Spotify Technology S.A.- From music app to data powerhouse

-

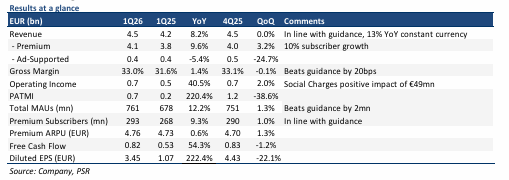

1Q26 revenue grew 8% and was within expectations. 1Q26 PATMI exceeded our estimates and jumped 220% YoY, driven by a €49mn benefit from social charges (due to share price movements) as well as a favourable revenue mix and cost discipline. 1Q26 revenue/PATMI were at 23%/30% of our FY26 forecasts.

-

User metrics ramped up to 761mn MAUs (+12% YoY). Premium subscribers grew to 293mn (+10% YoY, +1% QoQ).

-

We maintain our Buy recommendation with an unchanged target price of US$650. Our estimates remain unchanged, with a WACC of 7.5% and a terminal growth rate of 3.5%. SPOT continues to deliver strong user momentum and improve profitability, and its unique and hard-to-replicate dataset is its biggest advantage. Near-term margins may face some pressure from ongoing investment in AI and ad-tech, but these are strategic steps that position the company to emerge stronger with improved monetisation over the long term.

The Positives

+ Strong top-line growth, user momentum still intact. SPOT continued to deliver solid top

line user momentum in 1Q26, with MAUs reaching 761mn (+12% YoY), exceeding guidance

by 2mn. Growth was led by Rest of World and North America, supported by the enhanced

free-tier rollout, which improved engagement, with users “listening and watching more days

per month”. Management highlights the number of days per month as a key driver of

retention and lifetime value, reinforcing the company’s broader monetisation framework.

+ Margins continue to expand. Spotify delivered a gross margin of 33% (+133bps YoY),

surpassing guidance. The margin expansion was driven by the favourable cost of revenue and

revenue mix. This marks continued progress in SPOT’s multi-year profitability journey,

supported by Premium ARPU expansion (+5.7% YoY) and disciplined cost management,

including stable headcount. Management reiterated expectations for full-year margin

expansion in FY26, despite near-term reinvestment in AI and product initiatives, highlighting

confidence in sustaining operating leverage as the business scales.

+ AI-driven personalisation is accelerating engagement and reinforcing long-term

monetisation. SPOT continues to deepen its AI capabilities across the platform, with

features such as AI DJ reaching 94mn users (out of 293mn subscribers) and new launches

like SongDNA scaling to 52mn users within just four weeks, reflecting rapid adoption. AI is

enabling faster product iteration, lower cost per feature, and deeper personalisation. We

see SPOT increasingly evolving from a music app into a data powerhouse, leveraging its

0.76bn user base and decades of listening data to build highly granular “taste” profiles that

are difficult to replicate, providing a structural advantage.

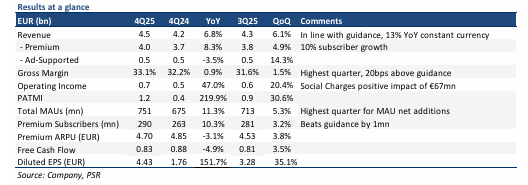

Spotify Technology S.A.- Record MAU addition

- 4Q25 revenue grew 7% and was within expectations. 4Q25 PATMI exceeded our estimates and jumped 220% YoY, driven by favorable content costs and a €67mn benefit from social charges. FY25 revenue/PATMI were at 99%/130% of our FY25 forecasts.

- User metrics ramped up to 751mn MAUs (+11% YoY), the highest quarter for MAU net additions. Premium subscribers grew in double digits to 290mn (+10% YoY).

- We upgrade our rating from ACCUMULATE to BUY rating due to recent price performance while maintaining a DCF target price of US$650 as we roll over our valuations to FY26e. Our FY26e forecast, terminal growth, and WACC assumptions remain unchanged. SPOT has demonstrated strong pricing power and monetization. AI-driven personalization should further deepen user attachment.

The Positives

+ Engagement is strong with record MAU addition. SPOT continued to expand its user base,

adding a record 51mn MAUs in 4Q25 to reach 751mn MAUs by year-end (+11% YoY), while

Premium Subscribers also grew solidly (+10% YoY). Management attributed the healthy

growth to stronger engagement-led conversion, particularly from product moments such as

the Wrapped campaign (300mn users engaged, +20% YoY; 630mn social shares, +42% YoY),

which delivered the highest single-day subscriber intake in the company’s history. The

enhanced free-tier rollout also helped tighten the funnel by improving retention and

downstream monetization, reinforcing the MAU → engagement → monetization cycle.

+ Margins are improving across both premium and ad-supported. SPOT showed continued

margin expansion alongside growth, with gross margin improving to 33.1% (+150 bps YoY), its

highest level to date. Margin expansion is across both Premium and Ad-Supported businesses.

The expansion was supported by favorable content costs, reflecting better monetization

relative to royalty costs and mix benefits from higher-margin formats. Management also

guided that Jan 26’s U.S. price increase (+8.3%) is expected to lift ARPU (guided at +5–6% in

1Q26), allowing revenue growth to outpace content cost growth. We expect both gross and

operating margins to continue improving in FY26 as pricing and scale efficiencies strengthen

operating leverage.

+ AI is a structural tailwind. New features such as AI DJ and Prompted Playlists show how

natural-language interaction can deepen personalization, increase engagement, and

ultimately improve retention and lifetime value. What we think differentiates SPOT is its

proprietary “language-to-taste” dataset, built from hundreds of millions of listener data

points, which is difficult to replicate and unlikely to be achieved with generic AI models. As

such, AI acts as a catalyst, strengthening the company’s existing monetization framework by

enhancing discovery, engagement, and pricing power.

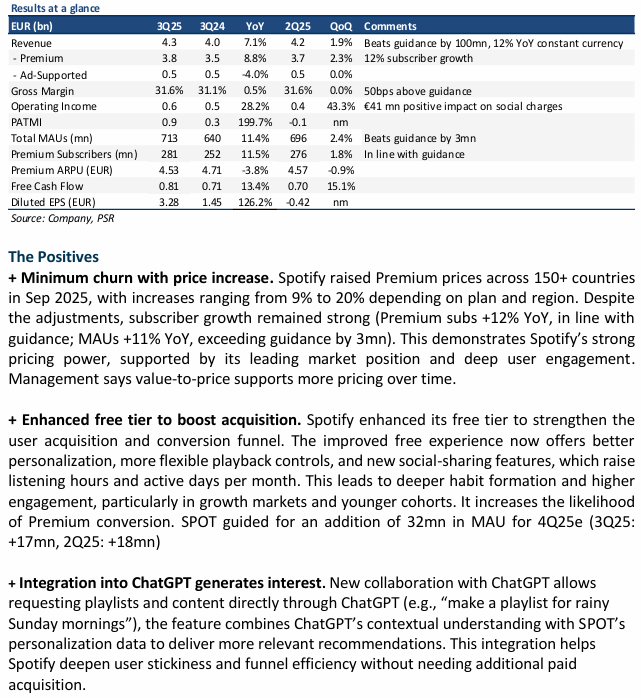

Spotify Technology S.A. – Strong pricing power in play

- 3Q25 revenue/PATMI grew 7% and 200% YoY respectively and were within expectations. PATMI’s big jump is mainly due to royalty accounting adjustment and reduced social charges. 9M25 revenue/PATMI were at 75%/70% of our FY25e forecasts.

- User metrics ramped up to 713mn MAUs (+11% YoY), beating guidance by 3mn. Premium subscribers grew in healthy double digits to 281mn (+12% YoY) despite a 9%-20% price increase in multiple markets.

- We increased FY25e/FY26e revenue and PATMI by 1%/1% and 3%/4% respectively to account for the recent increase in pricing. We have also lower SPOT’s beta to 0.75 to reflect improving revenue stability and demonstrated pricing power. We upgrade our recommendation from REDUCE to ACCUMULATE and our DCF target price is raised to US$650 (prev. US$600).

Spotify Technology S.A.- Strong user growth, but soft guidance

-

Both 2Q25 revenue and adj. PATMI fell short due to execution delays in scaling ad capabilities. 1H25 revenue/adj. PATMI were at 45%/30% of our FY25e forecasts.

-

User metrics ramp up to 696mn MAUs (+11% YoY), in line with guidance. Premium subscribers grew in healthy double digits to 276mn (+12% YoY). Margins are improving across both premium and ad-supported. Guidance for 3Q25e, however, remains soft (revenue +5% YoY) due to near-term investments.

-

We keep our FY25e revenue assumption unchanged. We decrease FY25e PATMI by 12% to account for the extra social charges after share price strength. Our DCF target price remains unchanged at US$600. We upgraded our recommendation from REDUCE to NEUTRAL due to the recent share price performance. While user and subscriber growth remain robust, lower 3Q25e guidance due to near-term investments —combined with high operating costs and currency drag—has tempered near-term expectations.

Spotify Technology S.A.- Growth story remains intact, yet full valuations

- 1Q25 revenue was within expectations while PATMI fell short due to €76mn in social charges - €58mn above forecast - driven by a surge in the share price. 1Q25 revenue/PATMI were at 24%/10% of our FY25e forecasts.

- User metrics ramp up to 678mn MAUs (+10% YoY), in line with guidance. Premium subscribers grew in healthy double digits to 268mn (+12% YoY). Management has indicated no change in demand due to macro-economic conditions and guided continued strong growth in revenue, MAUs, and premium subs for 2Q25.

- We keep our FY25e revenue assumption unchanged. We decrease FY25e PATMI by 4% to account for the extra social charges after share price strength. Our DCF target price remains unchanged at US$600. We downgraded our recommendation from NEUTRAL to REDUCE due to the recent share price strength. SPOT continues to be the industry leader in audio streaming with its growing subscriber base, lower cost structure, and pricing power. Yet we do not see much upside due to full valuations.

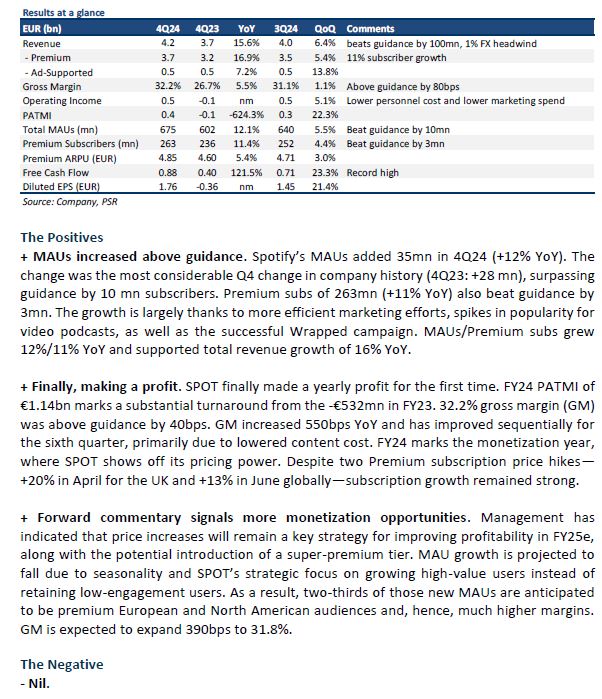

Spotify Technology S.A. – First year of profitability

- 4Q24 results were within expectations. FY24 revenue/PATMI were at 100%/102% of our FY24e forecasts. Revenue grew 16% YoY, while net margin expanded 5.5% YoY.

- User metrics ramp up, with 675mn MAUs above guidance by 10mn. Premium subscribers are still growing healthy double digits to 263mn (+11% YoY). Further margin expansion is expected into FY25e due to gaining greater scale, lowering costs and prioritization on premium subscribers.

- We roll over another year of valuations and keep our FY25e assumptions unchanged. Our DCF target price has been raised to US$600 (prev. US$485), but we downgraded to NEUTRAL from ACCUMULATE due to recent share price gains. SPOT continues to be the industry leader in audio streaming with its growing subscriber base, lower cost structure, and pricing power. Yet we do not see much upside due to full valuations.

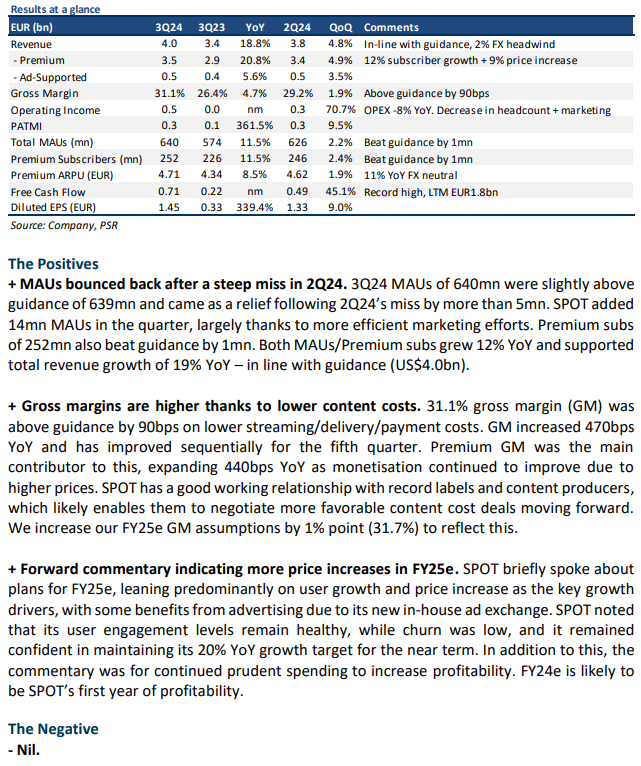

Spotify Technology S.A. – More monetisation the key driver

- 3Q24 results were within expectations. 9M24 revenue/PATMI was at 74%/62% of our FY24e forecasts. Revenue grew 19% YoY, while net margin expanded 6% points YoY.

- User metrics still improving, with 640mn MAUs above guidance by 1mn. Premium subscribers are still growing healthy double digits to 252mn (12% YoY). Further margin expansion is expected into FY25e due to gaining greater scale and lowering costs.

- We keep our FY24e assumptions unchanged, but raise FY25e PATMI by 9% on higher profitability. Our DCF target price has been raised to US$485 (prev. US$420), but we downgrade to ACCUMULATE from BUY due to recent share price gains. SPOT continues to be the industry leader in audio streaming with its growing subscriber base, lower cost structure, and pricing power.

Spotify Technology S.A. – Prime example of pricing power

Spotify Technology S.A. – Raised prices and subscribers still grew

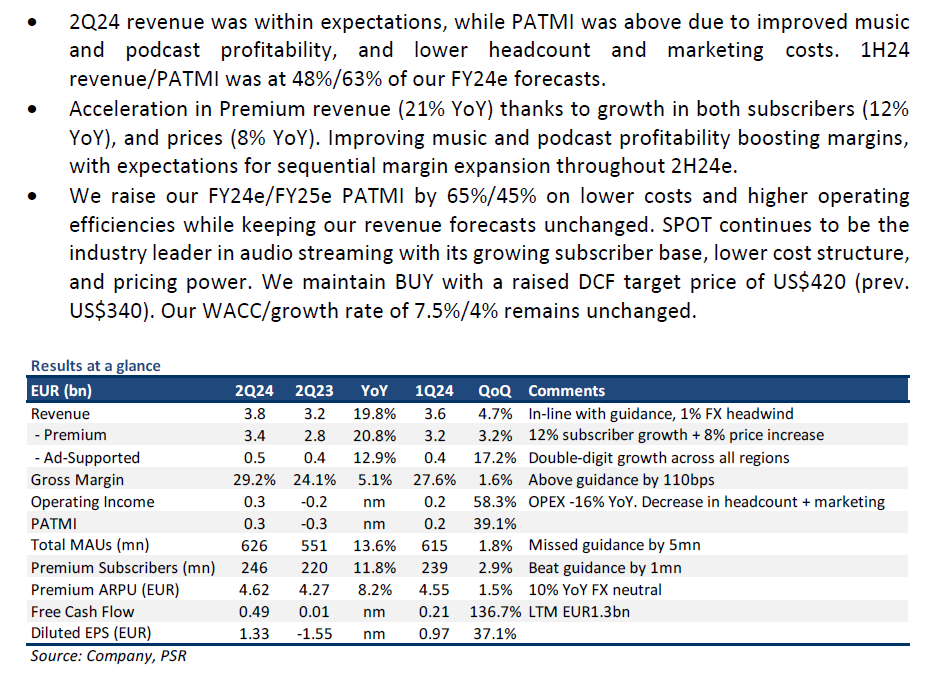

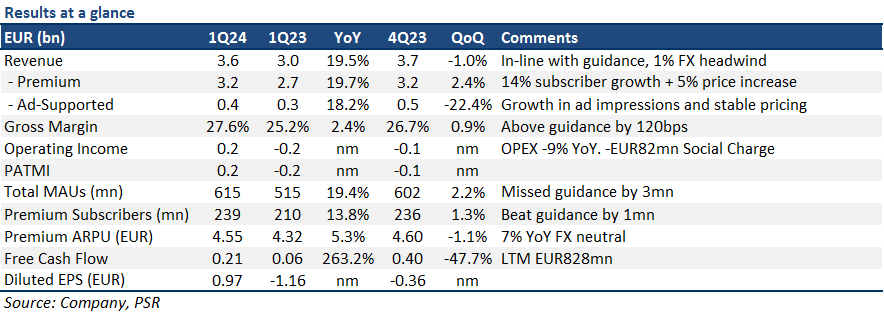

- 1Q24 revenue was within expectations, while PATMI was above due to lower-than-expected costs. 1Q24 revenue/PATMI was at 23%/33% of our FY24e forecasts.

- Growth driven by a combination of subscriber gains and price increases (ARPU 5% YoY). Leveraging scale for meaningful cost benefits through better royalty agreements, improving gross margin 240bps YoY to 27.6%.

- We raise our FY24e PATMI by 26% on lower costs and higher operating leverage while keeping our revenue forecast unchanged. SPOT continues solidifying its position as the industry leader in audio streaming with its growing subscriber base, lower cost structure, and pricing power. We upgrade to BUY from ACCUMULATE with a raised DCF target price of US$340 (prev. US$270) to reflect our assumptions. Our WACC/growth rate of 7.5%/4% remains unchanged.

The Positives

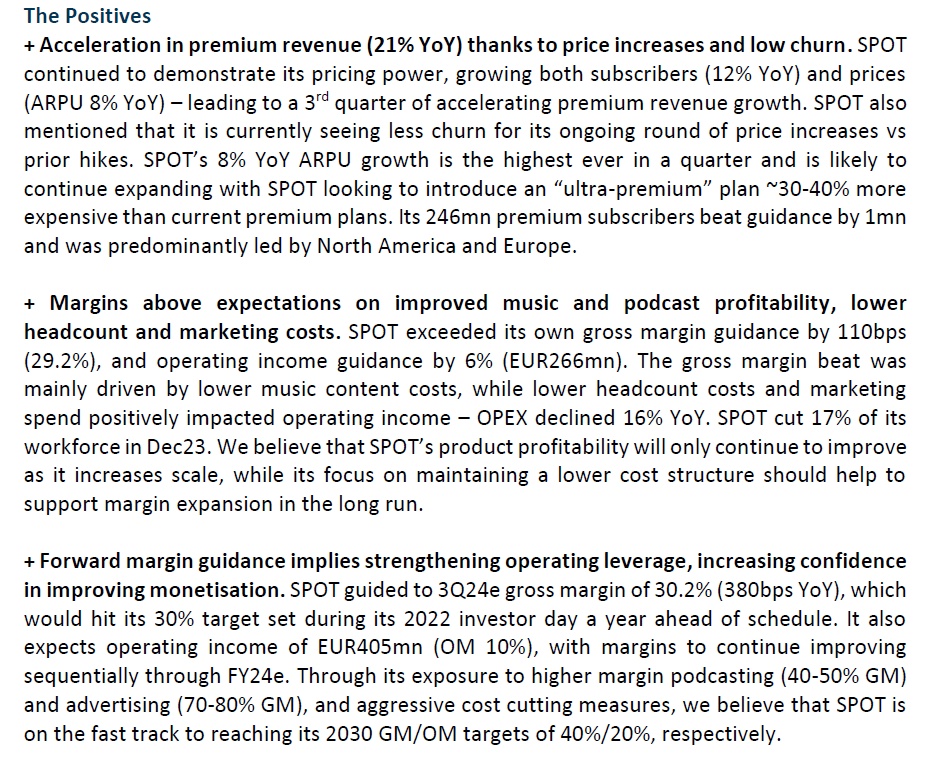

+ Premium revenue growth is accelerating, a sign of improving monetisation. Price hikes (ARPU 5% YoY) towards the back end of FY23 and broad-based growth in subscribers (14% YoY) across all regions drove Premium subscriber revenue growth of 20% YoY (21% FX neutral) in 1Q24 – 3% point increase in growth vs 4Q23. SPOT also expects another quarter of sequential ARPU growth in 2Q24e as it remains focused on improving monetisation of its users after several years of driving user growth. We remain positive about SPOT’s ability to keep churn low while raising prices as it delivers incremental value to its users through new products (Audiobooks, AI DJ, music videos) and platform improvements.

+ Meaningful cost benefits from reaching scale. SPOT has a variety of cost models for its different audio products, with most of its cost base comprised of revenue sharing (royalties) agreements with labels, and fixed content costs for podcasts. We believe that SPOT is beginning to see meaningful cost benefits from reaching scale as it: 1) leverages its distribution for more favourable agreements with its music partners and 2) continues to be more efficient with removing underperforming podcasts. Its 27.6% gross margin for 1Q24 (90/240bps QoQ/YoY) beat its own guidance by 120bps, with Premium gross margin of 30.2% and ad-supported gross margin of 6.4%.

The Negative

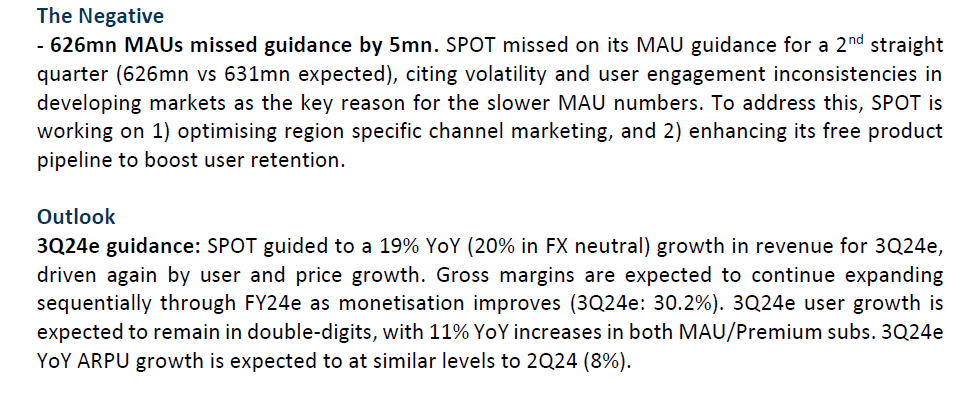

- 615mn MAU fell short of SPOT’s 618mn guidance. SPOT under-delivered on its MAUs for 1Q24, with 615mn MAUs and 3mn under its own guidance. The company attributed this to 3 main factors: 1) sequential slowdown in momentum after a very strong FY23, 2) slight disruption in BAU operations from its workforce reduction (-17% reduction) in Dec 23, 3) excessive pullback in marketing spend throughout FY23 (which has since been corrected).

Spotify Technology S.A. – Growth exceeds, monetisation to begin

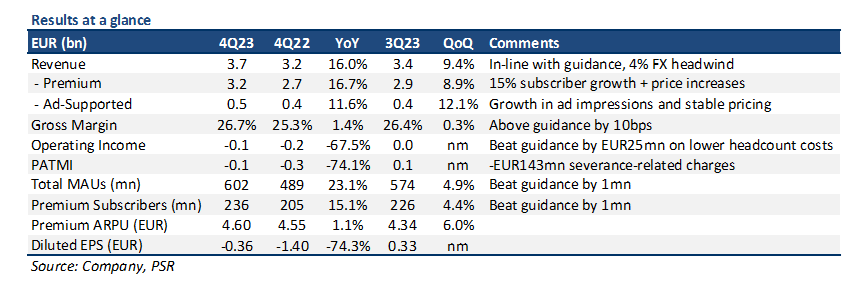

- 4Q23 results were within expectations. FY23 revenue was at 97% of our FY23e forecasts, with a net loss of ~EUR30mn more than our FY23e forecasts. SPOT added 113mn/31mn MAU/Premium Subs in FY23.

- MAU/Premium Subs outperformance keeping SPOT’s growth story intact; revenue growth of 16% YoY (20% FX neutral) accelerating into FY24e.

- Margins and profitability at an inflection point due to SPOT reaching scale; we expect a ~250bps increase in FY24e gross margin due to better monetisation.

- Due to increasing scale and operating leverage, we raise our FY24e PATMI by ~4x to EUR593mn. Our revenue forecast remains unchanged. We roll over an additional year of valuations and maintain our ACCUMULATE recommendation with a raised DCF target price of US$270 (prev. US$190) to reflect our assumptions. Our WACC/growth rate of 7.5%/4% remains unchanged.

The Positives

+ Revenue growth accelerating into FY24e with 28mn new MAUs, 10mn new premium subscribers. SPOT again exceeded its user growth expectations with 23%/15% YoY growth in MAU/Premium Subs. It ended FY23 adding 113mn monthly users, and 31mn new premium subscribers (Figure 1). MAU growth is extremely important for SPOT as it is the main channel used to convert free-to-listen users into premium subscribers. The outperformance in users, together with price increases mid-4Q23, drove an acceleration in revenue growth (4Q23: 16% YoY vs 3Q23: 11% YoY) – with SPOT also expecting growth to accelerate in FY24e.

+ Positive commentary on margins, focusing on monetisation for FY24e. Management was positive on its expanding margins, with 4Q23 gross margin of 26.7% 10bps above guidance. SPOT spent much of FY23 working on being more efficient in terms of investments and costs, from laying off employees to cutting non-performing content. Moving into FY24e, we expect gross margins to expand by ~250bps with sequential increases QoQ, driven by: 1) price increases; 2) improving efficiencies of scale; 3) better monetisation of Podcasts and advertising; and 4) improved deals with record labels/agencies.

+ Remaining focused on prudent spending moving forward. SPOT provided some near-term clarity for spending, saying that it would raise investment hurdle rates, and remain prudent on future spending – as it looks to balance growth and profitability. We forecast FY24e OPEX to decline -5% YoY due to the lumpiness of spend in FY22 and FY23, but to remain in line with its long-term linear trend. Long-term growth remains a key focus for SPOT, but we expect FY24e to be a year of monetising its ever-growing user base given its latest commentary.

The Negative

- Nil.

MAU (Monthly Active User): average number of active users during a month.

Get access to all the latest market news, reports, technical analysis

by signing up for a free account today!

Login

The full article is only available for premium content subscribers. To continue reading this article, please log in:

Not a Premium Content Subscriber yet? Sign up here!

- Home >

- Phillip Research Report