The Positives

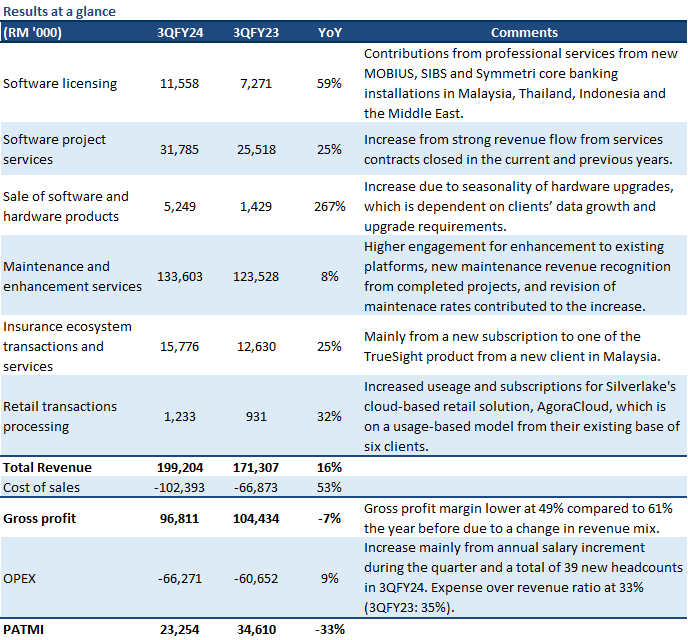

+ Recurring revenue rose 10% YoY. Recurring revenue comprises maintenance and enhancement services, insurance ecosystem transactions and services, and retail transactions processing revenue. Maintenance and enhancement services grew 8% YoY to RM134mn from new maintenance revenue recognition for projects that had been successfully completed and handed over to clients and revised maintenance rates for some clients upon maintenance renewal. There was also continued engagement from customers to enhance, modernise and provide up-to-date features in the platforms that were previously acquired. Silverlake expects this segment to continue to grow as new maintenance contracts and support will commence when current projects are completed and successfully handed over to clients. Insurance ecosystem transactions and services revenue rose 25% YoY, mainly due to new subscriptions to one of the TrueSight products from a new client in Malaysia. Retail transaction processing revenue grew 32% YoY from increased usage and subscriptions to new modules for Silverlake's cloud-based retail solution, AgoraCloud. As this is a usage-based model, Silverlake has seen increased usage from its existing base of six clients.

+ Non-recurring revenue grows 42% YoY. Non-recurring revenue comprises software licensing, software project services, and the sale of system software and hardware products. Software licensing revenue rose 59% YoY due to contributions from professional services from new MOBIUS, SIBS, and Symmetri core banking installations in Malaysia, Thailand, Indonesia, and the Middle East. Software project services revenue grew 25% YoY as a result of new revenue flow from strong revenue flow of services contracts closed in the current and prior years, while sales of seasonal system software and hardware products surged 267% YoY.

+ Order backlog healthy. Silverlake has a long track record and a proven client base in Southeast Asia. Three of the five largest Southeast Asia-based financial institutions use its core banking platform, and it has largely retained all its clients since bringing them on board its platform. Silverlake’s project pipeline is healthy, at RM1.2bn (2QFY24: RM1.4bn), with contract wins of RM99mn in 3QFY24 and an order backlog of RM180mn going into the rest of FY24. Silverlake is beginning to close more deals and is witnessing an uptick in inquiries about its financial services market solutions and capabilities.

The Negatives

- OPEX continues to climb. Operating expenses were 9% higher YoY due to an annual salary increment exercise, and new headcount to support business development, business expansion, improved sales and market coverage, and retirement gratuity granted to key management personnel. Notably, 39 new headcounts were added in 3QFY24 compared to 3QFY23. Other OPEX increases include IT-related expenses, particularly in software subscription and support, as well as laptop leasing for new headcounts, business travels and a conference held by Silverlake.

The Positives

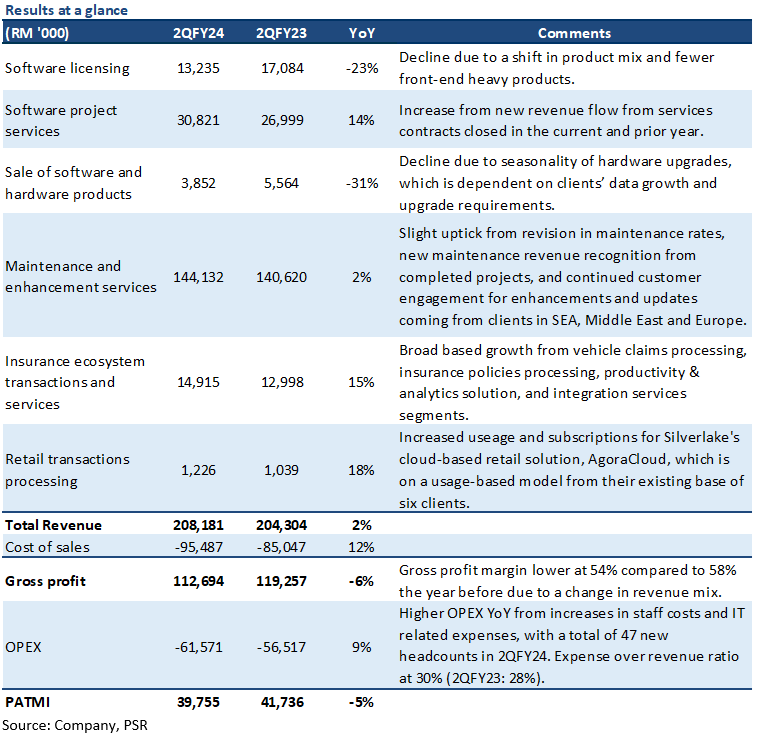

+ Recurring revenue rose 4% YoY. Recurring revenue comprises maintenance and enhancement services, insurance ecosystem transactions and services, and retail transactions processing revenue. Maintenance and enhancement services grew 2% YoY to RM144mn from revised maintenance rates for some clients upon maintenance renewal and new maintenance revenue recognition for projects that had been successfully completed and handed over to clients. There was also continued engagement from customers to enhance, modernise and provide up-to-date features in the platforms that were previously acquired. Growth mainly came from clients in Southeast Asia, the Middle East, and Europe. Silverlake expects this segment to continue to grow as new maintenance contracts and support will commence when current projects are completed and successfully handed over to clients. Insurance ecosystem transactions and services revenue rose 15% YoY as there was broad-based growth across all segments, from vehicle claims processing, insurance policies processing, productivity and analytics solutions, and integration services. Retail transaction processing revenue grew 18% YoY mainly due to increased usage and subscriptions to new modules for Silverlake's cloud-based retail solution, AgoraCloud. As this is a usage-based model, Silverlake has seen increased usage from its existing base of six clients as the client base grew from the retail sector in FY21 to the pharmaceutical industry.

+ Order backlog healthy. Silverlake has a long track record and a proven client base in Southeast Asia. Three of the five largest Southeast Asia-based financial institutions use its core banking platform, and it has largely retained all its clients since bringing them on board its platform. Silverlake’s project pipeline is healthy, at RM1.4bn (1QFY24: RM1.8bn), with contract wins of RM114mn in 2QFY24 and an order backlog of RM790mn going into the rest of FY24. Furthermore, Silverlake expects revenue from the multi-million 10-year core and channels digital banking MOBIUS deal with a client in Malaysia to come in FY24. Silverlake is beginning to close more deals and is witnessing an uptick in inquiries about its financial services market solutions and capabilities.

The Negatives

- OPEX rose 9% YoY. Operating expenses were higher mainly due to annual salary increments post-pandemic, effected in 3QFY23, and new headcounts added to support business development and business expansion, sales and market coverage, and retirement gratuity paid to key management personnel. Notably, there was an addition of 47 new headcounts in 2QFY24 as compared to 2QFY23. Other OPEX increases include IT-related expenses, particularly in software subscription and support, as well as laptop leasing for new headcounts; business travels due to the economic recovery post-pandemic, and interest charged on revolving credit utilised. As a result, the expense-over-revenue ratio rose to 30% (2QFY23: 28%).

- Non-recurring revenue falls 4% YoY. Non-recurring revenue comprises software licensing, software project services, and sale of system software and hardware products. Software licensing revenue fell 23% YoY as there was a shift towards cloud-based systems such as MÖBIUS and Symmetri, which do not have as much initial revenue recognition as compared to legacy systems like SIBS. Silverlake continues to see core banking installations in Malaysia, Thailand, Indonesia and the Middle East, and a digital identity and security software project implementation in Africa. The decline was slightly offset by software project services revenue increasing 14% YoY as a result of new revenue flow from strong revenue flow of services contracts closed this year and the prior year, with the projects proceeding as planned.

Outlook

Building a higher quality order book. Silverlake has a tender book of RM1.4bn going into the rest of FY24, with more than half of it coming from its core banking systems, MOBIUS and Symmetri. While the initial revenue from these systems will be smaller than that from legacy core banking systems, such as the Silverlake Integrated Banking Solution or SIBS, we expect it to improve recurrent fees. Cloud banking software, such as MOBIUS and Symmetri, avoid the need for banks to purchase and manage hardware assets, which results in lower initial costs and, consequently, initial revenue for Silverlake. However, there would be a need for continuous enhancement and maintenance of these systems, improving the quality of Silverlake’s order book with the bulk of growth coming from recurrent fees.

Visible growth from new product cycles - Silverlake signed a deal with one of the largest banks in Thailand and its first multi-million 10-year core and channels digital banking MOBIUS deal with a client in Malaysia. The collaboration with the Thailand bank has shown the proof of concept, and it is a significant reference site for MOBIUS. With this, we could see more inquiries for the rest of FY24, with an imminent deal with a Thailand bank worth ~RM30mn. There is also a potential for replacing core banking systems with MOBIUS as several legacy core banking systems approach end-of-life, and banks have fewer limitations to adopt a fully cloud-based core. Silverlake has seen a shift towards Software-as-a-Service (SaaS) and cloud computing. With Silverlake’s offering of cloud-based systems, we could expect the demand for these systems to continue going into the rest of FY24. Silverlake has also begun to offer a repackaged version of its legacy core system, SIBS, where only certain modules will be offered and have seen this banking-as-a-service being taken up by Thailand customers.

The Positives

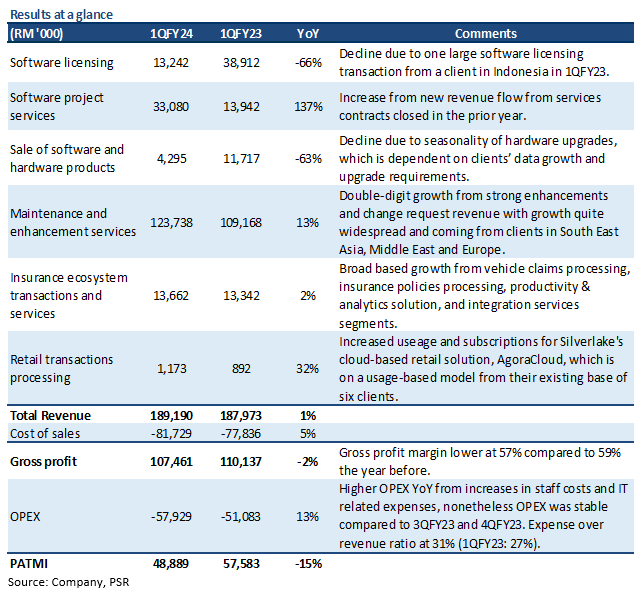

+ Recurring revenue rose 12% YoY. Recurring revenue comprises maintenance and enhancement services, insurance ecosystem transactions and services, and retail transactions processing revenue. Maintenance and enhancement services grew 8% YoY to RM124mn from strong enhancements and change request revenue as Silverlake continues to guide its customers in modernising their core platforms with growth coming from clients in Southeast Asia, the the Middle East and Europe. Silverlake expects this segment to continue to grow as new maintenance contracts and support will commence when current projects are completed and successfully handed over to clients. Insurance ecosystem transactions and services revenue increased 2% YoY as there was broad-based growth across all segments, from vehicle claims processing, insurance policies processing, productivity and analytics solutions, and integration services. Revenue from retail transactions processing grew 32% YoY mainly due to increased usage and subscriptions to new modules for Silverlake's cloud-based retail solution, AgoraCloud. As this is a usage-based model, Silverlake has seen increased usage from its existing base of six clients.

+ Order backlog healthy. Silverlake has a long track record and a proven client base in Southeast Asia. Three of the 5 largest Southeast Asia-based financial institutions use its core banking platform, and it has largely retained all its clients since bringing them on board its platform. Silverlake’s project pipeline is healthy, at RM1.8bn (4QFY23: RM1.5bn), with contract wins of RM125mn in 1QFY24 and an order backlog of RM720mn-730mn going into the rest of FY24. Furthermore, Silverlake expects revenue from the multi-million 10-year core and channels digital banking MOBIUS deal with a client in Malaysia to come in FY24. Silverlake is beginning to close more deals and is witnessing an uptick in inquiries about its financial services market solutions and capabilities.

The Negatives

- OPEX rose 13% YoY. Operating expenses were 13% higher YoY mainly due to annual salary increment post-pandemic, effected in 3QFY23 and new headcounts added to support business development and business expansion, sales and market coverage. Other OPEX increases include IT-related expenses particularly in software subscription and support as well as laptop leasing for new headcounts and business travels due to economic recovery post-pandemic. As a result, the expense over revenue ratio rose to 31% (1QFY23: 27%). Nonetheless, OPEX was stable when compared to 3QFY23 and 4QFY23, and management does not expect OPEX to increase QoQ going into the rest of FY24 with no current plans for further headcount increases.

- Project-related revenue falls 12% YoY. Project-related revenue comprises software licensing and software project services. Software licensing revenue fell 66% YoY as 1QFY23 included one large software licensing transaction from a client in Indonesia. Nonetheless, there were major contributions from professional services from key core banking projects secured in FY23 – namely new MÖBIUS, SIBS and Symmetri core banking installations in Malaysia, Thailand, the Middle East, and South Asia. The decline was slightly offset by software project services revenue increasing 137% YoY as a result of new revenue flow from services contracts closed in FY23.

The Positives

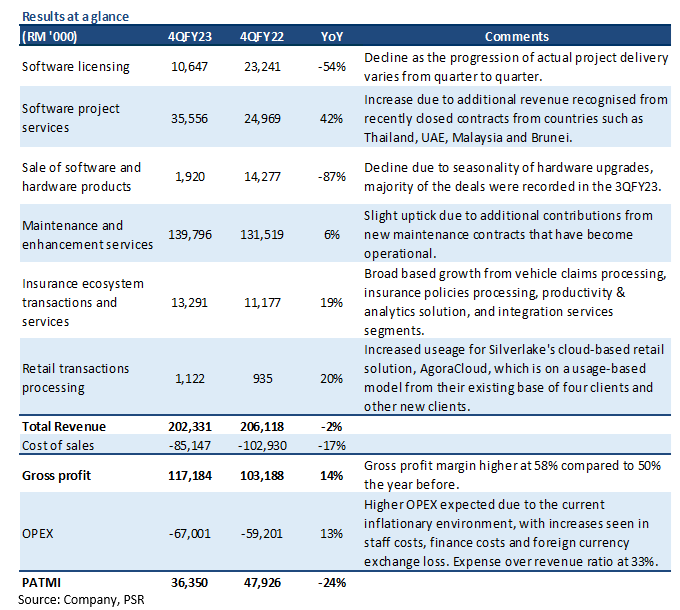

+ Recurring revenue rose 7% YoY. Recurring revenue comprises maintenance and enhancement services, insurance ecosystem transactions and services, and retail transactions processing revenue. Maintenance and enhancement services grew 6% YoY to RM140mn and Silverlake expects this segment to continue its growth as new maintenance contracts and support will commence when current projects are completed and successfully handed over to the clients. Insurance ecosystem transactions and services revenue increased 19% YoY as there was broad-based growth across all segments, from vehicle claims processing, insurance policies processing, productivity and analytics solutions, and integration services. Revenue from retail transactions processing grew 20% YoY mainly due to increased usage for Silverlake's cloud-based retail solution, AgoraCloud. As this is a usage-based model, Silverlake has seen increased usage from their existing base of four clients as well as new clients whom they have signed up.

+ Order backlog healthy. Silverlake has a long track record and a proven client base in Southeast Asia. Three of the 5 largest Southeast Asia-based financial institutions use its core banking platform, and it has largely retained all its clients since bringing them on board its platform. Silverlake’s project pipeline is healthy, at RM1.5bn (3QFY23: RM1.8bn), with contract wins of RM93mn in 4QFY23 and an order backlog of RM223mn on the verge of closing in 1QFY24. Furthermore, Silverlake expects revenue from the multi-million 10-year core and channels digital banking MOBIUS deal with a client in Malaysia to come in FY24. Silverlake is beginning to close more deals and is witnessing an uptick in inquiries about its financial services market solutions and capabilities.

The Negatives

- OPEX rose 13% YoY. Operating expenses were 13% higher YoY mainly due to the current inflationary environment, and to support growth in new delivery of services projects and future proofing of long-term growth and sustainability of their business. The increase was across all segments, with increases in staff costs due to additional headcount, increase in finance costs due to a revolving credit facility drawdown, increase in foreign currency exchange losses due to the fluctuation of foreign currencies, and higher costs for internal and external branding activities as markets opened up. Nonetheless, the expense over revenue ratio was kept at 33%.

- Project-related revenue fell 4% YoY. Software licensing revenue fell 54% YoY was due to the progression of actual project delivery varying from quarter to quarter, resulting in a lag in revenue contribution. However, this was offset by software project services revenue increasing 42% YoY as there was additional revenue recognised from recently closed contracts from countries such as Thailand, UAE, and Malaysia. In addition, progressive project revenue recognised from on-going secured projects remained at a stable level.

The Positives

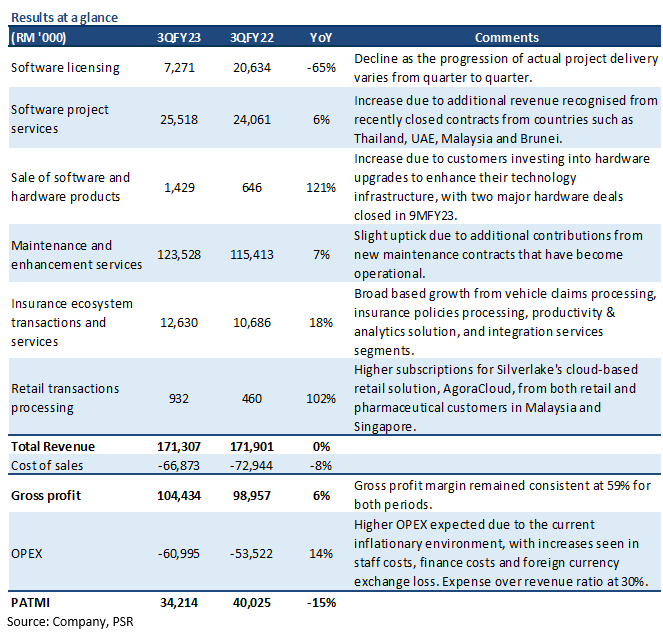

+ Recurring revenue rose 8% YoY. Recurring revenue comprises maintenance and enhancement services, insurance ecosystem transactions and services, and retail transactions processing revenue. Maintenance and enhancement services increased 7% YoY to RM124mn as the dip in enhancement services revenue was more than offset by the increase in maintenance revenue. The decline in enhancement services revenue was mainly due to the timing and progress of contracts fulfilment and delivery, and Silverlake anticipates this will be recognised and booked in the following quarter. Insurance ecosystem transactions and services revenue increased 18% YoY as there was broad-based growth

across all segments, from vehicle claims processing, insurance policies processing, productivity and analytics solutions, and integration services. Revenue from retail transactions processing surged 102% YoY mainly due to higher subscriptions for Silverlake's cloud-based retail solution, AgoraCloud, from both retail and pharmaceutical customers in Malaysia and Singapore.

+ Order backlog healthy. Silverlake has a long track record and a proven client base in Southeast Asia. Three of the 5 largest Southeast Asia-based financial institutions use its core banking platform, and it has largely retained all its clients since bringing them on board its platform. Silverlake’s project pipeline is healthy, at RM1.8bn (2QFY23: RM1.8bn), with a record contract wins of RM259mn in 3QFY23 and an order backlog of RM261mn on the verge of closing in 4QFY23. Furthermore, Silverlake has recently secured their first multi-million 10-year core and channels digital banking MOBIUS deal with a client in Malaysia. Silverlake is beginning to close more deals and is witnessing an uptick in inquiries about its financial services market solutions and capabilities.

The Negatives

- OPEX rose 14% YoY. Operating expenses were 14% higher YoY mainly due to the current inflationary environment and a need to support long-term growth and sustainability. The increase was across all segments, with increases in staff costs due to additional headcount, increase in finance costs due to a revolving credit facility drawdown, increase in foreign currency exchange losses due to the fluctuation of foreign currencies, and higher costs for internal and external branding activities as markets opened up. Nonetheless, the expense over revenue ratio was kept at 30%.

- Project-related revenue fell 27% YoY. Software licensing revenue fell 65% YoY to RM7mn. This was mainly due to the progression of actual project delivery varying from quarter to quarter, resulting in a lag in revenue contribution. However, this was offset by software project services revenue increasing 6% YoY to RM26mn as there was additional revenue recognised from recently closed contracts from countries such as Thailand, UAE, and Malaysia. In addition, progressive project revenue recognised from on-going secured projects remained at a stable level.

Collaboration with Siam Commercial Bank

In December 2022, Silverlake announced an agreement with Siam Commercial Bank (SCB), one of Thailand’s top five banks, to deploy an innovative transformation strategy with the use of the MOBIUS platform. MOBIUS was deployed under AutoX, SCB’s microlending arm, and designed to reach Thailand’s unbanked and unbankable population. With the use of MOBIUS, which is available on both hybrid and public clouds as a Software-as-a-Service (SaaS) offering, AutoX was able to deliver new products at a faster speed and lower cost. For example, with MOBIUS, customers were able to submit an unsecured loan application directly online with immediate account opening, credit scoring and funds dispersed. New products can be launched in a few hours by just defining parameters such as loan type, fees, price, etc. Current mainframe core banking software requires the programming of new code to add features or create a new product.

AutoX has a targeted loan portfolio of THB70bn by 2025 – generated from potentially 3,000 sales points. Furthermore, it is on track for its targeted IPO by 2027. We feel that Silverlake has shown the proof of concept and significant reference site for MOBIUS and we could see more inquiries for the rest of 2023.

*Link to Silverlake and SCB’s collaboration: https://www.silverlakeaxis.com/img/pdf/newsletter_Jan23.pdf

Potential for replacing core banking systems

Fidelity National Information Services (FIS), which provides core banking systems, has 5-6 banks with core banking systems in the region approaching their end-of-life by end 2023. This presents an opportunity for MOBIUS. Silverlake can offer MOBIUS as a core cloud banking system to these banks. Previously, it was hard to move a bank away from its existing core banking system as it was too costly and time-consuming to switch to a brand new core. However, with these banks existing core banking systems reaching expiration, Silverlake would be able to promote MOBIUS as a core without the previous limitations. We feel that this could provide a big boost to Silverlake as banks start to move from a traditional core to a fully cloud based core. Cloud reliefs the bank of many security challenges at scale and SAAS provides continuous updates with less costly upfront licensing.

Creating opportunities in Malaysia

In March 2023, Amazon Web Services (AWS) revealed an investment of US$6bn into Malaysia and the launch of an infrastructure region. Silverlake is currently an AWS partner and uses its cloud infrastructure for MOBIUS. With the development of infrastructure in Malaysia, Malaysian banks would be more likely to collaborate with Silverlake for either an upgrade to MOBIUS or to utilise it to expand its digital capabilities.

Outreach to smaller regional banks

As MOBIUS is cloud native, Silverlake is able to run a multi-tenanting platform, where several banks share the same cloud platform but are differentiated by their own passwords and security. In a way, this is like a building with multiple tenants, and each has his own “house” with keys to access the data and information. This is much more cost effective and products are released faster, which allows smaller banks to compete with the bigger players who would take months to configure and release a product. We feel that this would allow MOBIUS to reach smaller players who would otherwise not have the opportunity to use such a system.

Investment Actions

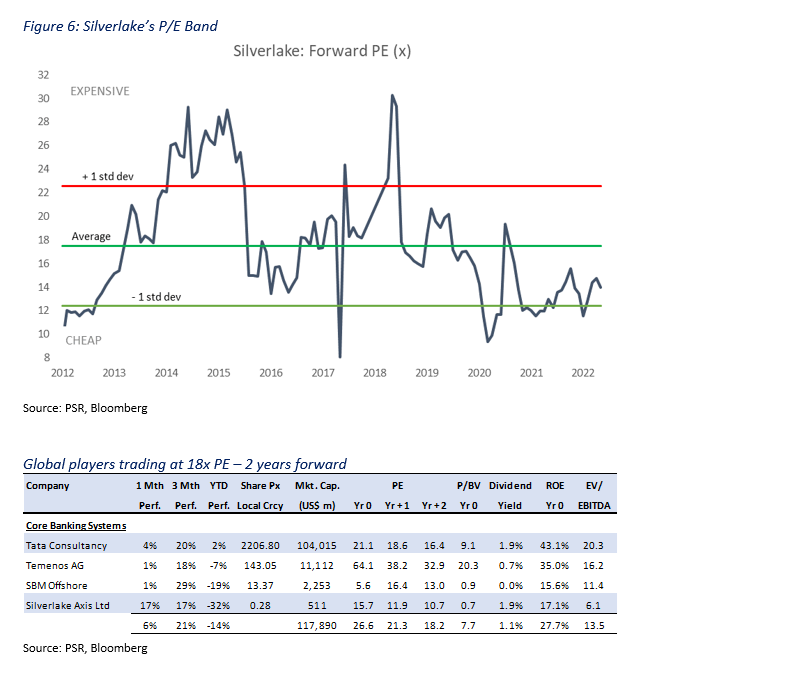

We maintain a BUY rating on Silverlake Axis Ltd with an unchanged target price of S$0.49. Our FY23e estimates remain unchanged. Our target price is pegged to 20x P/E FY23e. It is at 20% discount to peer valuations of around 25x PE (Figure 1).

Our target PE of 20x is 8% higher than the historical average PE of 18.5x (Figure 2). In our view, Silverlake should trade at a higher premium to its historical PE with the introduction of MOBIUS and the resumption of bank IT spending after the pandemic.

The Positives

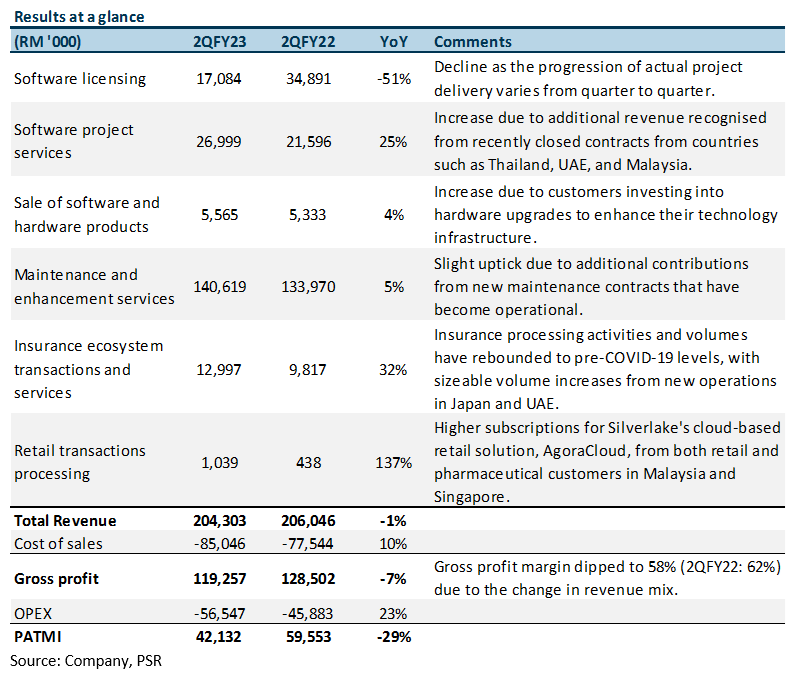

+ Recurring revenue rose 7% YoY. Recurring revenue comprises maintenance and enhancement services, insurance ecosystem transactions and services, and retail transactions processing revenue. Maintenance and enhancement services increased 5% YoY to RM141mn as the dip in enhancement services revenue was more than offset by the increase in maintenance revenue, due additional contributions from new maintenance contracts that have become operational. Furthermore, the decline in enhancement services revenue is temporary as the Group will direct more resources to fulfil their enhancement services contract backlog in 2HFY23. Insurance ecosystem transactions and services revenue increased 32% YoY as volumes have rebounded to pre-COVID-19 levels, with sizeable volume increases coming from new operations in Japan and the UAE. Revenue from retail transactions processing also surged 137% YoY mainly due to higher subscriptions for Silverlake's cloud-based retail solution, AgoraCloud, from both retail and pharmaceutical customers in Malaysia and Singapore.

+ Order backlog healthy. Silverlake has a long track record and a proven client base in Southeast Asia. Three of the 5 largest Southeast Asia-based financial institutions use its core banking platform, and it has largely retained all its clients since bringing them on board its platform. Silverlake’s project pipeline is healthy, at RM1.8bn (1QFY23: RM2.1bn), with an order backlog of RM275mn on the verge of closing in 3QFY23. Silverlake is beginning to close more deals and is witnessing an uptick in inquiries about its financial services market solutions and capabilities.

The Negatives

- Project-related revenue fell 22% YoY. Software licensing revenue fell 51% YoY to RM17mn. This was mainly due to the progression of actual project delivery varying from quarter to quarter, resulting in a lag in revenue contribution. However, this was offset by software project services revenue increasing 25% YoY to RM27mn as there was additional revenue recognised from recently closed contracts from countries such as Thailand, UAE, and Malaysia. As for the ongoing implementation of two new MOBIUS contracts secured in FY22, one has been completed and went live in 2QFY23 while the other is near completion and will be entering maintenance mode sometime in mid-2023.

The Positives

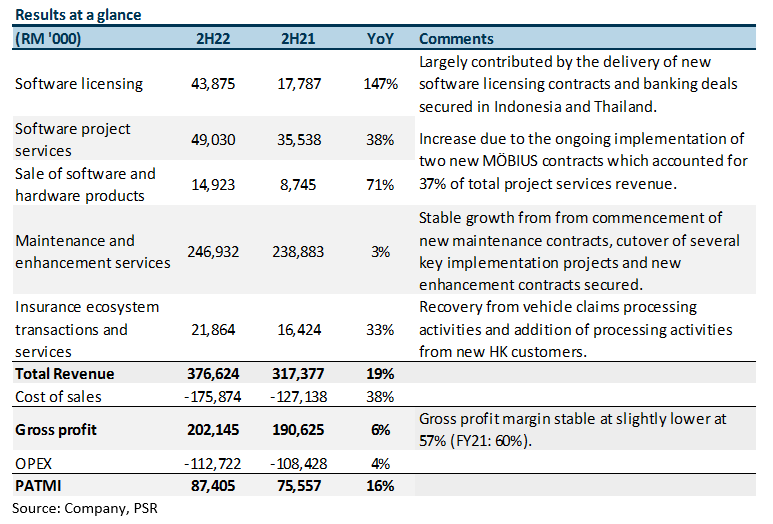

+ Project related revenue increased 66% YoY. Software licensing revenue increased by 110% YoY to RM84mn largely contributed by the delivery of new software licensing contracts and banking deals secured in Indonesia and Thailand. Software project services revenue increased 39% YoY to RM91mn mainly due to the ongoing implementation of two new MOBIUS contracts, which accounted for 37% of total project services revenue. Progressive revenue came from other ongoing projects.

+ Stable recurring revenue growth. Maintenance revenue grew 8% YoY while enhancement services revenue grew 2% YoY. The increase was from the commencement of new maintenance contracts upon completion and cutover of several key implementation projects as well as new enhancement contracts secured from customers. Insurance ecosystem transactions and services revenue also increased by 15% YoY as vehicle claims processing activities recovered. The addition of processing activities from new Hong Kong customers upon completion of system integration also contributed positively.

+ Record order backlog. Silverlake has a long track record and a proven client base in Southeast Asia. Three of the 5 largest Southeast Asian based financial institutions use its core banking platform, and it has largely retained all its clients since bringing them on board its platform. Silverlake’s project pipeline is healthy, at RM1.9bn, with a record-high order backlog of RM570-600mn. Silverlake is beginning to close more deals and is witnessing an uptick in inquiries about its financial services market solutions and capabilities.

The Negatives

- Lower GP margins in FY22. Gross margin was lower in FY22, at 57% compared with 60% in FY21. This was mainly due to higher provisions taken for bonus pay-outs in FY23. Management also said that there was a higher percentage of hardware sales, which usually has a lower GP margin.

Company Background

Silverlake Axis Ltd provides customized software solutions and core banking systems. It provides digital economy software solutions and services to the banking, insurance, payment, retail and logistics industries. To date, it has been the banking solutions provider for 40% of the 20 largest banks in Southeast Asia. As at Dec 2021, the balance sheet is in a net cash position of RM493mn (S$154mn).

Investment Merits

Revenue

Silverlake has several revenue segments: 1) Software licensing (making up 6% of FY21 revenue); 2) Software project services (11%); 3) Maintenance and enhancement services (76%); 4) Sale of software and hardware projects (2%); and 5) Software-as-a-Service (6%).

Software licensing: Silverlake is a digital economy solutions provider to the financial services, retail, and logistics industries. The group’s main products include Silverlake Axis Integrated Banking Solution (SIBS) and Silverlake Digital Banking MÖBIUS Open Banking Platform (SDE). Revenue from software licensing fell 29% YoY in FY21 as customers continue to be cautious in committing to significant new software licensing deals in the first 3 quarters of FY21. Significant new software licensing deals began to pick up in 4Q21 and it is anticipated that this will continue through to FY22.

Software project services: Silverlake’s software project services business is related to the provision of software customisation and implementation services to deliver the core banking, payment, and retail solutions. Software project services revenue declined 12% YoY in FY21 as several key projects were completed, nearing completion or delayed due to client requests. Nonetheless, the decrease in FY21 was mitigated by smaller scale contracts for SIBS technology refresh contracts secured in Malaysia in 2H20 and new MÖBIUS and banking implementation contracts secured in Sri Lanka, Thailand, and Malaysia in 2H21.

Maintenance and enhancement services: This segment is where Silverlake provides round-the-clock software support services as well as enhancement services to support its customers in the delivery and execution of their strategies in making available new capabilities to them. These capabilities can be in the areas of new channels, to augment customer experience and address any new regulatory and emerging governance, risk, and compliance requirements. This segment recorded a growth of 10% YoY in FY21 due to new maintenance contracts secured as well as revision of maintenance fees for existing contracts.

Sale of software and hardware projects: This refers to Silverlake’s non-proprietary software and where its acts as a reseller to customers who require bundled one-stop solutions. The Group is an authorised reseller of IBM hardware and system software in Malaysia. Hardware sales are seasonal by nature and dependent on the requirements and specifications to support the implementation of new or enhancement of existing systems. This segment declined by 60% YoY in FY21, and the lower sales were due to the deferment of capital expenditure during the pandemic period as well as they wait for the launch of the latest IBM iSeries in September 2021.

Software-as-a-Service: This segment consists of insurance processing, where Silverlake’s Merimen built platform processes insurance claims and premiums, and retail, and where Silverlake is a cloud-based SaaS solution provider in the retail industry. Software-as-a-Service revenue for Insurance processing was flat in FY21 while Retail processing grew 47% YoY in FY21 as the Group pivots to SaaS offerings to the larger SME market.

Expenses

The cost of sales fell 12% YoY in FY21, which was in line with the drop in revenue. Operating expenses include selling and distribution costs (15% of total operating expenses), administrative expenses (79%) and finance costs (6%). Selling and distribution costs fell 9% YoY in FY21 as a result of cost control measures during the pandemic period. Selling and distribution costs include staff costs and Silverlake has a total of 2,076 employees in FY21. Expense categories remain largely unchanged over the last 3 years. Notably, Silverlake spent 4% of FY21 revenue (~RM25mn) on research and development.

Margins

Gross profit margin improved from 57% in FY20 to 60% in FY21 mainly due to better margins generated from software project services as well as maintenance and enhancement services in FY21.

Net profit margin fell from 28% in FY20 to 23% in FY21 mainly due to non-operational losses of RM15.6mn and RM8.6mn from remeasurement of put liability for put option and remeasurement of derivative asset in relation to call option on the remaining 20% equity interest in XIT Group respectivly.

Balance Sheet

Assets: Cash and bank balances fell by 16% in FY21 to RM417mn mainly due to the full repayment of their revolving credit line and the cash payment for the acquisition of SISG Group. Intangible assets grew 6% in FY21 to RM317mn mainly due to the capitalisation of software development expenditure incurred on core and digital banking, Fintech and other solutions during the year.

Liabilities: Total liabilities fell 57% in FY21 to RM310mn mainly due to the settlement of the EOC for the acquisition of SISG Group and the full repayment of revolving credit line mentioned above. We expect total liabilities to remain stable as the revolving credit facility has been cancelled.

Cash Flow

Free Cash Flow (FCF) fell 10% in FY21 to RM155mn as operating cash flow fell 6% in FY21 to RM197mn. FCF averaged RM206mn for the past three years. Capital expenditure (CAPEX) fell 10% in FY21 to RM44mn with majority of CAPEX concentrated in Southeast Asia (95% of total CAPEX). Nonetheless, we expect FCF to improve as operating cash flow should increase with the increase in revenue.

Business Model

Silverlake's primary business is the development of core banking and payment processing technologies. The company also makes money from the license fees for its corporate software platforms. Following the completion of projects for customers, Silverlake gets contracts for maintenance and enhancement services, which pay a recurring fee. The maintenance and improvement services are normally recurring for a period of five years and are strongly tied to the installed base of its core banking system.

Silverlake’s recurring revenue from maintenance and enhancement services makes up the bulk of revenue, at 76% of FY21 total revenue. Nonetheless, it has expanded its services, primarily through acquisitions, to provide digital transaction processing in other industries such as retail and insurance.

Silverlake’s flagship product, the core banking system Silverlake Axis Integrated Banking Solution (SIBS), runs primarily on the IBM AS400 (Power Systems) Platform. SIBS offers the full range of commercial banking functions including financing (loans), funding (deposits), remittances, a general ledger module and the Customer Information Facility (CIF). Over the years, Silverlake has broadened its platform capabilities to include a credit card system, internet banking, trade finance, and treasury solutions.

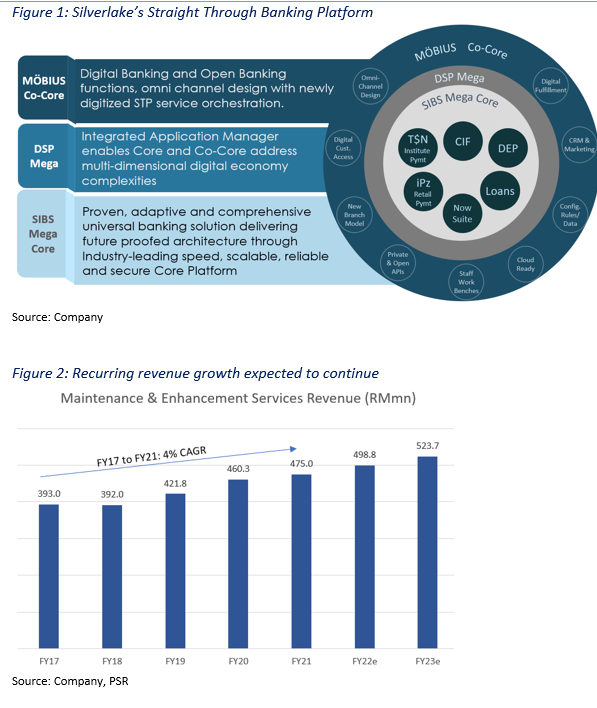

Silverlake has also introduced its Open Banking Platform, MOBIUS, which combines customer-facing digital capabilities with core banking processing capabilities, i.e., SIBS, to create a digital, unified, open end-to-end platform for commercial banking. This means customers can expand their core banking platforms to the MOBIUS platform, thus integrating their systems into one end-to-end banking platform. Furthermore, MOBIUS can be integrated across different core banking systems, without the need to switch to SIBS. Silverlake is able to target both new and existing customers. With MOBIUS being a cloud-based system, the cost is lower than traditional systems which are usually on-site platforms.

Industry

Core banking is evolving to meet the challenges of significant shifts in the banking industry, especially in digital banking. It is essential to provide enabling technologies that increase business agility and reduce operational costs in order to adapt to these changes.

An increasing number of banking segments and geographies are implementing cloud-only core banking system (CBS) strategies. Gartner estimated that 6.5% of core banking commercial off-the-shelf (COTS) CBS installations ran from the cloud in 2020, and this percentage is predicted to increase to 10% by 2023 when public cloud usage will equal private cloud at 5% each. The increased agility and operational excellence that cloud technology may provide to CBS installations have been the main drivers for this rise. Silverlake is able to offer these services with its MOBIUS platform.

Banks are also keener on buying their software, rather than building it. Purchasing software rather than producing it can be more convenient because it eliminates the need for the bank to maintain a software house with current skills and capabilities. The majority of banks with proprietary CBS aim to replace it with COTS applications. This deliberate choice leads to the need to select reliable suppliers that can quickly deploy the CBS, as well as maintain it in the after-sales process.

CBS's services are moving away from being isolated islands of functionality and toward becoming open, collaborative platforms. Banks are rethinking many parts of their business models as a result of digital business, and ecosystems are critical to this. With a digital business, banks can expand their digital business platform model options, connect to new sales channels, boost the variety and value of client interactions, and link to new sales channels.

Gartner notes that the number of net new deals for core banking replacement increased in 2021, despite the COVID-19 pandemic. There is a growing demand for core banking renewal, driven mainly by digital banking initiatives for which legacy systems prove to be inadequate.

According to Gartner, there are four market leaders. Gartner's Magic Quadrant analysis identified four leaders in the CBS industry. However, vendors whose offerings do not fit Gartner's stated criteria, such as Islamic banking vendors, are excluded from this research, which is why Silverlake was left off the list.

The analysis' main thesis is that this is a highly competitive field dominated by four big corporations. These four companies have a worldwide installation base of between 400 and 800 users. Silverlake, on the other hand, has between 70 and 80 installations worldwide, mostly in Asia.

Market leaders highlighted by Gartner:

Risks

Valuation

We initiate coverage on Silverlake Axis Ltd with a BUY rating and a target price of S$0.38. Our target price is pegged to 20x P/E FY22e. It is an 11% upside to peer valuations of around 18x PE (Figure 7).

Our target PE of 20x is 15% higher than the historical average PE of 17.5x. In our view, Silverlake should trade at a higher premium to its historical PE with the introduction of MOBIUS and resumption of bank IT spending post pandemic.