The Positives

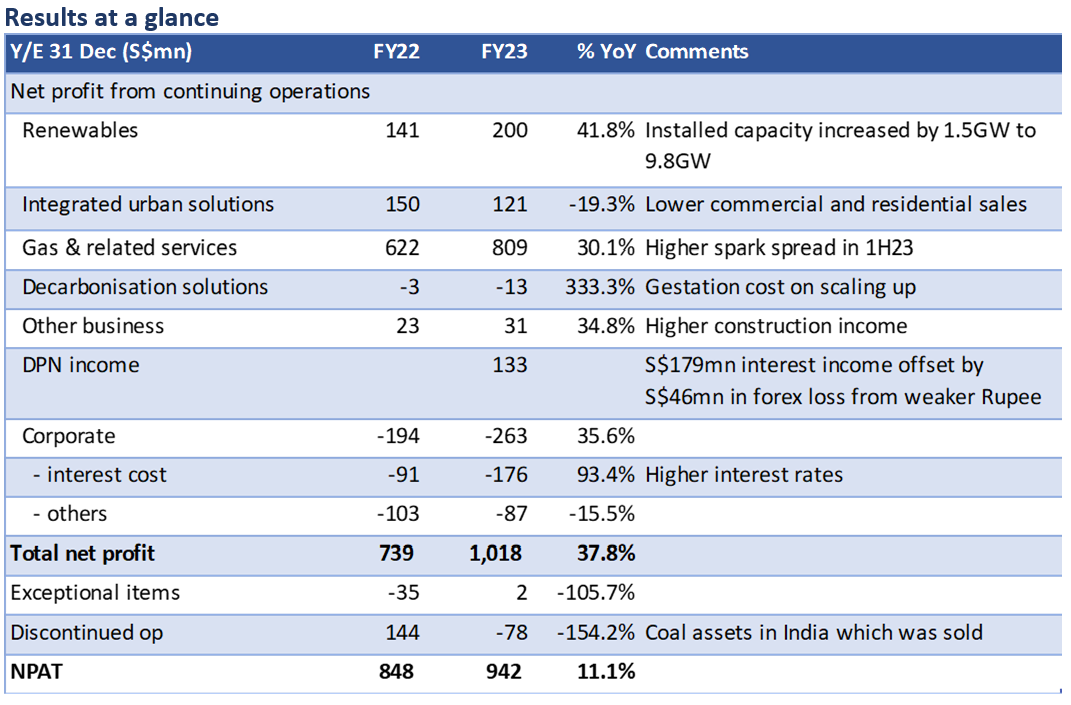

+ Singapore gas energy portfolio has locked in 99% of its capacity on contracts with average tenure of 12 years. These contracts are on a pre-determined dollar margin, with cost passed through to the customers. This provides visibility and stability to about 65% of earnings, making them highly visible and stable. The small spot market suggests that this is a sellers’ market, as customers are keen to lock in to ensure supply. SCI’s 600MW hydrogen-ready cogen plant will be completed in early 2026.

+ Renewable capacity increased by 4GW to 13.8 GW, of which 9.8 GW (+18.1% YoY) is operational. These are achieved through acquisitions as well as organic growth with key partners in China, India, and Southeast Asia. The power is sold to the grid and billed to the energy authority on a timely basis, cutting down on merchant risks and minimize collection risks. However, subsidy payments from the government are slower as the projects undergo audit assessments.

+ About S$355mn was received from the deferred payment note. About S$133mn was interest accrued, and the rest went towards principal repayment. A negative was the weak Rupee, which knocked off S$46mn. Management has not hedged its Rupee exposure, as the cost outweighs the forex loss. The DPN, which bears an interest rate of about 9%, will mature in 15 years with an option to extend for 9 more years. The outstanding amount of these notes is S$1.8bn as at Dec 2023.

The Negatives

- Land sales for commercial and residential land banks were lower due to the weak market sentiment in Vietnam. However, industrial land sales in Indonesia and Vietnam grew as manufacturers built supply chain networks in these two countries.

- Net debt has risen to S$6.5bn, and net gearing rose to 1.33x due to a bigger renewable portfolio. Still, EBITDA/interest improved from 4.2x to 4.4x.

Outlook

We maintain our earnings estimates for FY24e, which are expected to fall 11.9% YoY due to the maintenance shutdown at its power plant for two months and the absence of contributions from the Vietnam power plant. Contributions from renewables are expected to account for a larger share of net profit, from 21.2% in FY23 to 31.8% in FY25e. We expect integrated urban solutions to remain muted, but there is no risk of writedown in the value of the property assets.

Maintain ACCUMULATE and TP of S$6.00. Our TP is based on 11x of FY24e EV/EBITDA.

Investor Day Highlights

Outlook

We maintain our earnings estimates for FY23e and FY24e. The energy earnings are intact, while earnings at integrated urban solutions remain muted due to the lukewarm Vietnam property market. Maintain ACCUMULATE and TP of S$6.00.

The Positives

The Negatives

Highlights

Maintain BUY and raised TP to S$5.06

We maintain our BUY call and raise TP to S$5.06, based on 11x PE for FY24e.

The news

SCI announced the acquisition of 830MW of renewable assets in China through a joint venture with SPIC. Xingling New Energy owns a portfolio of wind and solar assets.

SCI has signed definitive agreements with Wuling Power, an affiliated company of SPIC, to acquire a 43.5% interest in Hunan Xingling New Energy for a total equity consideration of ~RMB1,058mn (~S$204mn).

Wuling Power holds the remaining 54.7% interest in Xingling New Energy.

The Positives

+ Acquisition of Xingling New Energy will be accretive to earnings. The valuation was not disclosed, but management guided that similar to its acquisition of BEI Energy and other acquisitions, this was done at low double-digit P/E. SCI will fund the acquisition through internal cash resources and external borrowings. Completion is expected in 1H23 and the acquisition is expected to be accretive to earnings. Financials however, were not provided.

+ Acquisition diversifies Group’s presence from north western China. The acquisition of Wuling Power will solidify the Group’s presence in central China, Hunan. According to management, Hunan is currently importing 90% of coal outside with reserve margin at less than 20%. As such, this makes power generation in Hunan a valuable prospect. The assets are also relatively new at 4.9 years, we estimate that IRR of the project is ~11-12%.

Importantly, the acquisition of a 54.7% stake in Xingling New Energy also allow the Group to broaden its partnership with SPIC in renewables and green energy.

+ The acquisition of Xingling New Energy will bring the Group’s gross renewable energy capacity to 9.4GW. With the Group within touching distance of its 10GW target ahead of its 2025 target (Figure 1). We believe the Group will provide an update to its target in its FY22 results.

+ Management ruled out equity funding to finance spate of acquisitions. Amid concerns over funding requirements following the Group’s spate of renewable energy acquisitions, management has affirmed its intention to stick to its previously stated guidance of ensuring that there will be no equity fundraising to hit its 10GW target. While net debt/equity will go towards 1-2x post-acquisition, we believe the Group will use the cash flows from these newly acquired assets to pay down the debt to reach its optimal gearing target of 1.3x. We believe the latest clarification will allay concerns of an equity call.

Outlook

Shareholders have approved the sale of Sembcorp Energy India Limited (SEIL) to Tanweer Infra fund. We believe management will further deploy the proceeds to grow its renewables portfolio to beyond its 10GW target.

For FY22e, we expect continued high electricity prices in Singapore and India to lift earnings. We expect SCI to pay out 16 cents of dividends (split between final and special due to the special circumstances for FY22) for FY22e, translating to a ~5.3% dividend yield.

The news

SCI announced acquisition of 795MW of solar assets in China and 583MW of renewable assets in India.

SCI’s 49%-owned JV Beijing Energy Sembcorp (Hainan) International has entered into share purchase agreements with BEI Energy Development (Beijing) Co., Ltd. to acquire three solar projects, for an initial equity consideration of ~RMB15mn (approximately S$3mn) and future capital injection of up to RMB1,148mn (approximately S$222mn).

SCI will also acquire 100% of Vector Green Energy for a base equity consideration of ~INR27.8bn (~S$474mn).

The Positives

+ Acquisition of BEI Energy and Vector Green will be accretive to earnings. The valuation was not disclosed, but management guided that this was done at low double digit P/E. SCI will fund the acquisition through internal cash resources and external borrowings. Completion is expected in 1Q23 and both acquisitions are expected to be accretive to earnings, financials however, were not provided.

+ China and Indian assets supported by mid- to long- term PPAs. The assets in China have PPAs ranging from three to five years. As the power market in China is regulated, this provides greater stability to tariff rates. Management is confident of renewing the PPAs when they become due as the solar assets are located in the south of Hebei Province, one of China’s main energy demand centres. The assets are contracted to the State Grid Corporation of China, a Chinese state-owned electric utility and grid operator.

The Indian assets, which comprise mainly solar assets, are covered by long-term PPAs averaging 19 years. With recent changes to the regulation on the payment of receivables in India, credit quality has improved and the receivables issue has been mostly resolved.

+ The two acquisitions will bring the Group’s gross renewable energy capacity to 8.5GW. This will bring it closer to its 2025 target of 10GW of gross installed renewable capacity (Figure 1). Its acquisition of Vector Green will also bring significant utility-scale solar capacity to its India business.

Outlook

Shareholders have approved the sale of Sembcorp Energy India Limited (SEIL) to Tanweer Infra fund. We believe management will further deploy the proceeds to grow its renewables portfolio to beyond its 10GW target.

For FY22e, we expect continued high electricity prices in Singapore and India to lift over earnings. We expect SCI to pay out 16 cents of dividends (split between final and special due to the special circumstances for FY22) for FY22e, translating to a ~5.3% dividend yield.

The news

The UK’s new leader, Liz Truss, has capped consumer energy bills at £2,500 (S$4,081) for two years to cushion rising energy prices. For businesses and public sector bodies, a sixth-month scheme will offer equivalent support to that for households, with a review in three months about how it could be better targeted.

SCI has 1.3GW of energy assets in the UK, consisting of energy generation and battery storage. The UK is not a significant contributor to its overall portfolio of energy assets, which are concentrated in South-east Asia, China and India.

The Positives

+ Impact on SCI expected to be subdued as cap will be funded by UK government. SCI’s contract with the national grid of the UK means that it generates electricity through a portfolio of diesel and gas generators. The price cap imposed, limits the amount that it can charge for its tariffs. The difference between the power in the wholesale markets, and the capped consumer price, however, is expected to be borne by the UK government.

+ Energy bill cap will not be financed by energy suppliers. Despite calls by the opposition Labour Party to partly fund the scheme by a windfall tax on energy suppliers, PM Liz Truss has ruled this out, favouring the entire bailout to be funded through more government borrowings instead.

The Negatives

- Review of the UK’s net zero strategy underway; could slow move to renewables. Liz Truss has announced a review of the government’s net zero strategy, which she argued is necessary under the current landscape. The review could potentially impact demand for energy storage, though this is still uncertain at this stage. Liz Truss has announced schemes she said would increase energy resilience, including launching about 100 new oil and gas licenses along with dozens of new North Sea licenses in an effort to boost domestic oil and gas production.

In the last 10 years, the UK has made significant progress to decarbonise its power sector (Figure 1). It has grown its renewable share of electricity generation from 7% to 43%. This has led to increased demand for energy storage, in which SCI is operating one of the largest energy storage portfolios in the UK at 120MWh.

Outlook

The impact of UK PM Liz Truss’ moves on the energy sector are still uncertain at the moment as the finer details are lacking. The impact on SCI is expected to be subdued as the contribution from UK is not large. That said, we are monitoring the developments, and will provide an update when more details are available.

SCI is currently in the midst of building a 360MW energy storage system at Wilton International on Teesside, which will help the UK achieve its net zero target.

Terms and conditions of proposed sale

SCI announced the proposed sale of SEIL for the equivalent of $2.059bn, or 1x NAV. The purchaser is the Tanweer Consortium led by Oman Investment Corporation S.A.O.C (OIC), the Ministry of Defence Pension Fund, Oman (MODPF) and Dar Investment SPC (Dar Investment).

On completion, Tanweer Consortium will settle the entire final purchase price through the DPN via a facility provided by SCI under the DPN. The DPN will bear interest at 9% interest (1.8% spread + 7.2% benchmark), minus a greenhouse gas (GHG) emissions intensity reduction incentive rate. This GHG reduction incentive rate is subject to a cap of 180 basis points if these emission targets are met. In other words, the current spread over the benchmark rate will be removed or reduced any time within the 15-year period if the Tanweer Consortium can meet the GHG emissions target. Such adjustments will affect the final purchase price. All outstanding payment under the DPN should be payable in full on the 15th anniversary date of the completion, which is also the maturity date. The yearly payments will be recorded under the Group’s EBITDA section. Should the outstanding payment obligations not be met, the maturity date will be extended for two years, and for every two years till the monies are paid. The maturity date will not be extended beyond the 24th anniversary date of completion.

Shareholders approval is required for the transaction, which is expected in November this year, and the expected completion is six months after EGM.

The Positives

+ Acquisition consideration implies S$0.8bn/GW of gross installed capacity, higher than average comparable transactions of S$0.5-1bn/GW. The acquisition price implies 1x of NTA, which we view as fair given the weak market environment around coal-related assets. SCI will recognise ~S$11mn in gains from the sale.

+ Debt-capitalisation ratio improve to 62% from 66% for pro-forma 1H22. We believe the Group will leverage its stronger balance sheet to further its transition to green energy. On a pro forma basis, SCI’s total debt as at 30 June 2022 will decrease to $7.1bn from $8.7bn due to the deconsolidation of SEIL in SCI’s balance sheet. SCI’s interest paying capacity will also improve with interest coverage rising to 6.3x in the same period from 5.1x. SCI still has ~$5bn of borrowing facilities to tap on, which will accelerate the transformation of its portfolio from brown to green.

+ $700mn in receivables from SEIL expected to be repaid within the next 24-48 months. The Indian Ministry of Power has recently directed Telangana and Andhra Pradesh to settle the overdue receivables within 20-48 months. Should this be adhered to, the Group is expected to receive ~$700mn in receivables in the next 1-2 years, which will lower the credit risk of SEIL, and by extension the risk for the DPN.

The Negatives

- SCI will still be exposed to operational risks of SEIL for at least 15 years after sale. Even though SEIL will be deconsolidated from SCI’s books after the sale, the DPN, which is a form of vendor financing means that SCI will still be exposed to the operational risks of SEIL for at least 15 years after the sale. Should the outstanding payment obligations not be met, the maturity date will be extended for two years, and for every two years till the monies are paid. The maturity date will not be extended beyond the 24th anniversary date of completion.

However, we believe this risk is mitigated by both mid- and long- term contracts for SEIL, totalling 85% of SEIL’s thermal plant capacity. SEIL will have 570MW up for renewal in 2024 (22% of the power purchase agreement). That said, we view the risk of non-renewal as low given the strong current energy environment. IEX prices remain elevated at ~7,500 Rupees/hr in September vs. an average ~7,600 Rupees/hr in 1H22.

Outlook

Shareholders approval is required for the transaction, which is expected in November this year, and the expected completion is six months after EGM.

For dividends, we model a ~30% payout ratio, in line with FY21’s payout. We expect SCI to pay out 16 cents of dividends (split between final and special due to the special circumstances for FY22) for FY22e, translating to a ~4.9% dividend yield

The Positives

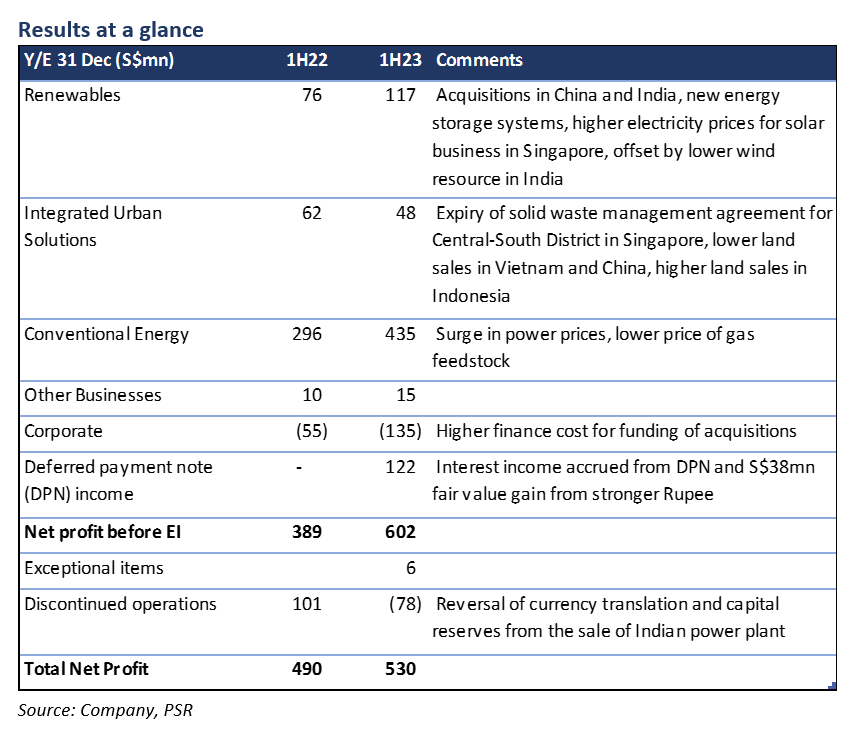

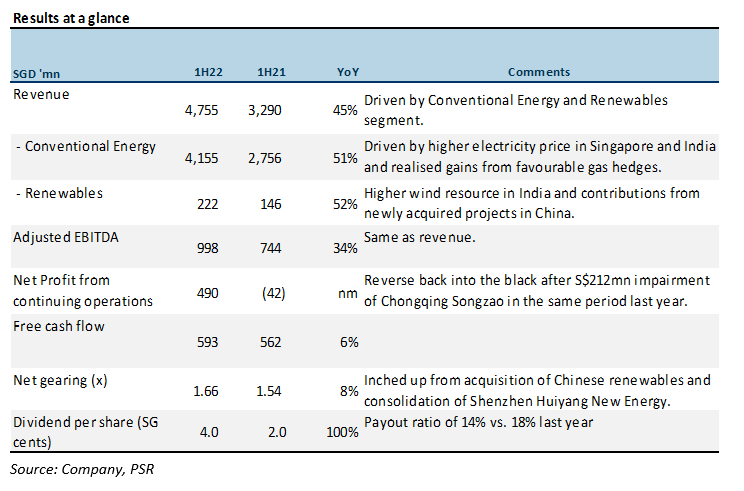

+ 1H22 profit ahead of our expectations, at 99% of FY22e as Conventional Energy and Renewable Energy beat. The surge in power prices and margins in Singapore and India drove Conventional Energy beat for the period (+115% YoY). Average USEP prices for 1H22 surged to S$324/MWh, higher than the S$295/MWh average in 2H21 and spark spreads have increased to $6.30/MWh YTD (Figure 1) as average USEP prices have moved ahead of HSFO in the last nine months. A one-off hedging gain of $92mn from gas hedges during the period also lifted profits, but we do not expect this to recur in 2H22. Contributions from newly acquired projects in 1H22, SDIC New Energy and Shenzhen Huiyang in China lifted Renewables profit.

+ Battery segment as key growth driver in medium- to long-term. The management re-affirmed its battery business as a key growth driver for the company, in line with its strategic plan announced at its Analyst Day in 2021. It currently has 120MW of energy storage in the UK which holds an important role in helping to stabilise the grid as the UK continues its pivot towards renewables.

SCI is currently in the process of building a 360MW battery facility at Teesside, UK. When completed, it will boost the Group’s capacity to take advantage of more volatile, uncertain markets with the rise of intermittent renewables.

+ Renewables profit at 74% of FY22e, lifted by better performance in key markets. Better wind resources in India and higher spot prices for its solar business in Singapore lifted profits (+217% YoY). SCI’s gross renewables capacity in operation and under development globally now stands at 7.1GW in 1H22 from 6.1GW as at end-2021. Its acquisition of a 98% stake in HYNE assets will contribute ~S$50mn per year to its profits.

The Negatives

- Lower land sales dragged Integrated Urban Solutions business, offset by higher ASPs. Higher contribution from Wilton 11 in the UK was offset by higher operating costs for the waste business in Singapore. Despite lower land sales, the Group remain confident of hitting its target of 500ha of land sales by FY25 as it plans the development of the 481-hectare Quang Tri Industrial Park in Vietnam and the 1,000ha of VSIP Binh Duong III.

Outlook

Management continued to guide for the Conventional Energy segment to perform well in the second half of this year as global energy markets remain firm. Despite this, we expect energy markets to moderate slightly in 2H22. USEP prices in July were ~9% lower than 1H22’s average. We expect some normalisation in FY23e.

Planned maintenance shutdowns for Sembcorp Biomass Power Station in the UK (~6 weeks) and India SEIL Project 2 (~45 days) in 2H22 will also put a drag on Conventional Energy earnings in 2H22.

We also modelled in a full half-year contribution from the newly acquired SDIC New Energy and Shenzhen Huiyang in China for its Renewables segment.

For dividends, we model a ~30% payout ratio, in line with FY21’s payout. We expect SCI to pay out 16 cents of dividends for FY22e, translating to a ~4.9% dividend yield.

The news

SCI financial results are expected to be materially higher for 1H22 vs. last year, driven by the Conventional Energy segment.

Contrary to a report that Myanmar’s central bank has ordered a halt on repayment of foreign loans, its subsidiary in Myanmar has not received such a directive. It has also received prompt payment from its offtaker and continues to operate its Myanmar power plant.

The Positives

+ Average USEP prices up 239% YoY or 9.8% HoH to lift SCI’s 1H22 Conventional Energy. The global energy crunch since September 2021 lifted SCI’s Conventional Energy segment in 2H21. The conflict in Ukraine at the beginning of the year has further exacerbated the risk of disruptions in oil and gas. As a result, average USEP prices for 1H22 surged to S$324/MWh, higher than the S$295/MWh average in 2H21 and spark spreads have increased to 6.3 YTD (Figure 1) as average USEP prices have moved ahead of HSFO in the last nine months.

+ Tariffs for power in India’s Tamil Nadu and Gujarat rose ~88% YoY in 1H22. Based on data from IEX, tariffs for power at Tamil Nadu and Gujarat rose to ~6.36Rs/kWh from ~3.39Rs/kWh from the same period last year. The higher tariff was driven by high global oil prices and higher temperatures in the country. The International Energy Agency (IEA) recently revised upward India’s electricity demand to 7% from negative previously in light of the intense heatwave in the country.

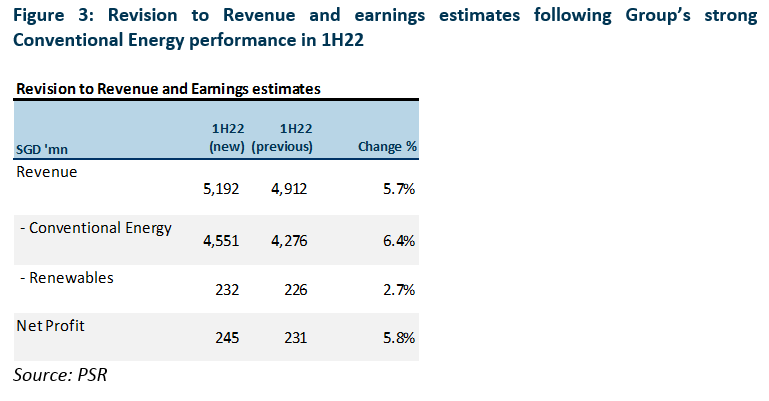

On the back of this, we revise FY22e Conventional Energy revenue up marginally from $8.6bn to $8.8bn to account for better spark spreads for Sembcorp Cogen and India (Figure 3).

+ On track to building up its green energy portfolio. SCI’s gross renewables capacity in operation and under development globally now stands at 6.8GW in 1H22 from 6.1GW as at end-2021 (Figure 2). This is ahead of our FY22e target of 7.3GW, accordingly, we revise our FY22e gross renewables capacity to 7.6GW on account of the Group’s aggressive build up of its renewables portfolio. We believe the company is on track to achieve its plans of increasing its renewable capacity to 10GW by 2025. We see the company’s transition toward green energy as an important driver of its re-rating.

The Negatives

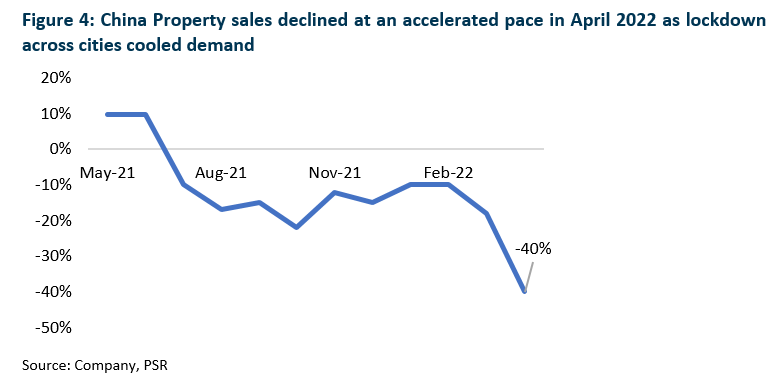

- Headwinds in China property market to put a drag on Group’s Urban development business. China’s property market has weakened sharply in the past year as a result of a government clampdown on excessive borrowings by developers, and a Covid-19 induced economic slowdown (Figure 4). We believe this will hurt the Group’s land sales in China, though the impact is not expected to be significant as China account for just 6% of the Group’s total saleable land.

Outlook

We expect the group to continue with its transition to sustainable solutions and sustainable development. Despite its ambitious growth plans, it will not require any equity fund-raising, relying entirely on internal sources.

The Conventional Energy segment continued to perform well in the first half of this year as global energy markets rose in tandem with commodity prices. For the rest of 2022, we expect this segment to be supported by energy markets and the continued uncertainty brought about by the Ukraine conflict.

However, we expect the slowdown in the Chinese property market to offset some of the growth from the Conventional Energy and Renewable Energy segment.

The Group continues to actively seek deals in India, China and the UK by leveraging its partnerships and platforms for their acquisitions.