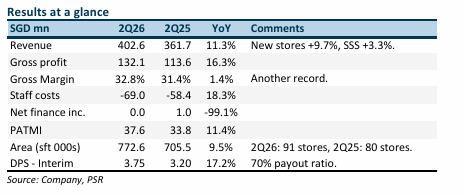

Sheng Siong Group Ltd – Pricey for now

- 1H26 revenue/PATMI were within expectations at 50%/48% respectively of our FY26e forecast. 2Q26 PATMI rose 11% YoY to S$38mn, aided by record gross margins of 32.8% and an additional store footprint of 9.5% YoY. The interim dividend was raised 17% YoY to 3.75 cents.

- Gross margins continue to exceed expectations. FY26e will be the 14th consecutive year of rising margins. The increased mix of fresh products has been supported by strong demand in frozen products. We also believe competition is more benign and pricing more rational.

- We maintain our FY26e earnings. We downgrade our recommendation from ACCUMULATE to NEUTRAL. Our target price is raised to S$3.31 (prev. S$3.16) as we roll over 28x PE valuations to FY27e. Our target price incorporates the peak valuations achieved during the pandemic. Sheng Siong is on track to raise its net store footprint by a slower 5% this year due to the closure of three stores. Operating costs will climb in 2H26 as utility costs are renegotiated. Free cash flow will also reduce as capex on the S$520mn Sungei Kadut distribution centre commences (2026-30).

The Positives

+ Jump in gross margins. Gross margins surged to a quarterly record of 32.8% in 2Q26.

Contribution from fresh products (which require equipment to prolong shelf life) rose to a

new high. Frozen meals and meat have been an area of growth.

+ New stores push revenue growth. The increase in store footprint of 9.5% YoY to 772.6k sft

or 4 stores, despite the closure of one (Elias Mall in Apr26), supported revenue growth. The

revenue per sft of stores was relatively flat at S$1100 despite the larger number of stores.

The Negative

- Nil.

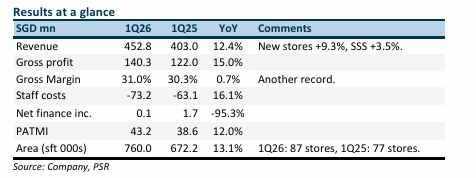

Sheng Siong Group Ltd – Taking more stores and market share

- 1Q26 revenue/PATMI were within expectations at 26%/25% respectively of our FY26e forecast. PATMI grew 12% YoY to S$43mn, supported by margin expansion of 0.7% points and revenue growth of 12.4%.

- 1Q26 marked the third straight quarter of low teens revenue growth. It is the fastest pace in almost five years, or since the pandemic. The store footprint rose by 13% YoY to 760k sft but unchanged QoQ. There are four new HDB stores or 39k sft (+5.2%) secured for FY26e so far. Another 25k pending, excluding potential private real estate transactions.

- We maintain our FY26e earnings and ACCUMULATE recommendation. Our target price is raised to S$3.16 (prev. S$2.82) or 28x PE FY26e, the record levels during the pandemic. We believe Sheng Siong continues to grab market share by taking over competitor stores. However, the expansion in stores this year will be mitigated by the estimated closure of two stores (-3% impact on revenue). The rise in fuel and other costs due to the Middle East conflict is likely to dampen margins in 2H26e.

The Positive

+ Momentum in revenue. Revenue growth of 12.4% was supported by both new stores

(+9.3%) and same-store sales (+3.5%). The jump in same-store sales from 0.4% in 1Q25 was

due to six stores opened in FY24 migrating to the same-store category. The longer period

from Christmas to the Lunar New Year also provided more time for promotions.

The Negative

- Employee costs limit operating leverage. Expansion in operating margins is limited by rising

staff costs. The competitive, tight labour environment and the progressive wage model in

the retail sector continue to place upward pressure on staff costs.

Sheng Siong Group Ltd – More optionality in store openings

- FY25 results were within expectations. Revenue/adj. PATMI was 99/98% of our FY25e forecast. 4Q25 PATMI rose 17% YoY to S$33.4mn. Earnings growth came from 11% rise in revenue, together with record gross margins.

- Sheng Siong (SSG) grew its store footprint by a record 98.4k sft or 12 new stores to 87 in FY25. The new base of stores is generating 10% points of revenue growth in 2H25. It should accelerate to 12% in FY26e. SSG is potentially expanding more aggressively outside the HDB store into retail malls. There have been better terms offered.

- We push up our FY26e earnings by 2%. Our target price is raised to S$2.82 (prev. S$2.55). Our valuation is raised to the higher quartile 25x PE of the 10-year average. Our ACCUMULATE recommendation is maintained. The record number of store openings in FY25 will carry over to revenue and earnings growth in FY26. Another support for earnings is the continuing rise in gross margins, aided by higher sales and greater bargaining power. Opening stores in retail malls is an additional pathway to expand their footprint more quickly.

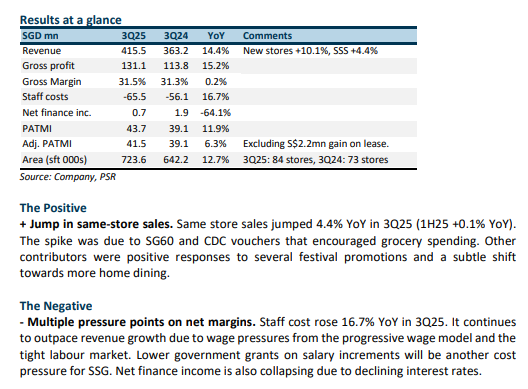

Sheng Siong Group Ltd – More stores, more growth ahead

- 3Q25 results were within expectations. 9M25 revenue and adjusted PATMI were 75%/76%, respectively, of our FY25e forecast. Adjusted PATMI (excluding gain on lease) rose 6.3% YoY to S$41.5mn. Pressuring net margins were higher wages, lower finance income, and a decline in wage grants.

- Sheng Siong (SSG) has grown its store footprint by 13% YoY (or 11 new stores) to 84. Two new stores will open in 4Q25. 2025 will record 10 new stores or an 11% rise in footprint to 736k sft. It will be the largest number of store openings since 2018 and support revenue growth for FY26e.

- We maintain our FY25e forecast. Our target price is raised from S$2.30 to S$2.55 as we roll over valuations to FY26e earnings. We peg SSG to 23x PE, valuations the company enjoyed during its growth years. Our ACCUMULATE recommendation is maintained. The pipeline for new stores remains robust, with opportunities in HDB and private-market locations. However, net margins will be under pressure in the near term from the new S$520mn Sungei Kadut distribution centre and extension of the progressive wage model.

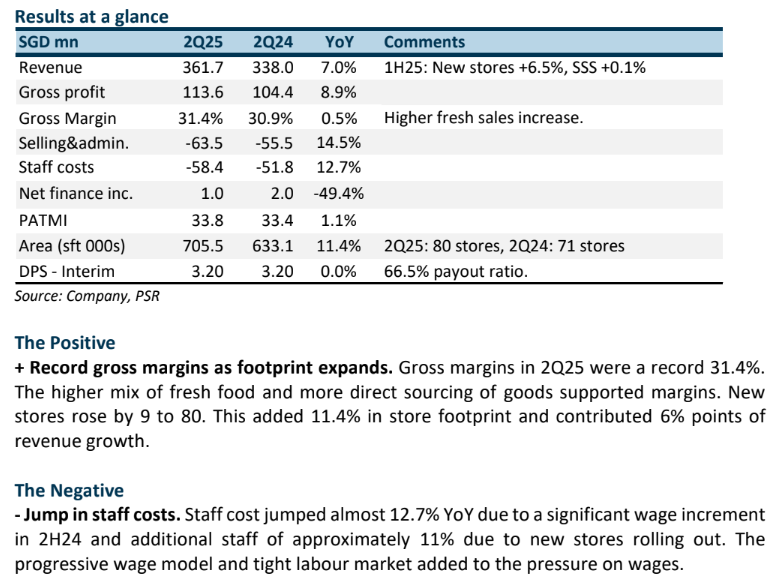

Sheng Siong Group Ltd – Operating leverage will return

- 2Q25 results were within expectations. 1H25 revenue and PATMI were 49%/48%, respectively, of our FY25e forecast. 2Q25 PATMI only expanded 1.1% YoY despite a record gross margin due to a jump in staff costs. Higher wages and new stores are weighing down operating margins in the near term.

- Sheng Siong (SSG) has grown its store footprint by 11% YoY (or 9 new stores to 80). Another three stores will be opened in 3Q25. SSG will end FY25 with at least a 9% rise in footprint. It is the biggest rollout in stores since 2018.

- We maintain our FY25e revenue and earnings forecast. The entire sector is enjoying a re-rating and expansion in the P/E ratio. During the high growth years of 2014-15, SSG’s P/E ratio averaged 23x. As SSG’s growth accelerates, we re-peg SSG's valuation from historical 18x to 23x PE. Our ACCUMULATE recommendation is maintained with a higher target price of S$2.30 (prev. S$1.89). New stores will provide the backdrop for revenue to accelerate. We expect operating leverage to creep in as new store sales pick up and wage growth decelerates.

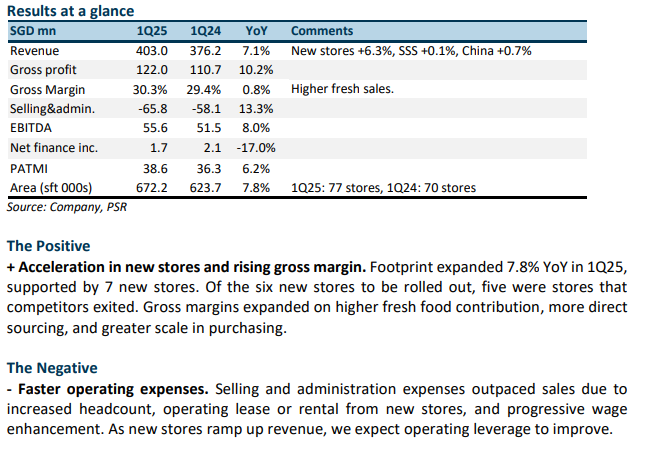

Sheng Siong Group Ltd – Surge in new stores

- 1Q25 results were within expectations. Revenue and PATMI were 26%/26%, respectively, of our FY25e forecast. PATMI rose 6% YoY from the 7.8% YoY increase in-store footprint and expansion in gross margins.

- Sheng Siong (SSG) is on track to open at least 8 new stores in FY25 (~10% in footprint). This is the 2nd largest expansion of stores since the 10 in 2018. The major difference is the current expansion is largely due to competitors exiting stores.

- We lift our FY25e revenue and earnings forecast by 2% from the higher number of expected stores. Our target price is increased to S$1.89 (prev. S$1.76) from a higher earnings estimate and PE ratio. Historical PE is 18x, but we nudge the target ratio to 19x as growth accelerates. Our ACCUMULATE recommendation is maintained. Growth rate is rising from the jump in new stores and steeper market share gains. Higher wages from the progressive wage model will weigh down operating margins.

Sheng Siong Group Ltd – Rising market share

- FY24 results were below expectations. Revenue/adj.PATMI were 98%/97%, respectively, of our FY24e forecast. Staff costs jumped 14% YoY to S$56.6mn in 4Q24. The progressive wage model is causing wage levels across roles in the store to continue climbing.

- Sheng Siong (SSG) added two stores in 4Q24, bringing the total to 75. Two more new stores have been opened this year, and eight more being tendered. Several HDB stores have been secured from competitors who have relinquished them in matured estates.

- We lowered our FY25e forecast by 4% to S$147.3mn. The rise in staff costs has been more severe than expected. FY25 will be the final year of the progressive wage model increases for the retail sector. We raised our target price to S$1.76 (prev. S$1.74) as we rolled over valuations to FY25e earnings. Our ACCUMULATE recommendation is maintained. The store openings for SSG are accelerating, further boosted by competitors reducing their footprint of supermarkets in HDB estates. Over the past 2 years, SSG’s revenue growth has been 4%-5% points p.a. faster than the industry.

Sheng Siong Group Ltd – More stores and margin expansion

- 9M24 revenue met our expectations, but PATMI exceeded at 75%/79% respectively of our FY24e forecast. Progressive wage reimbursement and gross margins were higher than expected. Gross margin was a record 31.3% in 3Q24 from higher fresh product contribution and margins.

- In 3Q24, Sheng Siong opened two new stores in Singapore, bringing the total to 73 (or +1.4% expansion in space). Another new store opened in October, and Toa Payoh store acquisition is pending completion by the end of this year. Furthermore, five new stores are waiting for their tender results from HDB.

- We raised our FY24e forecast by 5% to S$145.8mn. Our ACCUMULATE recommendation is maintained, and the target price has increased from S$1.66 to S$1.74, based on a historical PE of 18x. Sheng Siong will at least open five new stores in FY24. This will almost triple the average of two new stores per year over the past three years. New stores will provide at least 6% points of revenue growth next year. The unknown has been sluggish in same-store sales of around 2%, which includes the recent GST hike.

Sheng Siong Group Ltd – New stores start to accelerate

- 1H24 revenue and PATMI were within expectations at 49%/50% of our FY24e forecast. Revenue only grew 1.2% YoY in 2Q24. We estimate same-store sales sales contracted in 2Q24 by around 2% points. Gross margins at a new record of 30.9%.

- In 1H24, there were two new HDB stores opened. Another three new stores will be opening in 2H24 with three more pending results of the tender. In addition, seven more tenders are expected to be opened in 2H24. Some of the tenders included several competitor supermarkets closing down stores.

- We maintain our FY24e forecast and target price of S$1.66. Our valuations are based on historical PE of 18x. We forecasted a total of eight new stores in FY24e and FY25e. There is upside to our forecast as more tenders open up. Sheng Siong will face slower growth this year due to a lack of new stores of only three over the past twelve months. Gross margins continue rising to new record levels.

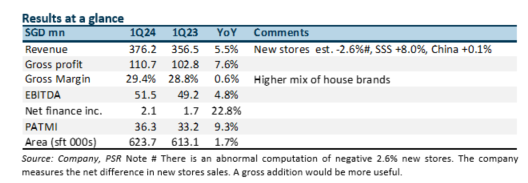

Sheng Siong Group Ltd – Seasonal and base effect bump

- 1Q24 revenue and PATMI were within expectations at 26%/26% of our FY24e forecast. Same-store sales growth accelerated to 3.6% benefitting from the later lunar new year.

- Only one new HDB store was secured in 1Q24. The pipeline is healthy with three stores tenders submitted and another six to be tendered out. The lack of new stores will keep growth muted this year.

- We maintain our FY24e forecast and target price of S$1.66. Our valuations are based on historical PE of 18x. Only two stores were opened last year. The lack of new stores will be a drag on revenue this year. With industry-leading margins, it will be challenging for Sheng Siong to expand further. Supply chain bottlenecks include distribution centres. Another avenue for growth is acquisitions, as the company has built up a record net cash hoard of S$352 million.

The Positive

+ Acceleration in revenue and margins. Same-store sales jumped 8% (effective growth from 63 matured stores is 3.6%). This year, the longer days between Christmas and Lunar New Year provided an additional runway for festive shopping. It was much closer last year, where shopper fatigue can occur. Margins were supported by higher house brand sales, especially the successful rollout of frozen products.

The Negative

- Only one new store was secured this year. Only one new store opened this quarter in Clementi. A positive has been the narrowing number of bidders for the stores. There are now typically three bidders for stores compared to four or five in the past.

Get access to all the latest market news, reports, technical analysis

by signing up for a free account today!

Login

The full article is only available for premium content subscribers. To continue reading this article, please log in:

Not a Premium Content Subscriber yet? Sign up here!

- Home >

- Phillip Research Report