Sheng Siong Group Ltd – Surge in new stores

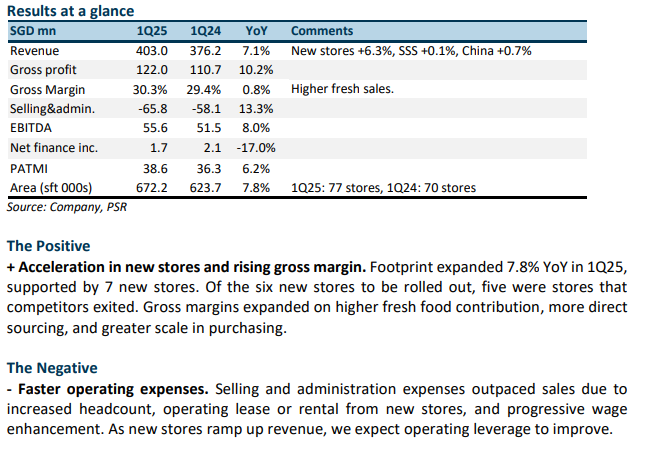

- 1Q25 results were within expectations. Revenue and PATMI were 26%/26%, respectively, of our FY25e forecast. PATMI rose 6% YoY from the 7.8% YoY increase in-store footprint and expansion in gross margins.

- Sheng Siong (SSG) is on track to open at least 8 new stores in FY25 (~10% in footprint). This is the 2nd largest expansion of stores since the 10 in 2018. The major difference is the current expansion is largely due to competitors exiting stores.

- We lift our FY25e revenue and earnings forecast by 2% from the higher number of expected stores. Our target price is increased to S$1.89 (prev. S$1.76) from a higher earnings estimate and PE ratio. Historical PE is 18x, but we nudge the target ratio to 19x as growth accelerates. Our ACCUMULATE recommendation is maintained. Growth rate is rising from the jump in new stores and steeper market share gains. Higher wages from the progressive wage model will weigh down operating margins.

Sheng Siong Group Ltd – Rising market share

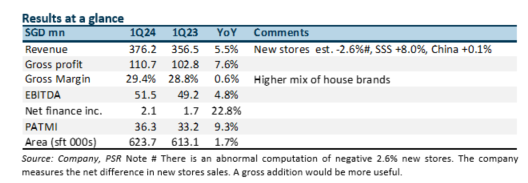

- FY24 results were below expectations. Revenue/adj.PATMI were 98%/97%, respectively, of our FY24e forecast. Staff costs jumped 14% YoY to S$56.6mn in 4Q24. The progressive wage model is causing wage levels across roles in the store to continue climbing.

- Sheng Siong (SSG) added two stores in 4Q24, bringing the total to 75. Two more new stores have been opened this year, and eight more being tendered. Several HDB stores have been secured from competitors who have relinquished them in matured estates.

- We lowered our FY25e forecast by 4% to S$147.3mn. The rise in staff costs has been more severe than expected. FY25 will be the final year of the progressive wage model increases for the retail sector. We raised our target price to S$1.76 (prev. S$1.74) as we rolled over valuations to FY25e earnings. Our ACCUMULATE recommendation is maintained. The store openings for SSG are accelerating, further boosted by competitors reducing their footprint of supermarkets in HDB estates. Over the past 2 years, SSG’s revenue growth has been 4%-5% points p.a. faster than the industry.

Sheng Siong Group Ltd – More stores and margin expansion

- 9M24 revenue met our expectations, but PATMI exceeded at 75%/79% respectively of our FY24e forecast. Progressive wage reimbursement and gross margins were higher than expected. Gross margin was a record 31.3% in 3Q24 from higher fresh product contribution and margins.

- In 3Q24, Sheng Siong opened two new stores in Singapore, bringing the total to 73 (or +1.4% expansion in space). Another new store opened in October, and Toa Payoh store acquisition is pending completion by the end of this year. Furthermore, five new stores are waiting for their tender results from HDB.

- We raised our FY24e forecast by 5% to S$145.8mn. Our ACCUMULATE recommendation is maintained, and the target price has increased from S$1.66 to S$1.74, based on a historical PE of 18x. Sheng Siong will at least open five new stores in FY24. This will almost triple the average of two new stores per year over the past three years. New stores will provide at least 6% points of revenue growth next year. The unknown has been sluggish in same-store sales of around 2%, which includes the recent GST hike.

Sheng Siong Group Ltd – New stores start to accelerate

- 1H24 revenue and PATMI were within expectations at 49%/50% of our FY24e forecast. Revenue only grew 1.2% YoY in 2Q24. We estimate same-store sales sales contracted in 2Q24 by around 2% points. Gross margins at a new record of 30.9%.

- In 1H24, there were two new HDB stores opened. Another three new stores will be opening in 2H24 with three more pending results of the tender. In addition, seven more tenders are expected to be opened in 2H24. Some of the tenders included several competitor supermarkets closing down stores.

- We maintain our FY24e forecast and target price of S$1.66. Our valuations are based on historical PE of 18x. We forecasted a total of eight new stores in FY24e and FY25e. There is upside to our forecast as more tenders open up. Sheng Siong will face slower growth this year due to a lack of new stores of only three over the past twelve months. Gross margins continue rising to new record levels.

Sheng Siong Group Ltd – Seasonal and base effect bump

- 1Q24 revenue and PATMI were within expectations at 26%/26% of our FY24e forecast. Same-store sales growth accelerated to 3.6% benefitting from the later lunar new year.

- Only one new HDB store was secured in 1Q24. The pipeline is healthy with three stores tenders submitted and another six to be tendered out. The lack of new stores will keep growth muted this year.

- We maintain our FY24e forecast and target price of S$1.66. Our valuations are based on historical PE of 18x. Only two stores were opened last year. The lack of new stores will be a drag on revenue this year. With industry-leading margins, it will be challenging for Sheng Siong to expand further. Supply chain bottlenecks include distribution centres. Another avenue for growth is acquisitions, as the company has built up a record net cash hoard of S$352 million.

The Positive

+ Acceleration in revenue and margins. Same-store sales jumped 8% (effective growth from 63 matured stores is 3.6%). This year, the longer days between Christmas and Lunar New Year provided an additional runway for festive shopping. It was much closer last year, where shopper fatigue can occur. Margins were supported by higher house brand sales, especially the successful rollout of frozen products.

The Negative

- Only one new store was secured this year. Only one new store opened this quarter in Clementi. A positive has been the narrowing number of bidders for the stores. There are now typically three bidders for stores compared to four or five in the past.

Sheng Siong Group Ltd – Lack of new stores

- FY23 revenue and PATMI were within expectations at 99%/99% of our forecast. Revenue growth was 2.1% YoY. Same-store sales contracted and new-store expansion was muted.

- For 2023, Sheng Siong only expanded with two new stores or a footprint growth of 1.7% (2022: +5.4%). The lack of new stores will weigh on revenue growth this year. The company aims to expand a minimum of three stores or equivalent 2.4% expansion per year.

- Same-store sales growth is expected to improve as outbound travel normalises. Inflationary pressure will also support more dining at home. The company has secured two stores so far this year in Singapore, with another ten likely to be tendered. We marginally lower our FY24e earnings by 2%. With a more sluggish growth outlook, we lower our target valuations from historical 20x PE to 18x. The target price is reduced to S$1.66 (prev. S$1.80). Until new stores accelerate, growth will be muted.

The Positives

+ Rise and rise of margins. Gross margins have been on an upward trajectory since listing. A decade ago, gross margins were 23% in FY13 and now stand at 30%. Scale, distribution centre, direct sourcing, and fresh food mix have been the major driver of margin expansion. The new driver is house brands. Competitors have also been raising prices to pass on their cost of production.

The Negatives

- No new stores. There were no new stores this quarter, and only two were opened this year. Expansion in new stores is a cumulative 8% over three years. Before this lull, new stores grew 7-8% p.a. The lack of new stores was due to fewer tenders made available. Of the five stores tendering in 2023, Sheng Siong has been successful in securing three.

Sheng Siong Group Ltd – Same-store sales inching up

- 3Q23 results were within expectations. 9M23 revenue and PATMI were 75%/74% of our FY23e forecast. Despite, the spike in salaries and electricity cost, PATMI grew 6% YoY on improving gross margins and interest income.

- Same-store sales in 3Q23 grew 1.8% YoY, inching up from 2Q23 by 1.5%. We believe the improvement is from market share gains. Visible promotions in the community and a reputation as a cost leader helped push revenue growth.

- We expect higher earnings growth in FY24e from new stores, lower utility costs, increase in same-store sales and interest income. Our FY23e earnings and BUY recommendation is maintained. However, we are lowering our target price to S$1.80 (prev. S$1.98). Historical valuations have been creeping downward from 22x PE to 20x PE. Post- pandemic there has been a de-rating of growth expectations.

The Positives

+ Same-store sales building momentum. We have seen same-store sales turning since 2Q23. Momentum has crept up to 1.8% YoY in 3Q23, from an estimated 1.5% YoY in 2Q23. Same-store sales is rising from market share gains and a jump in population in Singapore.

+New stores recovering. SSG added one new store in Yishun. There are three more stores pending award by HDB. Thereafter, there are another 5 stores in the pipeline by HDB over the next six months.

The Negative

- Operating expenses jumped S$6.1mn YoY. The introduction of a progressive wage model and higher utility costs drove up operating expenses by S$6.1mn (or 10% YoY). Despite higher wages, the number of staff at 3200 is similar to pre-pandemic levels. Utility cost is expected to decline in FY24e.

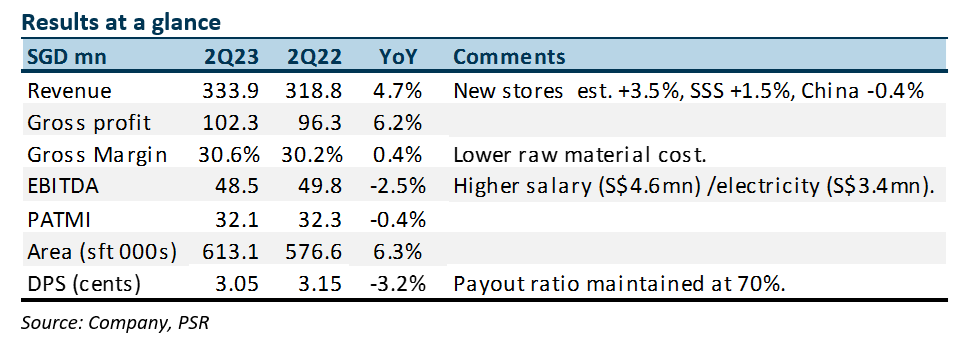

Sheng Siong Group Ltd – Back to revenue growth

- 2Q23 results were within expectations. 1H23 revenue and PATMI were 50%/48% of our FY23e forecast. Despite record gross margins, PATMI was down 0.4% YoY due to a jump in wages and utilities.

- After four quarters of decline, revenue grew 4.7% YoY in 2Q23. We estimate growth was driven by new stores (+3.5% pts) and same-store sales (+1.5% pts).

- New stores, recovery in same-store sales, interest income and higher gross margins will support earnings. But any improvement will be offset by a jump in operating expenses led by utilities and wages. Our FY23e expectations are a modest 1.5% earnings growth. No change to our FY23e earnings and target price of S$1.98, pegged to 22x PE, a 10-15% discount to the 5-year historical average of 25x PE. We upgrade to BUY from ACCUMULATE due to the recent performance of the share prices.

The Positives

+ Same-store sales back to growth. After four quarters of decline, we estimate same-store sales rose 1.5% YoY in 2Q23 (1Q23 -3.6% YoY). We believe market share gains and household budgets returning to home dining drove the improvement in same-store sales.

+Gross margins climb to record levels. 2Q23 gross margins rose to a record 30.6%. The drivers to higher margins were leaner inventory relative to peers (especially in fresh products) and lower purchasing costs. The supply chain was less disrupted and fuel costs were falling. Sales contribution from private labels and fresh is relatively stable as a percentage of sales.

The Negative

- 2Q23 operating expenses jumped 13% YoY. The re-contracting to higher electricity expenses and increased wages, caused operating expenses to rise 13% YoY or S$8mn. Opex to revenue nudged up 1.3% points to 20.1%. Higher wages from the progressive wage model and tight labour conditions will keep fixed costs elevated. An offset will be the lower variable wages or staff bonus.

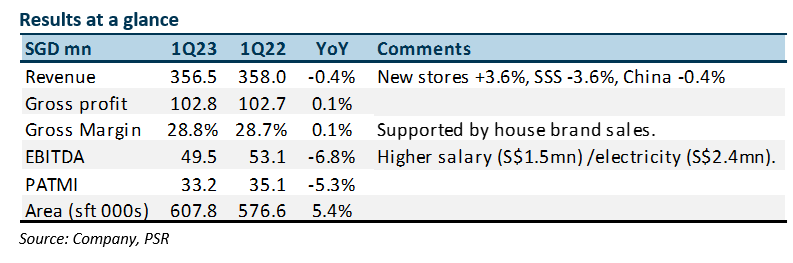

Sheng Siong Group Ltd – Lagged impact from inflation

- 1Q23 results were within expectations. Revenue and PATMI were 26%/25% of our FY23e forecast. PATMI declined 5.3% due to higher operating expenses namely electricity and staff cost.

- Sales were generally stable, despite a 3.6% fall in same-store sales growth. New stores contributed to 3.6% points of revenue growth.

- Revenue growth is still normalising post-re-opening. The weakness in same-store sales has improved from a decline of 3.6% in 1Q23 to 1H22 negative 7.0%. Higher electricity expenses of an annualised S$10mn will be a significant drag on operating margins in FY23e. The offset will be higher interest income. We maintain our FY23e earnings. But downgrade our recommendation from BUY to ACCUMULATE due to the recent performance of the share prices. The target price is maintained at S$1.98. Valuation is pegged to 22x PE, a 10-15% discount to the 5-year historical average of 25x PE. New stores remain the source of growth as tendering activity picks up pace.

The Positive

+ New stores and interest income supported earnings. New stores added 3.6% points of growth to revenue. There was 1 new store added in late March this year and another is under review. Available for tendering by HDB are another 11 stores till 2024. Finance income spiked by S$2.3mn YoY in 1Q23 to S$2.7mn. SSG’s cash hoard is benefiting from higher interest rates. The cash is parked in fixed deposits.

The Negative

- Lagged negative effects of inflation. Electricity expenses increased by S$2.4mn YoY in 1Q23. The new utility rates were signed at the end of last year. The total drag on earnings compared to last year can be an annualised S$10mn. Wages also experienced a S$1.5mn YoY rise in 1Q23, in part due to the progressive wage model but most of the wages are variable.

Outlook

We forecast modest growth in FY23e. The negative same-store sales growth from re-opening and household dining out will filter out for the rest of the year. New stores be the main engine of revenue growth. Gross margin will be supported by increased contribution of house brands and supplier support.

China was a modest 0.4% points drag in sales in 1Q23. Sales declined due to more consumers dining out with the re-opening. The focus is on fresh products and convincing customers to shop away from the wet markets. SSG can be the one-stop shop for all their requirements. Another key focus is building up the pool of human capital to operate the stores.

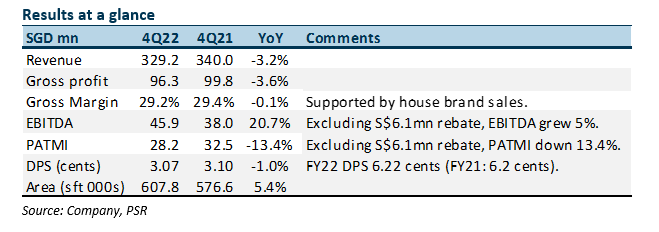

Sheng Siong Group Ltd – New stores, house brands, share gains for growth

- 4Q22 results were within expectations. Excluding a one-off marketing rebate of S$6mn, FY22 revenue and PATMI were 101%/100% of our forecast.

- Sales was supported by the return of new stores. The number of new stores increased by three to 67 and raised retail area by 5.4% in FY22.

- We expect growth in FY23e to be driven by new stores. We model 3 to 4 new stores per year. Our expectations are GP margins will be stable, supported by house brands. With re-opening and dining out, fresh food sales mix may hit the ceiling in the near term. A future catalyst will be China. Contribution is small currently with 4 stores, but we expect a planned roll-out to 15-20 stores to achieve scale. We raised our FY23e earnings by 6% to S$135.4mn on more resilient margins and a higher store count. Our BUY recommendation is maintained. The target price is raised to S$1.98 (prev. S$1.86). Valuation is pegged to 22x PE, a 10-15% discount to the 5-year historical average of 25x PE. The re-opening will have a dampening impact on same-store sales in the near term.

The Positive

+ Back to new stores for growth. There were net 3 new stores in FY22 (4 were opened and 1 closed). In comparison, FY21 saw only 1 store opened. The target remains to open 3 to 5 stores. With HDB ramping up the construction of flats there is more visibility in news stores. There are 13 new stores up for bidding until 1H24. Separately, the average size of the store is also larger with a minimum of 5,000 sft.

The Negative

- Gross margins may hit a ceiling temporarily. 4Q22 gross margins were stable at 29.2%. It remains resilient compared to pre-pandemic levels of around 27%. The ability to raise the mix of fresh food has been the key driver to margin expansion. We believe Sheng Siong has taken market share from wet markets. The next phase of margin expansion will come from house brands. More SKUs are being added.

Get access to all the latest market news, reports, technical analysis

by signing up for a free account today!

Login

The full article is only available for premium content subscribers. To continue reading this article, please log in:

Not a Premium Content Subscriber yet? Sign up here!

- Home >

- Phillip Research Report