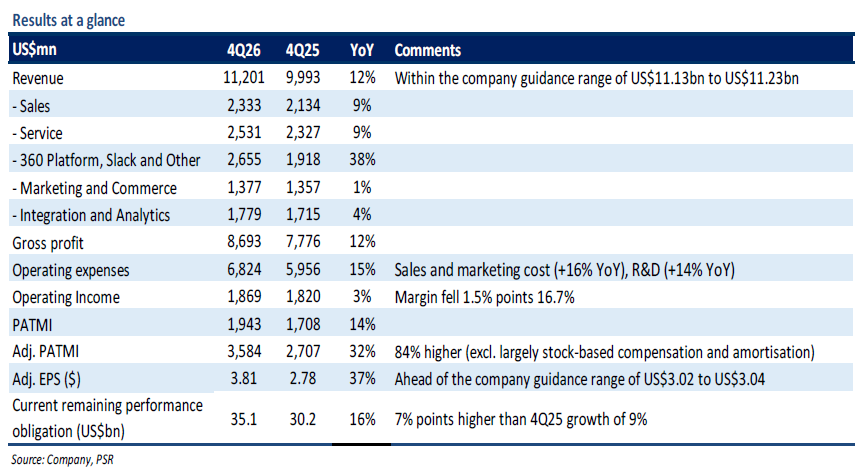

Salesforce Inc – Platform Cloud Growth Strengthens

- FY26 revenue met our expectations, while earnings were ahead. FY26 revenue/adj. PATMI were at 100%/109% of our forecasts. Adj. EPS came in at US$3.81, ahead of the US$3.03 guidance.

-

We expect group revenue to rise 10% YoY in FY27e, led by Platform Cloud growth of 22%, offsetting weakness in Commerce and Analytics Clouds. We think the opportunity lies in upselling to customers with higher AWU per token, driving high value at low cost. Margins could expand as token costs fall and AI models are commoditised. Current RPO is expected to rise 14% YoY (from 12% in 1Q26), with reacceleration likely and supported by larger deal wins. The company authorised a US$50bn share buyback for FY27e and beyond (27% of the US$183bn market cap).

-

We maintain a BUY recommendation with a TP of US$253 (prev. US$382). FY27e estimates revenue is up 1% on Platform Cloud growth, while adj. PATMI rises 10% from strong Q4 results. WACC raised to 9.9% (prev. 8.4%) due to higher Beta. Terminal growth cut to 5.5% (prev. 6%) due to competition from AI model providers, which could enable enterprises to bypass Salesforce and reduce premium SKU adoption. We think Salesforce is less affected by AI disruption, with three AI monetization levers 1) premium AI SKUs with embedded AI and unlimited agentic access, 2) seat expansion in core clouds as agentic AI scales, and 3) consumption credits for customer-facing agents.

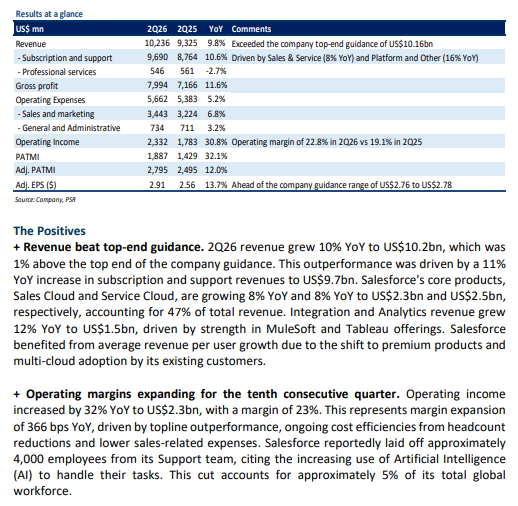

Salesforce Inc – Guidance rises from the Informatica acquisition

- 9M26 revenue met our expectations, while earnings were ahead. 9M26 revenue/adj. PATMI were at 74%/80% of our FY26e forecasts. The strong earnings benefited from delayed timing expenses and improved bad-debt collections.

- Salesforce raised its 4Q26e guidance, with the closed Informatica deal lifting revenue growth by 3% points to 11–12% and adding 0.8% points to FY26e Subscription and Support, bringing growth to 10% YoY. Current performance remaining obligation guidance was also increased by 4% points to 15% YoY.

- We maintain a BUY rating with a raised target price of US$382.00 (previously US$364.00), reflecting a 1%/5% upward revision to our FY26e revenue and adj. PATMI estimates following strong 3Q26 results and raised guidance. Our WACC and terminal growth assumptions remain at 8.4% and 6%, respectively. Our adjusted FY26e forward P/E of 22.7x is below the one-year historical average of 25.3x.

Salesforce Inc – Margin expansion for ten consecutive quarters

-

1H26 revenue/adj. PATMI met our expectations at 49%/51% of our FY26e forecasts. In 2Q26, adj. PATMI grew 12% YoY on higher operating leverage.

-

The company lifts its FY26e revenue guidance bottom end to US$41.1bn (+8.5% YoY) and raises its forecast of FY26e adj. EPS bottom end by US$0.06 to US$11.33. For 3Q26e, Salesforce projects total revenue to grow by 8% YoY, led by higher subscription sales for its Sales Cloud, Service Cloud, and MuleSoft offerings.

-

We maintain BUY with an unchanged TP of US$364.00. Our WACC/g assumptions remain unchanged at 8.4%/6%, respectively, while our FY26e revenue and earnings remain unchanged. Salesforce's catalysts include ongoing margin expansion, robust free cash flows, and resilient demand for its core offerings, especially in Agentforce and Data Cloud.

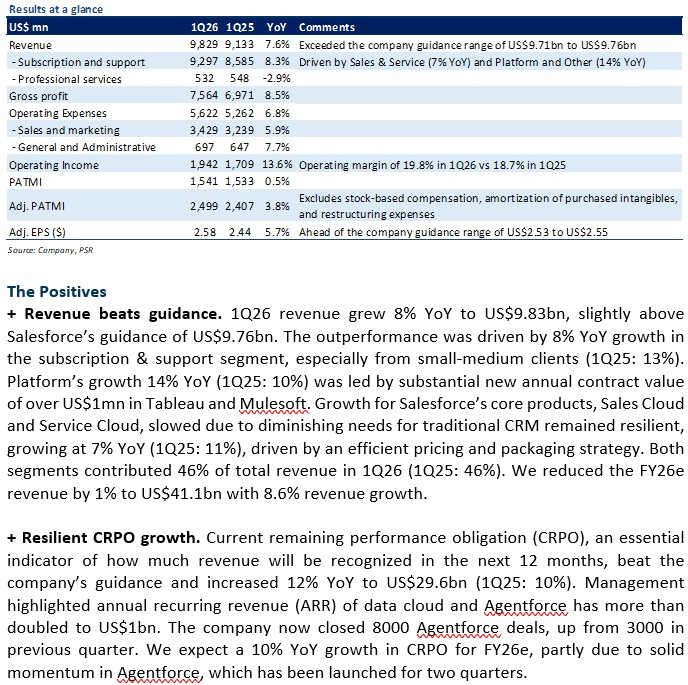

Salesforce Inc – Earnings beat guidance across all metrics

- 1Q26 revenue/adj. PATMI in line with our expectations at 23%/23% of our FY26e forecasts. Subscription & support growth was driven by demand from small-medium business customers while platform growth was led by substantial new annual contract value of over US$1mn in Tableau and Mulesoft.

- Salesforce increased its total revenue guidance by 1% (or US$400mn) to US$41.3bn, driven by foreign exchange tailwinds in FY26e. The company held its FY26e adj. operating margin guidance unchanged at 34%.

- We upgrade to a BUY recommendation from ACCUMULATE due to strong growth across business segments. We raise our DCF target price to US$364.00 (prev. US$305), with a higher WACC of 8.4%, led by acquisition and terminal growth rates of 6%. We reduced the FY26e revenue by 1% to US$41.1bn with 8.6% revenue growth.

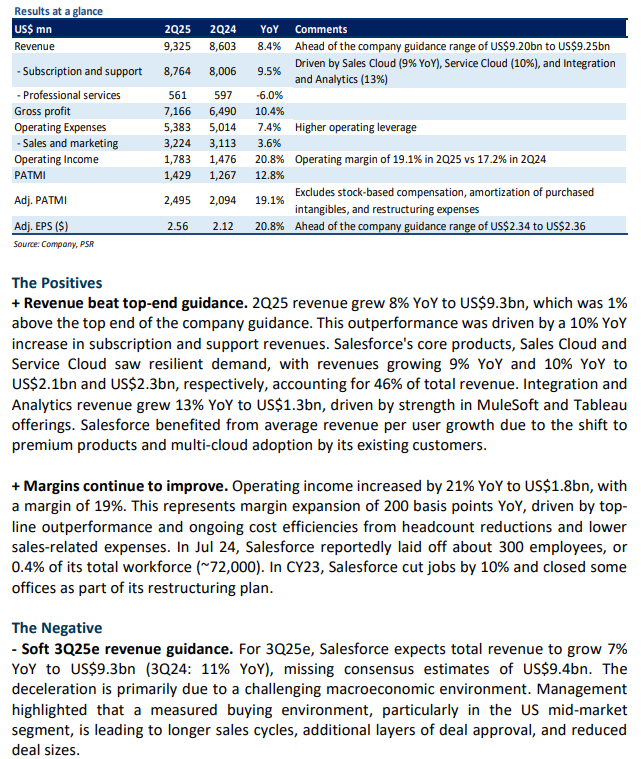

Salesforce Inc – Margins expansion still the main story

- 1H25 revenue/adj. PATMI was in line with expectations at 49%/50% of our FY25e forecasts. In 2Q25, adj. PATMI grew 19% YoY on higher operating leverage.

- For 3Q25e, Salesforce expects revenue to grow by 7% YoY to US$9.3bn led by higher subscription sales for its Sales Cloud, Service Cloud, and MuleSoft offerings. The company reaffirmed its FY25e revenue guidance of US$37.9bn (+9% YoY) but raised adj. operating margin outlook to 32.8% from 32.5% (FY24: 30.5%).

- We downgrade to ACCUMULATE from BUY recommendation as we account for recent share price performance. We maintain our DCF target price of US$305.00 with an unchanged WACC of 7% and terminal growth rate of 4%. Our FY25e revenue estimates remain unchanged while we nudge higher our PATMI by 1% to account for higher interest income. Catalysts for Salesforce include ongoing margin expansion, robust free cash flows, and resilient demand for its core offerings as enterprises look to form a 360-degree view of their customer data to provide better customer experiences.

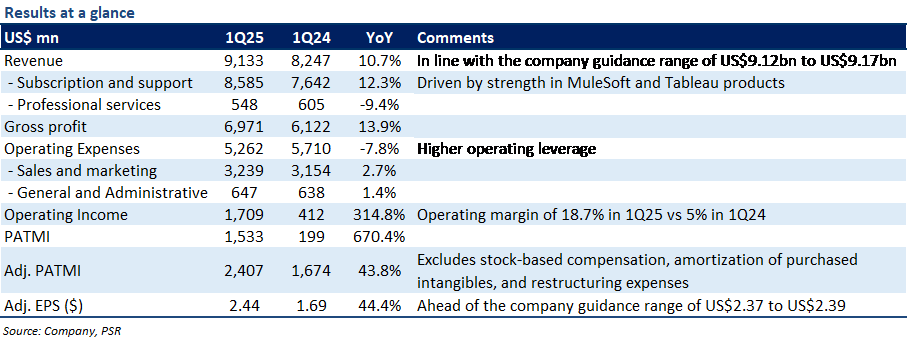

Salesforce Inc – Reaffirms revenue guidance

- 1Q25 revenue/PATMI was in line with expectations at 24%/25% of our FY25e forecasts. Revenue grew 11% YoY to US$9.1bn due to higher subscription sales. PATMI spiked 670% YoY (44% normalized) driven by higher operating leverage.

- For 2Q25e, Salesforce expects revenue to grow by 8% YoY to US$9.2bn led by strong demand for its data integration and analytics products like MuleSoft and Tableau. The company reaffirmed FY25e revenue guidance of US$37.9bn (+9% YoY) but lowered its GAAP operating margin to 19.9% from 20.4% (FY24: 14.4%).

- We upgrade to BUY from ACCUMULATE recommendation as we account for recent share price performance. We lower our DCF target price to US$305.00 (prev. US$323.00) with an unchanged WACC of 7% and a terminal growth rate of 4%. Our FY25e revenue/PATMI estimates are nudged lower by 1%/2% to reflect macro headwinds and higher expenses. Catalysts for Salesforce include ongoing margin expansion, robust free cash flows, and resilient demand for its data cloud offerings as enterprises look to form a 360-degree view of their customer data to provide better customer experiences.

The Positives

+ MuleSoft and Tableau products provided much of the strength. In 1Q25, subscription and support revenue grew 12% YoY to US$8.6bn. On a product level, revenues from Sales Cloud and Service Cloud grew 11% YoY to US$2.0bn and US$2.2bn, respectively. Data Cloud remained the fastest growing segment, increasing by 25% YoY to US$1.4bn, with MuleSoft (+27% YoY) and Tableau (+21% YoY) offerings being the largest contributors. Salesforce benefited from continuous product enhancements and its pricing and product bundling strategies.

+ Operating margins expanded on higher operating leverage. In 1Q25, Salesforce’s OPEX fell by 8% YoY to US$5.3bn, resulting in an operating margin expansion of 1,370bps YoY to 18.7%. This was mainly because the company continued to focus on improving cost efficiencies through headcount reductions and lower sales-related costs. In Jan, Salesforce reportedly laid off about 700 employees, or 1% of its total workforce (~72,000).

The Negative

- Soft 2Q25e revenue guidance. For 2Q25e, Salesforce expects total revenue to grow 8% YoY to US$9.2bn (2Q24: 11% YoY), missing consensus estimates of US$9.4bn. The significant slowdown is mainly because of a tough macroeconomic environment. Management highlighted that the company is witnessing continued measured buying behavior, leading to an elongated sales cycle, additional deal approval layers, and deal size compression.

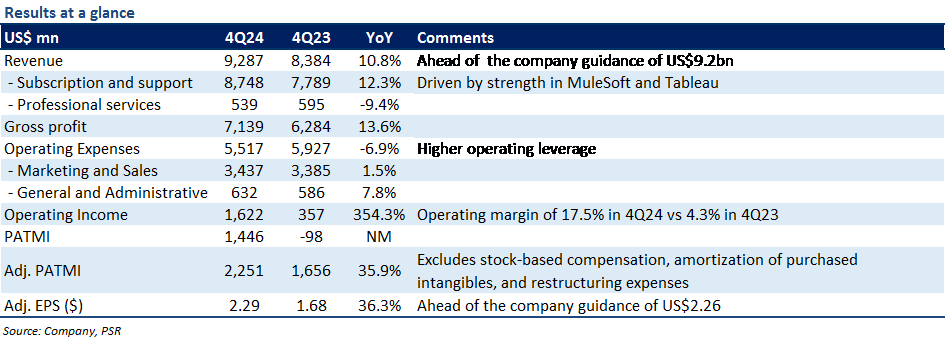

Salesforce Inc – Further margin expansion

- FY24 revenue/adj. PATMI met our expectations at 100% of our forecasts. 4Q24 adj. PATMI jumped 36% YoY to US$2.3bn driven by higher operating leverage.

- For FY25e, Salesforce expects revenue to grow 9% YoY to US$37.9bn driven by strong momentum in its MuleSoft and Tableau offerings. Adj. EPS expected to grow 18% YoY to US$9.7 led by cost-containment efforts. Salesforce declared its first-ever quarterly dividend of US$0.40 per share and increased its share buyback program by US$10bn.

- We maintain ACCUMULATE with a raised DCF target price of US$323.00 (prev. US$270.00) as we roll over an additional year of valuations. Our WACC/g assumptions remain unchanged at 7%/4%, respectively. We nudge lower our FY25e revenue estimates by 1% to account for FX headwinds and declining professional services revenue, while we increase our adj. PATMI by 3% due to lower expenses. Catalysts include continued margin expansion, focus on maximising shareholder returns, and resilient demand for its Customer 360 cloud offerings as companies look to form a more holistic view of their customer data to provide better customer experiences.

The Positives

+ Multiproduct deals continued to drive growth. 4Q24 revenue grew 11% YoY (10% in constant currency) to US$9.3bn, 1% above the top end of company guidance, driven by higher subscription sales. On a product level, Sales/Service Cloud demand remained resilient with revenues growing by 10%/12% YoY to US$2.0bn and US$2.2bn, respectively. Integration and Analytics revenue delivered robust growth of 21% YoY to US$1.6bn, driven by strength in MuleSoft and Tableau offerings. Management highlighted that the number of large enterprise deals (those greater than US$10mn) grew by 78% YoY, with over 86,000 multiproduct deals. This was mainly driven by continuous product enhancements and its pricing and product bundling strategies. For instance, Salesforce Starter suite bundles Sales, Service, and Marketing tools together in one platform leading to significant surge in average sales price.

+ Margins continue to improve. Gross and operating margins expanded by 200bps and 1,300bps YoY, respectively. Operating income spiked more than 4-fold to US$1.6bn. The margin improvement was mainly due to top-line upside and higher operating leverage (OPEX down 7% YoY) from prudent headcount control and lower sales-related costs. In FY23, Salesforce cut jobs by 10% and closed some offices.

The Negative

- FY25e revenue guidance below our forecast. For FY25e, Salesforce expects total revenue to grow 9% YoY to US$37.9bn at the midpoint, which was below our estimate of US$38.6bn. This was because the company expects foreign exchange currency rates to negatively impact its revenues by US$100mn. In addition, Salesforce’s professional services business (revenue down 9% YoY in 4Q24) is expected to continue to be impacted due to the compression of larger transformation deals.

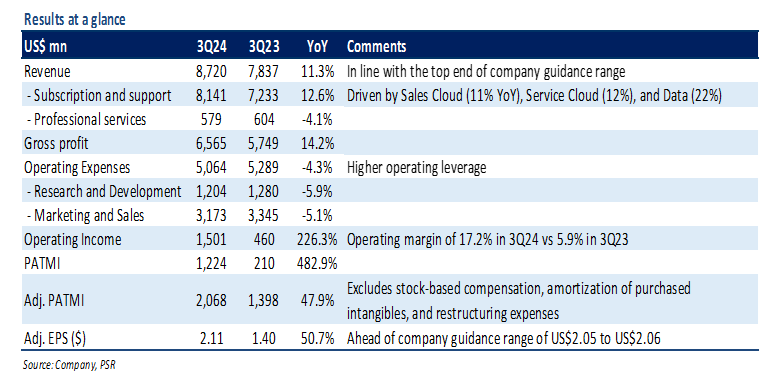

Salesforce Inc – Focused on improving earnings

- 9M24 revenue was within expectations but earnings were ahead. 9M24 revenue/PATMI were 74%/78% of our FY24e forecasts. 3Q24 PATMI spiked 483% YoY to US$1.2bn driven by higher operating leverage.

- For 4Q24e, Salesforce expects total revenue to grow 10% YoY to US$9.2bn driven by resilient demand for its Sales Cloud, Service Cloud, and MuleSoft offerings. GAAP EPS to be about US$1.27 vs -US$0.10 in 4Q23 led by cost-containment efforts.

- We maintain ACCUMULATE with a raised DCF target price of US$270.00 (prev. US$242.00), with a WACC of 7% and terminal growth of 4%. Our FY24e/FY25e revenue estimates remain unchanged; while we have increased PATMI estimates by 14%/13% to account for lower expenses. We believe Salesforce is well-positioned to benefit from cloud-based digital transformation trends as companies look to form a more holistic view of their customer data to provide better customer experiences.

The Positives

+ Strong demand across all products. 3Q24 total revenue grew 11% YoY to US$8.7bn, in line with the top end of company guidance, driven by higher subscription and support revenues. Salesforce witnessed resilient demand from large enterprises for its core products with Sales Cloud and Service Cloud revenues growing 11% YoY and 12% YoY to US$1.9bn and US$2.1bn, respectively. Within Data Cloud segment, revenues for integration software MuleSoft grew 26% YoY, while revenues for data visualization tool Tableau grew 16% YoY.

+ cRPO growth continued to accelerate. Salesforce’s current remaining performance obligations (cRPO), a measure of contracted sales to be recognised in the next 12 months, jumped 14% YoY to US$23.9bn. The cRPO growth came above the 11% company guidance and was driven by strong early renewals and large customer wins. Management highlighted that the number of deals over US$1mn grew by 80% YoY. We expect large deals and multi-cloud adoption momentum to support near-term growth as it will lead to higher subscription sales.

+ Margins rise on cost discipline. In 3Q24, Salesforce’s operating expenses fell by 4% YoY to US$5.1bn resulting in an operating margin of 17.2% (vs. 5.9% in 3Q23). The improvement was mainly driven by a leaner cost structure after significant cost-cutting measures over the last 12 months, including job cuts and lower sales-related costs. Headcount was down -11% YoY.

The Negative

- NIL

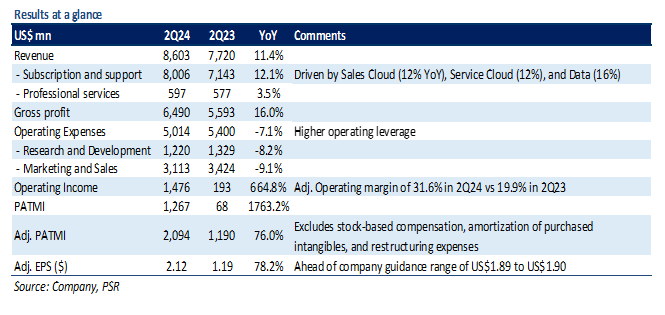

Salesforce Inc – Profit outlook raised

- 2Q24 revenue was in line with our expectations, while earnings exceeded expectations. 1H24 revenue/PATMI was at 49%/55% of our FY24e forecasts. In 2Q24, PATMI spiked by 19-fold YoY driven by higher operating leverage.

- For FY24e, Salesforce boosted its revenue outlook to US$34.75bn from the prev. US$34.6bn as it benefits from AI-related demand and a recent price hike of 9% across its cloud products. The company also raised its GAAP EPS outlook to US$3.51 from US$2.68 led by cost containment efforts.

- We maintain ACCUMULATE with a raised DCF target price of US$242.00 (prev. US$226.00), with a WACC of 7% and terminal growth of 4%. We increase our FY24e revenue/PATMI estimates by 1%/30% to reflect benefits from the price hike and lower expenses. We believe Salesforce is well-positioned to benefit from cloud-based digital transformation trends as companies look to form a more holistic view of their customer data to provide better customer experiences.

The Positives

+ Demand remains robust. 2Q24 total revenue grew 11% YoY to US$8.6bn, 1% above the top end of company guidance, driven by resilient demand for its cloud and business software offerings. Revenues from core products Sales Cloud and Service Cloud grew 12% YoY to US$1.9bn and US$2.1bn, respectively. Data Cloud remained the fastest growing segment, increasing by 16% YoY to US$1.2bn, with MuleSoft and Tableau offerings being the largest contributors.

+ cRPO growth beats guidance. Remaining performance obligation (RPO), which represents future revenue that is under contract but hasn’t been recognized, grew by 12% YoY to US$46.6bn. The current portion of RPO (cRPO), which the company expects to be recognized in the following 12 months, increased by 12% YoY to US$24.1bn. The cRPO growth came ahead of the company’s guidance of 10% YoY growth, and was largely driven by momentum in MuleSoft. The company also benefited from multi-cloud adoption strategy, with 6 of the top 10 deals in the quarter included five or more of its cloud products. Additionally, the number of customers whose annual contract value (ACV) exceeds US$10mn reached 450 (growth of 3x over 5 years).

+ Focused on improving profitability. In 2Q24, Salesforce’s operating expenses fell by 7% YoY to US$5bn resulting in an operating margin of 17% (vs. 3% in 2Q23). The improvement was mainly driven by higher operating leverage across all cost items, including job cuts (headcount dropped 11% YoY) and careful sales and marketing spend.

The Negative

- NIL

Outlook

For 3Q24e, Salesforce expects total revenue to be in the range of US$8.70bn to US$8.72bn, representing growth of about 11% YoY. The revenue guidance includes a US$100mn FX headwind. Management also guided GAAP EPS/adj. EPS to be in the range of US$1.02 to US$1.03 and US$2.05 to US$2.06, respectively.

Salesforce lifted its annual earnings/margin forecast despite the company witnessing an elongated sales cycle, additional deal approval layers, and deal size compression. For FY24e, the company now expects GAAP EPS of US$3.51 on total revenue of US$34.75bn (prev. GAAP EPS of US$2.68 on revenue of US$34.6bn) taking the midpoint (Figure 1). This implies total revenue growth of 11% YoY led by continued demand for its cloud products, particularly MuleSoft, Sales Cloud, and Service Cloud. Salesforce also raised its operating margin guidance to 13% from the prior guidance of 11% (up from 3% in FY23) driven by higher operating leverage.

In August, Salesforce hiked prices of its cloud products by an average of 9%. The company also plans to boost demand by introducing a generative AI-based tool named Einstein GPT for salespeople, customer service agents, and marketers. Management noted that the price increase will not have a material impact in FY24e as it is expected to hit the existing customer base over the next 1-3 years at renewals.

Salesforce generated about US$628mn (up 379% YoY) in Free Cash Flow in 2Q24, ending the quarter with US$6.8bn in cash and cash equivalents. The company returned US$1.9bn to shareholders in 2Q24 in the form of share repurchases.

Salesforce Inc – Continued margin expansion

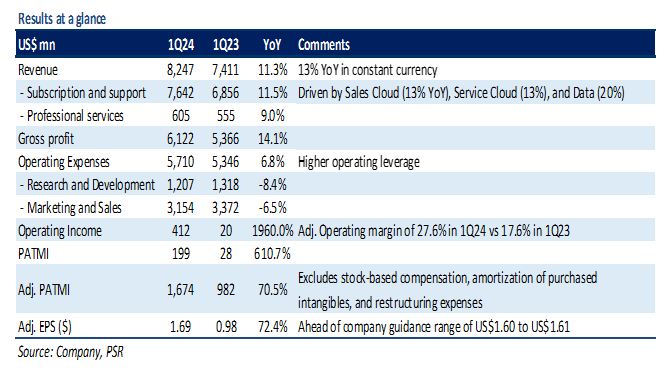

- 1Q24 revenue/Adj. PATMI was within expectations at 24%/23% of our FY24e forecasts, excluding a restructuring charge of US$0.7bn. Revenue grew 11% YoY to US$8.2bn due to higher subscription sales. PATMI spiked 611% YoY (71% normalized) driven by higher operating leverage.

- Future contracted revenue or remaining performance obligations (RPO) grew by 11% YoY to US$46.7bn. For FY24e, Salesforce maintained its total revenue guidance of US$34.6bn (up 10% YoY), while raised its GAAP EPS outlook to US$2.68 from US$2.60 taking the midpoint. Adj. operating margin expected to be 28% up from 22.5% in FY23.

- We downgrade to ACCUMULATE from BUY recommendation after the recent jump in its stock price. We increase our DCF target price to US$226.00 (prev. US$219.00) with a WACC of 7% and terminal growth of 4%. Our FY24e revenue estimates remain unchanged, while we have increased our PATMI by 2% due to lower expenses. Salesforce enjoys longer term tailwinds from cloud-based digital transformation trends as companies look to form a more holistic views of their customers.

The Positives

+ Strength in MuleSoft and core products drive growth. 1Q24 revenue grew 11.3% YoY (13% in constant currency) to US$8.2bn, 1% above the top end of company guidance, driven by higher subscription sales. Salesforce witnessed continued strength in its core products with Sales Cloud and Service Cloud revenues growing 13% YoY in constant currency to US$1.8bn and US$2.0bn, respectively. Within Data Cloud, MuleSoft revenues grew by 26% YoY, while Tableau grew by 12% YoY. Total remaining performance obligations (RPO), which represent future revenue under contract, grew by 11% YoY to US$46.7bn. The current portion of RPO (cRPO), which the company expects to be recognized in the next 12 months, increased by 12% YoY to US$24.1bn. This was driven by the strength of its Customer 360 platform, multi-cloud adoption trends, and low customer attrition rate of 8%.

+ Improvement in margins. In 1Q24, Salesforce reported adj. operating margin of 27.6% compared with 17.6% in 1Q23. This was mainly driven by continued focus on operational discipline, driving cost controls through job cuts, real estate consolidation, and lower travel and entertainment expenses.

The Negative

- CAPEX spending jumps. In 1Q24, Salesforce’s CAPEX increased by 36% YoY to US$243mn. The extra spending is towards the introduction and rollout of generative AI-driven product enhancements. During the quarter, Salesforce launched Einstein GPT, which is designed to help salespersons and customer-service agents to perform their duties more efficiently, including generation of personalized emails to send to customers. For FY24e, CAPEX is expected to be about US$865mn (2.5% of total revenue).

Get access to all the latest market news, reports, technical analysis

by signing up for a free account today!

Login

The full article is only available for premium content subscribers. To continue reading this article, please log in:

Not a Premium Content Subscriber yet? Sign up here!

- Home >

- Phillip Research Report