The Positives

+ Treasury income continues to climb. 1H24 total treasury income on collateral balances held in trust surged 47% YoY to S$67mn from 1H23’s treasury income of S$47mn. The increase was mainly due to higher average yields on margin deposits, partially offset by a decrease in margin balances. However, this was lower than the record high of S$90mn reached in 2H23. Notably, 1H24’s treasury income contributed 20% to PBT, similar to the contribution in full-year FY23.

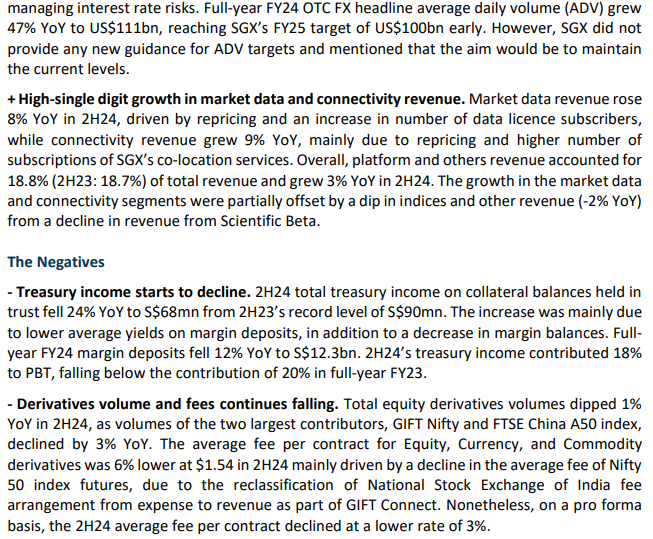

+ FICC – Currency and commodities surges. FICC - Currency and commodities trading and clearing revenue surged 30% YoY to S$148mn in 1H24, as volumes increased in commodity and currency derivatives, primarily from iron ore futures (up 49% YoY in 1H24) and USD/CNH FX futures; as well as higher contribution from OTC FX. SGX’s OTC FX business average daily volume spiked 46% YoY to US$100.1bn, on target to reach SGX’s FY25 target of US$100bn, and contributed S$40.9mn, or 7%, to 1H24 revenue. The increase was primarily due to higher volumes in currency swaps from clients managing interest rate risks.

+ Platform and Others revenue rose 8% YoY. Platform and Others revenue accounted for 20.3% (1H23: 19.5%) of total revenue and grew 8% YoY to S$120mn in 1H24. Market data revenue rose 10% YoY, driven by higher revenue realised from Securities and Derivatives Market Direct Feed subscribers, as well as growth in distribution of Commodities data, while connectivity revenue grew 9% YoY, mainly due to higher revenue from co-location subscribers. Indices and other revenue increased 7% YoY mainly from higher revenue contribution from Energy Market Company and Indices.

The Negatives

- Listing revenue continues decline. FICC - Fixed Income revenue fell 8% YoY in 1H24, dragged down by lower listing revenue. There were 489 bond listings raising S$132bn in 1H24 (2H22: 449 bond listings raised S$104bn). On Cash equities, revenue was 6% lower YoY in 1H24 mainly due to listing revenue declining 3% YoY and trading and clearing revenue falling 14% YoY as daily average traded value, total traded value, and overall average clearing fees fell. Overall, equities revenue accounted for 54% (1H23: 60%) of revenue and fell 6% YoY to S$320mn in 1H24.

- Derivatives volume and fees dip. Total equity derivatives volumes dipped 14% YoY in 1H24, as volumes of GIFT Nifty and FTSE China A50 index futures contracts declined. The average fee per contract for Equity, Currency, and Commodity derivatives was lower at $1.54 in 1H24 (1H23: $1.58) mainly driven by a decline in the average fee of Nifty 50 index futures, due to the reclassification of National Stock Exchange of India fee arrangement from expense to revenue as part of GIFT Connect. Nonetheless, on a pro forma basis, the 1H24 average fee per contract rose slightly to $1.54 (1H23: $1.53).

The Positives

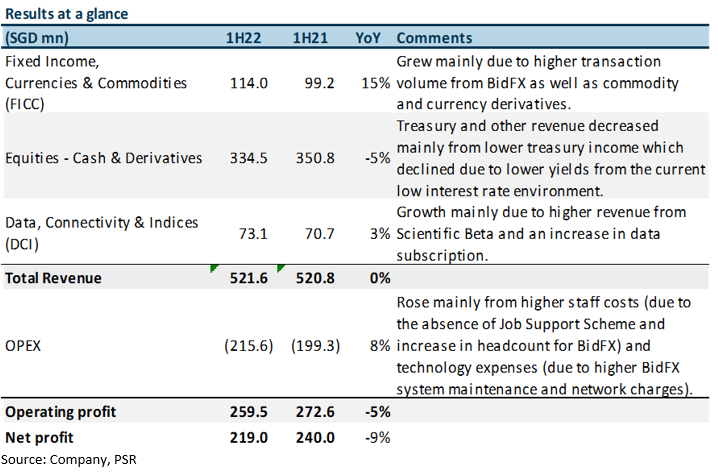

+ Treasury income surges to record levels. Treasury and other income surged 141% YoY to S$111mn in 2H23 mainly due to higher interest earned from customer collateral balances. 2H23 treasury income on collateral balances held in trust was reported at S$90mn, which surged 221% YoY from 2H22’s treasury income of S$28mn. Notably, full-year FY23’s treasury income of S$137mn contributed 20% to PBT and reached a record level, surpassing the previous high of FY20’s treasury income of S$135mn.

+ Higher fees from FTSE China A50 and Nifty 50 contracts. Despite equity derivatives volumes dipping 17% YoY in 2H23, Equities - Derivatives trading and clearing revenue only fell 10% YoY, as the lower volumes were offset by higher average fees from SGX Nifty 50 Index futures and SGX FTSE China A50 Index futures contracts. Average fee per contract for Equity, Currency and Commodity derivatives was higher at $1.61 in FY23 (FY22: $1.51) from an increase in higher fee-paying customers for SGX FTSE China A50 Index futures and Nifty 50 Index futures, coupled with strong volume growth in Iron Ore.

+ FICC – Currency and commodities continue growth. FICC - Currency and commodities trading and clearing revenue - rose 19% YoY to S$118mn in 2H23, as volumes increased in commodity and currency derivatives, primarily from iron ore futures (up 37% YoY in 2H23) and USD/CNH FX futures; as well as higher contribution from OTC FX. SGX’s OTC FX business (BidFX, MaxxTrader and Electronic Communication Network (ECN)) average daily volume grew 7.3% YoY to US$75.8bn with a target of US$100bn by FY25, and contributed S$39.2mn, or 6%, to 2H23 revenue. SGX said that it is on track to reach its ADV target of US$100bn as clients settle into the new platform.

The Negatives

- Listing revenue continues to dip. FICC - Fixed Income revenue - fell 28% YoY in 2H23 dragged down by lower listing revenue. There were 469 bond listings raising S$139bn in 2H23 (2H22: 687 bond listings raised S$220bn). On Cash equities, revenue was 12% lower YoY in 2H23 mainly due to listing revenue declining 9% YoY and trading and clearing revenue falling 21% YoY as daily average traded value, total traded value and overall average clearing fees fell. Overall, equities revenue accounted for 59% (2H22: 63%) of revenue and was flat YoY at S$365mn in 2H23, as the growth in Equities – Derivatives revenue pulled up the decline in the Equities – Cash business.

- Data, Connectivity and Indices (DCI) business growth flat. DCI revenue accounted for 12% (2H22: 13%) of total revenue and was flat YoY at S$75mn in 2H23. Market data and indices revenue dipped 4% YoY, mainly due to lower revenue from the index business. Nonetheless, this was offset by an increase of 5% YoY in connectivity revenue mainly due to the upselling of connectivity services to existing clients and the introduction of new GIFT Connect-related co-location and network services.

The Positives

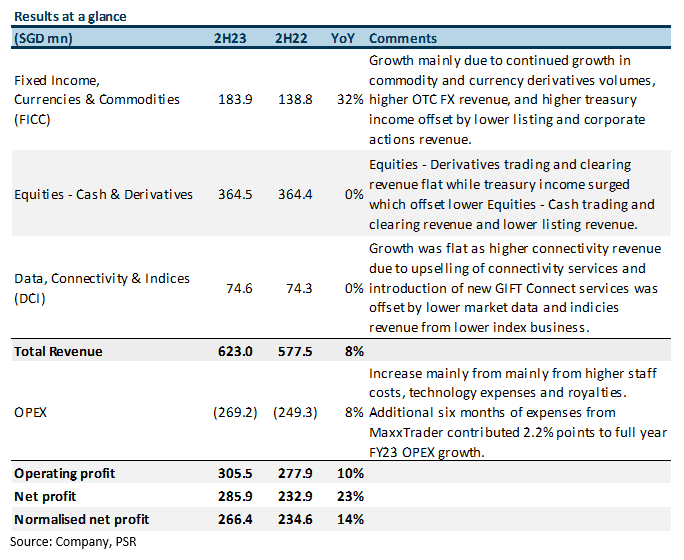

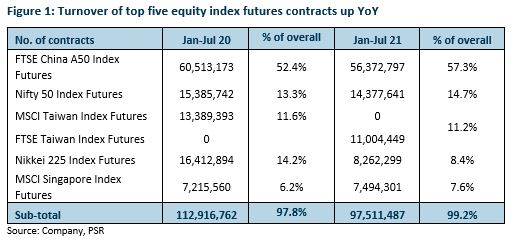

+ Treasury income surged in 1H23. Treasury and other income surged 85% YoY to S$73mn in 1H23 with higher interest rates earned from customer collateral balances. 1H23 treasury income on collateral balances held in trust was reported at S$47mn, which surged 124% YoY from 1H22’s treasury income of S$21mn and made up 96% of FY22’s treasury income of S$49mn.

+ Higher fees from FTSE China A50 and Nifty 50 contracts. Despite the flat growth of equity derivatives volumes of 1% YoY, Equities – Derivatives trading and clearing revenue grew 11% YoY to S$145.4mn in 1H23, mainly due to higher average fees from SGX Nifty 50 Index futures and SGX FTSE China A50 Index futures contracts. Average fee per contract for Equity, Currency and Commodity derivatives was higher at $1.58 (1H22: $1.50) mainly due an increase in proportion of higher fee-paying customers for SGX FTSE China A50 Index futures and higher fees realised from SGX Nifty 50 Index futures.

+ OTC FX business on track. SGX’s OTC FX business (BidFX, MaxxTrader and Electronic Communication Network (ECN)) average daily volume grew 34% YoY to US$68.4bn with a target of US$100bn in the medium term, and contributed S$36.2mn, or 6%, to 1H23 revenue. Consequently, FICC - Currencies and Commodities trading and clearing revenue grew 29% mainly due to increased volumes in commodity and currency derivatives and higher contribution from OTC FX. SGX said that it is on track to reach its ADV target of US$100bn as clients settle into the new platform.

The Negatives

- Lower listing revenue hurt Fixed Income and Cash businesses. FICC – Fixed Income revenue was down 35% YoY mainly due to lower listing revenue with 449 bond listings raising S$104.3bn in 1H23 (1H22: 492 bond listings raised S$209.4bn). On the Equities – Cash side, revenue was 10% lower YoY mainly due to listing revenue decreasing 13% YoY and trading and clearing revenue decreasing 11% YoY as daily average traded value, total traded value and overall average clearing fees declined. Overall, equities revenue accounted for 60% (1H22: 64%) of revenue and grew 3% YoY to S$344.7mn, as the growth in Equities – Derivatives revenue pulled up the decline in the Equities – Cash business.

- Data, Connectivity and Indices (DCI) business dipped in 1H23. DCI revenue accounted for 13% (1H22: 14%) of total revenue and decreased 1% YoY to S$0.6mn as market data and indices revenue dipped 8% YoY, mainly due to lower revenue from the index business. Nonetheless, this was offset by an increase of 9% in connectivity revenue mainly due to an increase in subscription of co-location services.

Outlook

Continued development of multi-assets to anchor long-term growth. SGX remains committed to expanding its suite of products through strategic partnerships and new product development for newly acquired businesses.

Investing for the medium term. SGX has maintained their guidance of FY23 expenses growth of 7-9% from FY22. This includes ~2% growth from the full-year impact of the acquisition of MaxxTrader. However, expectations are expenses growth will be at the lower end of guidance (7%). The higher expenses are mainly from the buildout of their OTC FX business and higher staff costs from salary increments. With that, SGX expects medium-term expense guidance to remain at mid-single digit growth.

Rising interest rates. Apart from the banks, SGX is another beneficiary of higher interest rates, and treasury income is expected to recover with rising interest rates. As at FY22, SGX reported a S$14bn float from collateral and S$49mn of interest income, which represents 10% of FY22 net income. 1H23 treasury income of S$47mn is currently at 97% of FY22’s. In comparison, in FY20, SGX reported interest income of S$135mn and earned a yield of 98bps on collateral balances when the Fed fund rate peaked at 2.50%. We believe there is a huge upside in their treasury income with the potential to more than triple with the current high interest rate environment.

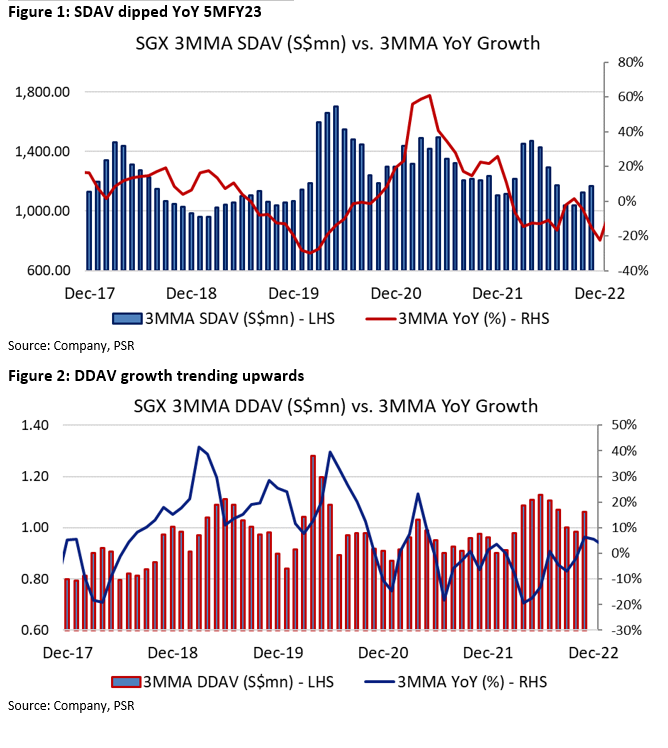

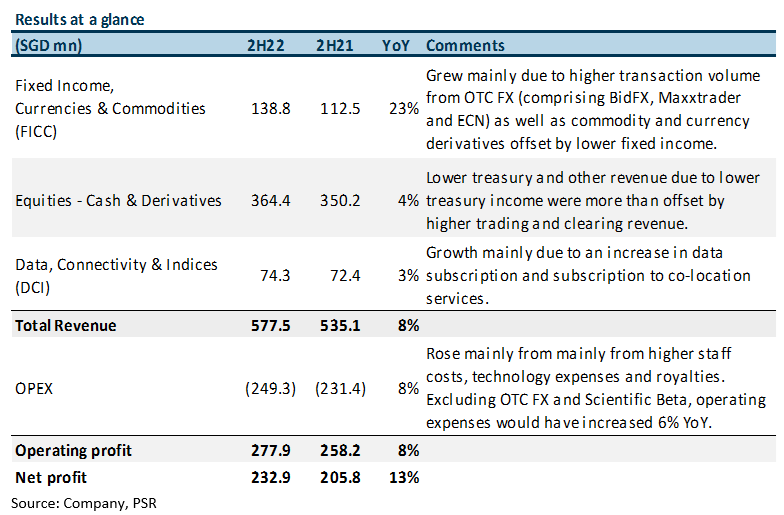

Securities volumes dip while derivatives volumes trend upwards

SGX’s securities volume is trending downwards, with the 5MFY23 securities daily average volume (SDAV) down 10.5% YoY at 1,095mn contracts as the market sentiment remained subdued due to macroeconomic factors, and the volumes moderated from a record year in FY22. However, SGX’s derivatives volume is trending upwards, with the 5MFY23 derivatives daily average volume (DDAV) up 9.4% YoY. As market volatility continues to rise, derivatives volume can climb for the rest of FY23e.

Treasury income to tick up in FY23

Treasury income dipped in FY21 and FY22 due to the low interest rate environment (Figure 3). However, we expect a rebound in treasury income in FY23e by 8%. Looking at the chart below, we can see that SGX’s treasury income is lagging behind the Fed Fund Rates. As a majority of SGX’s collateral balances (FY22: S$13.9bn) are placed in Fixed Deposits (FDs) with the tenure spread out, certain deposits have not matured yet and the interest rates have not been refreshed. Nonetheless, moving into FY23 we should expect the treasury income to recover to pre-pandemic levels as they get placed into higher interest FDs. In FY20, SGX earned a yield of 98 basis points on collateral balances when Fed fund rate peaked at 2.50%.

The Positives

+ New businesses accelerated growth. With the acquisition of MaxxTrader in Jan 2022, SGX’s OTC FX (BidFX, MaxxTrader and Electronic Communication Network (ECN)) average daily volume grew 64% YoY to US$70.6bn with a target of US$100bn in the medium term, and contributed S$55mn, or 5%, to FY22 revenue. Consequently, FICC and DCI grew 23% and 3% YoY respectively to boost revenue growth. Both businesses are expected to remain growth engines for SGX, with opportunities from cross-selling and new client acquisitions on the back of customer access to an enlarged trading network.

+ Underlying business resilient. Excluding treasury income, revenue grew 7% YoY, lifted by higher trading and clearing revenues from equity derivatives, currencies, and commodities. Treasury and other revenue income dropped as treasury income was affected by lower yields from low interest rates.

+ FTSE China A50 and Nifty 50 contracts continue to grow. Despite the introduction of HKEX’s MSCI China A50 Connect Index in Oct 2021, SGX’s FTSE China A50 contract saw increased volume, with growth of 9% YoY. SGX expects trading activity and open interest of the FTSE

China A50 contract to continue growing as the international A- share market expands. SGX’s Nifty 50 contract also showed increased volume and grew 14% YoY.

The Negatives

- Equities – Cash revenue and treasury income dip. Equities – Cash revenue was 6% lower YoY mainly due to corporate actions and other revenue dipping 14% YoY and trading and clearing revenue decreasing 9% YoY as daily average traded value, total traded value and overall average clearing fees declined. On the Equities – Derivatives side, treasury revenue was down 50% YoY to S$28.6mn mainly from treasury income, which declined primarily due to lower net yield. Nonetheless, this was offset by an increase of 22% YoY in trading and clearing revenue as equity derivatives volume increased 4% YoY and higher fees per contract of S$1.51 in FY22 (FY21: S$1.34), 13% higher YoY. Overall, equities revenue was stable YoY at S$699mn and accounted for 64% (FY21: 66%) of revenue.

Outlook

Continued development of multi-assets to anchor long-term growth. SGX remains committed to expanding its suite of products through strategic partnerships and new product development for newly acquired businesses.

Investing for the medium term. SGX has guided FY23 expenses to grow 7-9% from FY21. This includes ~2% growth from the full year impact of the acquisition of MaxxTrader. The higher expenses are mainly from the buildout of their OTC FX business and higher staff costs from salary increments. With that, SGX expects medium-term expense guidance to remain at mid-single digit growth.

Rising interest rates. Apart from the banks, SGX is another beneficiary of higher interest rates, and treasury income is expected to recover with rising interest rates, with SGX’s management mentioning that the low treasury income is to remain for the following months, with only an uptick expected later in the year. As at FY21, SGX reported a S$12bn float from collateral and S$72mn of interest income which represents 13% of FY21 operating profit. Based on our calculations, a 25 basis point rate hike would mean an increase of S$30mn in operating profit (or a 6% uplift).

The Positives

+ New businesses accelerated growth. Newly acquired BidFX and Scientific Beta contributed S$40mn, or 8%, to 1H22 revenue, which is 20% higher YoY. Consequently, FICC and DCI grew 15% and 3% YoY respectively to mitigate Equities - Cash & Derivatives revenue decline. Both businesses are expected to remain growth engines for SGX, with opportunities from cross-selling and new client acquisitions on the back of customer access to an enlarged trading network.

+ Underlying business resilient. Excluding treasury income, revenue grew 6% YoY, lifted by higher trading and clearing revenues from equity derivatives, currencies, and commodities. Treasury and other revenue income dropped as treasury income was affected by lower yields from low interest rates.

+ FTSE China A50 contract showed growth. Despite the introduction of HKEX’s MSCI China A50 Connect Index in Oct 2021, SGX’s FTSE China A50 contract saw increased volume, with open interest growing at more than 10% between Oct and Dec 2021. SGX expects trading activity and open interest of the FTSE China A50 contract to continue growing as the international A-share market expands.

The Negatives

- Lower yields drag equity derivatives treasury income. Equities - Cash & Derivatives was 5% lower YoY as equity derivatives volume declined 4%. This was mitigated by higher fees per contract of S$1.50 in 1H22, 18% higher YoY and in line with our expectations as introductory fees in 1H21 tapered off. 1H22 treasury and other revenue declined 46% YoY mainly from lower treasury income, which declined primarily due to lower yield. Nonetheless, this is expected to recover with rising interest rates, with SGX’s management mentioning that the low treasury income is to remain for the following months, with only an uptick expected later in the year.

Outlook

Continued development of multi-assets to anchor long-term growth. SGX remains committed to expanding its suite of products through strategic partnerships and new product development for newly acquired businesses.

Investing for medium term. SGX has guided FY22 expenses of S$565m-575mn, an 8.6% increase from FY21 at the mid-point. More than 50% of the increase will be for near-term investments. These include setting up FX ECN, climate-related initiatives and continued investments in BidFX and Scientific Beta. However, this guidance includes expenses for Maxxtrader, which was previously not included in their earlier guidance. With that, SGX expects FY22 expenses to remain flat or marginally higher compared with FY20’s pre-acquisition expense of S$475mn.

Rising interest rates. Apart from the banks, SGX is another beneficiary of higher interest rates. As at 2H21, SGX reported a S$12bn float from collateral and S$72mn of interest income which represents 13% of FY21 operating profit. Based on our calculations, a 25 basis point rate hike would mean an increase of S$30mn in operating profit (or a 6% uplift).

The news

HKEX has announced that it will launch a financial derivative in October this year for investors to hedge their risks of investments in China’s A-share market following green light from Hong Kong’s Securities and Futures Commission. HKEX has agreed with the MSCI to launch a US-dollar futures contract based on the MSCI China A50 Connect Index. This index tracks the performance of the 50 key Shanghai and Shenzhen stocks available via the Stock Connect.

The new derivative would help to plug a gap in the financial instruments and regulations that link China with Hong Kong, where the Shanghai-Hong Kong Stock Connect handles about HK$5bn a day in cross-border transactions. The A-share futures will enable offshore investors to hedge risks by taking contrarian positions to their underlying assets.

The Negatives

- Direct competition with FTSE China A50 Index Futures. The MSCI China A50 Connect Index Futures could divert trading volume away from the FTSE China A50 Index Futures on the SGX. This is the only A share futures available for offshore investors to date. The FTSE China A50 Index Futures has the largest turnover of equity index futures for the SGX, accounting for 57.3% of total equity index futures traded, up from 52.4% last year (Figure 1). Even though SGX does not provide a revenue for its China A50 contract, we estimate it contributed about 20% to its overall derivatives revenue and 10% to its overall revenue in FY21.

China’s importance in the global investment market is growing. The country’s weighting in the MSCI Emerging Markets Index increased from 18% at the end of December 2009 to 34% in August 2021. We believe growing demand for A-share futures will help to compensate for some of the volume that could be diverted to the HKEX’s MSCI China contract.

Moreover, SGX’s transition away from the MSCI to FTSE’s suite of products could potentially enhance client’s stickiness. We have seen this for its Taiwan index futures. The previous launch of a non-China related equity derivatives product by HKEX had a limited impact on SGX’s derivatives volume, as it was able to migrate to the FTSE product suite and maintain its leadership in Taiwan index contracts.

Outlook

Continued development of multi-assets to anchor long-term growth. SGX remains committed to expanding its suite of products through strategic partnerships and new product development for newly-acquired businesses.

Investing for medium term. SGX has guided for FY22 expenses of S$565-575mn, an 8.6% increase from FY21 at the mid-point. More than 50% of the increase will be for near-term investments. These include setting up FX ECN, climate-related initiatives and continued investments in BidFX and Scientific Beta.

Investment Actions

Maintain NEUTRAL with lower TP of S$10.78, from S$11.54. Our TP is still pegged to +2SD of its 5-year mean or 25x P/E (Figure 3). FY22e earnings have been reduced by 6.1% as we factor in lower volumes for its FTSE China A50 contracts. We believe the near-term impact could be cushioned by the usual adoption time of 3-5 years by global investors for the new MSCI China

At its recent Analysts’ Day, SGX detailed its plan to strengthen its core businesses and invest in its next leg of growth.

The Positives

+ Focus on building multi-asset exchange. SGX remains committed to expanding its suite of products through strategic partnerships and new product development for newly-acquired businesses with the aim of serving clients end to end. Fixed Income, Currencies and Commodities (FICC) and Data Connectivity and Indices (DCI) made up 33% of its revenue in 1HFY21, up from 20% in FY15 (Figure 1).

FICC and DCI will remain its growth engines, providing opportunities from cross-selling and new client acquisitions to an enlarged trading network. The exchange will deploy proceeds from its recent bond issuance of S$380mn to scale up its presence in FICC and DCI.

+ Pipeline for growth includes acquisitions, accelerating growth of Scientific Beta and building an integrated forex marketplace. The bourse is seeking out M&As to build capabilities in newer segments. It will seek “fill the gap” deals that will enhance its end-to-end offerings to clients. Its recent acquisitions of Scientific Beta and BidFX is a case in point.

The acquisition of Scientific Beta, a smart beta firm in January 2020, for €186mn or S$280mn in cash is expected to be earnings-accretive in FY21e. Over 60 asset owners and asset managers use Scientific Beta’s indices to track or benchmark their smart beta investments. We estimate about 30% of these assets under replication were integrating ESG dimensions. We see the bourse relying on Scientific Beta to create new products to mitigate the loss of MSCI product volumes.

+ Healthy pipeline for rest of 2021. The bourse reports a healthy pipeline of potential listings across sectors and geographies. With market infrastructure and processes in place, it also sees the potential for increased secondary listings of unicorns from the US via its Nasdaq partnership.