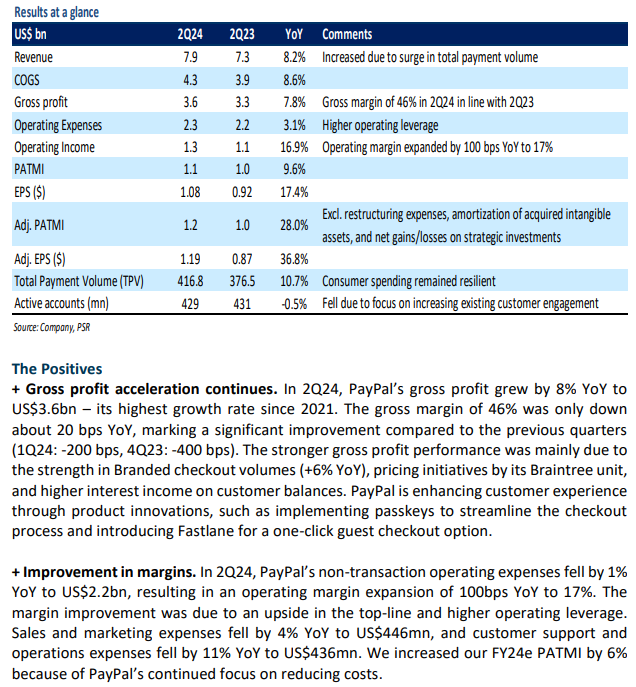

The Positives

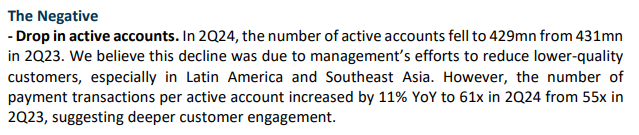

+ Payment volume and engagement trends continue to be healthy. In 1Q24, PayPal’s total revenue rose 9% YoY to US$7.7bn, which came 3% ahead of the company guidance. The upside to revenue was driven by a 14% YoY increase in total payment volume (TPV) to US$404bn as consumer spending remained resilient on its platforms. Management highlighted that branded checkout volumes grew 7% YoY (+200bps sequentially), unbranded processing volumes (Braintree) jumped 26% YoY, and Venmo volumes grew 8% YoY. Meanwhile, the number of payment transactions was up 11% YoY, while the number of payment transactions per active user rose 13% YoY to 60x in 1Q24 from 53x in 1Q23.

+ Operating margins expanded on higher operating leverage. In 1Q24, PayPal’s OPEX fell by 1% YoY to US$2.3bn, resulting in an operating margin expansion of 100bps YoY to 15%. The margin improvement was mainly due to top-line upside and higher operating leverage. Sales and marketing expenses fell by 3% YoY to US$421mn, and general and administrative expenses fell by 8% YoY to US$464mn. We expect margin contraction going forward as the company intends to reinvest its earnings into the business for continuous product enhancements.

The Negative

- Continuation of gross margin contraction. In 1Q24, the gross margin fell by 200bps YoY to 45%, though the margin contraction rate continued to slow down compared to the previous quarters (-400bps in 4Q23 and -600bps in 3Q23). The reduction is mainly due to the business-mix shift towards low-margin unbranded checkout solutions like Braintree. Unbranded processing volumes increased by 26% YoY in 1Q24 and now comprise about 37% of the total TPV (vs 33% in 1Q23).

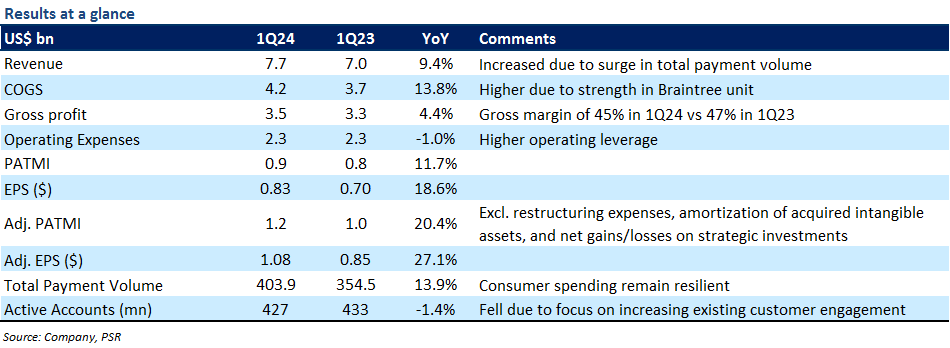

The Positives

+ Revenue beat on higher payments volume and user engagement. In 4Q23, PayPal’s total revenue rose 9% YoY to US$8.0b, which came ~2% ahead of the top end of company guidance. This was mainly driven by a 15% YoY rise in total payments volume (TPV) to US$409.8bn as consumer spending remained resilient on its platforms. PayPal’s branded checkout volumes grew 5% YoY, unbranded processing volumes (Braintree) grew 29% YoY, and Venmo volumes grew 8% YoY to US$68.9bn. Meanwhile, the number of payment transactions were up 13% YoY while the number of payment transactions per active account rose 14% YoY to 59x in 4Q23 from 51x in 4Q22.

+ Cost controls drive operating leverage. In 4Q23, PayPal’s OPEX fell by 20% YoY to US$1.9bn resulting in an operating margin of 22% (vs 17% in 4Q22). The improvement was mainly driven by cost-cutting measures including job cuts and lower sales-related costs. PayPal further plans to cut 2,500 jobs (9% of its workforce) this year to boost profitability.

The Negative

- Shrinking user base, Braintree continues to be a drag on gross margin. Active users fell by 2% YoY to 426mn as minimally engaged users continued to churn out, particularly in Latin America and Asia Pacific regions. In addition, the gross margin fell to 46% in 4Q23 from 50% in 4Q22 due to strength in its low-margin unbranded checkout solutions like Braintree. Management highlighted that unbranded processing volumes increased by 30% YoY in FY23 and now comprises about 35% of the total TPV (vs 30% in FY22).

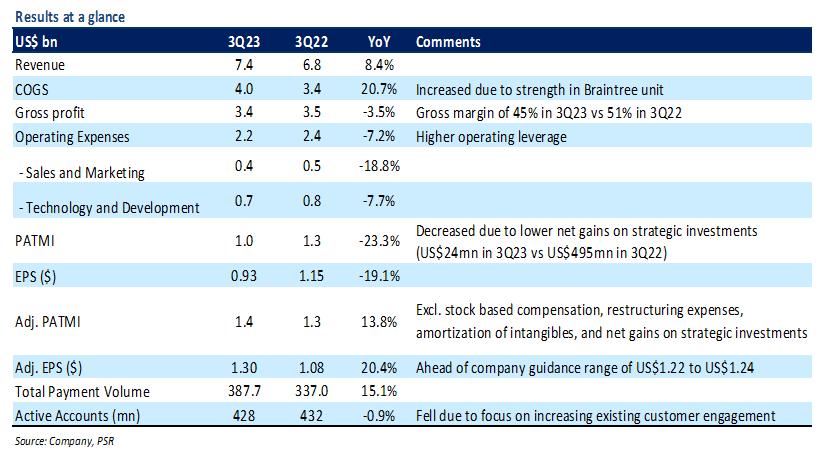

The Positives

+ Higher payment volumes. In 3Q23, PayPal’s total payment volume (TPV) surged by 15% YoY to US$388bn, driven by resilient consumer spending on its platforms (Braintree, PayPal branded checkout, and Venmo) amid moderating inflation. In 3Q23, PayPal delivered 32% YoY growth in unbranded processing volumes (Braintree), while branded checkout volumes grew by 6% YoY. Venmo’s TPV grew 7% YoY to US$68bn. We believe that the addition of Venmo as a payment option on Amazon’s check-out page will likely accelerate PayPal’s overall payment volumes.

+ Boost in transactions per active account. The number of transactions per active account rose 13% YoY to 57x in 3Q23 from 50x in 3Q22. This is a sizable increase given PayPal’s strategic decision to focus on driving higher engagement within existing active accounts instead of adding new accounts. PayPal is boosting customer engagements by adding new features like passkeys to allow frictionless payments, Tap to Pay on iPhone, and cryptocurrency buying and selling.

The Negative

- Drop in active accounts; gross margins remain under pressure. PayPal ended 3Q23 with 428mn active accounts, down 1% YoY. Management highlighted that this was mainly due to efforts to churn out lower-quality customers, particularly in Latin America and Southeast Asia. In addition, the gross margin fell to 45% in 3Q23 from 51% in 3Q22 due to strength in its lower-margin unbranded checkout solutions like Braintree.

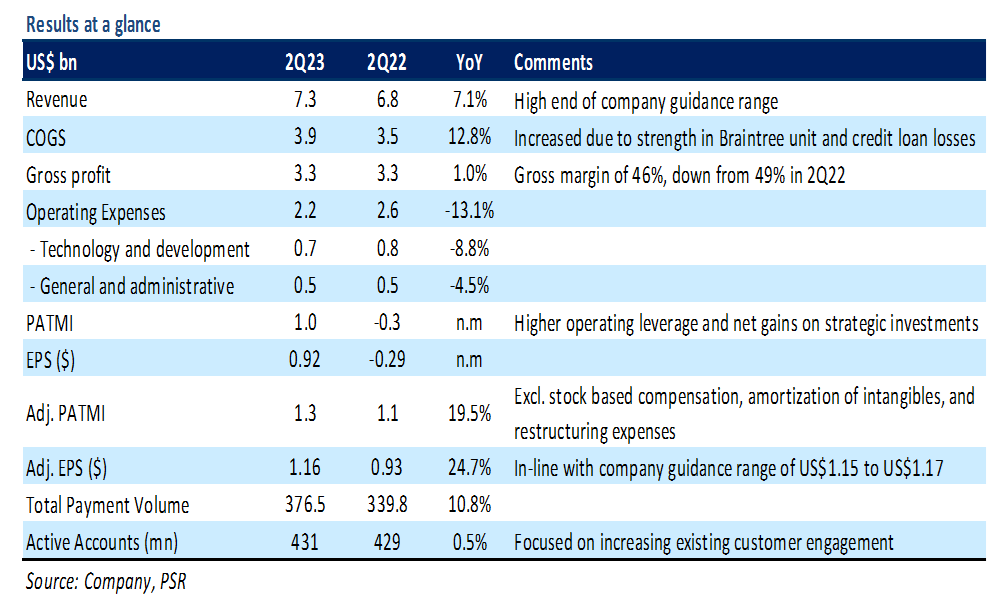

The Positives

+ Transactions per active account continued to climb. PayPal’s customer engagement as measured by the number of transactions per active user increased to 55x in2Q23 from 49x in 2Q22. The management has shifted its strategy to driving more engagement within existing users away from trying to grow active users. PayPal is boosting user engagements through new features, including Tap to Pay on iPhone, cryptocurrency buying and selling, and QR code payments. Moreover, PayPal’s Venmo (popular peer-to-peer payment platform) has been added as a payment option on Amazon’s checkout page.

+ Double-digit growth in total payment volume. In 2Q23, PayPal’s total payment volume (TPV) surged by 11% YoY to US$377bn driven by resilient consumer spending. Management highlighted that e-commerce spending is expected to grow by mid-single digits YoY in FY23e compared with its prior expectation of flat growth as there appears to be shift from travel and services to goods spending.

The Negative

- Active account growth slows, continuation of gross margin compression. In 2Q23, active accounts grew by 0.5% YoY to 431mn but decreased by 2mn sequentially due to higher churn from lower usage accounts. In addition, the gross margin fell to 46% in 2Q23 from 49% in 2Q22. The drop was mainly due to both the volume mix shift towards the lower-margin Braintree unit and higher loan provisions. In 2Q23, credit losses spiked by 65% YoY to US$112mn. Management highlighted that the company has tightened its underwriting standards for business loans offered to merchants.

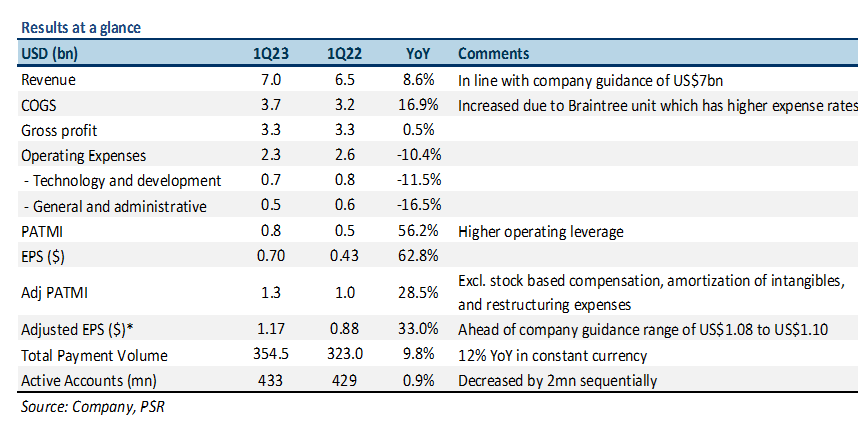

The Positives

+ Improvement in customer engagement. In 1Q23, the number of payment transactions per active account grew by 13% YoY to 53.1x on an annualized basis (up from 47x in 1Q22). PayPal is increasing customer engagement through product innovations and partnerships, including the roll-out of Venmo payment option for person-to-business (P2B) transactions on Amazon. PayPal has also partnered with Apple to allow merchants to use their iPhone as a mobile point of sale (POS) terminal without the need for any additional hardware.

+ Focused on improving profitability. In 1Q23, PayPal’s non-transaction expenses (general and administrative, and technology) fell by 10% YoY due to cost controls resulting in adj. operating margin of 23% (vs. 21% in 1Q22). For FY23e, PayPal has outlined a total of US$1.9bn in cost cuts, mostly through job cuts and real estate consolidation. In 1Q23, PayPal laid off 2,000 employees (7% of its workforce) citing challenging macro-economic environment.

The Negative

- Active accounts decline sequentially. In 1Q23, active accounts grew by 1% YoY to 433mn but decreased by 2mn compared with 4Q22. The drop was mainly driven by higher churn from lower usage accounts and the management’s decision to focus on driving more engagement with existing customers. Notably, PayPal indicated that it expects no net new additions in FY23e during 4Q22 earnings call.

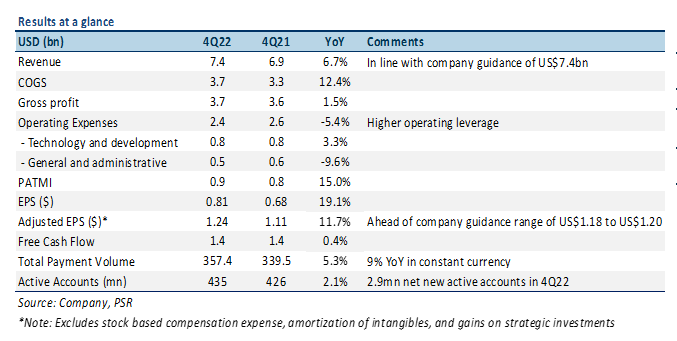

The Positives

+ Customer engagement continues to climb. In 4Q22, customer engagement improved, with the number of payment transactions per active account up by 13% YoY to 51.4x on an annualized basis. This is a sizable increase given PayPal’s intent to shift away from adding new accounts and toward more engagement with existing users. The rolling out of Venmo payment option for person-to-business (P2B) transactions on Amazon could accelerate this engagement.

+ Focused on improving operating margin. In 4Q22, PayPal’s operating expenses fell by 5% YoY due to cost controls (job cuts and real estate consolidation) resulting in adj. operating margin of 22.9% (vs. 21.8% in 4Q21). Management noted that the company has exceeded its US$900mn cost-savings target for FY22. In addition, the company has identified US$600mn of additional cost synergies for FY23e, on top of the previously announced US$1.3bn. This includes recently-announced layoffs of 2,000 employees (7% of its workforce).

The Negative

- Slowdown in TPV growth. In 4Q22, PayPal’s total payment volume (TPV) grew 5% YoY (9% YoY in constant currency) to US$357.4bn. The growth rate decelerated significantly from 23% in 4Q21 mainly due to weak trends in global e-commerce and cuts to consumer discretionary spending amid inflationary pressures.

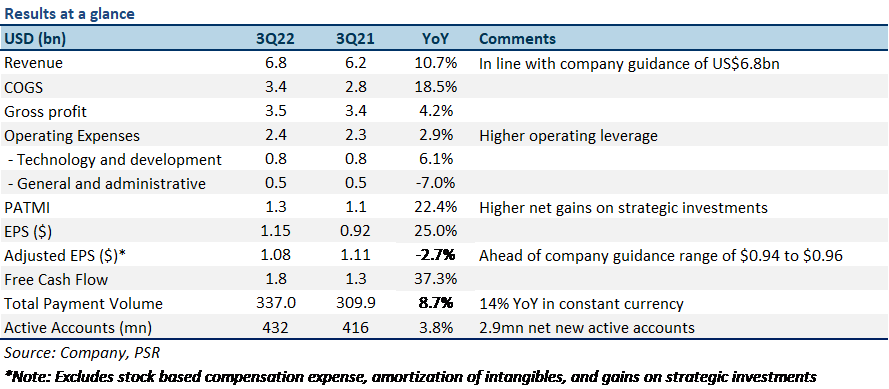

The Positives

+ Rising customer engagement. In 3Q22, PayPal gained traction in its effort to boost user engagement as average transactions per active account grew 13% YoY to 50.1x on an annualized basis. This is a sizable increase as the company is now focusing more on driving user engagement rather than adding more customers. PayPal added 2.9mn net new active accounts in 3Q22, taking its total to 432mn.

+ Cost saving initiatives boost profitability. In 3Q22, total expenses grew just 11.5% YoY, and were 5.2% lower sequentially. PayPal is on track to cut costs by US$900mn in FY22e and US$1.3bn in FY23e, across transaction and operating expenses. The company plans to reduce expenses through job cuts and real estate consolidation. The cost-cutting measures began in 3Q22 and are expected to ramp up in 4Q22e. Cost savings are expected to boost adj. operating margin to 22.5% in 4Q22e from 21.8% in 4Q21.

+ New strategic initiatives to support growth. PayPal is working with Apple on several new strategic initiatives that could benefit PayPal and Venmo merchants and consumers. PayPal will leverage Apple’s Tap to Pay on iPhone functionality for the U.S. merchants to accept contactless debit or credit card payments using an iPhone and the PayPal or Venmo iOS application. Apple Pay will also be added as a payment option in PayPal's checkout flows. Additionally, online retailer Amazon has agreed to accept Venmo payments on its platform. The payment option is likely to be available for all U.S. Amazon customers in time for the peak holiday season.

The Negative

- Decelerating growth in TPV. In 3Q22, PayPal’s total payment volume (TPV) grew 9% YoY (14% YoY in constant currency) to US$337bn. The growth rate decelerated significantly from 26% in 3Q21. PayPal expects that slowdown to continue in 4Q22 with just 8.5% TPV growth. The soft guidance reflects continued weakening trends in e-commerce, and an uncertain macroeconomic environment.

Outlook

For 4Q22e, PayPal expects total revenue to grow 7% YoY (9% YoY in constant currency) to US$7.4bn (Figure 1). The management attributes the soft revenue guidance to the slowing e-commerce market and early indications that low/middle-income level consumers are cutting back on their discretionary spending. Additionally, PayPal isn’t witnessing signs of an early start to the holiday season as occurred last year. PayPal expects to add 2.3mn to 4.3mn net new active accounts (implied).

For FY23e, PayPal expects e-commerce growth to remain under pressure but highlighted its confidence to deliver 100bps of adj. operating margin improvement and to grow adj. EPS by at least 15% YoY. This is mainly because non-transactional operating expenses are expected to remain flat or fall slightly YoY.

Company Background

Spun off from eBay in July 2015, PayPal Holdings Inc (PYPL) is a global provider of digital and mobile payment solutions. The company’s two-sided platform serves nearly 426mn active accounts in over 200 markets. Its payment solutions include PayPal, Venmo, Xoom and Honey. PayPal generates nearly 90% of its total revenues from transaction revenues.

Investment Merits

We initiate coverage with a BUY rating. Our target price is US$116 based on a DCF valuation with a WACC of 7.0% and terminal growth of 4.0%.

REVENUE

PayPal has two revenue segments: Transaction revenues (92% of FY21 revenues) and revenues from other value-added services (8%). Transaction revenues are generated from fees charged to consumers and merchants based on the total payments volume (TPV). Other value-added services include revenue from subscription fees, partnerships, referral fees, and interest earned on loan receivables or certain customer balances.

Total revenue expanded at 18% CAGR in the past four years (Figure 1) to US$25.4bn in FY21.

Over FY18-21, PayPal’s TPV rose at a CAGR of 29% to US$1.3tn in FY21 (Figure 2). The growth was mainly driven by the number of active users, merchant acceptance, and the secular shift towards digital payments and e-commerce. PayPal generates revenues from operations in several regions, primarily the US (54% of FY21 revenues) and the UK (9%) (Figure 3).