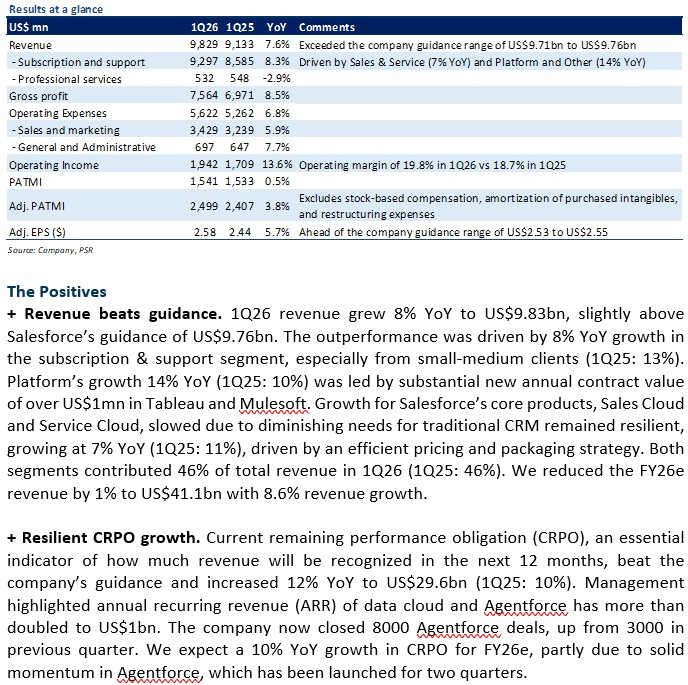

The Positives

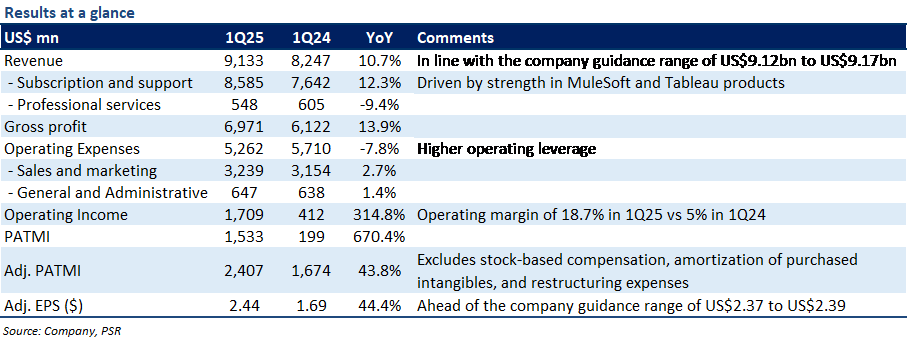

+ MuleSoft and Tableau products provided much of the strength. In 1Q25, subscription and support revenue grew 12% YoY to US$8.6bn. On a product level, revenues from Sales Cloud and Service Cloud grew 11% YoY to US$2.0bn and US$2.2bn, respectively. Data Cloud remained the fastest growing segment, increasing by 25% YoY to US$1.4bn, with MuleSoft (+27% YoY) and Tableau (+21% YoY) offerings being the largest contributors. Salesforce benefited from continuous product enhancements and its pricing and product bundling strategies.

+ Operating margins expanded on higher operating leverage. In 1Q25, Salesforce’s OPEX fell by 8% YoY to US$5.3bn, resulting in an operating margin expansion of 1,370bps YoY to 18.7%. This was mainly because the company continued to focus on improving cost efficiencies through headcount reductions and lower sales-related costs. In Jan, Salesforce reportedly laid off about 700 employees, or 1% of its total workforce (~72,000).

The Negative

- Soft 2Q25e revenue guidance. For 2Q25e, Salesforce expects total revenue to grow 8% YoY to US$9.2bn (2Q24: 11% YoY), missing consensus estimates of US$9.4bn. The significant slowdown is mainly because of a tough macroeconomic environment. Management highlighted that the company is witnessing continued measured buying behavior, leading to an elongated sales cycle, additional deal approval layers, and deal size compression.

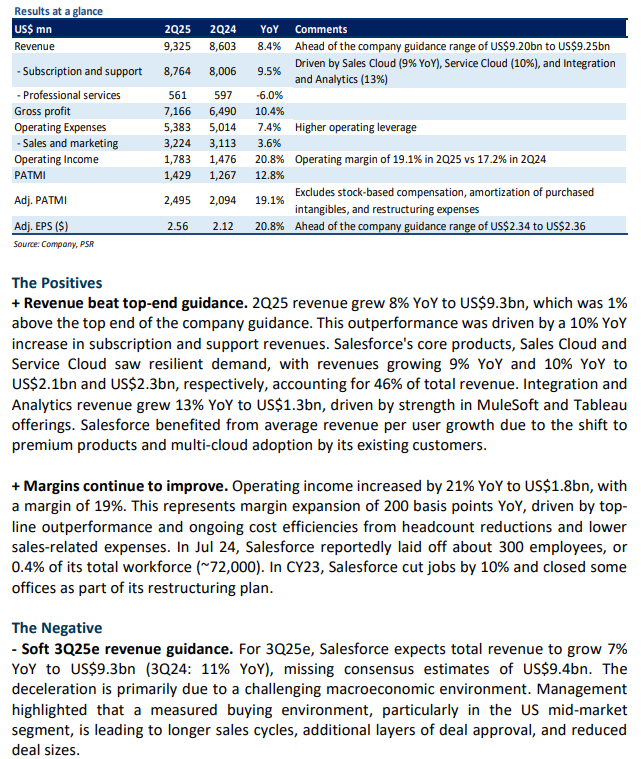

The Positives

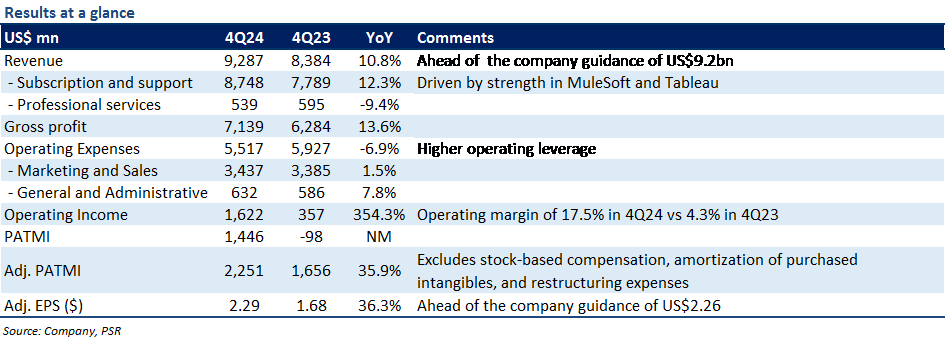

+ Multiproduct deals continued to drive growth. 4Q24 revenue grew 11% YoY (10% in constant currency) to US$9.3bn, 1% above the top end of company guidance, driven by higher subscription sales. On a product level, Sales/Service Cloud demand remained resilient with revenues growing by 10%/12% YoY to US$2.0bn and US$2.2bn, respectively. Integration and Analytics revenue delivered robust growth of 21% YoY to US$1.6bn, driven by strength in MuleSoft and Tableau offerings. Management highlighted that the number of large enterprise deals (those greater than US$10mn) grew by 78% YoY, with over 86,000 multiproduct deals. This was mainly driven by continuous product enhancements and its pricing and product bundling strategies. For instance, Salesforce Starter suite bundles Sales, Service, and Marketing tools together in one platform leading to significant surge in average sales price.

+ Margins continue to improve. Gross and operating margins expanded by 200bps and 1,300bps YoY, respectively. Operating income spiked more than 4-fold to US$1.6bn. The margin improvement was mainly due to top-line upside and higher operating leverage (OPEX down 7% YoY) from prudent headcount control and lower sales-related costs. In FY23, Salesforce cut jobs by 10% and closed some offices.

The Negative

- FY25e revenue guidance below our forecast. For FY25e, Salesforce expects total revenue to grow 9% YoY to US$37.9bn at the midpoint, which was below our estimate of US$38.6bn. This was because the company expects foreign exchange currency rates to negatively impact its revenues by US$100mn. In addition, Salesforce’s professional services business (revenue down 9% YoY in 4Q24) is expected to continue to be impacted due to the compression of larger transformation deals.

The Positives

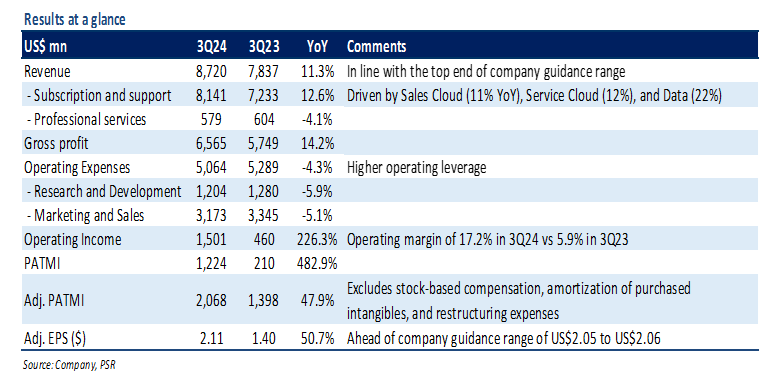

+ Strong demand across all products. 3Q24 total revenue grew 11% YoY to US$8.7bn, in line with the top end of company guidance, driven by higher subscription and support revenues. Salesforce witnessed resilient demand from large enterprises for its core products with Sales Cloud and Service Cloud revenues growing 11% YoY and 12% YoY to US$1.9bn and US$2.1bn, respectively. Within Data Cloud segment, revenues for integration software MuleSoft grew 26% YoY, while revenues for data visualization tool Tableau grew 16% YoY.

+ cRPO growth continued to accelerate. Salesforce’s current remaining performance obligations (cRPO), a measure of contracted sales to be recognised in the next 12 months, jumped 14% YoY to US$23.9bn. The cRPO growth came above the 11% company guidance and was driven by strong early renewals and large customer wins. Management highlighted that the number of deals over US$1mn grew by 80% YoY. We expect large deals and multi-cloud adoption momentum to support near-term growth as it will lead to higher subscription sales.

+ Margins rise on cost discipline. In 3Q24, Salesforce’s operating expenses fell by 4% YoY to US$5.1bn resulting in an operating margin of 17.2% (vs. 5.9% in 3Q23). The improvement was mainly driven by a leaner cost structure after significant cost-cutting measures over the last 12 months, including job cuts and lower sales-related costs. Headcount was down -11% YoY.

The Negative

- NIL

The Positives

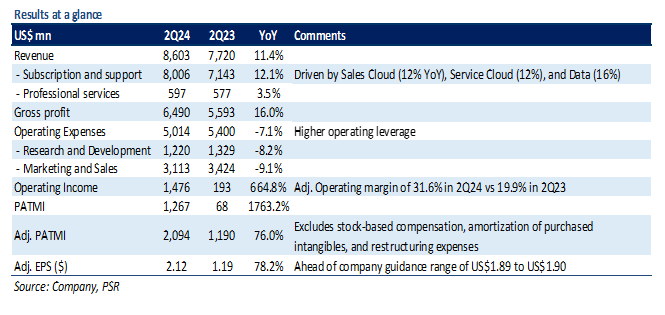

+ Demand remains robust. 2Q24 total revenue grew 11% YoY to US$8.6bn, 1% above the top end of company guidance, driven by resilient demand for its cloud and business software offerings. Revenues from core products Sales Cloud and Service Cloud grew 12% YoY to US$1.9bn and US$2.1bn, respectively. Data Cloud remained the fastest growing segment, increasing by 16% YoY to US$1.2bn, with MuleSoft and Tableau offerings being the largest contributors.

+ cRPO growth beats guidance. Remaining performance obligation (RPO), which represents future revenue that is under contract but hasn’t been recognized, grew by 12% YoY to US$46.6bn. The current portion of RPO (cRPO), which the company expects to be recognized in the following 12 months, increased by 12% YoY to US$24.1bn. The cRPO growth came ahead of the company’s guidance of 10% YoY growth, and was largely driven by momentum in MuleSoft. The company also benefited from multi-cloud adoption strategy, with 6 of the top 10 deals in the quarter included five or more of its cloud products. Additionally, the number of customers whose annual contract value (ACV) exceeds US$10mn reached 450 (growth of 3x over 5 years).

+ Focused on improving profitability. In 2Q24, Salesforce’s operating expenses fell by 7% YoY to US$5bn resulting in an operating margin of 17% (vs. 3% in 2Q23). The improvement was mainly driven by higher operating leverage across all cost items, including job cuts (headcount dropped 11% YoY) and careful sales and marketing spend.

The Negative

- NIL

Outlook

For 3Q24e, Salesforce expects total revenue to be in the range of US$8.70bn to US$8.72bn, representing growth of about 11% YoY. The revenue guidance includes a US$100mn FX headwind. Management also guided GAAP EPS/adj. EPS to be in the range of US$1.02 to US$1.03 and US$2.05 to US$2.06, respectively.

Salesforce lifted its annual earnings/margin forecast despite the company witnessing an elongated sales cycle, additional deal approval layers, and deal size compression. For FY24e, the company now expects GAAP EPS of US$3.51 on total revenue of US$34.75bn (prev. GAAP EPS of US$2.68 on revenue of US$34.6bn) taking the midpoint (Figure 1). This implies total revenue growth of 11% YoY led by continued demand for its cloud products, particularly MuleSoft, Sales Cloud, and Service Cloud. Salesforce also raised its operating margin guidance to 13% from the prior guidance of 11% (up from 3% in FY23) driven by higher operating leverage.

In August, Salesforce hiked prices of its cloud products by an average of 9%. The company also plans to boost demand by introducing a generative AI-based tool named Einstein GPT for salespeople, customer service agents, and marketers. Management noted that the price increase will not have a material impact in FY24e as it is expected to hit the existing customer base over the next 1-3 years at renewals.

Salesforce generated about US$628mn (up 379% YoY) in Free Cash Flow in 2Q24, ending the quarter with US$6.8bn in cash and cash equivalents. The company returned US$1.9bn to shareholders in 2Q24 in the form of share repurchases.

The Positives

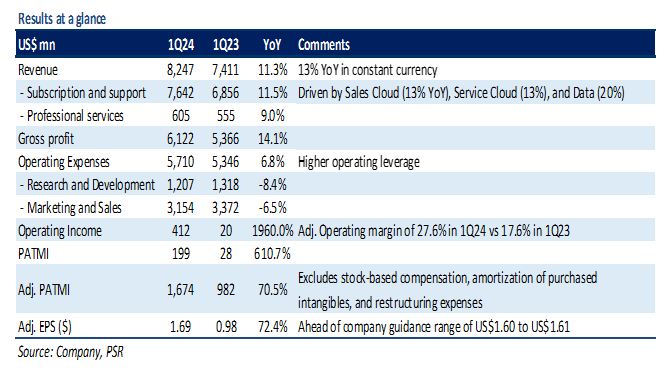

+ Strength in MuleSoft and core products drive growth. 1Q24 revenue grew 11.3% YoY (13% in constant currency) to US$8.2bn, 1% above the top end of company guidance, driven by higher subscription sales. Salesforce witnessed continued strength in its core products with Sales Cloud and Service Cloud revenues growing 13% YoY in constant currency to US$1.8bn and US$2.0bn, respectively. Within Data Cloud, MuleSoft revenues grew by 26% YoY, while Tableau grew by 12% YoY. Total remaining performance obligations (RPO), which represent future revenue under contract, grew by 11% YoY to US$46.7bn. The current portion of RPO (cRPO), which the company expects to be recognized in the next 12 months, increased by 12% YoY to US$24.1bn. This was driven by the strength of its Customer 360 platform, multi-cloud adoption trends, and low customer attrition rate of 8%.

+ Improvement in margins. In 1Q24, Salesforce reported adj. operating margin of 27.6% compared with 17.6% in 1Q23. This was mainly driven by continued focus on operational discipline, driving cost controls through job cuts, real estate consolidation, and lower travel and entertainment expenses.

The Negative

- CAPEX spending jumps. In 1Q24, Salesforce’s CAPEX increased by 36% YoY to US$243mn. The extra spending is towards the introduction and rollout of generative AI-driven product enhancements. During the quarter, Salesforce launched Einstein GPT, which is designed to help salespersons and customer-service agents to perform their duties more efficiently, including generation of personalized emails to send to customers. For FY24e, CAPEX is expected to be about US$865mn (2.5% of total revenue).

The Positives

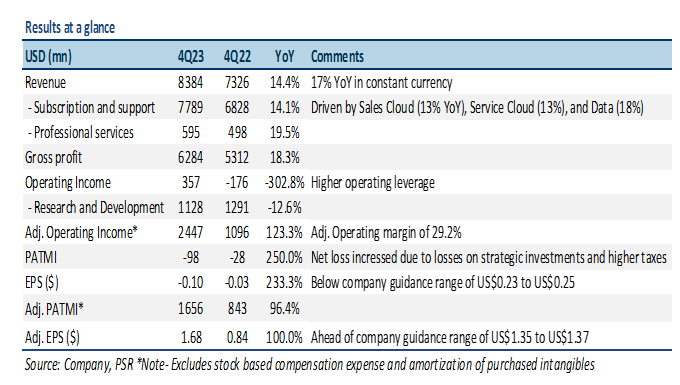

+ Strength in MuleSoft and Tableau products drive growth. Salesforce recorded revenue of US$8.4bn for 4Q23, ahead of the company’s guidance of US$8.0bn, and representing a 14% YoY growth (17% YoY in constant currency). Data, which includes MuleSoft and Tableau license sales, rose 18% YoY to US$1.3bn – the highest YoY revenue increase in 4Q23. Salesforce's other core businesses also performed well, with Sales and Service cloud revenues growing 13% YoY to US$1.8bn and US$1.9bn in 4Q23, respectively. Remaining performance obligations (RPO), which represent future revenue under contract, grew by 11% YoY to US$48.6bn. The current portion of RPO (cRPO), which the company expects to be recognized in the next 12 months, increased by 12% YoY to US$24.6bn. This was driven by the strength of its Customer 360 platform, multi-cloud adoption, and record low customer attrition rate of below 7.5%.

+ Cost cuts are paying off. In 4Q23, Salesforce reported a record high adj. operating margin of 29.2% compared with 15% in 4Q22 driven by higher operating leverage across all cost segments (particularly Research and Development). In 4Q23, Salesforce benefited about 6 percentage points from one-time items, including 1.5 points from restructuring. In Jan 23, the company announced that it would lay off 10% of its workforce (~7,000 employees).

The Negative

- Pressure from foreign exchange rates. Salesforce’s revenue was negatively impacted due to the strengthening of the dollar against several key foreign currencies, including the Euro, British pound, and Japanese yen. In 4Q23, the unfavorable foreign exchange rate movement negatively impacted revenue by about US$250mn (or 3% of total revenue). The foreign exchange impact was guided to decrease revenue growth in 1Q24e by US$150mn.

The Positives

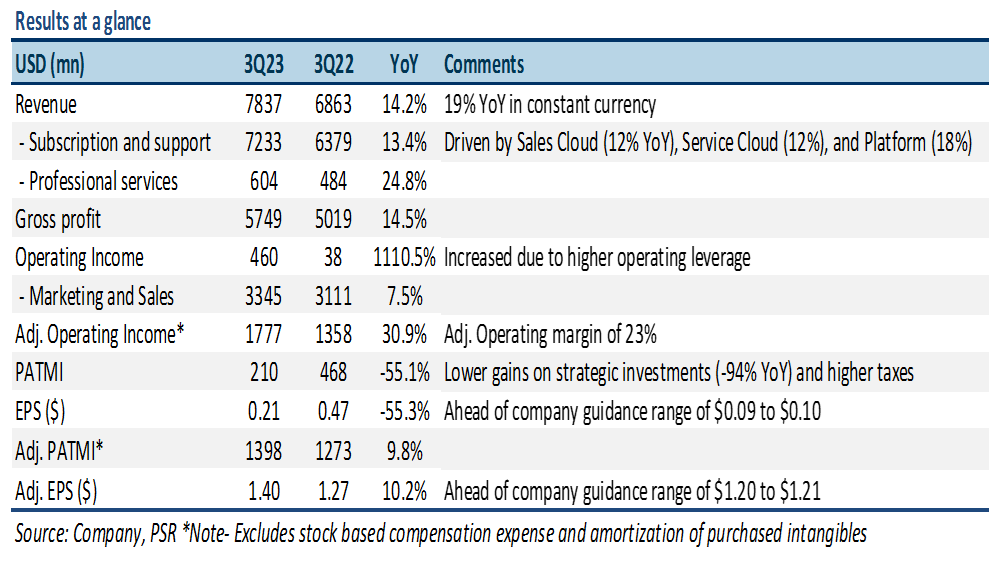

+ Strength in core products drives growth. Salesforce recorded revenue of US$7.8bn for 3Q23, slightly above the top-end of its guidance, representing a 14% YoY growth (19% YoY in constant currency). The core segments continued to gain momentum in the quarter with Sales Cloud revenue growing 12% YoY to US$1.7bn and Service Cloud also growing 12% YoY as it neared the US$2bn revenue mark. Slack revenue grew 46% YoY to about US$402mn. Remaining performance obligations (RPO), which represent future revenue under contract, grew by 10% YoY to US$40bn. The current portion of RPO (cRPO), which the company expects to be recognized in the next 12 months, increased by 11% YoY to US$20.9bn. This was driven by the strength of its Customer 360 platform, new customer wins (Bank of America and Dell), and multi-cloud adoption.

+ Record-high operating margin. In 3Q23, Salesforce reported adj. operating margin of 23% compared with 20% in 3Q22. This was mainly driven by continued focus on operational discipline, driving cost controls through measured hiring and reductions in sales-related travel and entertainment expenses.

The Negative

- FX continues to be a headwind. Salesforce’s revenue was negatively impacted due to the strengthening of the dollar against several key foreign currencies, including the Euro, British pound, and Japanese yen. In 3Q23, FX headwind to revenue was US$300mn (143% of PATMI), higher than the company’s guidance of US$250mn. Salesforce projects US$250mn headwind from FX in 4Q23e.

Outlook

For 4Q23e, Salesforce expects total revenue to be in the range of US$7.93bn to US$8.03bn, representing growth of 8% to 10% YoY. Management also guided GAAP EPS/adj. EPS to be in the range of US$0.23 to US$0.25 and US$1.35 to US$1.37, respectively. The current portion of RPO (cRPO) is expected to grow by 7% in 4Q23e, which implies cRPO of US$23.5bn. This suggests further deterioration in the quarter amid intense customer scrutiny of deals in the US and major European markets. Salesforce acknowledged tougher demand backdrop with elongated sales cycles and deal size compression.

While Salesforce didn’t provide preliminary guidance for FY24e, it did mention that investors should anticipate margin expansion driven by higher operating leverage, including measured hiring and lower travel and entertainment expenses. The company reiterated its target of returning 30% to 40% of free cash flow annually to shareholders on average. Salesforce repurchased US$1.7bn of its stock in 3Q23 out of its authorized US$10bn buyback program.

The Positives

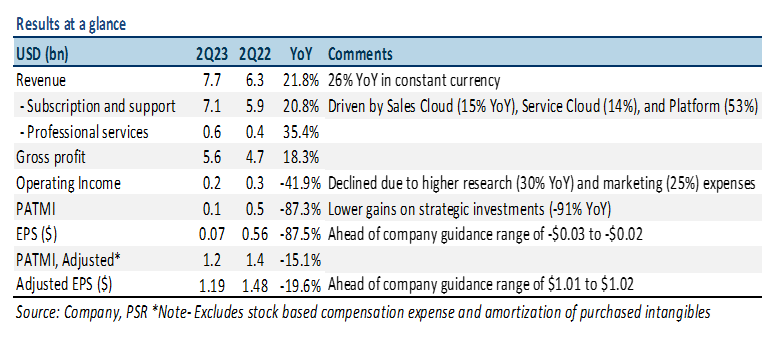

+ Revenue beat top-end of guidance. Salesforce recorded revenue of US$7.7bn for 2Q23, slightly above the top-end of its guidance, representing a 22% YoY growth (26% YoY in constant currency). Revenue growth was driven mainly by Sales (15% YoY) and Service (14% YoY) cloud segments and accounted for 49% of total revenue during the quarter. Platform, which includes collaboration tool Slack, rose 53% YoY to US$1.5bn – the highest YoY revenue increase in 2Q23. Slack contributed US$376mn to 2Q23 revenue (25% of Platform), above the company’s estimate of US$360mn. The number of paid customers on Slack spending over US$100K annually surged by more than 40% YoY in 2Q23.

+ In-line metrics supporting growth. Remaining performance obligations (RPO), which represent future revenue that is under contract but hasn’t been recognized, grew by 15% YoY to US$41.6bn. The current portion of RPO (cRPO), which the company expects to be recognized in the next 12 months, increased by 15% YoY to US$21.5bn. This is mainly because of continued demand for its Customer 360 offerings and new customer wins. Multi-cloud adoption maintained traction as the number of customers purchasing five or more of Salesforce’s cloud products grew by double digits. Also, the attrition rate remained at record lows of about 7.5%.

+ Authorizes first ever US$10bn stock buyback. Salesforce announced a share repurchase program for up to US$10bn to offset dilution from stock-based compensation. Management also stated that it plans to maintain a healthy balance sheet to help fund any future M&A and ongoing investments in organic innovation.

The Negatives

- Higher-than-expected FX headwinds. FX had a negative impact of US$250mn on 2Q23 revenues (368% of PATMI), higher than the company’s guidance of US$200mn. Currency is now expected to negatively impact FY23e revenue growth by US$800mn, up from the US$600mn projected previously.

Outlook

For FY23e, Salesforce reduced its revenue guidance to US$30.9bn to US$31.0bn (prev US$31.7bn to US$31.8bn), representing growth of about 17% YoY. The downward revision was mainly because of unfavorable foreign currency exchange rates and cautious buying behavior resulting in a lengthened sales cycle, increased deal scrutiny, and deal compression. The updated guidance includes US$1.5bn of revenue contribution from Slack business. However, Salesforce maintained its adjusted operating margin forecast of 20.4% driven by higher operating leverage (measured hiring and lower travel and entertainment expenses). Salesforce also slightly reduced its adjusted EPS guidance range to US$4.71 to US$4.73 (prev US$4.74 to US$4.76) but reiterated its GAAP EPS range of US$0.38 to US$0.40.

For 3Q23e, Salesforce expects adjusted EPS to be in the range of US$1.20 to US$1.21 on total revenue of US$7.825bn at the midpoint of guidance. The company also expects cRPO growth of about 12% YoY.