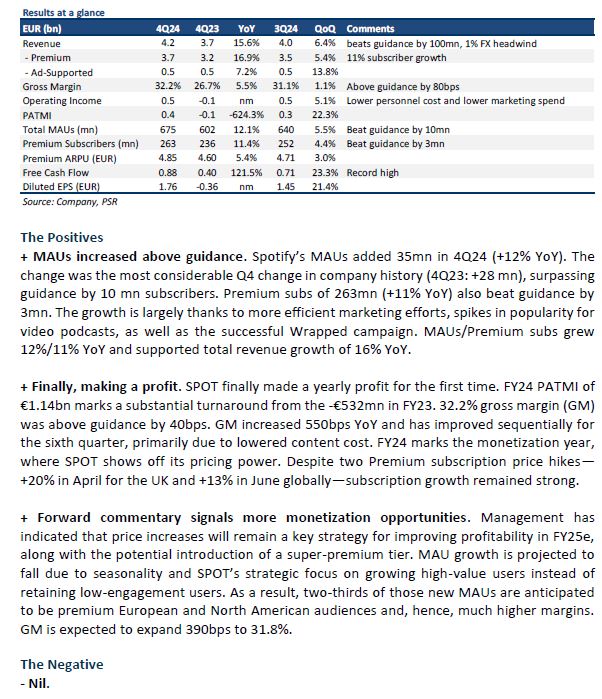

The Positives

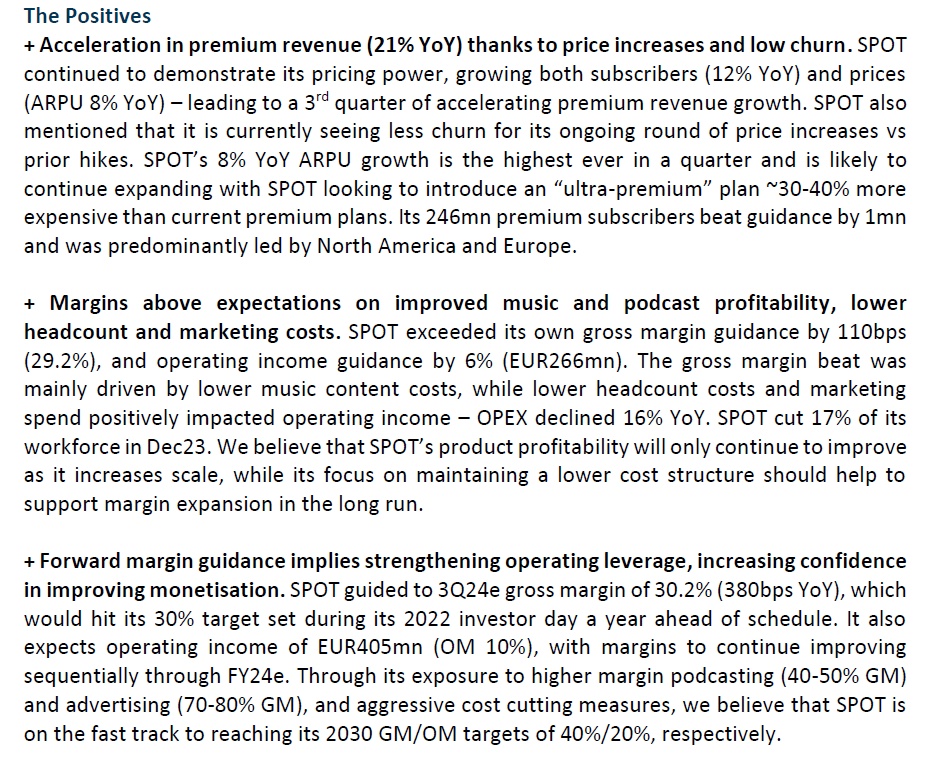

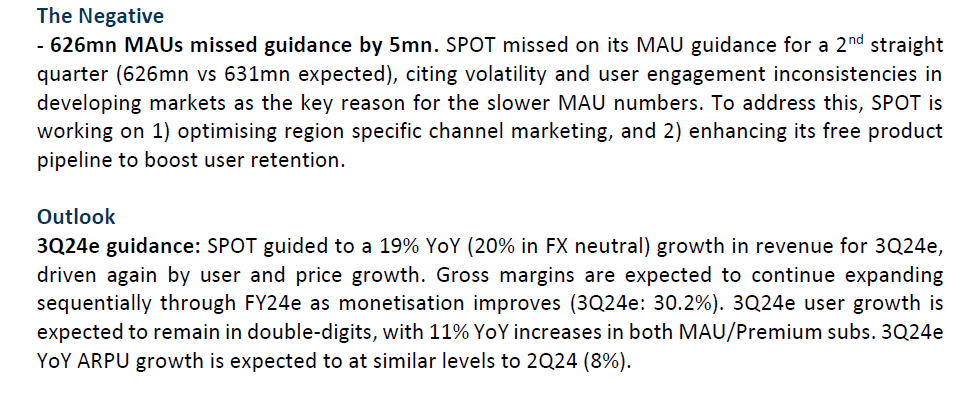

+ Premium revenue growth is accelerating, a sign of improving monetisation. Price hikes (ARPU 5% YoY) towards the back end of FY23 and broad-based growth in subscribers (14% YoY) across all regions drove Premium subscriber revenue growth of 20% YoY (21% FX neutral) in 1Q24 – 3% point increase in growth vs 4Q23. SPOT also expects another quarter of sequential ARPU growth in 2Q24e as it remains focused on improving monetisation of its users after several years of driving user growth. We remain positive about SPOT’s ability to keep churn low while raising prices as it delivers incremental value to its users through new products (Audiobooks, AI DJ, music videos) and platform improvements.

+ Meaningful cost benefits from reaching scale. SPOT has a variety of cost models for its different audio products, with most of its cost base comprised of revenue sharing (royalties) agreements with labels, and fixed content costs for podcasts. We believe that SPOT is beginning to see meaningful cost benefits from reaching scale as it: 1) leverages its distribution for more favourable agreements with its music partners and 2) continues to be more efficient with removing underperforming podcasts. Its 27.6% gross margin for 1Q24 (90/240bps QoQ/YoY) beat its own guidance by 120bps, with Premium gross margin of 30.2% and ad-supported gross margin of 6.4%.

The Negative

- 615mn MAU fell short of SPOT’s 618mn guidance. SPOT under-delivered on its MAUs for 1Q24, with 615mn MAUs and 3mn under its own guidance. The company attributed this to 3 main factors: 1) sequential slowdown in momentum after a very strong FY23, 2) slight disruption in BAU operations from its workforce reduction (-17% reduction) in Dec 23, 3) excessive pullback in marketing spend throughout FY23 (which has since been corrected).

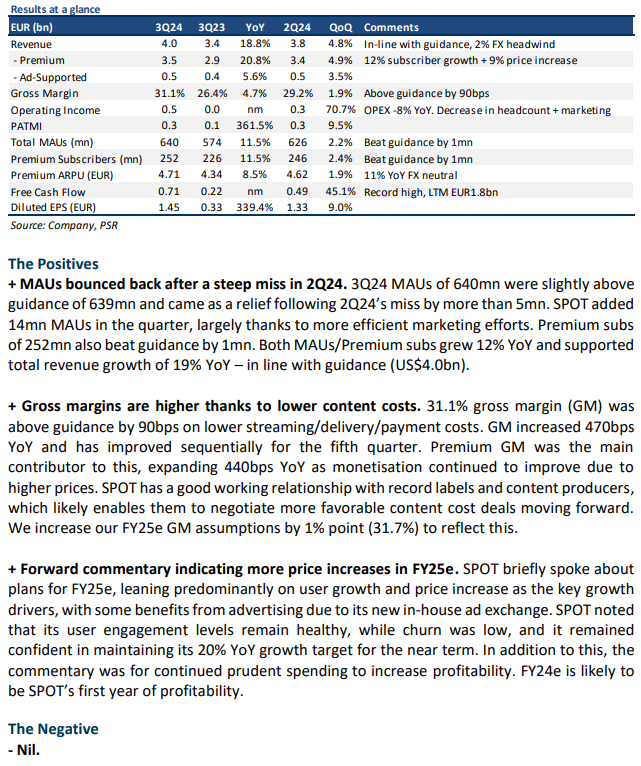

The Positives

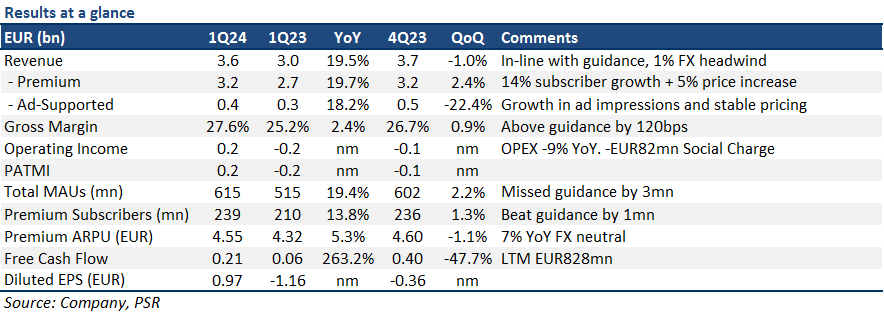

+ Revenue growth accelerating into FY24e with 28mn new MAUs, 10mn new premium subscribers. SPOT again exceeded its user growth expectations with 23%/15% YoY growth in MAU/Premium Subs. It ended FY23 adding 113mn monthly users, and 31mn new premium subscribers (Figure 1). MAU growth is extremely important for SPOT as it is the main channel used to convert free-to-listen users into premium subscribers. The outperformance in users, together with price increases mid-4Q23, drove an acceleration in revenue growth (4Q23: 16% YoY vs 3Q23: 11% YoY) – with SPOT also expecting growth to accelerate in FY24e.

+ Positive commentary on margins, focusing on monetisation for FY24e. Management was positive on its expanding margins, with 4Q23 gross margin of 26.7% 10bps above guidance. SPOT spent much of FY23 working on being more efficient in terms of investments and costs, from laying off employees to cutting non-performing content. Moving into FY24e, we expect gross margins to expand by ~250bps with sequential increases QoQ, driven by: 1) price increases; 2) improving efficiencies of scale; 3) better monetisation of Podcasts and advertising; and 4) improved deals with record labels/agencies.

+ Remaining focused on prudent spending moving forward. SPOT provided some near-term clarity for spending, saying that it would raise investment hurdle rates, and remain prudent on future spending – as it looks to balance growth and profitability. We forecast FY24e OPEX to decline -5% YoY due to the lumpiness of spend in FY22 and FY23, but to remain in line with its long-term linear trend. Long-term growth remains a key focus for SPOT, but we expect FY24e to be a year of monetising its ever-growing user base given its latest commentary.

The Negative

- Nil.

MAU (Monthly Active User): average number of active users during a month.

The Positives

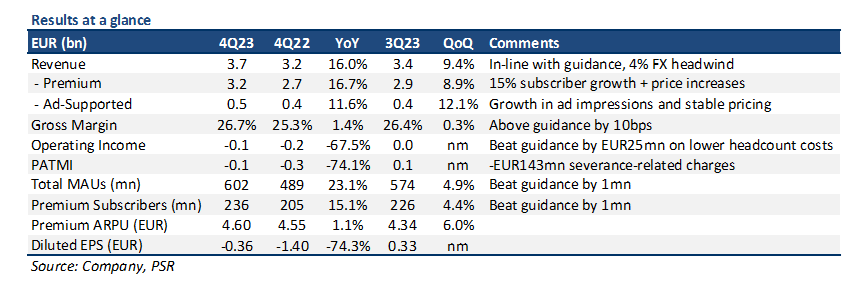

+ User metrics continue to outperform even after price hikes. SPOT’s outperformance in subscribers was the main driver for its slight revenue beat. The company added 6mn new premium subscribers (16% YoY) even after it raised prices during the quarter, and 23mn MAUs (26% YoY), both ahead of guidance by 2mn – indicating low levels of churn. The 23mn new MAUs was also SPOT’s 2nd largest Q3 addition ever. SPOT guided to 601mn MAUs (23% YoY) and 235mn Premium Subscribers (15% YoY) by the end of FY23e. We view user and subscriber growth as key, given that the company is still in its scaling up phase and has not yet begun to efficiently monetise its users.

+ Margins improving across both premium and ad-supported. Overall gross margins saw a 166bps YoY improvement to 26.4%, with margin expansion across both Premium and Ad-Supported businesses. Premium gross margin was 29.1%, the highest for any Q3, driven by efficiencies from scale, while ad-supported gross margin was 8.3%, a 646bps increase YoY as podcast margins improved. Overall margin expansion reflected improvements in both music profitability and podcast trends. Gross margin beat guidance by 40bps, with expectations for sequential expansion in 4Q23e.

+ Profitabilty seems to have reached an inflection point. With the increase in gross margins, operating profits returned, with SPOT posting EUR32mn in operating income – beating its own guidance by EUR77mn, on lower marketing and personnel costs. Operating leverage seems to have returned, signaling a potential inflection point for profits moving forward as revenue growth (11% YoY) outpaces OPEX (-13% YoY). As a result, we forecast a EUR162mn improvement in PATMI for FY24e.

MAU (Monthly Active User): average number of active users during a month.

ARPU (Average Revenue per User): premium revenue for period divided by average number of premium subscribers for same period.

The Negative

- Nil.

The Positives

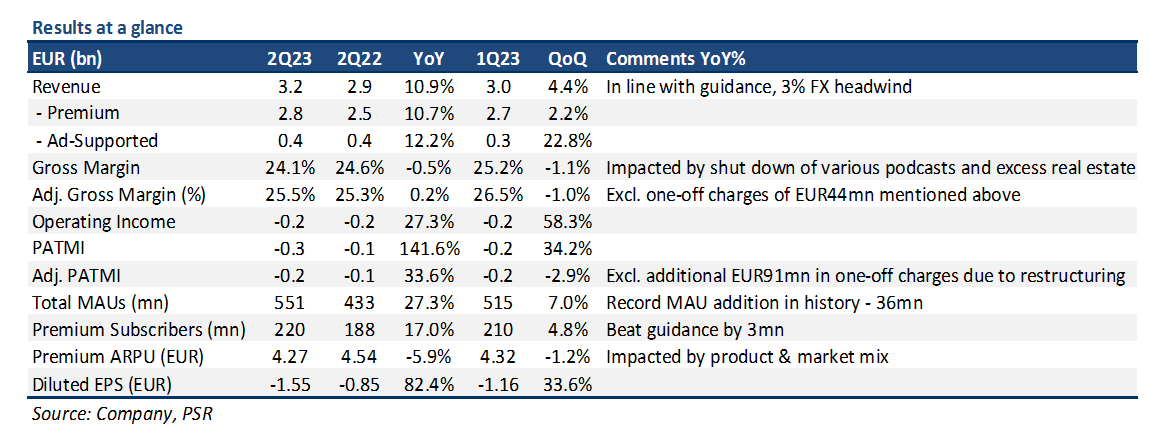

+ User growth continues to outperform, highest MAU growth. SPOT continues to attract more users onto its platform, with a record 36mn new MAUs in 2Q23, and 551mn MAUs to end the quarter (27% YoY). Similarly, Premium Subscribers also did well, with YoY growth accelerating over the last 4 quarters (2Q23: 17% YoY) as conversion rates remained healthy. Premium subscriber growth usually lags MAU growth as users gradually convert into paying subscribers.

+ Efficiency still front and centre. SPOT reiterated its focus on improving operational efficiency, evident from its reduction in headcount by 2% QoQ and downsizing of its real estate footprint in 2Q23. SPOT has also raised its hurdle rate for new investments, and also cut underperforming podcast content from its content library. The company also guided that OPEX as % of revenue should continue to fall over the long term as efficiency improves.

The Negative

- Losses widen due to EUR135mn in restructuring-related charges. 2Q23 operating loss stood at -EUR247mn, EUR53mn wider than a year ago. More than half the losses (-EUR135mn) were a result of charges relating to: 1) shutting down underperforming podcasts; 2) reducing real estate footprint; and 3) headcount reductions. Removing these charges, adj. operating loss of -EUR112mn would have been slightly ahead of guidance.

MAU (Monthly Average User): average number of users during a month.

ARPU (Average Revenue per User): premium revenue for period divided by average number of premium subscribers for same period.

The Positives

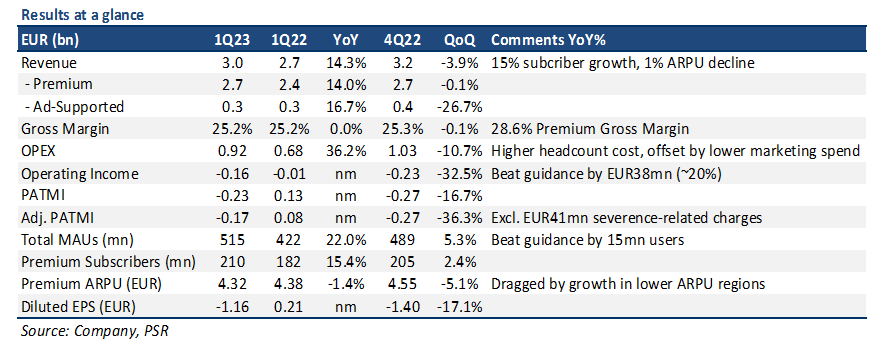

+ Record user additions for 1Q, both MAU/premium subscriber growth beat guidance. SPOT gained 26mn MAUs in 1Q23, a record number for the quarter; 515 mn MAUs beating guidance by 15mn; and 210mn Premium Subscribers, 3mn above guidance. The company also saw an acceleration in MAU retention and subscriber growth (1Q23: 22% YoY vs 4Q22: 20% YoY), with engagement trends also improving. MAU to Premium subscriber conversion rates also remained at healthy levels, which is important given MAUs are the main funnel that drives Premium subscriber additions.

+ Operating loss beat guidance on lower-than-expected spending. Operating losses fell sequentially by 33% QoQ to -EUR156mn on the back of reduced marketing spend. SPOT is also looking at reducing content production, and optimizing its real estate footprint in further efforts to reduce expenses. Improvements were offset by a EUR41mn severance-related charge and EUR12mn of social charges. 1Q23 operating loss was ~20% better than guidance, with operating margin improving sequentially from -7.3% in 4Q22 to -5.1% in 1Q23.

The Negative

- Revenue missed guidance slightly on weakness in advertising. SPOT’s 1Q23 revenue of EUR3.0bn slightly underperformed its own guidance of EUR3.1bn, citing a ~6% underperformance in Ad revenue as a drag. Additionally, Premium ARPU declined 1% YoY as a result of additional growth in family and duo plans vs single plans. Even with the decline, Premium ARPU was still within the company’s estimates, with the expectation of at least 1 price hike on the horizon this year.

MAU (Monthly Average User): average number of users during a month.

ARPU (Average Revenue per User): premium revenue for period divided by average number of premium subscribers for same period.

The Positives

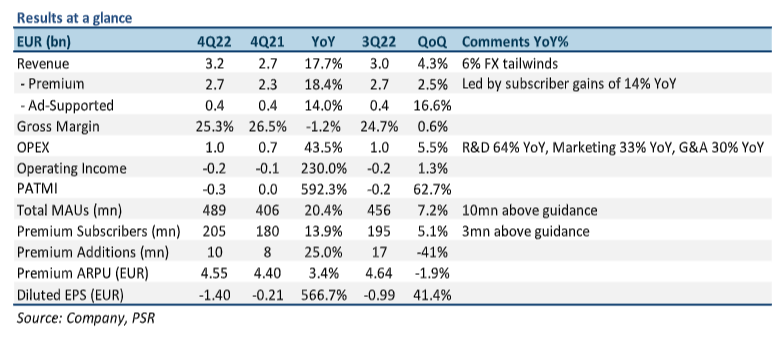

+ Premium subscriber base growing better than anticipated. SPOT ended 4Q22 with 205mn subscribers (14% YoY), with 10mn additions – 3mn more than it guided. Premium ARPU was up 3% YoY, with premium revenue hitting EUR2.7bn, 18% YoY. MAUs also hit 489mn for the quarter (20% YoY), with a record 33mn new users – 10mn above guidance. The strong set of subscriber/MAU numbers seemingly is validation of the company’s continuous investments in content and platform improvements over the last several years. SPOT guided 500mn MAUs, and 207mn premium subscribers by end 1Q23e.

+ Gross margin beat guidance by 0.8%, operating loss slightly ahead of guidance. Gross margin for 4Q22 was 25.3%, 0.8% above guidance primarily due to lower-than-expected podcast content spend and continued growth in its core music business. Operating loss of -EUR231mn was also slightly better than expected as SPOT benefitted from slowing expense growth. Guidance for 1Q23e is for slightly lower gross margin of 24.9% and operating loss of -EUR194mn due to some drag by severance-related charges and unfavourable FX impact.

The Negatives

- Operating expenses growth to slow, but still growing faster than revenue at 44% YoY. Operating expenses for 4Q22 came in at EUR1.0bn, or roughly 44% YoY, and 6% QoQ. Expenses growth was driven primarily due to higher headcount cost and increasing advertising expenses, with R&D up 64% YoY; Sales & Marketing up 33% YoY; and G&A up 30% YoY. However, expenses growth did slow from 65% YoY in 3Q22, and is expected to continue slowing for the remainder of FY23e with a 6% cut in headcount, reduced investments, and a shift in focus towards improving profitability.