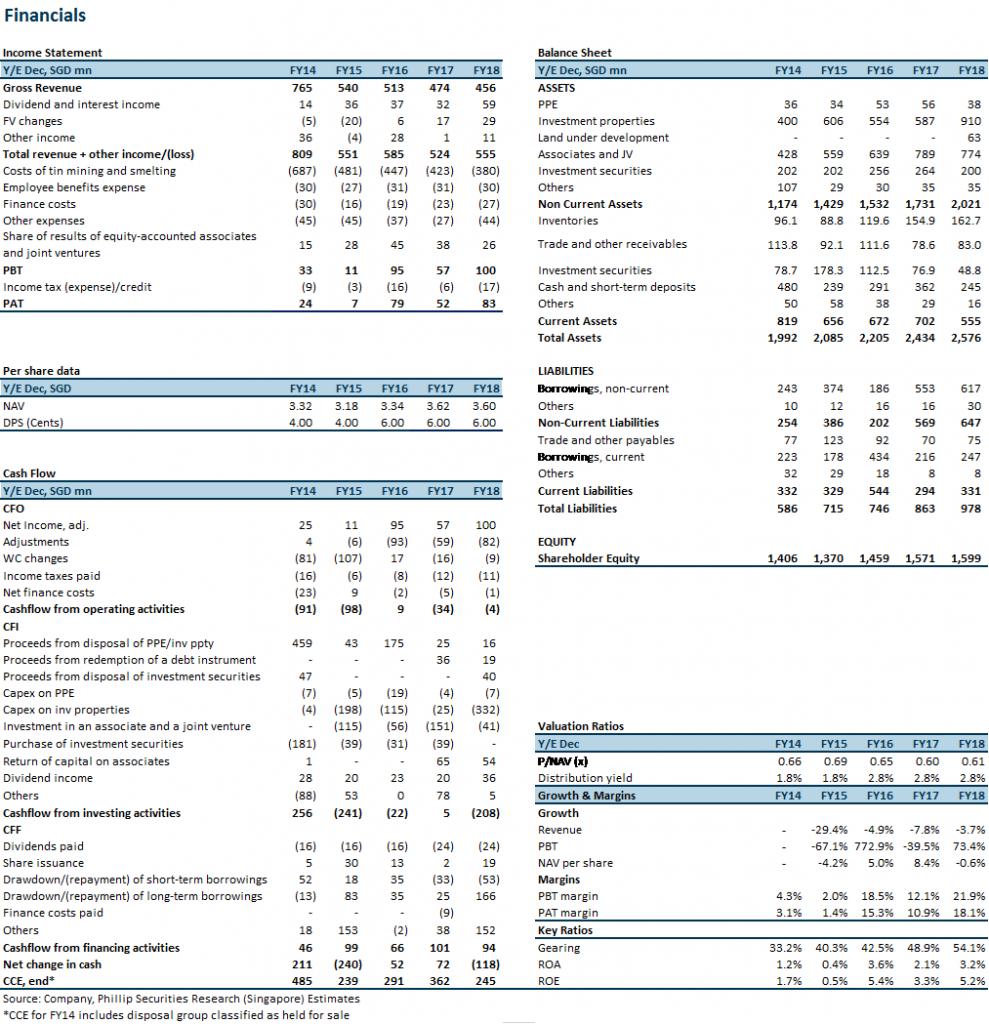

Company Background

The Straits Trading Company (STC) has a history dating back to 1887 when it started out as a tin smelter. In the 1960s, it began developing and constructing multiple prestigious property projects around Singapore. 2008 was a major turning point when privately held investment group, Tecity, acquired a controlling stake in the company. This began STC’s journey of transformation from a mere passive owner of low-yielding assets into an active financial investor and developer of real estate.

STC had since successfully divested S$1bn of non-core assets, refocusing on its resource business and restructured its hospitality operations. It now has three core businesses:

Outlook

BACKGROUND

The Straits Trading Company has a history dating back to 1887 when it started out a tin smelter. Straits Trading formed its property division in 1960. It developed and constructed many prestigious projects around Singapore, including the first iconic 21-storey Straits Trading Building (1972), Great Eastern Centre and China Square Central (2002), and good class bungalows at Cable Road and Nathan Road (2006). 2008 was a major turning point when privately held investment group, Tecity, acquired a controlling stake in the company. This began STC’s journey of transformation from a mere passive owner of low-yielding assets into an active financial investor and developer of real estate.

Figure 1: STC’s three core pillars are real estate, hospitality and resources

Source: Company. * Aggregate interest in Suntec REIT held by STC Group of companies

REAL ESTATE

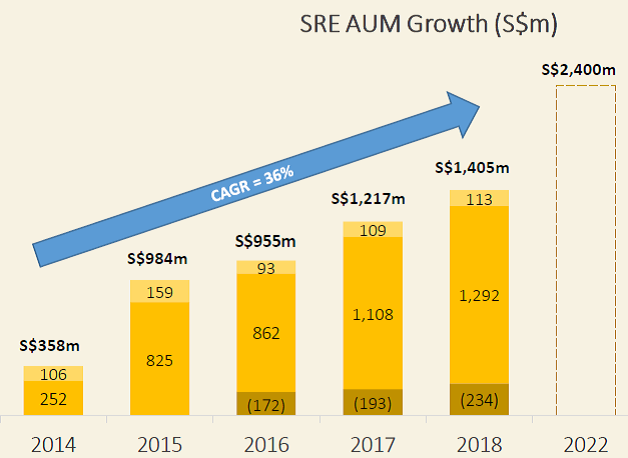

1. Straits Real Estate (89.5%): This is STC’s in-house real estate investment business. The remaining 10.5% is owned by the John Lim Family Office. The objective of SRE is to build a geographically diversified portfolio of property assets that will generate attractive recurrent earnings or returns and capital upside. It may invest directly in real estate or via real estate funds. SRE’s modus operandi is to invest in projects with value-add opportunity and manage them to drive capital upside. Operating since 2014, SRE has been building its scale and track record. Assets under management have grown at a 36% CAGR from S$358mn in 2014 to S$1.4bn in 2018 (Figure 8). 114 William Street (Melbourne) is an example of a property that SRE invested in and enhanced, eventually increasing its occupancy and WALE, repositioning it as an institutional-grade asset for sale. SRE later successfully monetised it for a profit of A$21.7, at an IRR of 25%. Another successful investment was the divestment of the Greater Tokyo Office Fund, with its four office buildings, for an IRR of 19%. The direct real estate portfolio of SRE is now spread across three key geographies – namely, Australia, Japan and China. There are also three property funds under SRE that invest in Japan, Malaysia and Australia.

Figure 2: 320 Pitt Street, Sydney

Source: Company

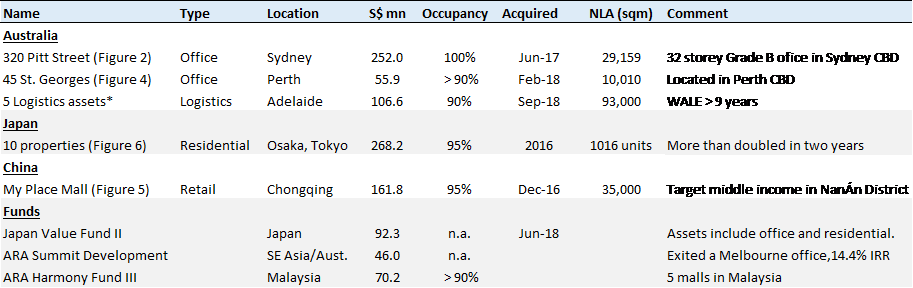

Figure 3: SRE portfolio of direct investments and funds

Source: Company *SRE ha 80% stake in five assets. Tenants include Coca-Cola Amatil, Incitec Pivot Centre and Siemens

Private Equity Funds

ARA Harmony Fund III (40%): owns a portfolio of five commercial properties in Malaysia. The income-generating properties include Ipoh Parade Mall in Perak, Klang Parade Mall and Citta Mall in Selangor, 1 Mont Kiara Retail Mall and Office Tower in Kuala Lumpur, and AEON Bandaraya in Malacca.

Japan Value Fund II (40.82%): the objective is to acquire assets in the Greater Tokyo area and other cities in Japan. The fund is managed by Savills Investment Management.

ARA Summit Development Fund (89%) (substantially exited in end 2018): co-invest with developers in projects in South East Asia and Australia. The fund may invest as an equity partner to share a project’s development risk and returns, or participate in a project as a mezzanine loan lender for lower risk.

Figure 4: 45 St Georges Terrace, Perth

Figure 5: My Place Mall, Chongqing

Source: Company, PSR

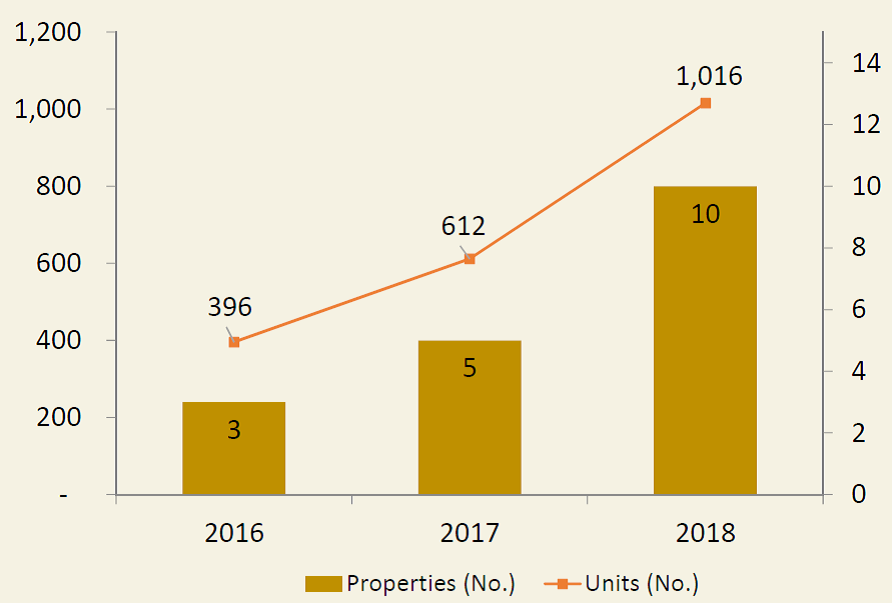

Figure 6: Residential properties in Japan expanded to 1,016 units

Source: Company

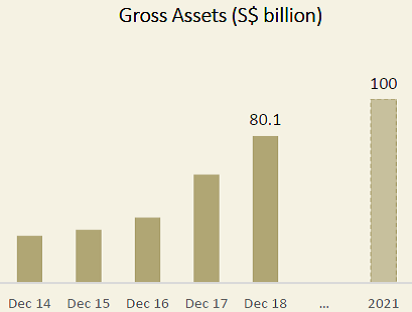

Figure 7: To hit S$100bn AUM by 2021

Source: Company

Figure 8: SRE’s target is to expand AUM by another S$1bn within 4 years

Source: Company

2. ARA Asset Management (20.95%): In October 2013, STC acquired a 20% stake in ARA from Cheung Kong for S$294.4mn. Established in 2002, ARA is one of the largest real estate fund managers in the region with assets under management of S$80bn. ARA was established in 2002 and listed on the SGX in 2007. In November 2016, together with a consortium that included STC, ARA was privatised for S$1.8bn (of 5% equity value to AUM).

Gross assets managed by the ARA Group is currently c.S$80.1bn across over 100 cities in 23 countries. ARA plans to grow gross assets by another S$20bn in the next three years (Figure 7). ARA is focused on the management of REITs, private real estate funds, infrastructure funds and operates country desks in China, Korea, Japan, Malaysia, Australia, Europe and the United States. ARA manages 20 REITs, six of which are listed – these are Fortune REIT, Suntec REIT, Cache Logistics Trust, Prosperity REIT, Hui Xuan REIT and ARA US Hospitality Trust.

3. Suntec REIT (9.8%): STC first acquired a stake in Suntec REIT in 2014. Suntec owns seven assets, four of which are in Singapore, one in Sydney and two in Melbourne. Assets under management is S$9.9bn. STC’s stake in SGX-listed Suntec REIT is recorded as investment securities. STC recognises dividend income from this REIT.

4. Singapore and Malaysia properties available for sale (100%): A S$317mn portfolio of legacy investment properties in Singapore and Malaysia is available to be monetised and for capital to be redeployed towards. These include (i) apartments/ townhouses in Gallop Green development; (ii) good class bungalows in Cable and Nathan road; (iii) several parcels of land and shophouses in Malaysia.

HOSPITALITY

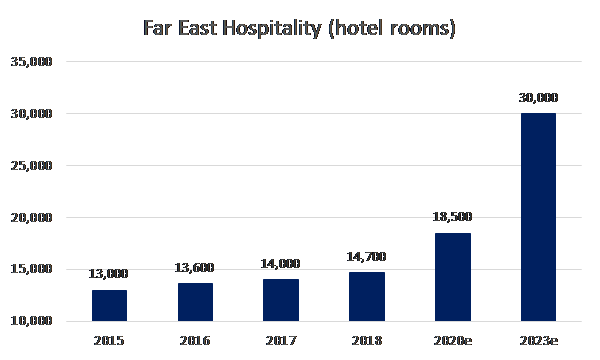

Far East Hospitality Holdings (FEHH) (30%): In November 2013, STC formed a 30:70 joint venture, FEHH, with SGX-listed Far East Orchard. STC injected three hotel properties and 13 management contracts into this joint venture. FEHH currently owns and operates a combined portfolio of 94 properties with over 14,700 rooms across seven countries and 25 cities. FEHH also operates nine hotel brands such as Rendezvous, Oasia, Quincy, Village, Far East Collection, Adina Apartment Hotels and Adina Serviced Apartments, Vibe Hotels, Travelodge Hotels and TFE Hotels Collection. Targets to double the rooms under management from 14,700 to 30,000 in 2023.

Figure 9: Far East room count target is to double in five years

Source: Company, PSR

RESOURCES

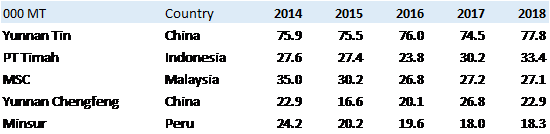

Malaysia Smelting Corporation (MSC) (54.8%): MSC is the largest tin mining company in Malaysia and the third largest globally, in terms of output (Figure 10). The company is listed on both Bursa Malaysia and SGX.

MSC’s end-product is refined tin bars. It has a tin mine in Perak - Rahman Hydraulic - with an annual production of around 2,300MT per annum. It is considered the largest operating open-pit hard rock tin mine in Malaysia (Figure 14). Tin ore extracted from this mine is processed into tin-in-concentrates which are then converted into refined tin metal products at the smelter in Butterworth, Penang. The mine meets 10% of MSC requirements, with the remaining raw materials sourced locally or overseas.

Figure 10: Top 5 largest tin producers in the world

Source: International Tin Association, PT Timah, PSR

Figure 11: The nine brands under Far East Hospitality Holdings

Source: Company

Figure 12: The newly opened 606 room Village hotel at Sentosa

Source: Company

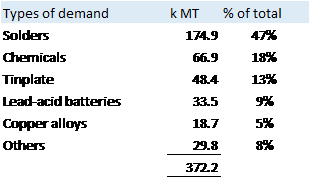

Figure 13: Types of demand for tin (2018)

Source: ITA, PT Timah, PSR

Figure 14: Rahman Hydraulic operates largest open pit tin min in Malaysia

Source: Company

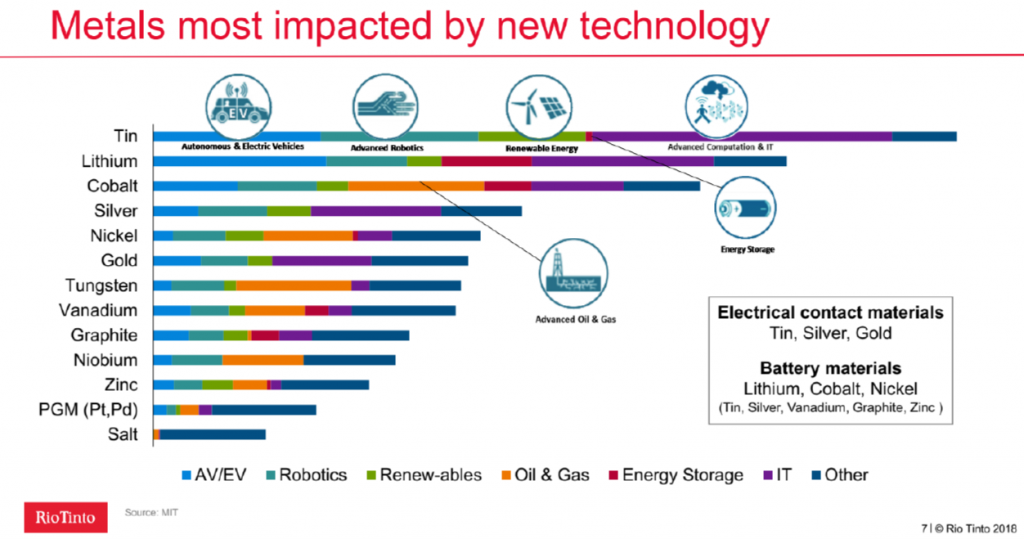

Figure 15: Tin would be the most positively impacted metal by new technologies

Source: Rio Tinto

MSC will be relocating from its current plant in Butterworth (operational since 1902) to a new smelter in Pulau Indah, Port Klang. The new facility will be using a more efficient smelting process - Top Submerged Lance furnace. The new plant will boost maximum production capacity by 50% or up to 60,000 tonnes p.a.

In view of the relocation, MSC and STC signed a Memorandum of Understanding (MOU) to jointly redevelop a 40.1 acre land site comprising the current factory land (13.9 acres) and adjacent land (26.2 acres) into a integrated waterfront development. The site is freehold and is near the new Penang Sentral, which will be the new transport hub of Penang (Figure 16).

Figure 16: The upcoming mixed-development (~RM3bn GDV) is near the new Penang Sentral transport hub

Source: Company

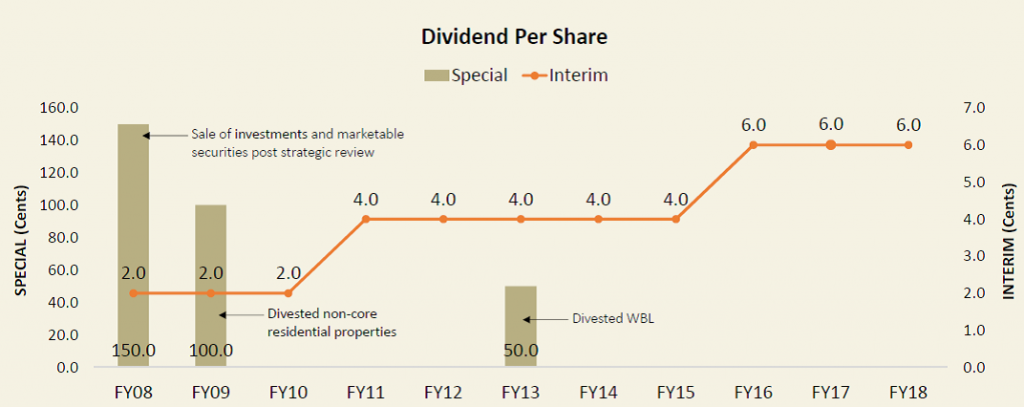

Figure 17: Dividend per share has tripled since 2008

Source: Company

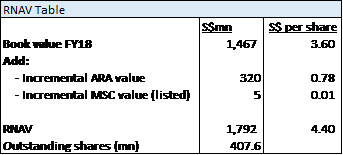

RNAV

Our RNAV of STC is S$4.40 (Figure 18).

Figure 18: STC RNAV Estimates

Source: Company, PSR

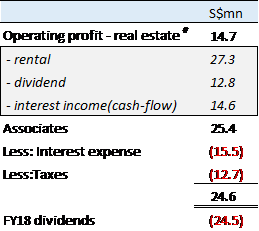

Figure 19: FY18 recurrent income of around S$25mn from the real estate

Source: Company, PSR

#Excludes income from resources business where net profit was S$6.7mn.

Our estimate of real estate operating profit is S$46mn less implied fair value gain within interest income of S$31.3mn.

*Based on data provided in 22Mar19 Circular on Capitaland acquisition of Ascendas and Singbridge. Some of the equity to AUM valuations used were Blackstone 4.8% and Cohen and Steers 3.2%. Incidentally, ARA was privatised at 5% equity to AUM or PE of 17.9x.

APPENDIX 1: Understanding the financials

Revenue

STC has multiple sources of revenue and income.

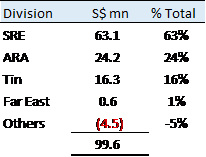

Figure 20: PBT break-down (2018)

Source: Company, PSR

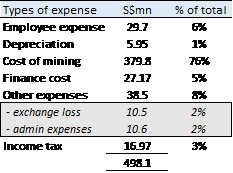

Cost

Biggest component of operating cost relates to the tin mining operations. Excluding mining cost, the largest expense are employee and finance costs (Figure 21).

Figure 21: Expense breakdown (2018)

Source: Company, PSR

Balance Sheet

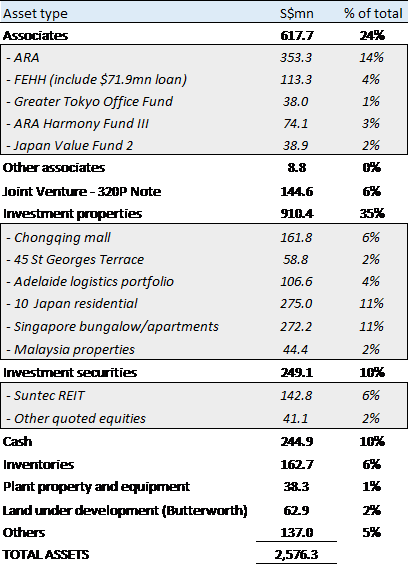

Assets: Around one-third of STC’s assets are investment properties. The largest investment properties are the Singapore bungalows and apartments, and the 10 Japan residential apartment blocks, followed by the associates -the single largest asset being the 21% stake in ARA (Figure 22).

Figure 22: Break-down of total assets

Source: Company, PSR

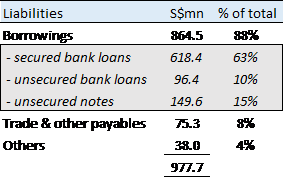

Liabilities: STC’s gross debt is around S$864.5mn. Bulk of the debt is secured bank loans. The interest rates are 0.5% to 5.2% for floating rate debt and 3.7% for fixed rate notes.

Figure 23: Bulk of the liabilities are secured bank loans (as at FY18)

Source: Company, PSR