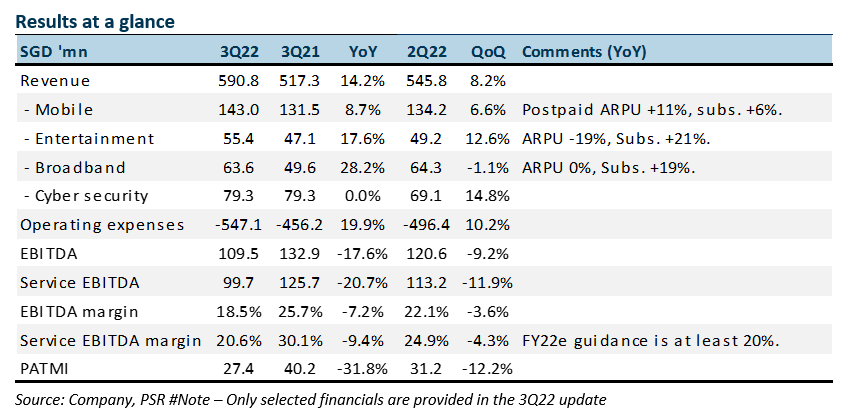

The Positive

+ Volume and price rebound in mobile revenue. 3Q22 mobile revenue rose 8.7% YoY, the fastest rate of growth since FY07. The rebound in ARPU from roaming was expected as borders re-open but the rise in subscribers by 26,000 was above expectations. Subscriber growth was from no-contract SIM-only giga! plans.

The Negative

- Surge in operating expenses. 3Q22 operating expenses jumped almost 20% YoY to S$547mn. Higher cost from EPL content and IT investments. These costs are expected to continue into 4Q22 as part of the DARE+ transformation roadmap.

Outlook

Management lifted FY22e revenue guidance by 2-5% points to 12-15% revenue growth (PSR +11.8%). Capex for FY22e was also lowered by 2% points to 5-7% of revenue, but the service EBITDA margin was unchanged at least 20% (PSR: 20.6%). This implies a 14% margin in 4Q22. Higher costs in 4Q22 will stem from marketing and promotion, especially for the World Cup and new services in 2023 plus the full impact of EPL content cost. There are possible write-offs from the Strateq healthcare business and legacy IT systems.

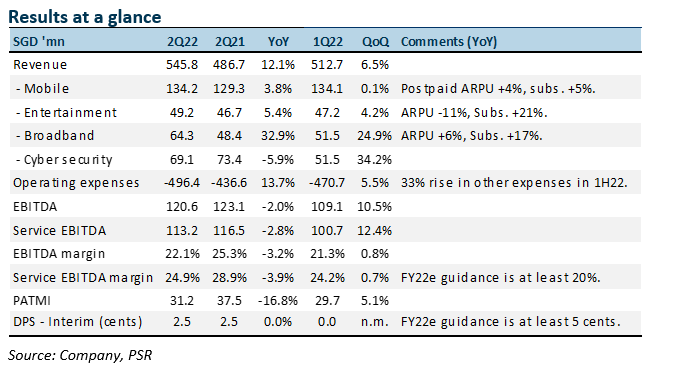

The Positive

+ Exceeds guidance in multiple areas. 1H22 performance exceeded management FY22 guidance. Revenue growth (at least 10%), service EBITDA margin (at least 20%) and CAPEX (12-15% of revenue) were higher in 1H22. However, there was no change in guidance implying a much weaker 2H22. Dividend of 2.5 cents per share was within the FY22e guidance of at least 5 cents.

The Negative

- Costs start to build. Operating cost has started to climb faster. 2Q22 operating expenses increased 14% YoY to S$496mn. The bulk of the cost increase was in other operating expenses (IT outsourcing, license fees, utilities), EPL marketing and broadband acquisition. The cost is part of the DARE+ transformation plan to invest in a new revenue stream and cost savings.

Outlook

There was no change in FY22e guidance by management. We expect EBITDA margins to drop significantly from 24.6% in 1H22 to 17.4% in 2H22. Our FY22e service EBITDA margin is 20.9% vs management guidance of at least 20%. Operating expenses are expected to rise further in 2H22 from IT outsourcing, EPL content, software licensing and 5G wholesale cost. Unless roaming revenue gains further momentum or new revenue (not fully disclosed) begins to contribute meaningfully following the DARE+ investments, earnings will be sluggish in 2H22.

Maintain ACCUMULATE with an unchanged TP of S$1.35

Our target price is based on regional peers’ 8x FY22e EV/EBITDA.