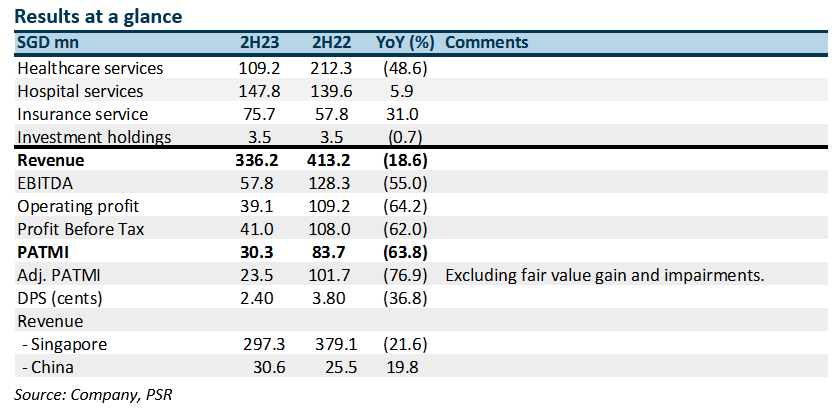

• 1H24 revenue and PATMI were within expectations at 57% / 52% of our FY24e estimates respectively. 1H24 PATMI declined 49% YoY to S$30.9mn.

• 1H24 EBITDA margins collapsed 9% points YoY to 16.6% from higher losses at the insurance operations, continued losses in China, lower margins from transitional care facilities and lower government grants.

• We maintain our FY24e PATMI and NEUTRAL recommendation. Our DCF target price of S$0.96 is unchanged. We expect earnings to normalise back to pre-pandemic levels until China hospitals can achieve scale and operating leverage. We believe the Singapore hospital operations are facing multiple competitive pressures. Volumes from domestic patients are under pressure from insurers diverting patients to public hospitals. Meanwhile, competition for foreign patients face lower priced alternatives in Thailand and Malaysia. The ability to scale up into higher margin complex cases may come under pressure from their largest private competitor with their larger number of specialists.

The Positive

+ Growth in China. 2023 is effectively the first full year of operation for their new hospital in China, absent the pandemic interruptions. 2H23 revenue grew 20% YoY. Raffles is gradually gaining traction with foreign corporations operating in China. EBITDA break-even will require 2 to 3 years, but patient load is building momentum as marketing efforts intensify.

The Negative

- Revenue and margin collapse. Absent pandemic-related activities, including testing, vaccination, and even TCF, revenue and margins suffered. The pandemic provided extra services for Raffles and margins were high due to the urgency and limited competition.

The Positive

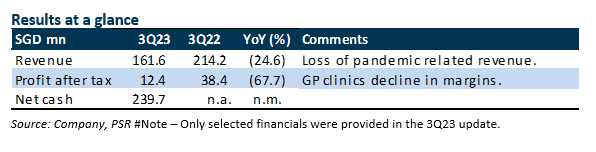

+ Healthy cash flow. The net cash continues to grow at S$239mn (2Q23: S$230mn). Cash continues to pile up after the completion of the hospitals in China. Capex has collapsed from a peak of S$96mn in FY19 to S$25mn last year.

The Negatives

- Revenue is down sharper than expected. We believe the drag in revenue came from lower pandemic-related vaccination and test service at the clinics and centres and softer foreign patient revenue. Revenue at the GP clinics is normalising back to pre-pandemic levels. Foreign patient volumes are below expectations due to the rising cost in Singapore.

- Margins collapsed. Margin weakness was from the loss of high-margin vaccination and testing services. Other expenses such as utilities and staff cost continue to climb. There were only moderate price increases during the period.

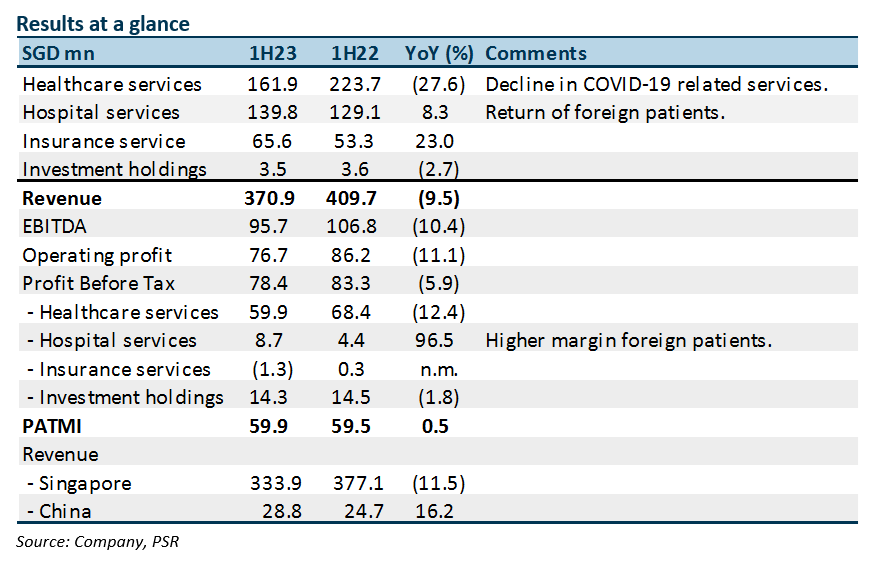

The Positives

+ Resilient hospital services revenue and margins. Hospital services enjoyed growth from increased foreign patients, which are 70-80% of pre-pandemic level. Patients from Vietnam and China have not returned to pre-pandemic levels. Operating margins in 1H23 was 20.7%, higher than pre-pandemic levels of around 16%. The company managed to lower staff costs by S$34mn or 17% YoY by reducing part-time workers. Meanwhile, 1H23 PBT margin is also supported by S$4.6mn improvement in net finance income.

+ Healthy FCF* with lower capex cycle. 1H23 FCF remains strong at S$111mn (1H22: S$117mn), driving up net cash to S$230mn (1H22: S$135mn). Annualised capex is trending towards S$30mn. This compares to S$45mn p.a. over the past three years.

*Free cash flow = Operating cash-flow less Capex less Lease payments

The Negative

+ China is still a drag. Despite revenue growth of 16% YoY in 1H23, China continues to experience operating losses. The losses are estimated at between S$12mn and $14mn. The next few years are the investment phase to build brand awareness of the hospital amongst the locals. We believe locals still prefer government hospitals for their perceived pool of more experienced doctors.

Outlook

We expect 2H23 to be stable supported by the inflow of foreign patients and higher prices. Meanwhile, headwinds will stem from loss of COVID-19 PCR tests and lower margins for TCFs. Insurance will also continue suffering losses as claims rebound with the increase of more insured patients. During the pandemic, patients generally avoided the hospital if the illness was less serious.

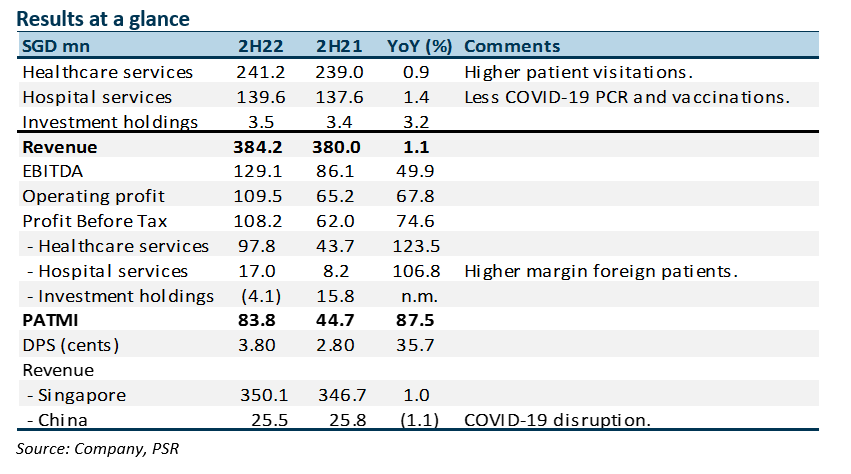

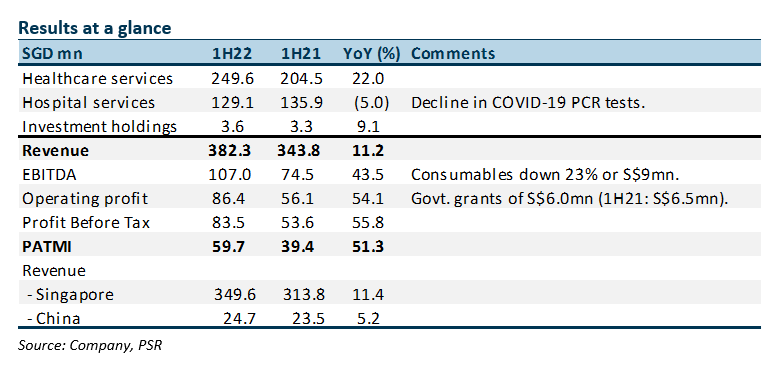

The Positives

+ Spike in healthcare services earnings. 2H22 PBT for healthcare services more than doubled to S$97.8mn. The jump was due to higher GP visits as re-opening saw a jump in non-COVID infections. In addition, patients with COVID-19 symptoms preferred GP visits rather than hospitals. Increased volumes boosted operating leverage for the business.

+ Return of foreign patients. With borders re-opening, revenue from foreign patients has returned to close to pre-pandemic levels. Such patients have higher revenue intensity and better margins. We expect the return of foreign patients to continue into 1H23. We believe foreign patient revenue has surged back to around 20% of revenue. This is below the estimated 25-30% pre-pandemic.

+ Jump in FCF*. In line with the record earnings, FCF rose 51% to a record S$183mn for FY22. Capital expenditure should normalise to S$30mn-35mn after the major ramp-up of the past 3 years for the new hospitals in China. Net cash has doubled from S$90.7mn to S$180mn. FY22 dividend was increased by 36% to 3.8 cents.

*Free cash flow = Operating cash-flow less Capex less Lease payments

The Negative

+ Losses in China hospitals. EBITDA losses in China were larger than expected due to the lockdown. There was vaccination work, but revenue was low. The decline in foreigners was another negative, especially for the Beijing hospital. We expect S$10mn EBITDA loss per hospital for Chongqing and Shanghai.

The Positives

+ Resilient revenue despite less COVID related revenue. Revenue expanded 11% YoY despite the decline in PCR testing services. Growth in 1H22 was driven by (i) higher foreign patients, now 60% of pre-pandemic levels; (ii) return of elective treatments especially from elderly patients that had avoided hospitals during the pandemic; (iii) more GP clinic visits from more unmasked events and greater brand awareness. The number of GP visits exceeds pre-pandemic levels; (iv) COVID-19 related revenue was resilient with vaccinations still underway and higher patient load at the CTFs.

+ Surge in operating margins. Operating margins surged 6% bps to 22.6%. Staff cost rose a slower 7% YoY and purchasing cost was down 23%. We believe the margin pick-up was due to higher revenue intensity from foreign patients.

+ Growth in China despite lockdown. Revenue in China rose 5% supported by Chongqing hospital volumes. Raffles hospitals in China are gaining more recognition, especially from the targeted upper middle income households. The Shanghai hospital was opened but lockdown affected the flow of patients and staff availability.

+ Surge in operating cash flow. 1H22 free cash flow jumped S$80mn YoY to S123mn, due to higher profits, a decline in receivables and lower CAPEX. Net cash improved by S$100mn YoY to S$134mn as of June 2022.

The Negative

- Nil.

Outlook

We expect 2H22 revenue to be resilient, supported by foreign patient admissions, return of elective treatments, price increases and increased visits to GP clinics. The revenue drag will come from lower COVID-19 related services such as vaccination, testing and CTF. We believe losses in China will persist as Shanghai operations ramp up capacity and cost.

Upgrade to BUY with a higher TP of S$1.46 (prev. S$1.27)

We raised our FY22e earnings by 60%, with an 18% increase in revenue and a 5% point increase in margins. Our WACC was also nudged up by 0.4% points to 7.5% to account for the higher risk-free rate.

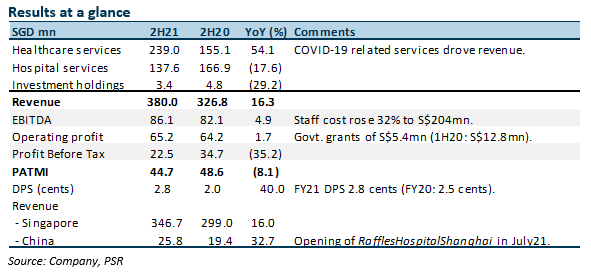

The Positives

+ Pandemic services driving growth. 2H21 revenue jumped 54% YoY. Driving growth were COVID-19-related services such as vaccinations, PCR swab tests and management of community treatment facilities. Contribution from COVID-19 services was not disclosed. However, peer hospitals' contribution from COVID-19-related services is around 20%. Another revenue driver was China, up 33%, but contribution was only 7% of 2H21 revenue.

+ Record cash flows. Free cash flow generated during the year was a record S$110mn (FY20: +S$74.3mn). Net cash improved to S$91mn from S$32mn a year ago. A dividend of 2.8 cents is a 60% payout ratio or S$50mn cash outlay.

The Negative

- Rising staff cost. Staff cost jumped 32% YoY in 2H21 to S$204mn. Staff cost as a percentage of sales in FY21 is around 53.5%. This compares with the pre-pandemic level of 51%. We expect staff costs to remain elevated due to labour shortage and tougher operating conditions. Other cost pressures are from personal protective equipment (such as masks, gowns, etc). The impact of rising electricity costs is less significant. There is a need to raise prices by 3-5% to offset some of these higher costs.

Outlook

We expect earnings to be weaker in FY22e:

Maintain NEUTRAL with a lower TP of S$1.27, from S$1.35

Our FY22e earnings are cut by 8% and our DCF valuation WACC is nudged up from 6.8% to 7.1% due to a higher risk-free rate assumption.

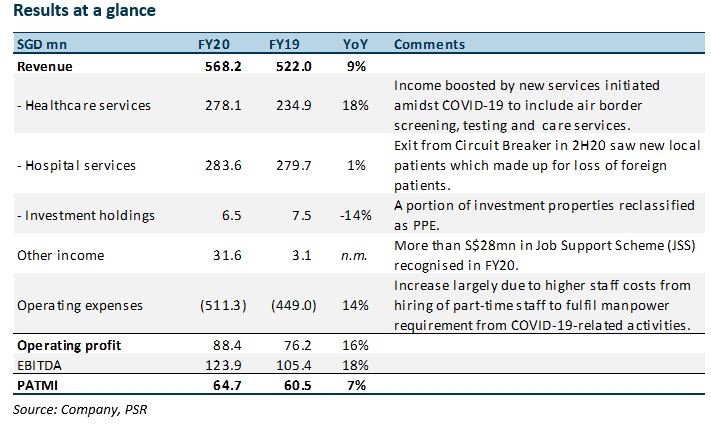

The Positives

+ Strong healthcare services

Income grew 20% YoY in FY20, faster than the +6% in 1H20. Apart from offering air border screening and testing of foreign workers in dormitories in 1H20, the Group introduced new services such as PCR and serology testing in 2H20 as part of the national effort to combat COVID-19.

+ Hospital services stable with new patients

Despite loss of foreign patients due to travel restrictions, revenue from hospital services was resilient with new patients after Singapore exited its circuit breaker. As countries roll out vaccination programmes, we expect a gradual recovery in foreign patient load.

The Negatives

- Operating expenses rose on higher staff costs

Staff costs increased 9.3% YoY from S$267mn to S$291mn due to manpower intensity during COVID-19. JSS income of S$28mn in FY20 minimised the impact on earnings. With wage support tapering off by 1H21 and RafflesHospitalShanghai’s gestation, costs are expected to continue creeping up in FY21e.

Outlook

China operations back in action

The performance of RafflesHospitalChongqing improved in FY20 from FY19 despite a challenging operating environment. It remains on track to break even in FY21 as China has contained COVID-19 swiftly.

The Group completed upgrading work at RafflesHospitalBeijing to support inpatient services and offer minimally-invasive surgeries. This is expected to boost profitability.

The opening of RafflesHospitalShanghai has been delayed. It will open by mid-FY21. We expect narrower EBITDA losses than RafflesHospitalChongqing due to the existing presence of Raffles Medical’s clinics in Shanghai. Being a more cosmopolitan city with a bigger expat presence, demand for private healthcare in Shanghai is expected to be higher.

Recommendation

Upgrade to ACCUMULATE with higher TP of S$1.18, from S$0.94

While revenue growth is expected to be healthy in FY21, we lower earnings by 10% to factor in RafflesHospitalShanghai’s gestation in 1H21 and the higher expenses related to expanded businesses.

We also roll forward our DCF (WACC 6.6%) valuation to include FY23e free cash flows, when we expect Chongqing to turn profitable and Shanghai to break even.

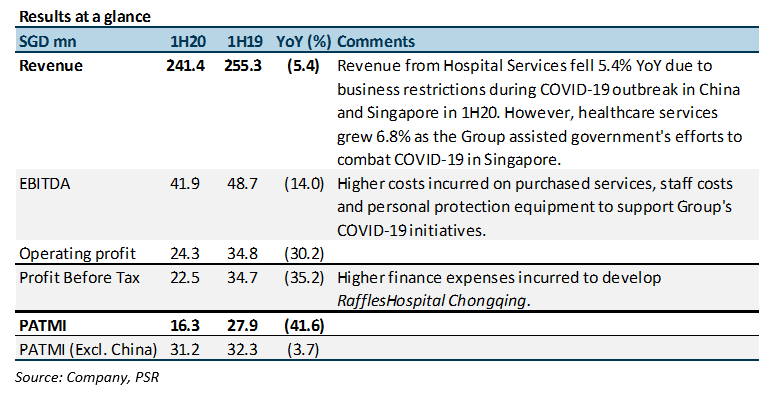

The Positives

+ Healthcare Services saw revenue grow 6.8% YoY from S$116.6mn to S$124.6mn in 1H20 as the Group rendered services to assist the government’s effort to tackle the COVID-19 pandemic, providing an alternative sources of income. These included providing air-border screening at Changi Airport, swabbing of foreign workers at the dormitories, as well as providing medical services to COVID-19 patients at the Changi Exhibition Centre-Community Care Facility.

The Negatives

- Hospital Services fell 5.4% YoY from S$148.1mn to S$126.6mn on business disruptions across China and Singapore. Initial outbreak of COVID-19 in China saw operations in China affected in 1Q20. This was followed by the 2-month Circuit Breaker in Singapore with non-essential activities (including services such as dental and health-screening) mandated to cease, hurting the Group’s business momentum in 1H20. As a result, Group revenue declined from S$255.3mn to S$241.4mn (-5.4% YoY) in 1H20.

- Operating margin was lower (1H20: 10.0% vs. 1H19: 13.6%) due to higher staff costs (+4.8% YoY) and purchased and contracted services (+24.0%). To support manpower demands from COVID-19-related projects with the government, the Group incurred higher outsourced recruitment agency costs as well as salaries from hiring of temporary staff. The increased costs were partially offset by government grants such as the Job Support Scheme (JSS), higher wage credit and property tax rebates. Nevertheless, operating profit fell 30.2% YoY to S$24.3mn (1H19: S$34.8mn).

Outlook

Gradual return to normalcy observed across operating geographies. Raffles Medical has started to observe return of patient load in 3Q20 to pre-COVID-19 levels as both China and Singapore started to ease restrictions on businesses. As cross-border travel begins to ease, Hospital Services is likely to recover, as foreign patients make up 20 to 30% of revenue in Singapore. Margins will also revert to previous levels as contribution from in-patient services pick up.

Setback to operations in China

RafflesHospitalChongqing (RHCQ) was slated to breakeven in FY21. However, the hospital saw less patient load in 1H20 with travel restrictions. As a result, the Group expects breakeven to be delayed by up to a year, prolonging gestations period and cost. RafflesHospitalShanghai is currently in the final stages of out-fitting and is expected to begin operations at end-FY20. However, this is barring further delays should the COVID-19 situation take a turn for the worse.

Maintain NEUTRAL with revised TP of S$0.94 (previous TP S$0.99).

We revise our FY20e earnings estimate downwards by 25% after considering the slowing business momentum in 1H20. However, we expect business to recover by FY21. The current shift in business dynamics does not represent the nature of the Group’s business in a steady-state environment as Hospital Services segment was depressed from business restrictions during the pandemic. We expect business momentum from Hospital Services segment to return gradually with healthier margins moving forward.

Nevertheless, the Group has maintained strong cash position and distributed 0.5 cents in interim dividends for 1H20, steady from a year ago. The Group is expected to remain profitable for the remaining of FY20.