Singapore Telecommunications Ltd – The Giving Pledge

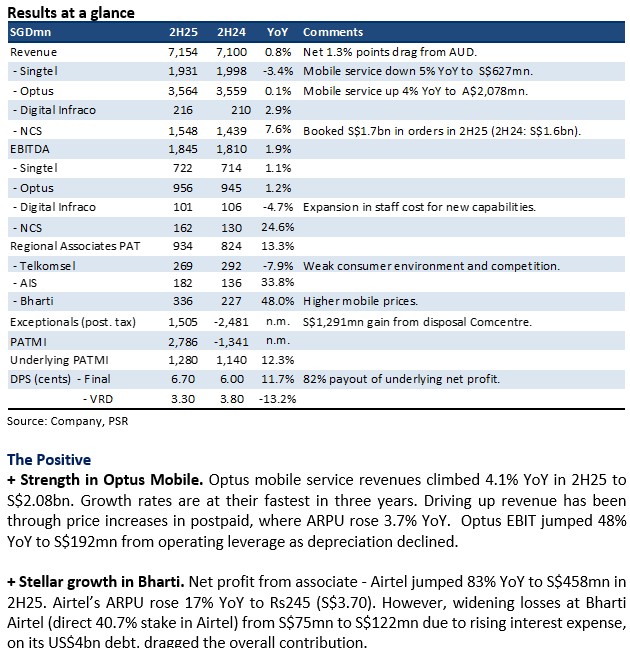

- 2H25 results were within expectations. Revenue and underlying PATMI were 97%/99% of our FY25e forecast. The 12% YoY rise in underlying net profit to S$2.78bn was supported by a 48% rise in Optus EBIT and 48% growth in associate Bharti earnings.

- The mid-term asset recycling target has been raised from S$6bn to S$9bn. Proceeds from assets recycled continue to be distributed as a value realisation dividend of 3 to 6 cents annually. Singtel will add a S$2bn share buyback over three years. Core dividend remains a payout ratio of 70-90% of the underlying net profit.

- Our ACCUMULATE recommendation is maintained. We raised our target price to S$4.40 (prev. S$3.77). We narrowed our discount to associates from 20% to 15% as Singtel intensifies its monetisation efforts. We raised the EV/EBITDA of the subsidiaries from 6x to 7x due to the stronger operating performance. Lowering the discount on associates invariably leads to more volatility and momentum in our target price. Operationally, mobile price repair and operating leverage are underway in Optus. Conversely, Singapore mobile remains under intense competition but is undertaking a significant realignment of costs. We believe asset monetisation efforts will be from disposing of the 7.7% stake in Gulf Development (~S$2bn) and another 3% in Bharti Airtel (~S$5bn).

Singapore Telecommunications Ltd – Earnings spike in India and Australia

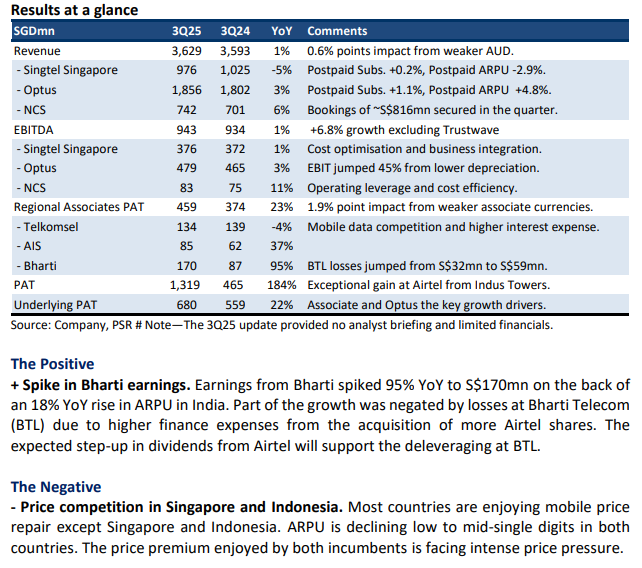

- 3Q25 results were within expectation. 9MFY25 Revenue and EBITDA were 73%/75% of our FY25e forecast. PATMI exceeded estimates at 79% of FY25e due to stronger than-expected performance from associate Bharti. Dividend guidance for FY25e was around 16.6 cents, higher than our initial estimate of 15.9 cents.

- Singapore continues to face revenue pressure from mobile competition, dragging down Average Revenue Per User (ARPU) and structural weakness in legacy voice. Recovery in Optus gains momentum, with EBIT jumping 43% YoY in 3Q25 to S$91mn. Aggressive cost-cut measures and revenue growth were the key drivers.

- Our ACCUMULATE recommendation is maintained. We raise our target price to S$3.77 (prev. S$3.44) due to mark-to-market gains in associates. Revenue and EBITDA forecast remained unchanged, but PATMI raised 6% to incorporate higher associate earnings and lower depreciation. Multiple growth drivers are underway, including Optus, NCS, and Bharti. We expect S$6bn monetisation to be gradually realized from stakes in Intouch and Bharti Airtel.

Singapore Telecommunications Ltd – Positives in Australia and asset monetisation

- 1H25 results were within expectation. Revenue and EBITDA were 48%/51% of our FY25e forecast. Optus continued its commendable performance with EBITDA growth of 10% YoY in 2Q25 from cost savings and rising prices.

- Associate earnings fell 3% YoY to S$411mn in 2Q25. Mobile competition in Telkomsel has hurt earnings together with expanded losses at Bharti Telecom due to higher interest rates. Singtel has raised their EBIT growth guidance for FY25e from “high single digit to low double digits” to “low double digits”.

- Our ACCUMULATE recommendation and target price of S$3.44 is maintained. We reduced our FY25e associate earnings but offset by a reduction in effective tax. PATMI is unchanged. Cost-out efforts in Singapore and Australia are supporting a recovery in margin. There is no change in the strategy to monetize S$6bn of assets including Intouch, Comcentre and Bharti Airtel.

Singapore Telecommunications Ltd – Eyeballing cost and AI opportunity

- 2024 Investor Day: The effects of higher mobile prices in Australia, India, and Thailand will flow into upcoming quarters via higher margins. The S$200mn cost out p.a. in Optus and Singapore are on track together with an additional 20% cut in S$150mn corporate cost. Capital expenditure has peaked and will gradually decline.

- The most exciting division is Digital Infrastructure, which has three major growth drivers. Firstly, data centre (attributable) capacity will almost triple from 62MW currently to 166MW by 2026. Besides capacity, a new GPU-as-a-service revenue streaming service utilising Nvidia AI chips will be rolled out. Finally, revenue from its patented Paragon platform is beginning to surge as deployment is underway in multiple countries.

- We maintain our ACCUMULATE recommendation with an unchanged target price of S$3.44. We expect earnings growth to be largely driven by cost savings, higher mobile prices, and data centre capacity. Paragon and GPU-as-a-Service are two new growth drivers and share price catalysts. AI is also an opportunity for NCS as a catalyst for new application and integration projects. The pace of earning growth for the group will depend on currency and the health of consumer spending, especially in Thailand and Australia.

Singapore Telecommunications Ltd – Prices are up, costs down, but currency headwind

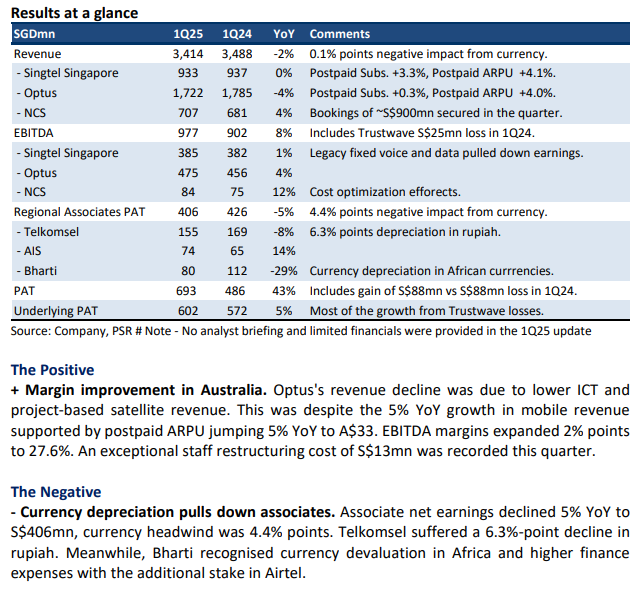

- 1Q25 results were within expectation. Revenue and EBITDA were 23%/25% of our FY25e forecast. Optus reported stronger margins offset by weaker associate income due to currency depreciation. 1Q25 net profit growth was largely driven by an absence of losses in Trustwave.

- Associate earnings were down 5% YoY to S$406mn. A weaker Indonesia rupiah pulled down Telkomsel's net profit by 6.3% points. Bharti suffered from Nigerian Naira translation losses and higher interest expenses from the additional stake in Airtel.

- Our ACCUMULATE recommendation and target price of S$3.44 is unchanged. We nudge our PATMI by 2% to account for lower depreciation. Optus operations are benefiting from the planned S$200mn cost-out plans p.a. Associates will benefit from higher mobile price plans, especially India’s repricing in July. Currency depreciation will be the headwind. Further monetization of assets will be a share price catalyst.

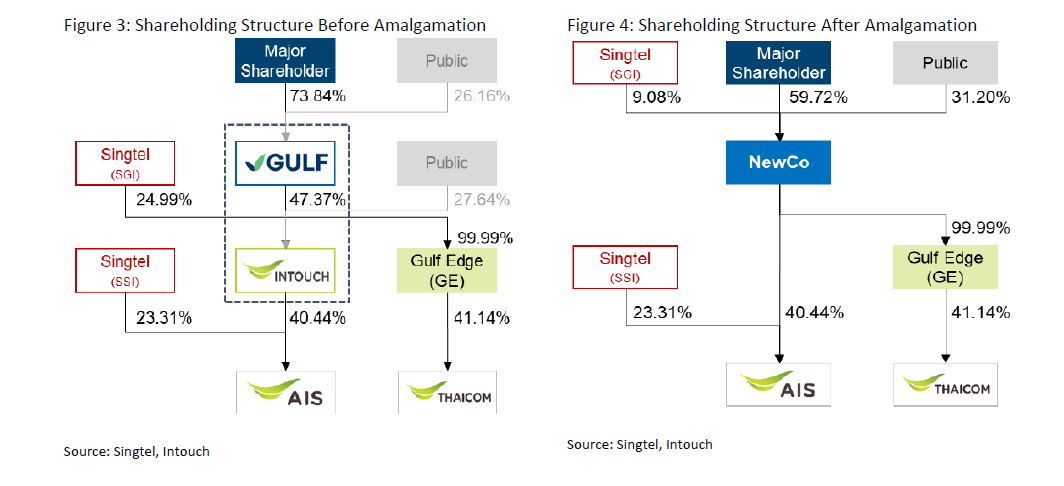

Singapore Telecommunications Ltd – Adding liquidity to associates

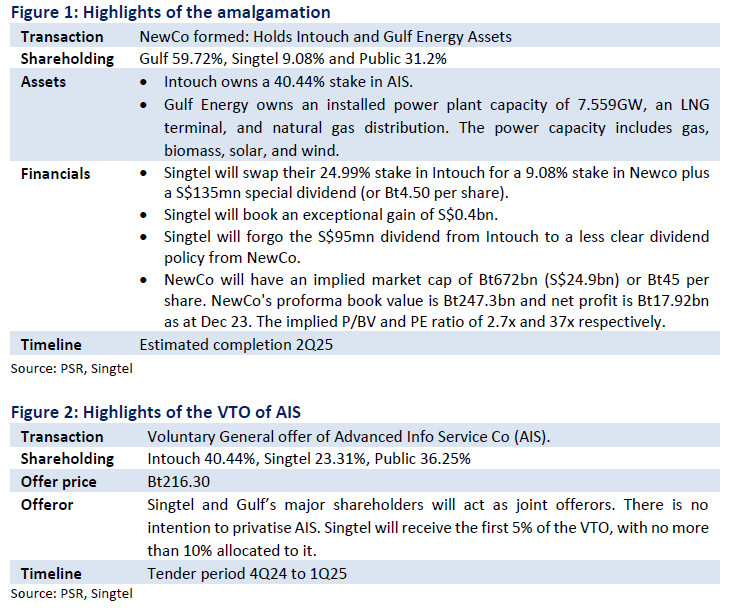

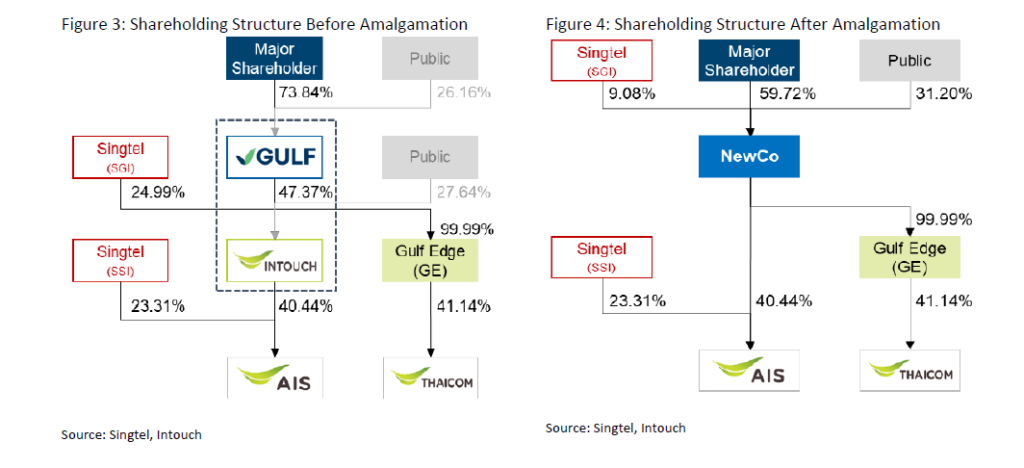

- A new company (NewCo) will be created to own Singtel’s 24.99% stake in Intouch and Gulf Energy Development’s assets such as gas-fired and renewable power plants. In exchange, Singtel will own 9.08% of NewCo and receive S$135mn in special dividends.

- Singtel and Gulf Energy will launch a voluntary tender offer for the 36.25% stake in Advanced Info Service (AIS) they do not own. The offer price of Bt216.30 per share is below the closing price of Bt220. Therefore, we assume Singtel’s stake in AIS will remain unchanged at 23.31%.

- We are positive on the transaction. It partially monetises Singtel’s stake in Intouch and AIS with the S$135mn special dividend. Furthermore, the Intouch stake will become part of a much larger (and likely more liquid) Newco with a market cap of S$25bn. We believe the trade-off is lower dividends from Intouch into a faster-growing NewCo, propelled by the planned build-up of energy assets. The eventual listing of NewCo shares above the implied Bt45 per share will be a value accretive catalyst. We downgrade our recommendation from BUY to ACCUMULATE due to the recent price rally. Our target is raised from S$3.00 to S$3.44 as we lower the discount on associates from 30% to 25%. The discount is narrowing as Singtel moves closer to achieving its S$6bn divestment target. No change in our forecast.

Key Highlights

There are essentially two transactions. The first is to amalgamate Intouch and Gulf Energy Development (Gulf Energy) assets in a new company (NewCo). The second transaction involves a voluntary tender offer (VTO) of Advanced Info Service (AIS).

Singapore Telecommunications Ltd – Down Under is turning around

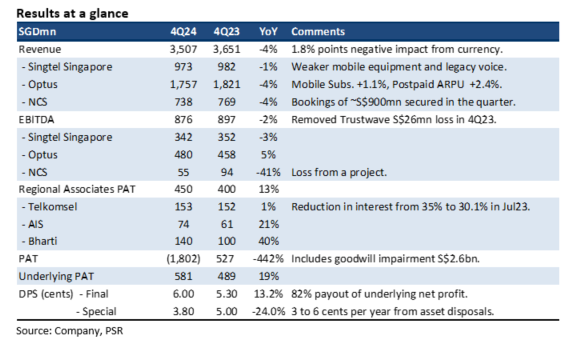

- 4Q24 revenue was within expectations, with FY24 revenue at 97% of our EBITDA exceeded 105% of forecasts due to higher other income and Optus margins. The final dividend was raised by 13% to 6 cents and an inaugural “value realisation dividend” (or recurrent special) of 3.8 cents.

- Optus managed to expand 4Q24 EBITDA margins to the highest in six quarters. Headcount at Optus declined by 12% over the past twelve months. Mobile price repair is also underway with postpaid ARPU rising 2.4% YoY.

- We maintain BUY with a higher target price of S$3.00 (prev. S$2.80). We raised our FY25e EBITDA by 5% and the market valuations of associates are higher. We see multiple earnings and share price drivers for Singtel. These include (i) S$200mn p.a. cost down in Australia and Singapore. FY24 combined headcount is down almost 7% YoY; (ii) S$300-400mn EBITDA opportunity in GPU-as-a-Service; (iii) planned asset disposals of S$6bn; (iv) recovery in associate earnings post current de-valuation in Airtel Africa, growth in home broadband and higher mobile prices. The dividend yield is now 6.2%.

The Positive

+ Margin recovery in Optus. Optus 4Q24 EBITDA margin of 27% was the highest in six quarters. The recovery was due to aggressive cost management. Headcount was lowered by 12% YoY to 6,313. The lower cost structure will carry into the FY25e. Another driver to earnings has been the growth in mobile service revenue of 5% YoY in 4Q24 as postpaid ARPU and subscribers creep up.

The Negative

- Weakness in Singapore and NCS. Singapore's profitability was negatively impacted by lower equipment sales and constant drag from legacy voice services. Weakness in margin was due to higher staff, selling, and administrative costs. NCS's drop in earnings was due to a loss from an undisclosed project. Earnings would have grown, excluding this impact.

Singapore Telecommunications Ltd – Accounting spring cleaning, sprinkled with cash

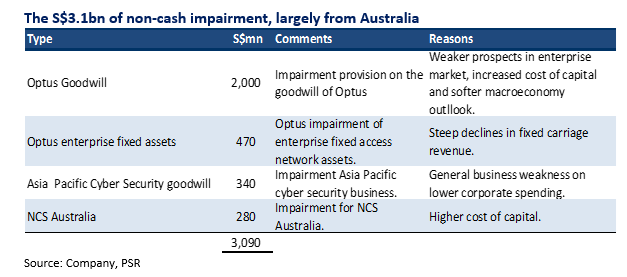

- Singtel announced exceptional non-cash impairment provisions of around S$3.1 bn in 2HFY24. As a result, Singtel will report a net loss in 2H24. Reasons for the impairment include higher interest rates, the rollout of NBN, weaker enterprise spending, and softer macro conditions.

- Singtel also announced that Optus has signed an 11-year agreement to provide TPG Telecom with access to Optus mobile network sites in regional Australia. Optus will receive a service fee worth A$1.6bn over the 11 years. There is an A$900mn fixed fee and A$690mn variable as the Optus 5G network rolls out.

- We view the write-offs as one-offs without impacting our valuations. Singtel also made a S$1bn goodwill impairment on Optus in FY23. Sharing networks with TPG would be positive in terms of conserving cash flows and reducing excess capacity if TPG were to roll out its network. We maintain BUY with an unchanged target price of S$2.80. We expect Singtel's operational performance to improve as mobile price repair occurs in multiple countries. Other share price catalysts include plans to monetise S$4bn of assets further, S$600mn of operating expense savings, and GPU-as-a-Service with Nvidia.

The exceptional provisions will not impact Singtel’s dividend policy (70% and 90% of underlying net profit). Singtel is on track to pay at the upper end of its dividend policy for FY24 (PSR: 84% payout ratio).

Network sharing agreement between Optus and TPG Telecom

- What will Optus provide? Optus will provide TPG Telecom access to its 2,444 regional radio access network sites in regional Australia, of which only 200 are 5G enabled. Optus will accelerate its 5G sites in regional Australia to 1,500 by 2028 and 2,444 by end-2030. There is an option for TPG Telecom to extend the agreement for a further five years. Optus will receive total service fees of around A$1.6bn over the 11-year agreement (net of the spectrum fees A$1.17bn).

- What will TPG provide? TPG will license some of its spectrum to Optus. Optus will pay A$420mn over the entire 11-year term for the use of the spectrum, which allows Optus to improve the capacity of its network without requiring more network sites.

Singapore Telecommunications Ltd – Bruised by currency

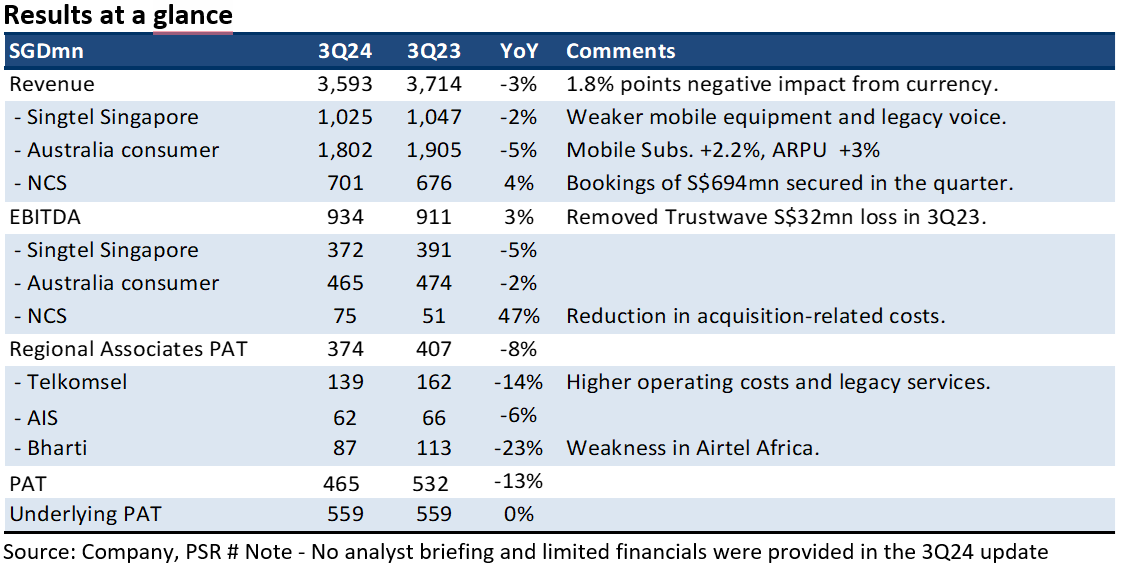

- 3Q24 earnings were within expectation. 9M24 revenue and EBITDA were 73%/75% of our FY24e forecast. Currency was almost a 2% point drag to earnings.

- 3Q24 associate contribution disappointed with an 8% YoY decline to S$374mn. Airtel Africa suffered a YTD24 translation of S$130mn following a massive depreciation of the Nigerian Naira during the quarter. Direct stake in Airtel Africa has been divested.

- We maintain BUY with an unchanged target price of S$2.80. We lowered our associate earnings by 10% due to the weakness in Airtel Africa. But this was offset by a lower finance expense assumption. Our FY24e PATMI is reduced by 3%. We expect an upside surprise in EBITDA margins in 4Q24 if Singtel can deliver its S$200mn of cost out by the end of FY24. Mobile price repair is underway in multiple countries where Singtel operates. We expect this to drive earnings together with plans to monetise S$4bn of assets further.

The Positive

+ Early mobile price repair in Australia. Optus postpaid ARPU of A$42 is the highest in more than four years. We believe price repair is underway. Competition, especially for entry-level price plans, has eased, and prices are edging higher. Despite the network outage, mobile service revenue grew 3.4% YoY.

The Negative

- Airtel Africa currency hit. Contribution from Bharti Telecom declined 23% YoY to S$87mn. Operations in India grew 14% YoY supported by an 8% rise in ARPU to Rp208. Currency took a toll on the results, with a 4% decline in the rupee against the Singapore dollar. A translation loss hit Africa operations due to the weakness in the Nigerian Naira.

Outlook

We expect mobile price recovery in Australia, India, Thailand, and Indonesia to drive earnings growth. An upside surprise in margins will stem from Singtel’s planned S$600mn reduction in core cost, largely in Optus.

Maintain BUY with unchanged TP of S$2.80

Our SOTP valuation is based on 6x EV/EBITDA (in line with peer valuation) for Singtel’s core Singapore and Australia businesses, and associates are marked to market after a 20% discount to reflect volatility in their share prices.

Singapore Telecommunications Ltd – Aggressively restructuring to reality

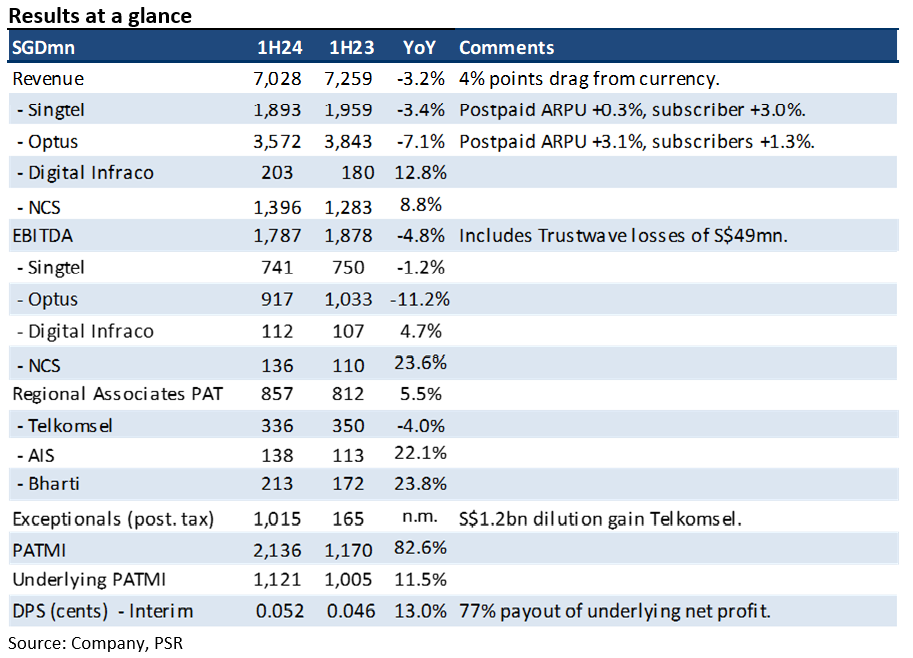

- 1H24 revenue and EBITDA were within our expectations at 46% of our FY24e forecast. EBITDA declined 5% YoY to S$1.78bn due to an 11% contraction in Optus earnings. Underlying net profit rose 11% to S$1.12bn despite a 4% point drag on currency.

- Singtel increased interim dividends by 13% to 5.2 cents and revised higher its payout ratio from 60-80% to 70-90%. A 3-year programme to remove S$600mn (of S$200mn p.a. FY24-26) of indirect cost was announced.

- We maintain BUY with an unchanged target price of S$2.80. Our earnings are largely unchanged before incorporating exceptional items. We believe Singtel is making significant strides in restructuring the entire group, monetising assets, and shedding unprofitable entities. Mobile competition in Australia is not abating and Optus needs to realign its cost structure to this reality. Underlying net profit in 1H24 fell 69% YoY to A$13mn.

The Positives

+ Increase in dividends and payout ratio. Singtel raised interim dividends by 13% to 5.2 cents. The company also increased its committed dividend payout ratio to 70-90% of underlying net profit (prev. 60-80%). Supporting dividends was FCF (plus associate dividends and lease payments) of S$817mn (1H23: S$1.29bn).

+ Strong margin expansion at NCS. NCS is beginning to contribute more significantly to group earnings. EBITDA expanded 24% YoY to S$136mn from revenue growth and cost optimisations. NCS booked S$1.4bn in orders in 1H24 (1H23: S$1.3bn). Much of the growth was outside the traditional government sector.

The Negative

- Still stubborn cost structure at Optus. Optus EBITDA declined 3% YoY to A$1.03bn despite revenues growing. There was an almost 50% jump in utility cost or an additional A$24mn. It was encouraging that staff costs have started to stabilise. 1H24 underlying net profit fell 69% ToT to A$13mn on lower operating earnings and higher finance costs. There was a staff restructuring cost of S$21mn under exceptionals, but which division was not disclosed.

Outlook

We believe management’s restructuring strategy is beginning to yield results:

- Of the planned $6bn of assets to be monetised in the near-term S$2bn has been unlocked*.

- Re-organising the group and resources into growth sectors has seen improvement in earnings at NCS and monetisation of the digital infrastructure division.

- Closure of Hooq (Mar20), divestment of Amobee (Jul22) and Trustwave (Oct23) has removed an estimated S$200mn of operating losses.

- The planned S$600mn cost out programme (or removal of S$200mn p.a. of indirect cost) from FY24 to FY26, will be a key initiative to lower fixed costs, especially at Optus.

Maintain BUY with unchanged TP of S$2.80

Our SOTP valuation is based on 6x EV/EBITDA (in line with peer valuation) for Singtel’s core Singapore and Australia businesses, at S$0.90/share. Associates are marked to market at S$1.90/share after a 20% discount to reflect volatility in their share prices.

Get access to all the latest market news, reports, technical analysis

by signing up for a free account today!

Login

The full article is only available for premium content subscribers. To continue reading this article, please log in:

Not a Premium Content Subscriber yet? Sign up here!

- Home >

- Phillip Research Report