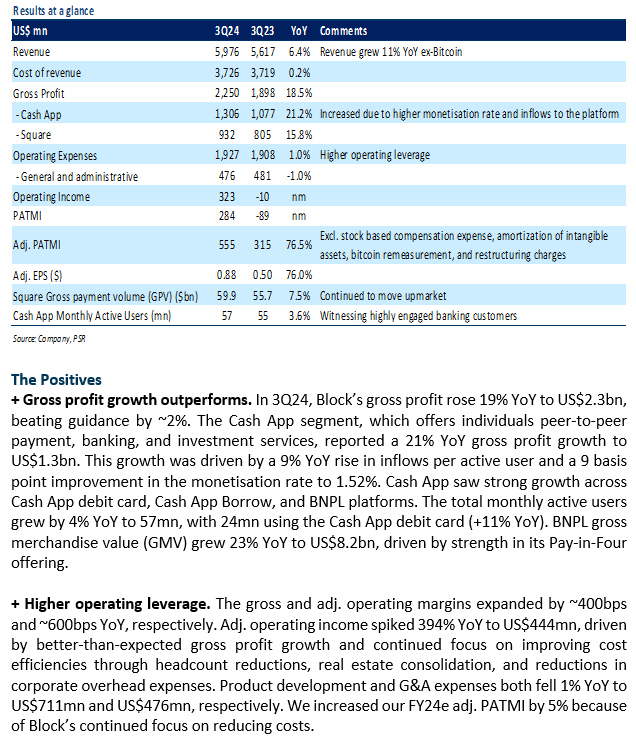

The Positives

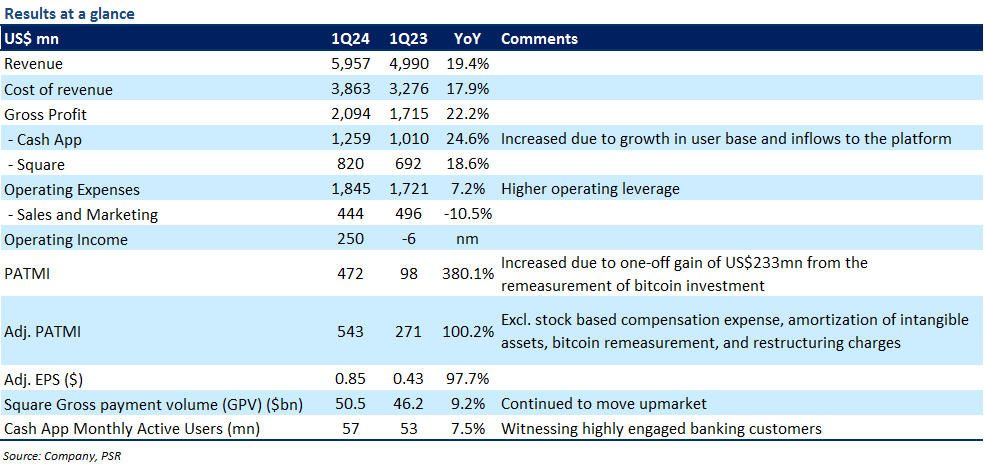

+ Cash App business sees strong growth. In 1Q24, Block’s Cash App segment, which offers peer-to-peer payment, banking, and investment services to individuals, generated revenue growth of 23% YoY to US$4.2bn (ex-bitcoin was up 18% YoY to US$1.4bn) and gross profit growth of 25% YoY to US$1.3bn. The growth was supported by a 7% YoY surge in monthly transacting active users to 57mn, of which 24mn (+20% YoY) used a Cash App debit card. In addition, inflows per transacting active user grew by 11% YoY to US$1,255, leading to wider adoption of its products and services, including ATM withdrawals, bitcoin investments, Cash App Borrow, and Cash App Pay.

+ Strength in Square segment. In 1Q24, Block’s Square segment, which enables merchants to accept payments, reported gross profit growth of 19% YoY to US$820mn (1Q23: 12% YoY) despite the company’s guidance for a slight moderation. The gross profit growth was supported by strength in its banking products (Square Loans and Instant Transfer) and international markets. Meanwhile, Square’s gross payment volume (GPV) grew by 9% YoY to US$50.5bn as consumer spending remained resilient.

+ Cost-cutting measures boost earnings. Block expanded its adj. net profit margin by 4% points YoY to 9%, while adj. PATMI more than doubled to US$543mn. This was mainly because the company continued to focus on improving cost efficiencies through measured hiring (headcount cap of 12,000) and reductions in corporate overhead expenses. Sales and marketing expenses fell by 11% YoY to US$444mn. We raise our FY24e adj. PATMI by 3% on higher operating leverage.

The Negative

- Nil

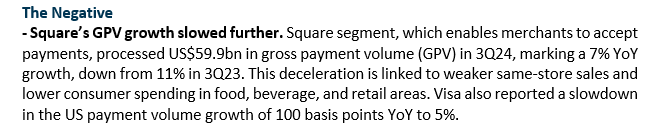

The Positives

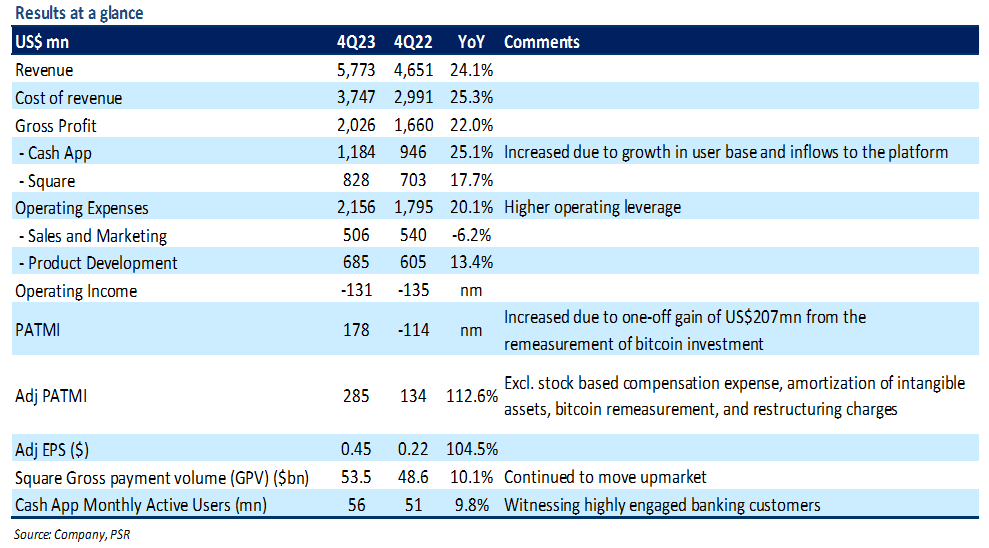

+ Strength in Cash App revenue. Block’s Cash App segment, which offers digital banking and investing services to consumers, reported revenue growth of 31% YoY to US$3.9bn (ex-bitcoin was up 20% YoY to US$1.4bn) and gross profit growth of 25% YoY to US$1.2bn. The growth was mainly driven by a 10% YoY surge in its monthly transacting active users (MAUs) to 56mn led by continued product enhancements and addition of new features like free overdraft coverage and a 4.5% annual interest on savings balances. Block reported a 20% YoY jump in Cash App debit card active users to 23mn. In addition, inflows per active user grew by 8% YoY to US$1,137, leading to increased adoption of its Cash App products and services, including debit cards, ATM withdrawals, investing in stocks/bitcoin, and Cash App Pay.

+ Higher operating leverage. Block expanded its adj. net profit margin by 200bps YoY to 5%, with adj. PATMI also more than doubled to US$285mn. This was mainly because the company continued to show improvements in cost efficiencies as OPEX growth slowed to 20% YoY (4Q22: 45% YoY) – Sales & Marketing expenses were down 6% YoY. Management highlighted that the company met the goal of reducing the number of employees to under 12,000 compared with 13,000 employees as of 3Q23.

The Negative

- Square’s GPV growth further decelerates. Square segment, which enables merchants to accept payments, processed US$53.5bn of gross payment volume (GPV) in 4Q23, an increase of 10% YoY compared to 14% YoY growth in 4Q22. Management highlighted that the severe weather conditions in the US in January had a 3% to 4% moderation in GPV growth, specifically lower in-person discretionary spending within food and beverages and retail categories. Notably, Visa also reported a slowdown in US payments volume growth in January due to cold weather.

The Positives

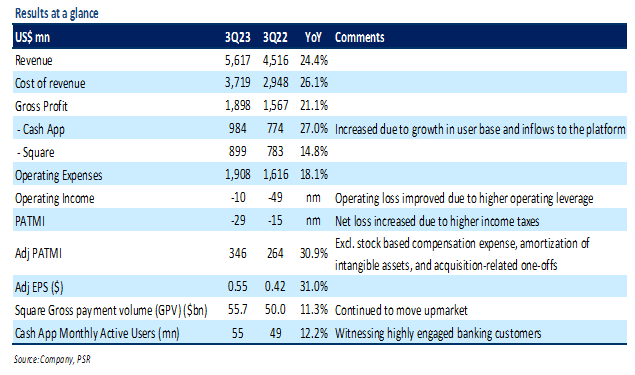

+ Cash App posted robust growth. Block’s Cash App segment, which mainly offers consumer banking products, reported revenue growth of 34% YoY to US$3.6bn and gross profit growth of 27% YoY to US$984mn. Excluding Bitcoin, Cash App revenue grew by 26% YoY to US$1.2bn. The growth was led by 12% YoY growth in monthly transacting active users to 55mn, of which 22mn used a Cash App debit card. In addition, inflows per active user grew by 8% YoY to US$1,132 leading to wider adoption of its products and services, including debit card, ATM withdrawal, and investing in stocks/bitcoin.

+ Focused on improving earnings. OPEX for 3Q23 grew 18% YoY to US$1.9bn compared with 45% YoY growth in 3Q22. The slower OPEX growth is mainly because the management remains focused on cost controls, including headcount reduction, real estate consolidation, and careful discretionary spends like on travel. Management highlighted that the company plans to reduce the number of employees to 12,000 by the end of FY24e compared with 13,000 currently. 3Q23 adj. PATMI spiked 31% YoY to US$346mn driven by higher operating leverage.

The Negative

- Square segment GPV growth decelerated. The Square segment, which provides merchants with payment services, processed US$55.7bn of gross payment volume (GPV) in 3Q23, an increase of 11% YoY compared with 20% YoY growth in 3Q22. GPV growth slowed further in October to 9% due to lower consumer discretionary spending, particularly in food and beverages, and retail categories.

The Positives

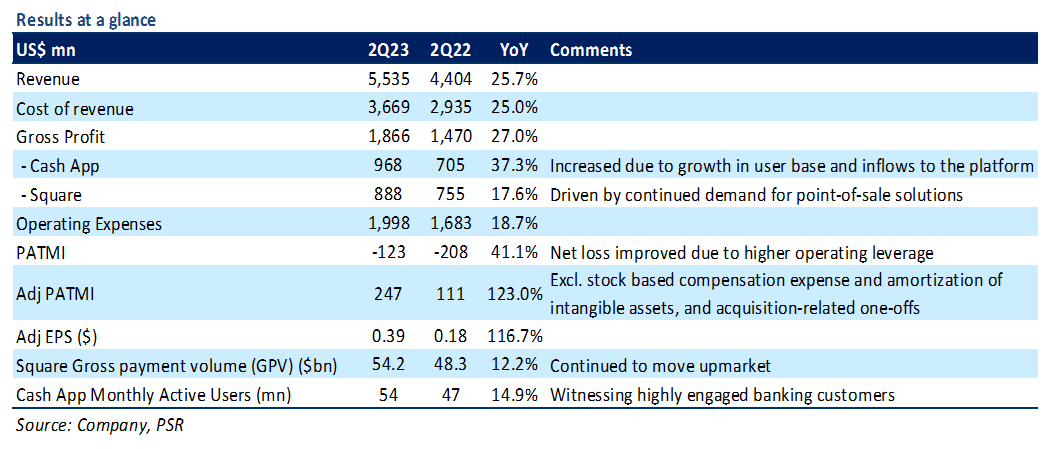

+ Cash App strength continues. Block’s Cash App segment, which offers peer-to-peer payment and consumer banking services, reported revenue growth of 36% YoY to US$3.6bn (39% YoY ex-bitcoin) and gross profit growth of 37% YoY to US$968mn. This growth was mainly driven by 15% YoY growth in Cash App’s monthly transacting active users to 54mn and 8% YoY growth in inflows per transacting active user to US$1,134. The greater inflows led to wider adoption across the Cash App ecosystem, including debit card, crypto trading, tax filing, and direct deposit.

+ Improvements in profitability. The net loss for Block improved by 41% YoY to -US$123mn in 2Q23 compared with -US$208mn in 2Q22. The improvement was mainly driven by higher operating leverage, including careful sales and marketing spend, and lower headcount growth. YoY headcount growth for FY23e is now expected to be below the 10% targeted range earlier this year (vs. 46% growth in FY22).

The Negative

- Deceleration in gross payment volume. In 2Q23, Square’s gross payment volume (GPV) grew 12% YoY to US$54.2bn compared with 17% growth rate in 1Q23 and 25% in 2Q22. Management said that the deceleration was primarily because processing volumes at existing sellers has fallen due to weak trends in global e-commerce and cuts to consumer discretionary spending.

The Positives

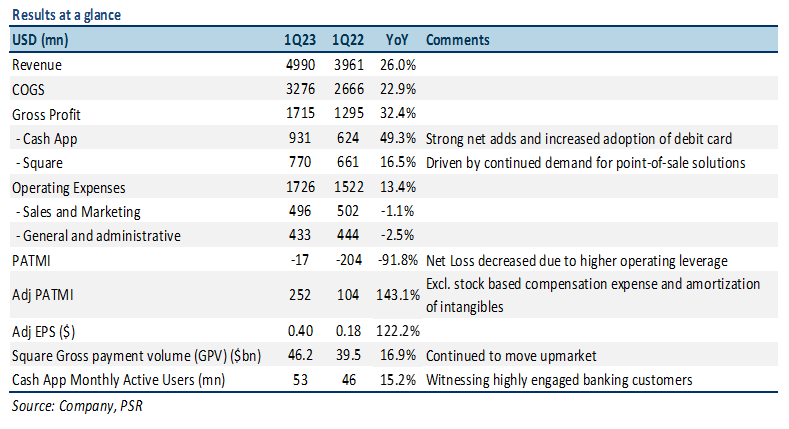

+ Continued momentum in Cash App. In 1Q23, Block’s consumer-facing Cash App segment reported revenue growth of 33% YoY to US$3.3bn (52% YoY ex-bitcoin) and gross profit growth of 49% YoY to US$931mn. This growth was mainly driven by growth in Cash App’s monthly active users (MAUs) (15% YoY to 53mn) and strong engagement led by adoption of the debit card. Additionally, Cash App benefited from strong in-flows driven by growth in monthly direct deposit actives.

+ Focused on expense controls. Operating expenses for 1Q23 grew 13% YoY to US$1.7bn compared with 45% YoY growth in 4Q22 and 70% in 1Q22. The slower operating expenses growth is mainly because the management remains focused on cost controls in FY23e including moderating its headcount growth to 10% (vs 46% growth in FY22) as well as careful sales and marketing spend. Net loss improved to US$17mn in 1Q23 compared with US$204mn in 1Q22.

The Negative

- Slowdown in Square segment GPV. In 1Q23, Square division’s gross payment volume (GPV) grew 17% YoY to US$46.2bn. The growth rate decelerated significantly from 33% in 1Q22 mainly due to weak trends in global e-commerce and cuts to consumer discretionary spending (particularly food/beverage and retail) amid inflationary pressures.

The Positives

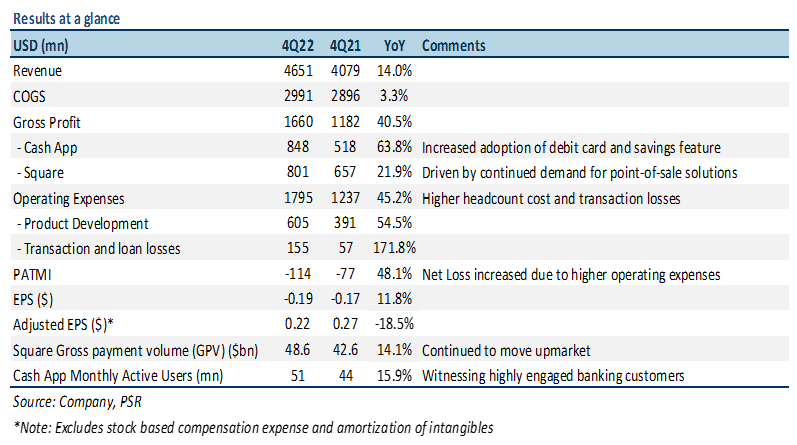

+ Cash App demand remained strong. In 4Q22, Block’s consumer-facing Cash App division reported revenue growth of 12% YoY to US$2.9bn (73% YoY ex-bitcoin) and gross profit growth of 64% YoY to US$848mn. This was mainly driven by strength in Cash App debit card, instant deposit activity, and new savings feature. Cash App’s monthly active users (MAUs) grew 16% YoY to 51mn, with two out of three of those active users transacting on a weekly basis.

+ Square segment remained resilient. In 4Q22, Square division (point-of-sale merchant business) revenue grew by 19% YoY to US$1.8bn and gross profit grew by 22% YoY to US$801mn. The growth was driven by a 14% YoY surge in Square Gross Payment Volume (GPV) to US$48.6bn and increased origination volumes of Square Loans. Mid-market sellers (merchants that generate annualized GPV of >US$500K) accounted for 39% of Square GPV and continued to remain the fastest-growing seller segment.

The Negative

- Operating expenses growth to slow, but still growing faster than revenue. Operating expenses for 4Q22 grew 45% YoY to US$1.8bn. Expenses growth was driven primarily due to higher headcount cost and loan losses. Losses increased due to the surge in volumes on Square loans and losses related to the buy-now-pay-later platform. However, total operating expenses growth did slow in 4Q22 compared with the first three quarters of FY22 (70% YoY growth in 1Q22, 66% in 2Q22, and 46% in 3Q22). Management remains committed to slowing expense growth in FY23e driven by measured hiring, real estate consolidation, and careful marketing spend across both Square and Cash App divisions. Net loss for 4Q22 was US$114mn, with FY22 net loss at US$541mn.

Company Background

Block (SQ), which changed its name from Square in Dec. 2021, operates as a financial services and digital payments company. Block’s two primary business segments are Square (29% of FY21 revenue), which offers point-of-sale (POS) hardware, software, and financial services to micro/small merchants, and Cash App (70%), a personal finance app for individuals that offers peer-to-peer (P2P) money transfers, debit card services, and investing (equities & Bitcoin). The US accounts for the majority (>95%) of revenue.

Investment Highlights

We initiate coverage with a NEUTRAL rating. Our target price is US$70 based on a DCF valuation with a WACC of 7.1% and terminal growth of 4.0%.

|

REVENUE Block generates revenue through four sources: 1) transaction-based revenue (27% of total revenue in FY21), which is calculated as a percentage of GPV; 2) subscription and services-based revenue (15%), earned from Instant Transfer fees charged to Cash App users and Square retailers, web hosting and domain name registration services, and servicing fees on Square Loans; 3) hardware revenue (1%), which is generated from sales of Square’s POS devices including contactless, EVM chip readers, and Square Stand; 4) bitcoin revenue (57%), which is recognized when Cash App customers purchase bitcoin at the cost of sale. In order to provide bitcoin to customers, the company typically buys the cryptocurrency from private brokers/dealers and charges a small margin before selling it to customers.

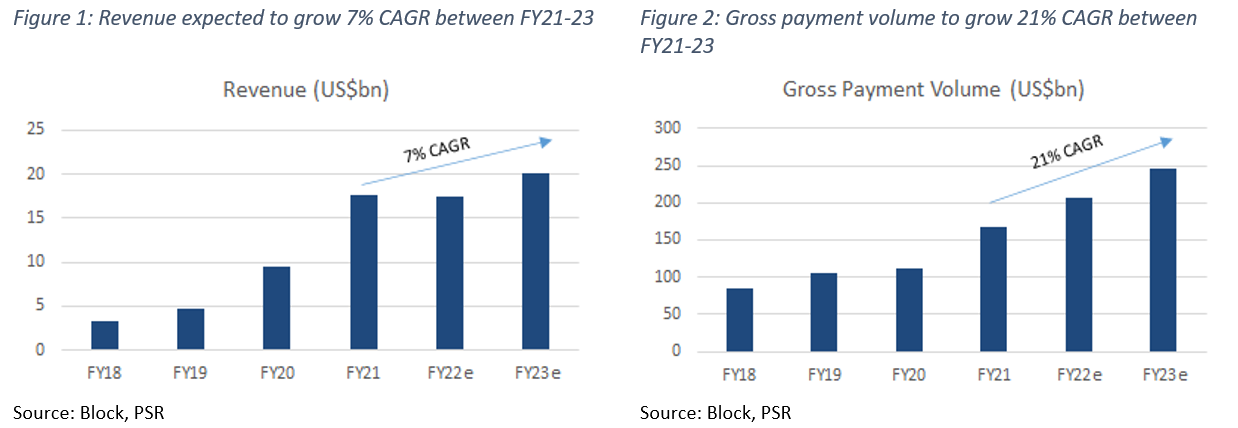

Block posted US$17.7bn in revenue for FY21 – increasing 86% YoY (Figure 1), with 70% of its total revenue coming from its Cash App segment and 29% from its Square segment. Square provides POS solutions to small merchants, while Cash App is a personal finance app for individuals. Block’s total revenue expanded at 75% CAGR in the past three years mainly driven by a surge in number of active Cash App customers and the number of business accounts. In FY21, Block’s GPV rose 49% to US$167.7bn (Figure 2) as retailers witnessed a significant rebound in sales activity post the COVID-19 vaccine roll-out, specifically from brick-and-mortar channels that had been adversely impacted by lockdowns in FY20. The US accounts for the majority (>95%) of revenue.

Revenue growth: We forecast total revenue of US$17.5bn in FY22e, which would represent a fall of 1% YoY, mainly due to weak consumer demand for Bitcoin and decline in cryptocurrency prices. Revenue from the Cash App segment in FY22e is expected to reach US$10.5bn (15% YoY drop), primarily from decline in Bitocin revenue slightly offset by growth in Cash for Business and Cash App Instant Deposit. Excluding Bitcoin, Cash App’s revenue is expected to grow by 46% YoY to US$3.4bn in FY22e. Square revenue is expected to grow by 30% YoY to US$6.8bn, on the back of increasing Square gross payment volume, origination volumes of Square Loans, as well as software subscriptions.

|

RULE OF 40

The “Rule of 40” was first introduced as a benchmark to measure the balance between growth and profitability of SaaS companies, taking into account both revenue growth, as well as profitability (Revenue Growth + EBITDA Margins), with the addition of both metrics needing to exceed the 40% threshold. We have modified this slightly by averaging revenue growth over a 3-year period compared to just a single period growth rate. Adding together Block’s 3-year average revenue growth of 77% and its adjusted EBITDA margin of 6%, the total of 83% is > than our required threshold of 40% (Figure 3).

|

RULE OF 40 The “Rule of 40” was first introduced as a benchmark to measure the balance between growth and profitability of SaaS companies, taking into account both revenue growth, as well as profitability (Revenue Growth + EBITDA Margins), with the addition of both metrics needing to exceed the 40% threshold. We have modified this slightly by averaging revenue growth over a 3-year period compared to just a single period growth rate. Adding together Block’s 3-year average revenue growth of 77% and its adjusted EBITDA margin of 6%, the total of 83% is > than our required threshold of 40% (Figure 3).

EXPENSES Block’s cost of sales grew 96% YoY in FY21 to US$13.2bn, above the total revenue growth of 86%. Cost of sales (75% of total revenue in FY21) includes transaction-based costs (processing fees and bank settlement fees), hardware costs consisting of product costs related to the company’s POS devices (Figure 4), and bitcoin costs comprising the amounts paid by Block to purchase Bitcoin.

Cash App cost of sales grew 116% YoY to US$10.2bn (58% of FY21 revenue) driven by growth in Cash App Instant Deposit, Cash for Business, and bitcoin costs. Square cost of sales grew 42% YoY to US$2.9bn (16% of FY21 revenue) primarily due to growth in GPV and growth in both card-present volumes and higher priced card-not-present transactions that occur over the phone, internet, or mail.

Operating expenses include product development (8% of FY21 revenue); sales and marketing (9%); general and administrative (6%); transaction and loan losses (1%); and bitcoin impairment losses (0.4%). Total operating expenses as a percentage of revenue have reduced from 41% in FY18 to 24% in FY21. We expect operating expenses as a percentage of revenue to be 37% in FY22e due to ongoing product innovation and sales and marketing spend to attract users to its platform.

MARGINS In FY21, Block's revenues nearly doubled, but at the same time, its cost of sales also doubled. The company’s high cost of sales significantly lowers margins. Gross margins declined from 40% in FY18 to 25% in FY21 as expenses outpaced revenue growth. Gross margins from Cash App are down from 45% in FY18 to 17% in FY21, mainly due to the company’s bitcoin operations. Bitcoin is a negligible 2-3% gross margin business for Block. Meanwhile, Square’s gross margin is up from 39% to 45% over the same period due to increasing gross payment volumes.

In FY21, operating margin was at 1%, up from -0.2% in FY20, driven by lower operarting expenses. Block recorded net profit margin of 1% for FY21, a decrease from 2% the year before, and this was mainly due to lower other income. In FY21, Adjusted PATMI grew by 111% YoY to US$898mn, which mainly excludes stock-based compensation expense, amortization of acquired intangible assets, and bitcoin impairment losses.

We anticipate Block to continue generating small margins on revenues due to ongoing product innovation and growth investments.

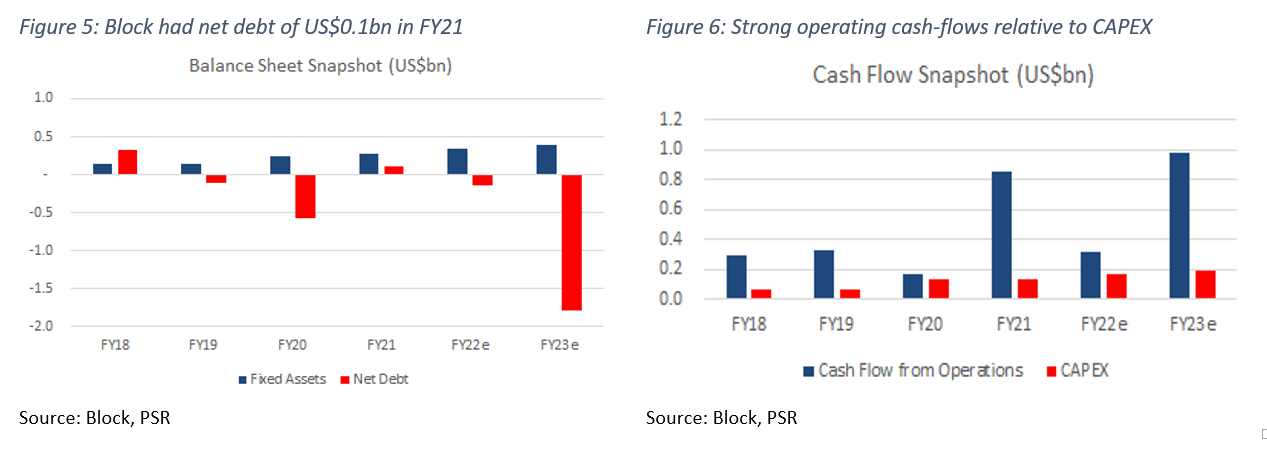

BALANCE SHEET Assets: In FY21, cash and cash equivalents increased by 41% YoY to US$4.4bn. Customer funds accounted for US$2.8bn (up 39% YoY) of assets in FY21, and are attributed to the customers stored balances that they could later use to make payments or send money. Block is a relatively asset-light business and doesn’t need heavy investments in fixed assets. In FY21, the company reported fixed assets of US$282mn. Block’s current ratio for FY21 is 1.9x.

Liabilities: Current liabilities for FY21 were US$5.4bn, almost US$1.3bn more than FY20. This increase was mainly due to a rise in customer payable balances. Non-current liabilities saw a surge of US$2.1bn in FY21. Block had a net debt position of US$0.1bn in FY21 (Figure 5). Block’s debt-to-equity ratio is 1.4x.

CASH-FLOW Cash-flow from operations has steadily risen from US$295mn in FY18 to US$848mn in FY21 (Figure 6). CAPEX for FY21 was US$134mn (1% of revenue), in line with the previous year. The company generated US$714mn in free cash flow in FY21. This translates to a 4% free cash flow margin.

|

BUSINESS MODEL

Block has two reportable segments: Cash App and Square. Cash App helps individuals transact and manage their money, while Square helps sellers start, manage, and grow their businesses.

Cash App (70% of FY21 revenue): Block drives most of its revenue through its mobile application Cash App. The application allows consumers to send and receive P2P (peer-to-peer) money for free, but charges about 3% fees on transactions involving credit cards (Figure 7). Cash App also allows consumers to deposit funds, invest in stocks and bitcoin, and use its debit card (Visa Cash Card), that is linked to customer stored balances, to withdraw funds from an ATM or to make purchases. Consumers can also directly deposit checks and store money in accounts. Cash App reported 44mn monthly active users as of FY21 (up 22% YoY).

In FY21, Cash App generated US$12.3bn in revenue, up 106% from the prior year. The primary drivers were growth in bitcoin revenue, Cash App Instant Deposit, Cash Card, and Cash for Business. Cash App gross profit was US$2.1bn in FY21, which is an increase of 69% compared to US$1.2bn in FY20. The segment’s gross profit accounts for about 47% of the company’s overall gross profit.

Bitcoin revenue will fluctuate based on customer demand as well as changes in the bitcoin market price. While bitcoin accounted for 57% of total revenue in FY21, it contributed only 5% of total gross profit. Revenue from Cash App segment in FY22e is expected to reach US$10.5bn (15% YoY drop), primarily from the decline in Bitocin revenue slightly offset by growth in Cash for Business and Cash App Instant Deposit (Figure 8).

Square (29% of FY21 revenue): The Square segment allows merchants of all sizes to accept debit and credit card payments through its point-of-sale (POS) products. Square charges a standard processing fee of 2.6% plus US$0.10 for most transactions regardless the type of card or size of merchant. However, transactions entered through a terminal manually will incur a fee of 3.5% plus US$0.15. Square’s product suite includes POS hardware (card reader and Square stand) and software (inventory tracking), scheduling services, invoicing, e-commerce solutions, payroll, and business loans. This suite of products enables merchants to work with Square to run and grow their businesses in an integrated and seamless manner instead of working with multiple vendors.

In FY21, Square generated US$5.2bn in revenue, up 47% from the prior year. This was primarily driven by growth in GPV attributable to higher consumer spending fueled in part by resumed in-person activity at sellers and broader macro economic recovery. Square gross profit was US$2.3bn in FY21, which is an increase of 54% YoY. The segment’s gross profit accounts for about 52% of the company’s overall gross profit. Square revenue is expected to grow by 30% YoY to US$6.8bn in FY22e (Figure 9), on the back of increasing Square gross payment volume, origination volumes of Square Loans, as well as software subscriptions.

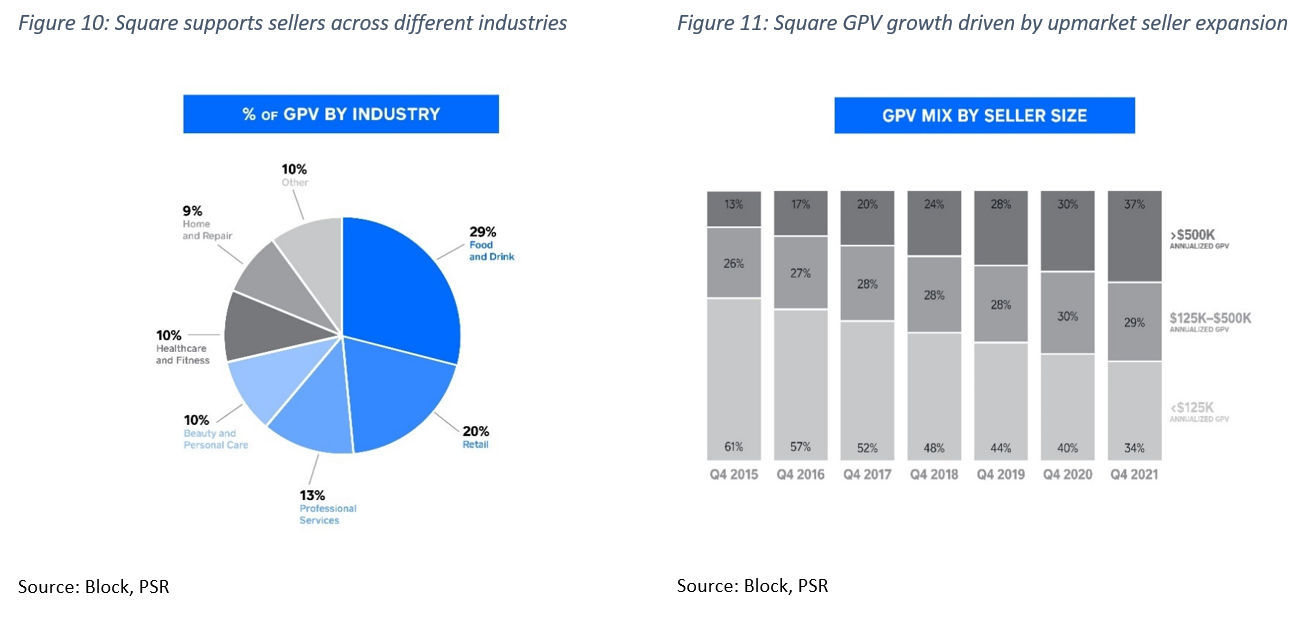

The Square segment serves merchants across several industries including Food & Drink, Retail, Professional Services, Healthcare and Fitness, and others (Figure 10). Square started out serving micro sellers but over time has been expanding upmarket to serve mid-market sellers (larger merchants that generate annualized GPV of >US$500K). In 4Q21, mid-market sellers accounted for 37% of total GPV for Square, up from 30% in 4Q20 (Figure 11). The growth was mainly driven by targeted product development (adding valuable new services) to create a unique experience for merchants. Block has also significantly expanded its business operations over time through acquisitions, notably acquiring buy now pay later (BNPL) company Afterpay, website builder Weebly, and music streaming service TIDAL.

|

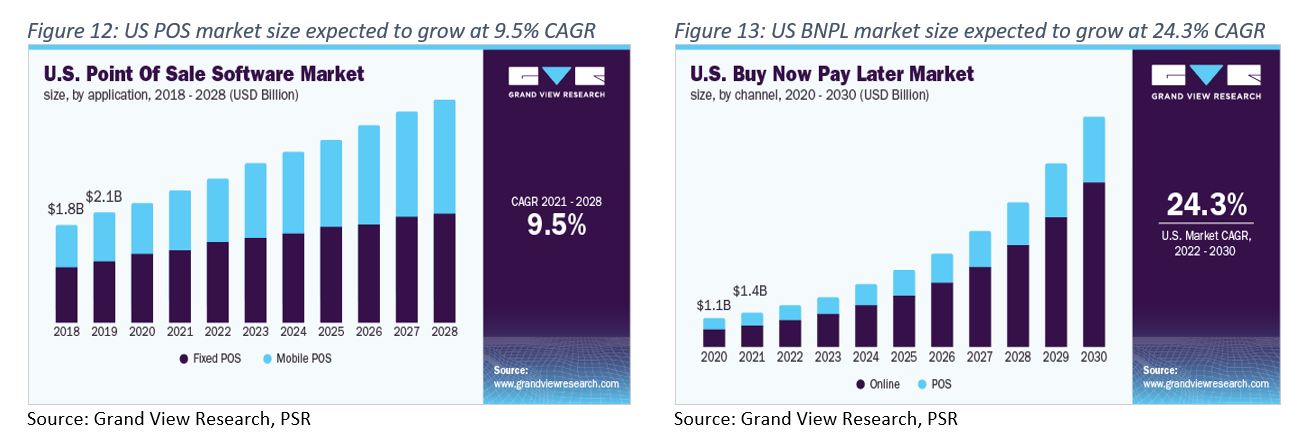

INDUSTRY Block is mainly part of two markets; point-of-sale (POS) system and payment processing solutions. A POS system enables businesses to accept payments from customers, keep track of sales, create receipts, inventory management, and more. According to Grand View Research, the global POS software market size, valued at an estimated US$10.4bn in 2021, is set to reach US$19.6bn in value by 2028, which indicates a 9.5% CAGR. The US POS software market size is also expected to see a CAGR of 9.5% (Figure 12). The main growth drivers for the market include rising interest in cashless transactions among customers, brick-and-mortar sales rebounding after the pandemic, and businesses transitioning to cloud-based POS systems from legacy hardware. In the POS market, Block competes with Lightspeed, PAR Technology and Toast. Lightspeed operates both in the retail and hospitality space, while Toast and PAR focuses on serving restaurants.

A payment processor communicates financial transaction information between the merchant, the bank that issued a customer’s credit or debit card, and the merchant’s bank. The payment processor ensures that the funds are transferred to the merchant's account, and in turn earn revenues from transaction fees. According to Grand View Research, the global payment processing solutions market size, valued at an estimated US$38bn in 2020, is set to reach US$98bn in value by 2027, which indicates a 14.5% CAGR. The major growth drivers for the market are continued growth in the number of merchants seeking integrated payment processing solutions; high penetration of smartphones; and rising demand for online payments. In the payment processing services market, Block competes with PayPal, Stripe, and Global Payments. While PayPal has a competitive advantage in the payment processing solutions market, Block is the leader in the POS market. PayPal operates a two-sided payment network with 392mn active consumer accounts and 34mn active merchant accounts across 200 markets (compared with Block’s 80mn annual active Cash App users). PayPal has a market share of 41.9% in the online payment processing solutions worldwide.

With the acquisition of Australian payment platform Afterpay for US$29bn on Jan 31 2022, Block got access to the buy now pay later (BNPL) market. BNPL is a payment method that enables customers make purchases both online and in-store without having to pay the full amount upfront. According to Grand View Research, the global BNPL market size, valued at an estimated US$6.2bn in 2022, is set to reach US$39.4bn in value by 2030, which indicates a 26% CAGR. The US BNPL market size is expected to see a CAGR of 24.3% (Figure 13). The main growth drivers for the market are digitization, rising merchant adoption, and the increasing repeat usage among younger consumers. Young consumers prefer using BNPL services as it provides interest-free financing for buying high cost electronic devices, clothes, paying tuition fees and stationery products, and other items for general use.

|

|

RISKS 1. Consumer spending and economic pressure. Block’s operations are closely linked to the changes in consumer discretionary spending. A deterioration in the macroeconomic environment or a sudden surge in the unemployment rate could reduce consumer sentiment and spending, and adversely impact Block's revenue growth and profitability. In addition, Block is exposed to greater degree of cyclical risks due to its disproportional exposure to micro merchants.

2. Intense Competition. Block faces competition from several players in the payment processing and peer-to-peer payment markets, including PayPal, Shopify, Apple Pay, Google Pay, and Stripe. With the acquisition of Afterpay, Block also directly competes against BNPL service providers such as Affirm. As a result, Block will need to keep strengthening its network effects and upgrade its products to maintain its historical growth rate.

3. Exposure to Bitcoin. Block is exposed to bitcoin price volatility through Cash App and company investments worth US$220mn. The cryptocurrency’s long-term adoption is still uncertain. For its investments in bitcoin, Block recognizes any decline in the market price below the original cost as an impairment charge as the cryptocurrency is an indefinite-lived intangible asset. |

|

VALUATION We initiate coverage of Block Inc with a NEUTRAL rating and a price target of US$70.00. Our valuation is based on DCF valuation, using a 7.1% WACC and a 4.0% terminal growth rate (Figure 14).

|