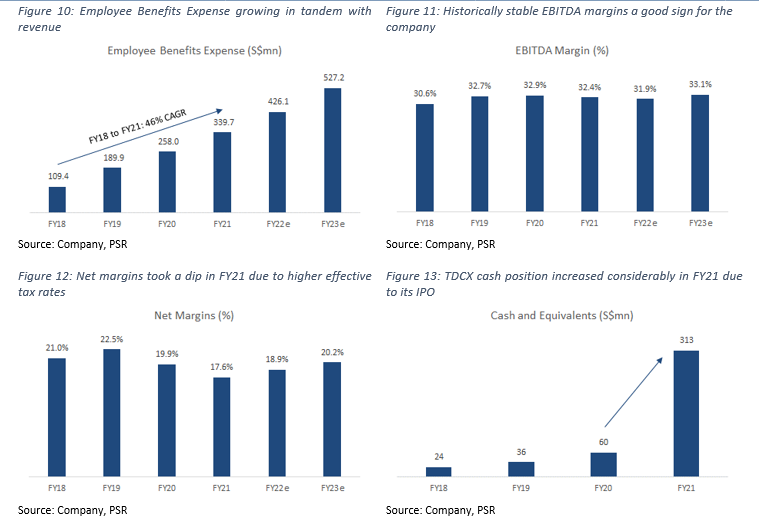

As a service provider, the bulk of TDCX’s expenses come from employee-related expenses which the company labels as “Employee Benefits Expense”. In FY21, the company recorded S$340mn in Employee Benefits Expense, which represents roughly 61% of revenue (Figure 10). This expense grew 32% YoY, slightly faster than revenue growth, and was primarily due to an increase in employee headcount to support business volume, and share-based expenses from the introduction and implementation of the company’s maiden performance share plan.

MARGINS

TDCX recorded gross profit margins of 38.8% for FY21, a slight decrease from 40.7% the year before, and was mainly due to an increase in Employee benefits Expense.

EBITDA margins for FY21 remained stable at around 32.4% (Figure 11), with a 4-year range of 30-33%. This is significantly higher compared with its peers: TaskUs (24.8%), Concentrix (16.2%), Teleperformance (15.1%), Telus International (24.6%)

Net margins for FY21 were 17.6% (Figure 12), and have been decreasing slightly over the last few years, this has been largely due to an increasing effective tax rate.

BALANCE SHEET

Assets: Cash and cash equivalents increased from S$60mn to S$313mn in FY21 (Figure 13), due to an inflow of capital from the company’s IPO listing. Receivables increased from S$49mn to S$106mn, and this was due to a couple of large clients that had some administrative challenges, leading to a backlog in billings. These receivables had been recovered during the middle of 1Q22. TDCX recorded total assets of S$582mn in FY21.

Liabilities: Short-term and long-term debt reduced by S$10mn and S$13mn respectively, and this debt was paid down using cash from the company’s IPO listing in FY21. Other payables were recorded at S$39mn for FY21, with lease liabilities (both current and non-current) amounting to S$36mn.

CASH-FLOW

TDCX recorded Free Cash Flow (FCF) of S$83mn in FY21, a 27% YoY decrease from FY20, largely in part from a S$58mn increase in receivables which were collected only in 1Q22. The company has been FCF positive since FY18, and we expect this trend to continue moving forward based on its highly stable, cash generative business model.

BUSINESS MODEL

TDCX operates as an outsourced digital customer experience provider, with 3 main pillars of focus: Omnichannel Customer Experience (CX), Sales & Digital Marketing, Content Monitoring & Moderation. The company focuses predominantly on servicing fast growing new economy clients, particularly in the Southeast Asian region, while looking to other Asian and European markets for opportunities to expand. As of end FY21, TDCX had 52 clients, 20 of which were added in FY21 alone, and extend to a wide range of verticals ranging from travel and hospitality to fintech. Prominent clients of TDCX include leading social media platform, Facebook, leading travel & hospitality platform, Airbnb, and leaders in other high-growth verticals (Figure 14).

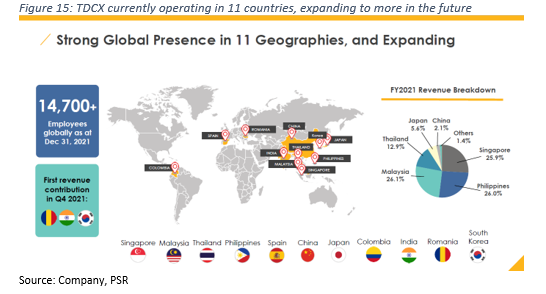

The company currently has almost 15,000 employees globally, with 3,000 additions in 4Q21 alone (Figure 15), and is constantly striving to keep up with the needs of its fast-moving clients. TDCX has a very extensive network of delivery centers both from a local level, and a regional level, with talent proficient in more than 20 languages and a deep understanding of high-growth verticals in the region – a key component when serving such a diverse group of geographies. From a strategic point on view, leverages on its expertise and presence in the different countries it operates in to help cross-border expansion of its clients.

TDCX leverages on technology like Artificial Intelligence and Machine Learning to improve the quality and efficiency of its services, they also deploy bots and robotic process automation (RPA) to drive productivity gains. As their business model is very labour reliant, TDCX has also developed a proprietary virtual recruitment platform, Flash Hire, to assist in speeding up its own hiring process, improving the company’s ability to scale and fulfil the requirements of its clients at a fast and efficient rate. According to the company, Flash Hire helped to reduce hiring time by almost 62%.

TDCX’s revenue stream comes mainly from service contracts it negotiates with its clients, which usually run from 1-3 years and are generally quite sticky in nature. Some of the terms in these contracts include clauses like variable relocation benefits, which allow TDCX to charge their clients accordingly if the cost of living fluctuates in a particular region.

Omnichannel Customer Experience (CX): This segment entails managing clients’ customer relationships by providing both inbound and outbound customer experience solutions, which also generally cover the entire life-cycle of the customer. The services that fall under this segment are also usually highly tailored to specific companies or verticals, and also involve more complexed interactions between agent and customer – technical end-user troubleshooting for software and consumer electronic devices, aftersales service and support, etc. TDCX uses metrics like average inbound holding time and percentage of first call resolution to measure its service levels.

Sales & Digital Marketing: It develops digital advertising campaigns for B2B and B2C clients to market their products and services. For B2B, this usually involves helping an advertising platform client grow and attract more advertising dollars, while B2C generally involves more sales and direct-marketing capabilities for clients. TDCX leverages on its analytical capabilities in this domain to provide valuable business insights to increase marketing efficiency. Return on advertising spend and conversion ratios are some metrics TDCX monitors to ensure performance of its marketing services.

Content Monitoring & Moderation: It assists clients in creating a safe and secure online environment for social media and gaming platforms through content monitoring and moderation services performed by an actual human.